Reports

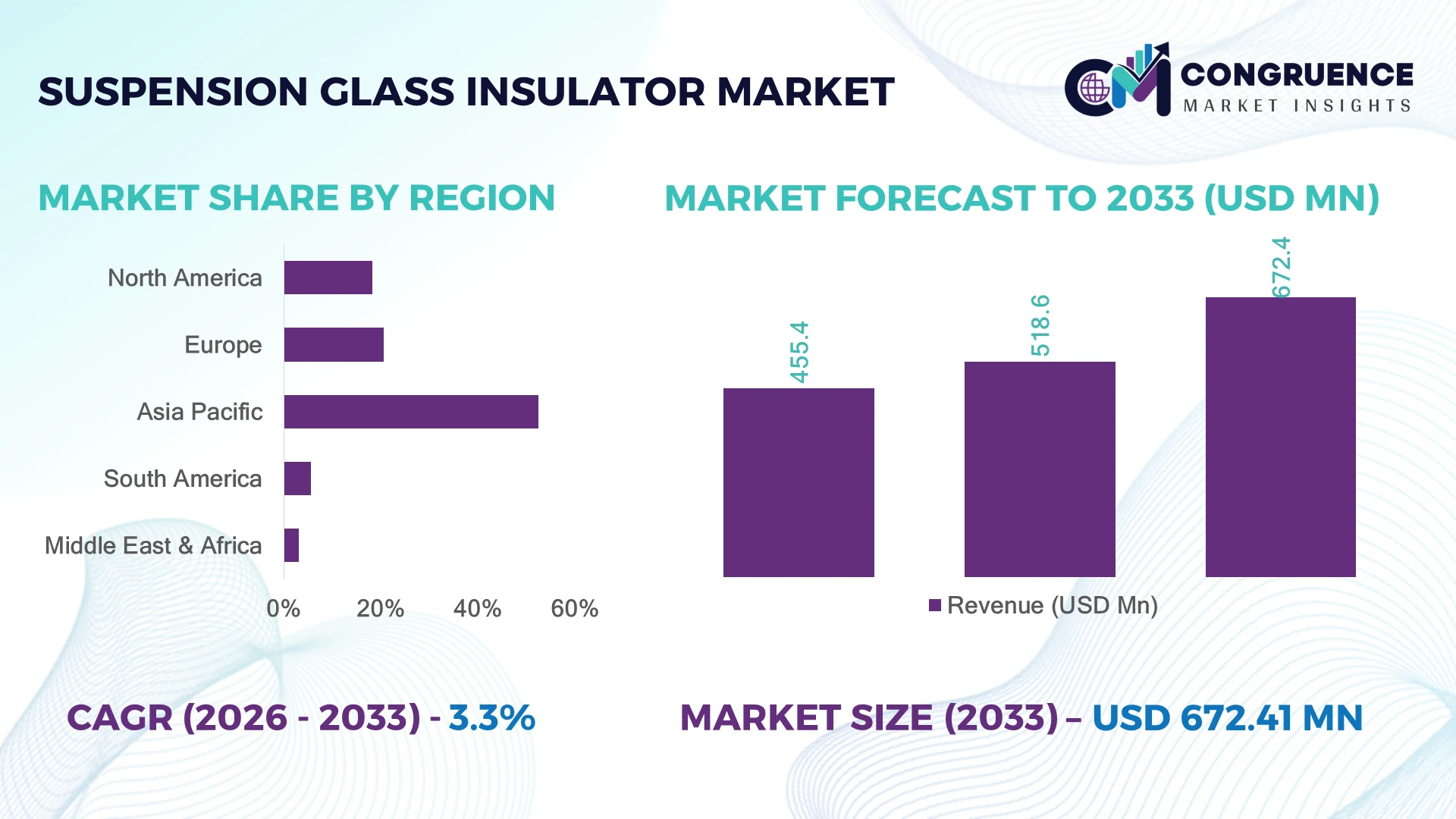

The Global Suspension Glass Insulator Market was valued at USD 518.6 Million in 2025 and is anticipated to reach a value of USD 672.4 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. Grid modernization programs, ultra-high-voltage transmission expansion, and replacement of aging power infrastructure are accelerating demand for advanced suspension glass insulators with higher mechanical strength and longer service life.

