Reports

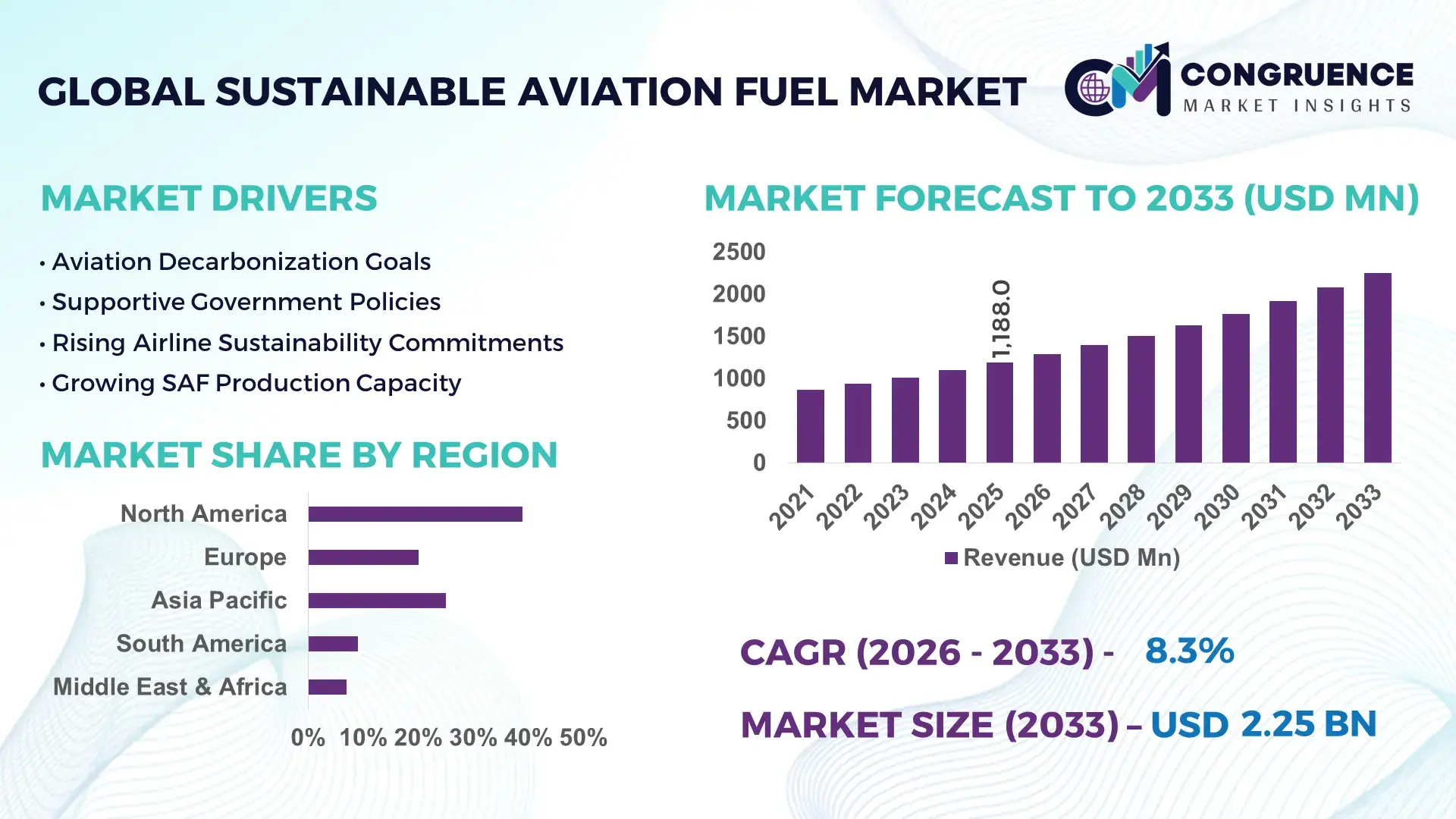

The Global Sustainable Aviation Fuel Market was valued at USD 1188 Million in 2025 and is anticipated to reach a value of USD 2248.24 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033.

Rising airline decarbonization mandates, expanding HEFA and alcohol-to-jet production capacity, and stricter carbon reduction frameworks across North America and Europe are accelerating long-term procurement agreements and refinery conversions in the global sustainable aviation fuel ecosystem.

The United States dominates the Sustainable Aviation Fuel Market with nearly 38% of global production capacity in 2026, supported by refinery expansion projects, federal tax incentives, and strong airline procurement activity across commercial and defense aviation segments. The country operates over 15 large-scale SAF production initiatives, while Singapore and the Netherlands continue strengthening Asia-Europe supply corridors through advanced biofuel logistics infrastructure. Compared to Germany’s slower feedstock scaling pace, the U.S. recorded over 22% higher SAF blending deployment across major international airports, driven by aviation fuel security concerns following Red Sea shipping disruptions and tightening international emissions frameworks.

Strategic alignment between fuel producers, airport operators, and airlines is becoming critical for securing feedstock access, stabilizing long-term supply contracts, and protecting competitive positioning in the high-growth aviation decarbonization landscape.

Market Size & Growth: USD 1188 Million in 2025 to USD 2248.24 Million by 2033 at 8.3% growth, driven by refinery conversion projects and commercial airline decarbonization targets.

Top Growth Drivers: Carbon emission reduction mandates increased 31%, SAF blending targets expanded 28%, and airline sustainability procurement rose 24% globally.

Short-Term Forecast: By 2028, advanced SAF processing technologies reduce production costs by 18% while improving refinery throughput efficiency by 14%.

Emerging Technologies: AI-enabled refinery optimization, alcohol-to-jet conversion, and waste-based feedstock automation improve operational yield by nearly 21%.

Regional Leaders: North America exceeds USD 840 Million with strong airline partnerships, Europe crosses USD 620 Million through regulatory adoption, and Asia-Pacific surpasses USD 410 Million from airport infrastructure expansion.

Consumer/End-User Trends: More than 46% of international airlines integrated SAF blending agreements into long-haul operations by 2026.

Pilot/Case Example: In 2026, a large-scale airport SAF deployment program reduced lifecycle aviation emissions by 63% across regional commercial fleets.

Competitive Landscape: Leading producers control approximately 42% market share, with major competition centered on feedstock integration and supply scalability among global energy and aviation firms.

Regulatory & ESG Impact: European aviation carbon compliance programs increased SAF procurement commitments by 35% following stricter emissions benchmarks.

Investment & Funding: Global SAF infrastructure and refinery investments exceeded USD 16 Billion, led by strategic partnerships and cross-border supply-chain expansion initiatives.

Innovation & Future Outlook: Synthetic e-fuels, carbon capture integration, and advanced biomass conversion are reshaping next-generation aviation fuel commercialization strategies.

The Sustainable Aviation Fuel Market is gaining momentum across commercial aviation, cargo transport, and defense aviation segments as airlines prioritize lower-emission fuel integration within global fleet modernization programs. Advanced feedstock conversion technologies improved fuel yield efficiency by nearly 19% in 2026, while waste-to-fuel partnerships strengthened regional supply reliability. Expanding airport blending infrastructure and tighter international aviation emissions frameworks are also accelerating long-term procurement strategies, creating a strong foundation for the next phase of strategic market expansion.

Sustainable aviation fuel is becoming a strategic priority across the aviation value chain as airlines, fuel producers, and airport operators compete to secure long-term low-emission fuel access and regulatory compliance capacity. The market is reshaping aviation procurement models through refinery retrofits, feedstock localization, and integrated supply-chain agreements. In 2026, several international carriers increased multi-year SAF offtake contracts by over 30% to reduce exposure to carbon pricing frameworks and volatile fossil fuel logistics following continued maritime trade disruptions across key shipping corridors.

Advanced alcohol-to-jet and Fischer–Tropsch conversion technologies are improving lifecycle emissions reduction by nearly 65% compared to conventional jet fuel systems while lowering processing waste by approximately 18% versus legacy hydroprocessed pathways. The United States continues leading commercial-scale deployment through integrated refinery infrastructure, whereas Japan is focusing on municipal waste-based SAF innovation with tighter urban feedstock utilization models. Over the next two years, airport blending infrastructure installations are expected to expand by more than 25% across high-traffic international aviation hubs.