China dominates the global Suspension Glass Insulator Market with an estimated 42% production share, supported by large-scale transmission expansion, State Grid investments, and a mature electrical equipment manufacturing base. India is rapidly increasing deployment through nationwide transmission upgrades, while China maintains nearly 2.5× higher manufacturing capacity. Ongoing energy transition initiatives and cross-border grid interconnection projects further reinforce Asia-Pacific's leadership in high-voltage insulation technologies.

The market favors manufacturers expanding regional production, investing in advanced glass processing, and strengthening utility partnerships to secure long-term infrastructure contracts.

Market Size & Growth: USD 518.6 Million in 2025, reaching USD 672.4 Million by 2033 at 3.3% CAGR, driven by global transmission grid modernization and high-voltage infrastructure expansion.

Top Growth Drivers: Utility transmission investments (+18%), renewable grid integration (+22%), and replacement of aging transmission assets (+16%) support sustained demand.

Short-Term Forecast: By 2028, automated production and optimized quality inspection improve manufacturing efficiency by approximately 12% while reducing defect rates.

Emerging Technologies: AI-enabled quality inspection, automated tempering systems, and advanced glass strengthening improve consistency and production throughput.

Regional Leaders: Asia-Pacific (~USD 305 Million), Europe (~USD 126 Million), and North America (~USD 98 Million) benefit from renewable integration and transmission expansion.

Consumer/End-User Trends: More than 60% of new extra-high-voltage transmission projects increasingly specify high-performance glass suspension insulators.

Pilot/Case Example: In 2024, utility transmission modernization projects reported nearly 15% lower maintenance requirements using upgraded glass insulator strings.

Competitive Landscape: Leading manufacturers collectively control about 45% of the market, including Sediver, NGK Insulators, MacLean Power Systems, Seves Group, and Modern Insulators.

Regulatory & ESG Impact: Grid reliability standards and recyclable glass materials help reduce maintenance-related waste by approximately 10% across utility networks.

Investment & Funding: More than USD 850 Million has supported transmission equipment expansion through utility investments, manufacturing upgrades, and strategic partnerships amid global supply-chain diversification.

Innovation & Future Outlook: Digital inspection, smart asset monitoring, and advanced high-strength glass formulations strengthen long-term competitiveness and utility network resilience.

Suspension Glass Insulator Market demand is strengthening across ultra-high-voltage transmission, renewable energy interconnections, railway electrification, and cross-border power networks. Manufacturers are introducing advanced toughened glass designs with improved contamination resistance and digital quality inspection systems, increasing production consistency by nearly 14%. Supply-chain localization and grid reliability regulations are encouraging regional manufacturing expansion, creating a stronger foundation for strategic investment and competitive differentiation.

The Suspension Glass Insulator Market has become strategically important as utilities accelerate transmission network modernization to support renewable energy integration, electrification, and higher grid reliability. Infrastructure upgrades, supply-chain restructuring, and national energy security programs are reshaping procurement priorities, encouraging utilities to source durable, high-performance insulation solutions with longer operational lifecycles. Manufacturers are responding by expanding production capacity closer to key transmission projects and strengthening regional supply ecosystems.

Modern automated glass manufacturing and AI-assisted optical inspection systems reduce production defects by nearly 20% compared with conventional manual inspection while improving quality consistency and lowering lifecycle maintenance requirements. Asia-Pacific continues to lead large-scale deployment through extensive ultra-high-voltage projects, whereas Europe focuses on grid resilience, renewable integration, and stricter reliability standards. Over the next two to three years, digital inspection adoption across manufacturing facilities is expected to expand significantly as utilities emphasize predictive asset management.

A practical example includes transmission utilities replacing aging porcelain strings with toughened glass suspension insulators during network refurbishment, reducing inspection frequency and improving operational reliability. Leading companies are expanding manufacturing facilities, forming utility partnerships, and investing in automated production technologies to strengthen delivery capabilities. These strategies position suppliers to secure long-term infrastructure contracts while establishing durable competitive advantages in an increasingly technology-driven transmission equipment market.

Large-scale transmission expansion and aging grid replacement are creating sustained demand for suspension glass insulators with superior mechanical performance and long service life. China accounts for nearly 42% of global manufacturing capacity, while more than 65% of newly commissioned extra-high-voltage transmission projects increasingly specify toughened glass insulation because of its lower inspection complexity and visible failure characteristics. National grid modernization programs in India and China's continued ultra-high-voltage network expansion are accelerating procurement cycles. This structural infrastructure shift improves network reliability while reducing lifecycle maintenance costs. Manufacturers are responding through automated production investments, localized manufacturing, and long-term utility supply agreements, strengthening delivery resilience and creating competitive advantages in large-scale transmission infrastructure projects.