Large energy companies and airline alliances are accelerating joint ventures to secure feedstock availability and optimize regional distribution economics. A 2026 airport deployment program in Singapore demonstrated improved fuel supply reliability through digital fuel-tracking integration and centralized blending operations. Companies prioritizing scalable feedstock ecosystems, long-term procurement contracts, and infrastructure modernization are strengthening operational resilience and securing competitive advantage within the evolving aviation decarbonization framework.

Global aviation decarbonization mandates and refinery transformation projects are accelerating sustainable aviation fuel deployment across commercial aviation networks. More than 42% of large international airlines expanded SAF procurement agreements in 2026, while refinery conversion investments increased by nearly 27% across the United States and Northern Europe. Stricter emissions frameworks and airport-level carbon reduction targets are forcing carriers to integrate low-emission fuel strategies into long-haul operations. In response, energy companies are converting conventional refining assets into multi-feedstock SAF facilities to improve production flexibility and reduce operational dependency on crude-based aviation fuels. Singapore and the Netherlands strengthened strategic aviation fuel logistics corridors through port-linked storage and blending infrastructure, enabling faster supply integration. Companies securing early feedstock partnerships and airport distribution access are gaining stronger operational leverage in long-term aviation fuel contracting negotiations.

Limited feedstock availability and elevated production economics remain major structural restraints for large-scale sustainable aviation fuel commercialization. Used cooking oil and agricultural residue supply costs increased by approximately 19% in 2026 due to tightening global biofuel demand and cross-sector competition from renewable diesel producers. In Germany and South Korea, SAF production utilization rates remained below 68% because of inconsistent waste-feedstock aggregation and fragmented collection infrastructure. These constraints directly affect production scalability, airline procurement consistency, and long-term pricing stability for international carriers. Airlines operating on thin-margin regional routes continue facing operational pressure as SAF blending raises fuel expenditure levels by nearly 14% compared to conventional jet fuel sourcing models. To reduce exposure, companies are diversifying feedstock procurement through municipal waste contracts, algae-based fuel trials, and localized agricultural partnerships to improve supply security and stabilize long-term production economics.

Synthetic e-fuels and digitally optimized production systems are creating high-value expansion opportunities within the sustainable aviation fuel ecosystem. Advanced carbon capture-linked SAF technologies improved fuel conversion efficiency by nearly 22% in pilot-scale operations during 2026, while AI-driven refinery monitoring reduced operational downtime by approximately 16%. Japan and the United Arab Emirates are accelerating investment in green hydrogen-linked aviation fuel infrastructure to strengthen future export positioning and industrial energy diversification strategies. Emerging airport fuel management platforms are also enabling real-time blending verification and emissions tracking, improving regulatory reporting accuracy for global airline operators. Energy firms and aviation groups are increasing joint R&D partnerships focused on scalable synthetic fuel commercialization and feedstock-independent production systems. Companies capable of integrating digital operations with diversified low-carbon fuel technologies are positioning themselves for stronger long-term margin optimization and cross-border aviation supply leadership.

Long-term market expansion is increasingly constrained by aviation fuel distribution complexity, storage compatibility limitations, and uneven infrastructure readiness across global airport networks. Nearly 34% of secondary international airports still lack dedicated SAF blending and storage systems in 2026, creating deployment inconsistency across regional aviation routes. In India and Brazil, fragmented transport logistics and limited pipeline connectivity continue slowing commercial-scale fuel distribution despite rising airline procurement commitments. The challenge extends beyond production capacity, as inconsistent certification protocols and airport handling standards increase operational coordination costs for fuel suppliers and carriers. Several airlines also reported fuel scheduling inefficiencies exceeding 11% due to fragmented multi-airport supply management systems. Companies must accelerate investment in integrated storage terminals, digital logistics coordination platforms, and standardized airport fueling frameworks to maintain deployment consistency and protect long-term operational competitiveness in the global sustainable aviation fuel market.

Advanced Feedstock Diversification Expands Feedstock procurement strategies are shifting beyond used cooking oil toward agricultural residue, municipal waste, and algae-derived inputs to reduce supply volatility and improve production continuity. In 2026, multi-feedstock processing adoption increased by 29%, while waste-based SAF integration improved refinery utilization rates by 17%. Following tightening biofuel import restrictions in parts of Europe, companies in the United States and Singapore accelerated localized feedstock aggregation partnerships and long-term municipal sourcing contracts to stabilize operational throughput and reduce logistics dependency.

Airport Blending Infrastructure Accelerates International airports are rapidly expanding dedicated SAF blending and storage systems to support commercial-scale deployment across long-haul aviation routes. More than 33% of high-traffic airports upgraded digital fuel management systems in 2026, reducing fuel scheduling delays by 14% and improving supply traceability efficiency by 21%. Japan and the United Arab Emirates increased airport-linked infrastructure investments following stricter aviation emissions compliance standards, while airlines strengthened integrated procurement partnerships to secure guaranteed low-emission fuel allocation across strategic flight corridors.

Synthetic Fuel Programs Scale Faster Synthetic aviation fuel commercialization is advancing through green hydrogen integration and carbon-capture-linked production models. Pilot-scale e-fuel conversion efficiency improved by nearly 24% during 2026, while automated refining systems reduced energy consumption by 13% compared to conventional SAF processing lines. Germany and Norway expanded industrial partnerships focused on synthetic fuel scalability to reduce long-term feedstock dependency risks. Companies are restructuring R&D portfolios toward modular production systems that support faster deployment across decentralized aviation fuel networks.

Digital Fuel Tracking Intensifies Aviation fuel suppliers and airline operators are increasingly deploying blockchain-enabled fuel verification and AI-driven logistics monitoring platforms to improve emissions accountability and operational coordination. Digital compliance integration increased by 31% across major airline procurement systems in 2026, helping reduce manual reporting workloads by 18%. Continued geopolitical shipping disruptions and tightening carbon disclosure requirements pushed companies in South Korea and the Netherlands to automate fuel certification workflows, improving contract transparency and accelerating multi-airport SAF distribution management.

HEFA Fuel remains the leading segment in the Sustainable Aviation Fuel Market due to its mature refining compatibility, established feedstock ecosystem, and immediate integration capability within existing aviation infrastructure. In 2026, HEFA-based fuel accounted for nearly 46% of global SAF deployment volume, supported by large-scale refinery conversions in the United States and Finland. Compared to Hydrogen-Based Fuel and Synthetic Fuel systems, HEFA processing delivers nearly 18% lower operational adaptation costs for airlines and airport fuel operators. Companies are expanding HEFA production capacity through long-term feedstock procurement agreements and integrated refinery modernization projects to secure stable commercial aviation supply.

Synthetic Fuel is emerging as the fastest-growing segment as energy companies prioritize feedstock-independent production systems and green hydrogen integration. Pilot-scale synthetic fuel efficiency improved by approximately 22% in 2026, particularly across Germany and Japan. Alcohol-to-Jet Fuel is also gaining momentum through agricultural waste conversion partnerships, while Biofuel-Based and Hydrogen-Based Fuel segments remain strategically relevant for regional decarbonization frameworks and defense aviation trials. Companies are increasingly diversifying technology portfolios to balance near-term deployment scalability with long-term emissions optimization and supply resilience.

Commercial Aviation dominates the Sustainable Aviation Fuel Market as international airlines accelerate emissions reduction strategies and expand low-emission fuel procurement across long-haul fleets. In 2026, commercial carriers represented nearly 58% of SAF consumption volume, supported by mandatory emissions compliance frameworks and airport blending infrastructure upgrades. Large airline operators improved SAF integration across premium international routes by approximately 27%, particularly in the United States and Singapore. Companies are prioritizing multi-year procurement agreements, fuel logistics optimization, and integrated digital fuel tracking systems to stabilize supply continuity and improve operational sustainability performance.

Cargo Aviation is emerging as the fastest-growing application segment due to rising pressure from global logistics operators to reduce transport emissions across international freight corridors. Cargo fleet SAF utilization increased by nearly 24% during 2026 as e-commerce distribution networks expanded low-emission shipping programs. Military Aviation continues investing in strategic fuel diversification for operational resilience, while Business Jets and Regional Aviation are gradually adopting SAF through premium sustainability initiatives and localized airport partnerships. Airlines and fuel suppliers are increasingly customizing deployment strategies based on route economics, fleet utilization intensity, and airport infrastructure readiness.