Fluctuating prices of high-purity silica, energy-intensive glass production, and utility procurement delays continue to pressure operational margins. Energy expenses contribute nearly 30% of manufacturing costs, while logistics disruptions have increased lead times by approximately 18% for selected export markets. European manufacturers also face higher electricity costs, affecting production competitiveness against Asian suppliers. These structural constraints delay project execution, complicate pricing strategies, and reduce manufacturing flexibility for large transmission contracts. Companies are mitigating exposure through long-term raw material agreements, localized sourcing strategies, production automation, and geographically diversified manufacturing footprints that improve supply continuity while reducing dependence on single-country procurement networks.

The transition toward intelligent transmission infrastructure is opening new opportunities beyond conventional insulator supply. Digital inspection technologies and AI-enabled defect detection reduce manual inspection requirements by nearly 25%, while predictive maintenance platforms improve asset utilization by around 15%. India's Green Energy Corridor expansion and increasing cross-border transmission projects encourage utilities to adopt higher-performance insulation systems compatible with digital asset management. Manufacturers are investing in R&D for advanced toughened glass formulations, drone-based inspection compatibility, and strategic partnerships with grid technology providers. A less obvious opportunity lies in integrating inspection data with utility asset management platforms, enabling service-based business models alongside traditional equipment sales.

Meeting rising transmission equipment demand without compromising product reliability remains a critical execution challenge. Automated optical inspection can reduce manufacturing defects by approximately 20%, yet many facilities continue to depend on skilled manual quality validation for critical production stages. Japan and Germany maintain stringent utility qualification standards, requiring extensive product testing before commercial deployment, extending approval timelines by nearly 15%. These technical and certification requirements increase operational complexity as manufacturers expand production capacity. Companies must strengthen automation, workforce training, digital quality assurance, and international certification capabilities while expanding manufacturing infrastructure to sustain long-term competitiveness and consistent performance across increasingly complex global transmission projects.

Automated Glass Manufacturing Expansion Manufacturers are accelerating automation across tempering, molding, and inspection processes to improve consistency and reduce production losses. Automated production lines have increased throughput by nearly 18%, while AI-enabled optical inspection has lowered defect rates by approximately 20%. Rising labor costs in China and stricter quality requirements from transmission utilities are driving this transition. Companies are expanding smart manufacturing facilities, integrating robotics into finishing operations, and standardizing production workflows to improve delivery reliability and support growing utility procurement requirements.

Localized Supply Chain Strategies Utilities and manufacturers are restructuring procurement networks to reduce dependence on single-country sourcing and shorten delivery timelines. Localized sourcing has reduced logistics lead times by nearly 15%, while regional inventory programs have improved project fulfillment by around 12%. India's transmission infrastructure expansion and supply-chain diversification initiatives have encouraged new manufacturing investments. Leading suppliers are establishing regional assembly hubs, expanding supplier partnerships, and increasing inventory visibility to strengthen operational resilience during large-scale transmission projects.

Digital Transmission Asset Monitoring Utilities are increasingly integrating suspension glass insulators into digital asset management programs using drone inspections, image analytics, and predictive maintenance software. Inspection productivity has improved by approximately 30%, while manual field inspections have declined by nearly 25% across digitally managed transmission corridors. Utilities in Germany and Japan are adopting condition-based maintenance practices to improve network reliability. Manufacturers are designing insulators compatible with automated inspection technologies and collaborating with digital grid solution providers to enhance long-term asset performance.

Sustainable Manufacturing Priorities Environmental performance is becoming a competitive differentiator as manufacturers improve furnace efficiency, increase recycled glass usage, and optimize energy consumption. Modern production facilities have reduced energy intensity by approximately 12%, while recycled glass utilization has increased by nearly 15% in selected manufacturing plants. Carbon reduction policies and utility sustainability procurement standards are influencing purchasing decisions. Companies are modernizing production equipment, investing in cleaner melting technologies, and implementing environmental certification programs to strengthen competitiveness in international utility tenders.

Standard Type suspension glass insulators remain the dominant segment, accounting for approximately 58% of global demand due to their proven mechanical strength, standardized specifications, and cost-effective deployment across conventional transmission infrastructure. Utilities continue specifying these insulators for medium- and high-voltage overhead lines because they simplify maintenance while offering reliable long-term performance. Manufacturers prioritize production efficiency and standardized product portfolios to support high-volume utility contracts, particularly across China and India where national transmission expansion remains extensive. Anti-Pollution Type represents the fastest-growing segment as utilities operating in coastal, desert, and industrial environments increasingly require enhanced contamination resistance. Adoption has increased by nearly 16% across heavily polluted transmission corridors. Fog Type insulators continue serving humid and high-altitude applications where moisture accumulation affects electrical performance. Companies are expanding specialized product lines, investing in advanced toughened glass formulations, and strengthening engineering support for application-specific utility projects. Investment priorities increasingly favor premium-performance insulators capable of reducing maintenance frequency and improving long-term transmission reliability.

Transmission Lines remain the largest application segment, representing nearly 68% of total suspension glass insulator deployment due to continuous investment in extra-high-voltage and long-distance electricity networks. These projects require high mechanical strength, electrical reliability, and long service life under demanding environmental conditions. China and India continue expanding national transmission corridors, while interconnection projects increasingly specify standardized glass suspension systems to simplify maintenance and improve operational reliability. Manufacturers are expanding production capacity and strengthening long-term supply agreements with grid operators to support these infrastructure programs. Substations are the fastest-growing application as utilities modernize switching facilities, renewable integration points, and digital substations requiring high-performance insulation systems. Installations within substations have increased by approximately 14%, supported by grid automation initiatives. Distribution Lines remain an important application for medium-voltage networks, particularly in urban expansion and rural electrification projects where durable and low-maintenance components reduce lifecycle operating costs. Companies are broadening application-specific product portfolios while investing in engineering services to meet increasingly customized utility specifications.

Utilities remain the largest end-user segment, accounting for approximately 72% of overall market demand because national grid operators and transmission companies manage extensive overhead power networks requiring reliable suspension insulation systems. Ongoing replacement of aging infrastructure, renewable energy integration, and grid resilience programs continue driving procurement activity. Large utilities increasingly favor long-term framework agreements and standardized specifications to improve procurement efficiency and lifecycle asset performance. Manufacturers are responding through localized production, dedicated utility engineering teams, and expanded after-sales technical support. Industrial end-users represent the fastest-growing segment as mining operations, steel manufacturing, petrochemical facilities, and renewable energy developers construct dedicated high-voltage transmission infrastructure. Industrial demand has expanded by nearly 13% through increasing private power network investments. Commercial users maintain comparatively smaller demand, primarily supporting institutional campuses, transport infrastructure, and specialized electrical installations. Companies are introducing customized product configurations, flexible commercial agreements, and project-specific technical consulting to strengthen competitiveness across emerging industrial power infrastructure developments.

Asia-Pacific accounted for the largest market share at 52.4% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 3.9% between 2026 and 2033.

North America represents approximately 18.3% of the global Suspension Glass Insulator Market, supported by transmission modernization, renewable energy integration, and replacement of aging overhead infrastructure. Utilities are prioritizing high-strength suspension glass insulators to improve grid reliability and reduce maintenance frequency across high-voltage corridors. More than 65% of planned transmission investments are directed toward upgrading existing infrastructure and expanding interregional electricity networks. Grid resilience initiatives, digital asset management, and utility partnerships continue strengthening procurement activity. Manufacturers are expanding local inventories, enhancing engineering support, and collaborating with transmission operators to improve delivery schedules and project execution efficiency.

United States Market Outlook: The United States remains the region's largest market due to extensive transmission infrastructure, utility modernization programs, and renewable energy integration. More than 75,000 km of new transmission lines are proposed or under development to strengthen long-distance electricity delivery. Utilities are increasingly replacing aging porcelain insulation with advanced glass alternatives that improve inspection efficiency and operational reliability. Domestic suppliers continue investing in manufacturing expansion, inventory localization, and strategic utility partnerships to support long-term transmission infrastructure requirements.

Europe accounts for nearly 20.6% of global demand as utilities modernize transmission systems to support renewable integration and cross-border electricity exchanges. Expansion of offshore wind connections, high-voltage interconnectors, and digital substations continues increasing demand for durable suspension glass insulators. Approximately 40% of ongoing transmission projects involve network reinforcement linked to clean energy deployment. Utilities are emphasizing lifecycle performance, environmental compliance, and predictive maintenance capabilities. Manufacturers are strengthening regional production, expanding technical partnerships, and investing in advanced manufacturing technologies to meet increasingly demanding utility specifications.

Germany Market Outlook: Germany leads the European market through extensive transmission upgrades supporting renewable generation and industrial electrification. National grid operators continue expanding high-voltage direct current infrastructure while modernizing conventional transmission corridors. More than 900 km of major transmission projects remain under phased implementation, reinforcing long-term demand for premium insulation systems. Equipment suppliers are expanding engineering collaboration with utilities and introducing higher-performance glass insulators designed for enhanced operational reliability and lower maintenance requirements.

Asia-Pacific dominates the Suspension Glass Insulator Market with approximately 52.4% of global demand, supported by unmatched manufacturing capacity, rapid transmission expansion, and large-scale electrification projects. China and India continue investing in ultra-high-voltage transmission, renewable integration, and national grid reinforcement programs. The region contributes more than 60% of global suspension glass insulator production capacity, supported by vertically integrated manufacturing ecosystems and competitive production costs. Companies continue expanding automated production facilities, strengthening export capabilities, and increasing localized supply networks to support both domestic infrastructure and international utility markets.

China Market Outlook: China remains the world's largest producer and consumer of suspension glass insulators through continuous investment in ultra-high-voltage transmission infrastructure and State Grid development programs. The country accounts for roughly 42% of global manufacturing capacity and maintains one of the most integrated electrical equipment supply chains worldwide. Domestic manufacturers continue expanding automated production, investing in advanced glass processing technologies, and strengthening export competitiveness while supporting large-scale domestic transmission modernization projects.

South America represents approximately 5.6% of the global market, with investment concentrated in transmission expansion supporting mining, hydropower, and renewable energy integration. Governments and utilities continue upgrading long-distance electricity networks connecting resource-rich regions with industrial demand centers. Nearly 30% of recently approved transmission projects focus on strengthening interregional electricity reliability. Infrastructure financing and permitting timelines remain operational constraints, yet manufacturers continue developing regional distribution partnerships and expanding technical service capabilities to improve project responsiveness and utility engagement.

Brazil Market Outlook: Brazil leads the South American market through one of the world's largest interconnected transmission systems and sustained investment in renewable electricity infrastructure. Expansion of wind and hydropower generation continues increasing demand for high-voltage transmission equipment across long-distance corridors. Utilities are prioritizing durable suspension glass insulators to reduce maintenance costs in challenging environmental conditions. Equipment suppliers continue strengthening regional logistics, technical support networks, and project partnerships to improve supply reliability for large transmission developments.

The Middle East & Africa accounts for approximately 3.1% of global market demand, supported by electricity network expansion, industrial diversification, and cross-border transmission initiatives. National utilities continue investing in high-voltage infrastructure to improve grid stability, support urbanization, and connect renewable energy projects. More than 25% of ongoing utility infrastructure programs include transmission modernization components requiring advanced insulation equipment. Manufacturers are expanding distributor partnerships, improving regional inventory availability, and providing engineering services tailored to harsh operating environments with high temperatures and dust exposure.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategically important market through extensive power infrastructure investment linked to industrial diversification and large-scale development initiatives. Transmission expansion supporting renewable energy projects and smart grid deployment continues increasing procurement of premium insulation systems. National electricity infrastructure programs emphasize operational reliability under demanding climatic conditions. Manufacturers are strengthening regional partnerships, expanding technical service capabilities, and positioning localized inventories to improve responsiveness for utility modernization and high-voltage transmission projects.

The Suspension Glass Insulator Market is led by global specialists including Sediver, NGK Insulators, MacLean Power Systems, Dalian Insulator Group, and Modern Insulators, competing against regional manufacturers in China and India on quality, delivery, and lifecycle performance rather than price alone. The top five players collectively control approximately 48% of the global market, while regional suppliers compete through lower production costs and faster domestic fulfillment. Premium manufacturers achieve 15–20% lower lifecycle maintenance requirements through advanced glass formulations and automated quality inspection, whereas cost-focused producers shorten lead times by nearly 18% using localized supply chains. Competition increasingly centers on utility qualification, manufacturing automation, customized contamination-resistant designs, and vertically integrated production. Strategic partnerships with transmission utilities, production expansion, and digital inspection technologies are reshaping market leadership. Lengthy utility certification cycles and stringent performance testing remain key entry barriers. Success depends on combining proven product reliability, responsive supply capability, application engineering expertise, and long-term utility relationships.

NGK Insulators, Ltd.

MacLean Power Systems

Dalian Insulator Group Co., Ltd.

Modern Insulators Ltd.

Aditya Birla Insulators

INAEL Electrical Systems

LAPP Insulators Group

Elsewedy Electric

Verescence La Granja Insulators

TCI Power

Orient Insulators

Gamma Insulators

Advanced manufacturing technologies are transforming suspension glass insulator production through AI-based visual inspection, robotic handling, and precision tempering systems. Automated inspection reduces manufacturing defects by approximately 20%, while digital furnace controls improve energy efficiency by nearly 12%. More than 45% of newly commissioned production facilities now incorporate automated quality monitoring, enabling consistent product performance and faster qualification for utility transmission projects. Manufacturers adopting these technologies strengthen delivery reliability while reducing operational costs.

Emerging technologies focus on high-strength glass compositions, digital twin manufacturing, predictive maintenance compatibility, and drone-assisted transmission inspections. Compared with conventional manual inspection methods, AI-enabled optical systems improve inspection accuracy by nearly 30% while reducing evaluation time by approximately 25%. Global technology leaders such as Sediver and NGK benefit most through stronger product differentiation, faster certification, and enhanced lifecycle performance demanded by transmission utilities operating extra-high-voltage networks.

Between 2026 and 2028, intelligent manufacturing platforms, machine vision, and industrial IoT integration will become mainstream across premium production facilities. Adoption is expected to exceed 60% among leading manufacturers as utilities increasingly prioritize traceability, quality consistency, and predictive asset management. Companies investing early in digital production, advanced materials engineering, and inspection automation will strengthen competitive positioning, accelerate project execution, and secure long-term utility supply agreements.

March 2024 – NGK Insulators announced a production expansion for AMB ceramic substrates, increasing planned monthly manufacturing capacity by 2.5× by 2026 through a ¥5 billion investment, strengthening advanced ceramic manufacturing capabilities and supply-chain resilience. Source: www.ngk-global.com

January 2025 – Borosil Renewables approved a 50% manufacturing capacity expansion after favorable trade measures supported domestic glass production, reinforcing regional glass-processing capability and encouraging investment across high-performance industrial glass manufacturing.

February 2026 – Sediver USA announced expansion of its Arkansas manufacturing facility, creating 40 new jobs while scaling automated production following the milestone of 5 million insulator units produced, strengthening North American utility supply capability.

February 2025 – NGK Insulators partnered with AIST to develop higher-accuracy thermal diffusivity evaluation methods for advanced ceramic substrates, improving testing precision and strengthening next-generation materials development for high-performance electrical applications.

The report delivers a comprehensive assessment of the Suspension Glass Insulator Market across Standard Type, Fog Type, and Anti-Pollution Type, evaluating their deployment across Transmission Lines, Distribution Lines, and Substations, while analyzing demand from Utilities, Industrial, and Commercial end-users. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level analysis of major manufacturing, infrastructure, and transmission investment trends. More than 45% of the assessment focuses on operational performance, technology adoption, procurement patterns, and competitive positioning influencing utility purchasing decisions.

The study examines advanced manufacturing technologies, automated inspection systems, digital asset management, contamination-resistant product innovations, and evolving transmission infrastructure requirements. It provides strategic benchmarking of leading manufacturers, evaluates deployment trends, supply-chain developments, and regional production capabilities, and supports investment planning, product portfolio optimization, geographic expansion, partnership strategies, and competitive positioning between 2026 and 2033 through data-driven operational and market intelligence.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 518.6 Million |

| Market Revenue (2033) | USD 672.4 Million |

| CAGR (2026–2033) | 3.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Sediver; NGK Insulators, Ltd.; MacLean Power Systems; Dalian Insulator Group Co., Ltd.; Modern Insulators Ltd.; Aditya Birla Insulators; INAEL Electrical Systems; LAPP Insulators Group; Elsewedy Electric; TCI Power; Orient Insulators; Gamma Insulators |

| Customization & Pricing | Available on Request (10% Customization Free) |