Airlines remain the dominant end-user group in the Sustainable Aviation Fuel Market due to large-scale fuel consumption intensity, international compliance obligations, and direct exposure to aviation emissions frameworks. In 2026, airlines accounted for approximately 52% of SAF procurement activity, with major carriers increasing long-term supply agreements by nearly 34% to secure operational fuel stability. Airlines in the United States and the Netherlands accelerated integrated procurement partnerships with refinery operators and airport fuel distributors to improve supply reliability and reduce exposure to carbon pricing volatility. Companies are also deploying AI-enabled fuel optimization systems to improve blending efficiency and route-level emissions management.

Airport Operators are emerging as the fastest-growing end-user segment as infrastructure modernization becomes operationally critical for SAF deployment consistency. Airport-linked storage and blending investments increased by approximately 26% in 2026, particularly across Singapore and the United Arab Emirates. Aviation Fuel Suppliers continue strengthening feedstock integration capabilities, while Cargo Operators and Defense Sector buyers are expanding SAF procurement for logistics resilience and fuel diversification strategies. Aircraft Manufacturers are supporting adoption through engine certification advancements and compatibility testing programs that accelerate commercial-scale deployment confidence.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Refinery Conversion and Airline Procurement Expansion

North America maintains leadership in the Sustainable Aviation Fuel Market through large-scale refinery retrofits, integrated airport fuel infrastructure, and aggressive airline procurement strategies. The region contributed nearly 41% of global SAF production capacity in 2026, supported by strong feedstock aggregation networks across the United States and Canada. Major aviation corridors expanded SAF blending integration by approximately 28% during the year, while long-term fuel supply partnerships accelerated deployment consistency across commercial fleets. Companies are prioritizing multi-feedstock processing systems and digital fuel-tracking platforms to optimize operational efficiency and emissions compliance. Increasing collaboration between energy producers, airport operators, and airline alliances is strengthening regional supply resilience and reducing dependence on imported low-emission aviation fuel infrastructure.

United States Market Outlook: The United States remains the operational center of North America’s SAF ecosystem due to extensive refining infrastructure, federal low-carbon fuel incentives, and high airline procurement concentration. More than 15 large-scale SAF production projects remained active in 2026, with refinery conversion activity increasing by nearly 24%. Major airport hubs in California and Texas accelerated dedicated SAF storage and blending modernization programs, while airlines expanded long-term procurement agreements to stabilize future fuel allocation and reduce carbon compliance exposure across international flight networks.

Carbon Compliance and Circular Feedstock Integration

Europe is strengthening its Sustainable Aviation Fuel Market position through aggressive emissions regulation, advanced waste-based fuel processing, and airport-level decarbonization frameworks. The region represented approximately 31% of global SAF deployment activity in 2026, with strong concentration across the Netherlands, Germany, and Nordic aviation corridors. SAF blending mandates pushed fuel procurement activity up by nearly 26% among major European carriers, while municipal waste integration improved regional feedstock utilization efficiency. Energy firms are expanding refinery modernization and cross-border fuel logistics partnerships to secure long-term aviation supply stability. Continued pressure from aviation carbon reduction frameworks is also accelerating adoption of digital compliance monitoring and certified emissions tracking systems across international airport operations.

Netherlands Market Outlook: The Netherlands continues leading Europe’s SAF commercialization strategy through advanced port logistics, integrated refinery infrastructure, and high-volume international aviation traffic. Rotterdam-based fuel logistics networks strengthened SAF import-export coordination in 2026, while airport-linked blending operations improved fuel distribution efficiency by approximately 19%. Dutch aviation stakeholders are also investing heavily in synthetic fuel pilot systems and digital emissions verification technologies to strengthen long-term competitiveness within Europe’s tightening low-carbon aviation ecosystem.

Airport Infrastructure and Production Scale Acceleration

Asia-Pacific is rapidly emerging as the fastest-scaling Sustainable Aviation Fuel Market due to expanding airport infrastructure, rising airline emissions targets, and accelerating industrial fuel diversification programs. The region accounted for nearly 24% of global SAF deployment activity in 2026, supported by infrastructure expansion across Singapore, Japan, South Korea, and Australia. International airport blending capacity increased by approximately 32% during the year, while regional airlines strengthened multi-year SAF procurement partnerships to secure future operational continuity. Companies are prioritizing localized feedstock processing and integrated airport storage modernization to reduce import dependency and improve distribution efficiency across high-density aviation routes.

Singapore Market Outlook: Singapore has become a strategic SAF distribution and blending hub within Asia-Pacific due to its advanced airport infrastructure, integrated refining ecosystem, and maritime logistics connectivity. In 2026, airport-linked SAF handling capacity expanded by nearly 27% as aviation operators accelerated low-emission fuel integration across international transit routes. The country is also strengthening digital fuel-tracking deployment and regional supply-chain coordination programs to improve aviation fuel traceability, operational resilience, and long-term export positioning within Asia’s expanding sustainable aviation network.

Biofeedstock Utilization and Export Positioning

South America is strengthening its Sustainable Aviation Fuel Market presence through agricultural feedstock availability, biofuel expertise, and expanding aviation decarbonization initiatives. The region contributed nearly 9% of global SAF feedstock supply activity in 2026, with Brazil leading production-oriented investment programs. Regional airlines increased SAF integration trials by approximately 18%, while fuel producers accelerated partnerships focused on sugarcane residue and agricultural waste conversion technologies. Infrastructure constraints and fragmented fuel logistics networks continue limiting rapid commercial-scale deployment across secondary aviation corridors. However, companies are increasingly targeting export-oriented SAF production models to leverage regional feedstock cost advantages and strengthen participation within international low-carbon fuel supply chains.

Brazil Market Outlook: Brazil remains the dominant SAF growth engine in South America due to its large agricultural feedstock base, established biofuel ecosystem, and expanding refinery adaptation initiatives. In 2026, industrial biofeedstock processing capacity linked to aviation fuel applications increased by nearly 21%. National aviation and energy companies are strengthening partnerships focused on ethanol-to-jet conversion systems and localized fuel supply infrastructure to improve commercial aviation deployment readiness and expand Brazil’s position within global sustainable fuel export markets.

Energy Diversification and Aviation Infrastructure Modernization

The Middle East & Africa Sustainable Aviation Fuel Market is advancing through aviation infrastructure modernization, energy diversification programs, and large-scale airport expansion initiatives. The region represented approximately 7% of global SAF deployment activity in 2026, with strong investment concentration in the United Arab Emirates and Saudi Arabia. International airport modernization programs increased dedicated low-emission fuel handling capacity by nearly 23%, while regional aviation operators accelerated partnerships focused on synthetic fuel and green hydrogen integration. Energy companies are leveraging existing refining expertise and export infrastructure to position the region as a future aviation fuel supply hub connecting Europe and Asia through strategic transit corridors.

United Arab Emirates Market Outlook: The United Arab Emirates is strengthening its position as the region’s leading SAF innovation and aviation infrastructure center through integrated airport expansion, advanced refinery capabilities, and green fuel investment programs. In 2026, airport-linked sustainable fuel infrastructure projects expanded by approximately 25%, supported by strategic airline and energy-sector collaborations. National aviation stakeholders are also accelerating synthetic fuel pilot deployments and hydrogen-linked SAF research initiatives to enhance long-term aviation fuel competitiveness and support international decarbonization commitments.

The Sustainable Aviation Fuel Market is led by integrated energy producers, aviation fuel innovators, and refinery conversion specialists competing across technology scalability, feedstock control, and long-term airline supply agreements. Neste, World Energy, TotalEnergies, Gevo, and LanzaJet collectively control nearly 48% of commercial SAF deployment capacity, while regional biofuel producers compete aggressively on localized feedstock economics and distribution access. Global leaders are competing with emerging synthetic fuel developers through process efficiency improvements exceeding 20% and logistics optimization reducing operational handling costs by nearly 14%. Companies are accelerating vertical integration strategies, refinery modernization, airport fuel partnerships, and multi-feedstock expansion programs to secure procurement contracts with international airlines. Competition is shifting toward synthetic fuel commercialization and feedstock diversification as conventional waste-oil supply tightens across North America and Europe. High infrastructure investment requirements, certification complexity, and long-term fuel supply commitments remain major entry barriers. Winning increasingly depends on scalable production, integrated logistics, and secured feedstock ecosystems.

Neste

World Energy

TotalEnergies

Gevo

LanzaJet

Fulcrum BioEnergy

SkyNRG

Honeywell UOP

Velocys

Shell

BP

Aemetis

OMV

Repsol

HEFA processing technology remains the dominant production pathway in the Sustainable Aviation Fuel Market due to refinery compatibility and immediate deployment capability across existing aviation infrastructure. In 2026, nearly 46% of commercial SAF output relied on HEFA systems, while advanced process automation improved refining efficiency by approximately 17%. Compared to legacy fossil jet fuel production models, modern HEFA integration reduced lifecycle carbon intensity by up to 75% without requiring aircraft engine modification. Large energy producers are strengthening multi-feedstock processing capabilities to stabilize production economics and improve operational flexibility across high-volume airport supply networks.

Emerging alcohol-to-jet and Fischer–Tropsch conversion technologies are accelerating next-generation SAF commercialization through waste-based and biomass-derived feedstock integration. Alcohol-to-jet conversion efficiency improved by nearly 21% during 2026 pilot deployments, while AI-driven refinery monitoring reduced operational downtime by approximately 14%. Japan, the United States, and the Netherlands are expanding digital refinery partnerships and automated fuel certification systems to improve supply traceability, blending precision, and regulatory compliance efficiency.

Disruptive synthetic e-fuel technologies linked with green hydrogen and carbon capture systems are reshaping long-term aviation fuel competitiveness between 2026 and 2028. Companies advancing scalable synthetic fuel ecosystems and integrated airport logistics infrastructure will secure stronger procurement positioning as airlines prioritize resilient, low-emission fuel supply chains.

January 2024 – LanzaJet launched Freedom Pines Fuels in Georgia, the world’s first commercial ethanol-to-SAF facility, capable of producing 9 million gallons of SAF annually. The project strengthened large-scale alcohol-to-jet commercialization and accelerated low-carbon aviation fuel deployment. Source: LanzaJet

July 2024 – Airbus announced a strategic investment in LanzaJet to accelerate scaling of proprietary SAF technology platforms and global production partnerships. The collaboration expanded industry-backed commercialization efforts and strengthened technology deployment across international aviation fuel networks. Source: LanzaJet

July 2025 – Neste signed one of Asia’s largest air cargo SAF agreements with DHL Express at Singapore Changi Airport, supplying 7,400 tons of SAF between 2025 and 2026. The partnership strengthened cargo aviation decarbonization and improved long-haul low-emission fuel adoption. Source: Neste

September 2025 – TotalEnergies began SAF production at the La Mède biorefinery in France with annual output reaching 15,000 tons using waste oils and animal fats. The development improved localized airport fuel supply resilience and strengthened European SAF infrastructure integration. Source: TotalEnergies Aviation

The Sustainable Aviation Fuel Market report provides comprehensive analysis across production technologies, operational deployment patterns, end-user demand shifts, and infrastructure modernization trends shaping the aviation decarbonization ecosystem between 2026 and 2033. The study evaluates key fuel categories including HEFA Fuel, Synthetic Fuel, Alcohol-to-Jet Fuel, Hydrogen-Based Fuel, and Biofuel-Based systems across commercial aviation, cargo aviation, military aviation, business jets, and regional aviation applications. More than 40% of assessed deployment activity is concentrated around integrated airport blending infrastructure and refinery conversion programs.

The report further examines strategic developments across airlines, airport operators, fuel suppliers, defense organizations, and aircraft manufacturers, highlighting procurement behavior, supply-chain restructuring, and emerging technology adoption trends. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed focus on industrial hubs, airport modernization, feedstock diversification, and synthetic fuel innovation. The study supports competitive benchmarking, expansion planning, infrastructure investment prioritization, and long-term aviation fuel ecosystem positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1188 Million |

|

Market Revenue in 2033 |

USD 2248.24 Million |

|

CAGR (2026 - 2033) |

8.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Neste, World Energy, TotalEnergies, Gevo, LanzaJet, Fulcrum BioEnergy, SkyNRG, Honeywell UOP, Velocys, Shell, BP, Aemetis, OMV, Repsol |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |