Reports

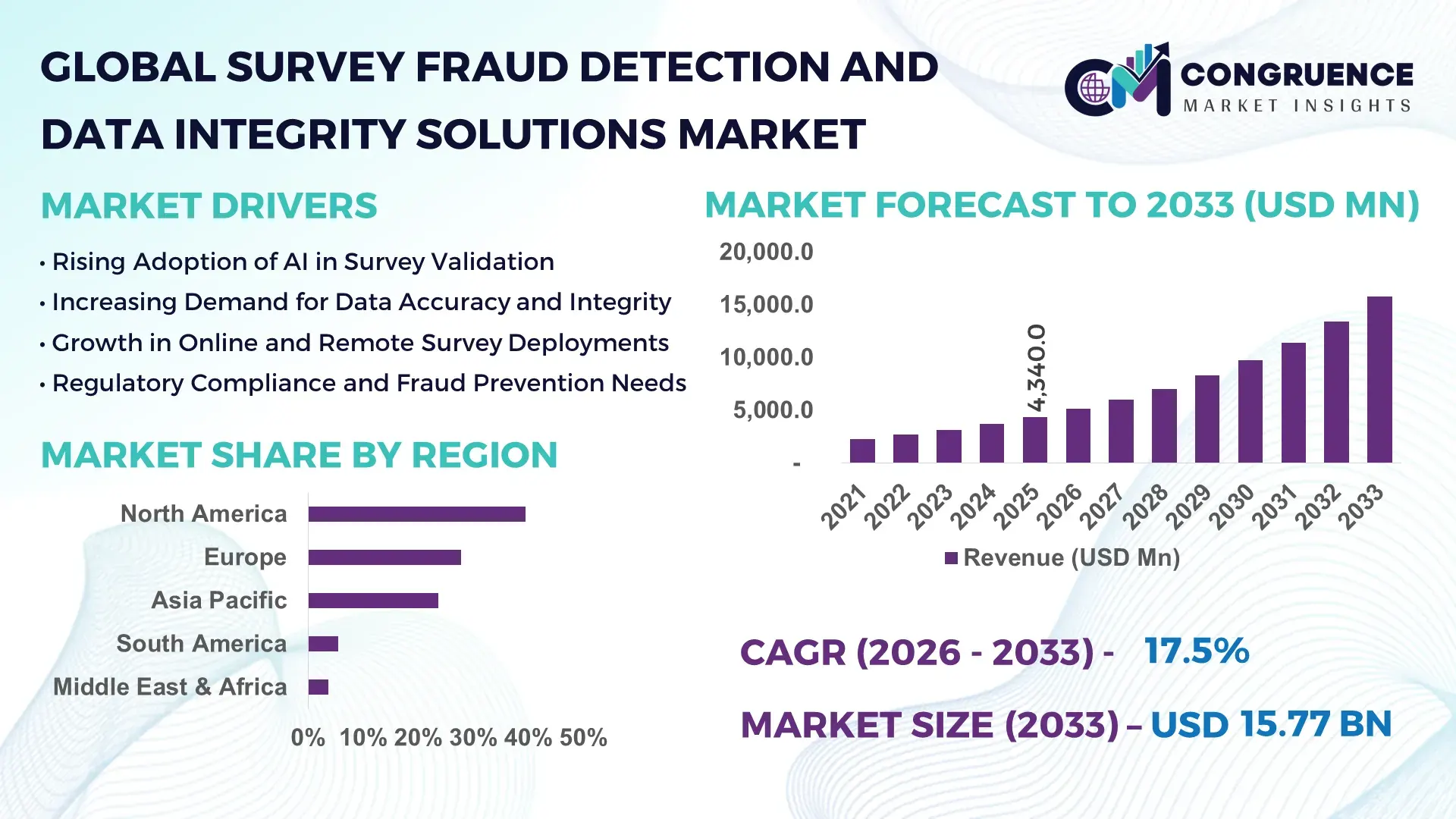

The Global Survey Fraud Detection and Data Integrity Solutions Market was valued at USD 4,340.0 Million in 2025 and is anticipated to reach a value of USD 15,768.6 Million by 2033 expanding at a CAGR of 17.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rising dependence on digital survey data for enterprise decision-making, regulatory reporting, and AI model training, which has intensified demand for advanced fraud detection, respondent authentication, and data quality assurance solutions.

The United States dominates the Survey Fraud Detection and Data Integrity Solutions Market in terms of solution development, deployment scale, and enterprise adoption depth. The country hosts over 60% of global survey analytics and market research software vendors, with large-scale investments exceeding USD 1.2 billion annually in data quality, identity verification, and behavioral analytics platforms. More than 70% of Fortune 500 enterprises operating in the U.S. integrate automated fraud detection layers into customer, employee, and panel-based surveys. Advanced applications span political polling, healthcare outcomes research, financial services risk assessments, and AI training datasets. The U.S. also leads in technological advancement, with over 65% of deployed solutions incorporating machine learning-based anomaly detection, biometric verification, or device fingerprinting, and cloud-native platforms supporting survey volumes exceeding 10 billion responses annually.

Market Size & Growth: Valued at USD 4,340.0 Million in 2025, projected to reach USD 15,768.6 Million by 2033 at a CAGR of 17.5%, driven by enterprise-wide digital data validation needs.

Top Growth Drivers: Rising online survey adoption (68%), automation-led fraud detection efficiency gains (42%), and regulatory-driven data audit requirements (36%).

Short-Term Forecast: By 2028, automated survey fraud detection is expected to reduce invalid response costs by approximately 35%.

Emerging Technologies: AI-driven behavioral analytics, device fingerprinting, biometric respondent verification, and real-time anomaly detection engines.

Regional Leaders: North America projected at USD 6.1 Billion by 2033 with enterprise SaaS adoption; Europe at USD 4.3 Billion driven by compliance-led deployments; Asia Pacific at USD 3.8 Billion supported by digital panel expansion.

Consumer/End-User Trends: Market research firms, enterprises, and academic institutions increasingly adopt continuous data integrity monitoring across multi-channel surveys.

Pilot or Case Example: In 2024, a U.S.-based research platform reduced survey fraud incidents by 48% through AI-based response pattern analysis.

Competitive Landscape: Market leader holds approximately 18% share, followed by 3–5 major global analytics and data integrity solution providers.

Regulatory & ESG Impact: Data protection regulations and ethical AI mandates are accelerating adoption of transparent and auditable survey validation systems.

Investment & Funding Patterns: Over USD 2.6 Billion invested globally in survey analytics, identity verification, and data integrity startups during the past three years.

Innovation & Future Outlook: Integration of survey data integrity tools with enterprise BI, CRM, and AI training pipelines is shaping long-term market evolution.

The Survey Fraud Detection and Data Integrity Solutions Market is closely linked to market research, healthcare studies, political polling, financial services risk analysis, and AI data labeling, with these sectors collectively accounting for over 75% of deployments. Recent innovations include adaptive fraud scoring, real-time respondent behavior monitoring, and cross-survey identity mapping. Regulatory data accuracy mandates, regional digitization rates, and rising remote data collection are shaping consumption patterns, while AI-native validation platforms are defining the future outlook.

The Survey Fraud Detection and Data Integrity Solutions Market has become strategically critical as organizations increasingly rely on survey-derived data to guide investments, policy decisions, and AI-driven automation. High-quality survey data directly influences forecasting accuracy, customer experience strategies, healthcare outcomes research, and regulatory submissions. AI-powered fraud detection delivers up to 45% improvement in invalid response identification compared to rule-based validation standards, enabling enterprises to significantly improve data reliability and decision confidence.

North America dominates in survey data processing volume, while Europe leads in regulated adoption, with over 62% of enterprises deploying compliance-aligned survey validation frameworks. Asia Pacific is rapidly scaling digital panel participation, with enterprise adoption expanding across technology, education, and consumer goods sectors. By 2028, real-time AI-driven respondent authentication is expected to cut survey rework and validation time by 40%, improving operational efficiency and project turnaround cycles.

Compliance and ESG considerations are increasingly embedded into survey data governance. Firms are committing to measurable data integrity improvements, including up to 50% reduction in biased or non-consensual data usage by 2030 through transparent validation workflows. In 2024, a European public-sector research initiative achieved a 52% reduction in fraudulent survey entries by deploying biometric verification and device-level anomaly detection.

Looking ahead, the Survey Fraud Detection and Data Integrity Solutions Market is positioned as a foundational pillar for enterprise resilience, regulatory compliance, and sustainable data-driven growth, supporting trustworthy analytics across increasingly complex digital ecosystems.

The Survey Fraud Detection and Data Integrity Solutions Market is shaped by the rapid digitization of research methodologies, the expansion of online panels, and increasing scrutiny over data accuracy. Organizations are moving away from manual validation toward automated, AI-enabled integrity frameworks that can process large-scale, multi-device survey inputs. Cross-border data collection, remote respondent engagement, and integration with enterprise analytics systems are influencing deployment models. Additionally, stricter data governance standards and rising reputational risks linked to flawed insights are reinforcing the importance of robust fraud detection mechanisms across industries.

The surge in digital surveys across customer experience, employee engagement, healthcare research, and public policy is a primary growth driver. Over 80% of enterprises now use online surveys as a core decision-support tool, significantly increasing exposure to bot traffic, duplicate respondents, and professional survey fraud. Automated fraud detection tools improve data validity rates by more than 40%, enabling organizations to reduce downstream analytics errors. The need for faster insights and scalable validation across millions of responses is accelerating enterprise-wide adoption of advanced integrity solutions.

Despite strong demand, integration complexity remains a key restraint. Many enterprises operate fragmented survey platforms, CRM systems, and analytics tools, making seamless fraud detection deployment challenging. Additionally, heightened data privacy expectations require careful handling of biometric, behavioral, and device-level identifiers. Nearly 38% of organizations report delays in deployment due to internal data governance approvals, while compliance alignment across jurisdictions adds operational overhead, slowing adoption cycles in regulated environments.

AI-driven behavioral analytics offers significant untapped opportunity by enabling real-time identification of suspicious response patterns. Adaptive learning models can analyze response speed, consistency, and interaction behavior to improve fraud detection accuracy by over 50%. Expanding use in healthcare outcomes research, political polling, and AI training datasets creates demand for highly reliable survey data. Cloud-native deployment and API-based integrations further open opportunities among mid-sized enterprises and academic institutions.

Survey fraud tactics are becoming increasingly sophisticated, including human-assisted bots, VPN masking, and coordinated response farms. This requires continuous model retraining and system upgrades, increasing operational costs. Organizations must balance detection sensitivity with respondent experience, as overly aggressive filters risk excluding legitimate participants. Maintaining high accuracy while adapting to evolving fraud behaviors remains a persistent challenge for solution providers and end-users.

Expansion of AI-Based Behavioral Fraud Detection: AI-driven behavioral analysis is now deployed in over 65% of enterprise survey platforms, reducing invalid response rates by up to 47% while improving data consistency scores by 38%.

Integration with Enterprise Analytics Ecosystems: Approximately 58% of large organizations have integrated survey fraud detection tools with BI and CRM platforms, enabling end-to-end data validation and improving insight reliability by 41%.

Growth of Real-Time Respondent Authentication: Real-time identity and device verification adoption has increased by 44%, cutting duplicate participation incidents by nearly 50% across large-scale online panels.

Rising Demand for Compliance-Ready Data Integrity Frameworks: More than 60% of new deployments now include audit-ready validation logs and consent tracking, supporting regulatory alignment and reducing compliance review cycles by 33%.

The Survey Fraud Detection and Data Integrity Solutions Market is segmented across types, applications, and end-user groups, reflecting the diverse operational needs of organizations that rely on survey-driven insights. By type, solutions range from rule-based validation tools to advanced AI-driven behavioral and biometric systems, each addressing different fraud vectors such as bots, duplicate respondents, and professional survey farms. Application-wise, adoption spans market research, healthcare and life sciences, public sector surveys, financial services, and academic research, with varying validation depth and compliance requirements. End-user segmentation highlights strong demand from market research firms, enterprises, government agencies, and educational institutions. Increasing survey volumes, multi-device participation, and cross-border data collection are driving segmentation complexity, as decision-makers prioritize scalable, automated, and audit-ready integrity frameworks tailored to their specific operational environments.

Survey Fraud Detection and Data Integrity Solutions are broadly categorized into rule-based validation systems, AI-driven behavioral analytics, identity and device verification tools, and biometric authentication solutions. AI-driven behavioral analytics currently lead the market, accounting for approximately 46% of adoption, as these systems dynamically analyze response patterns, completion speed, and interaction behavior to detect anomalies at scale. Identity and device verification tools follow with around 28% adoption, focusing on IP intelligence, device fingerprinting, and geolocation consistency. However, biometric-based respondent authentication is the fastest-growing type, expanding at an estimated 19.2% CAGR, driven by rising demand for high-trust surveys in healthcare, public policy, and regulated research environments.

Rule-based validation and manual review tools continue to serve niche use cases, particularly in small-scale academic or internal surveys, contributing a combined 26% share. These tools remain relevant where cost sensitivity or low survey volumes limit advanced automation deployment, but their relative importance is declining as fraud tactics evolve.

• In 2025, a large national public opinion research program implemented AI-based behavioral fraud detection across millions of online responses, reducing duplicate and automated submissions by over 45% while maintaining respondent completion rates above 90%.

Market research and consumer insights represent the leading application segment, accounting for nearly 41% of overall adoption, as enterprises increasingly depend on high-frequency surveys for product, pricing, and brand strategy decisions. Healthcare and life sciences follow with approximately 23% adoption, driven by the need to validate patient-reported outcomes, clinical study surveys, and real-world evidence data. Public sector and government surveys account for around 17%, reflecting large-scale census, labor, and policy feedback initiatives.

Among applications, healthcare and life sciences surveys are the fastest-growing, expanding at an estimated 18.6% CAGR, supported by stricter data integrity expectations and increasing digital patient engagement. Financial services, education, and HR-related surveys collectively contribute the remaining 19% share, serving risk assessment, employee engagement, and academic research needs.

Consumer adoption trends reinforce this segmentation. In 2025, more than 44% of global enterprises reported piloting advanced survey fraud detection within customer experience platforms, while 37% of healthcare organizations indicated active testing of automated validation for patient surveys.

• In 2024, a nationwide healthcare outcomes initiative deployed automated survey integrity tools across digital patient questionnaires, improving valid response rates by over 50% within the first year of implementation.

Market research firms are the leading end-user segment, representing approximately 38% of total adoption, as their business models depend directly on data accuracy, respondent authenticity, and panel quality. Large enterprises follow with around 29% adoption, integrating survey fraud detection into customer experience, employee feedback, and product development workflows. Government and public sector organizations account for nearly 18%, while academic institutions and non-profits contribute the remaining 15%.

Enterprises are the fastest-growing end-user group, with adoption expanding at an estimated 17.9% CAGR, fueled by digital transformation, omnichannel customer engagement, and increased use of survey data in AI-driven decision systems. Market research firms maintain high penetration, with over 70% using some form of automated validation, while government agencies report adoption rates nearing 45% for large-scale digital surveys.

End-user behavior trends show that over 40% of enterprises in 2025 prioritized real-time fraud detection to shorten survey cycles, and nearly 60% of research agencies emphasized continuous panel monitoring to maintain data trust.

• In 2025, a national statistics agency implemented centralized survey data integrity software across multiple departments, achieving a 35% reduction in manual validation effort and significantly improving cross-survey consistency.

North America accounted for the largest market share at 39.5% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19.1% between 2026 and 2033.

Europe followed North America with a 27.8% share, supported by strong regulatory enforcement and enterprise compliance requirements, while Asia-Pacific held approximately 23.6% driven by rapid digitization and large-scale online survey adoption. South America and the Middle East & Africa together represented nearly 9.1% of global demand, reflecting emerging adoption across public sector surveys, telecom, and media research. Globally, more than 72% of large enterprises now conduct surveys primarily through digital channels, increasing exposure to fraud risks and accelerating demand for automated data integrity tools. Cross-border survey execution now represents over 44% of total survey volume, further intensifying the need for region-specific fraud detection frameworks aligned with local regulations, languages, and device usage patterns.

The region accounts for approximately 39.5% of global market adoption, supported by early technology uptake and strong enterprise spending on data governance. Key industries driving demand include healthcare, financial services, technology, and political research, where survey data directly influences compliance, investment, and policy outcomes. Regulatory requirements related to data protection, consent, and auditability have increased deployment of automated validation systems across both public and private sectors. Digital transformation trends show that over 68% of enterprises integrate survey fraud detection with CRM and analytics platforms. Local solution providers are actively enhancing AI-driven behavioral models and real-time device intelligence to manage surveys exceeding billions of annual responses. Consumer behavior shows higher enterprise adoption in healthcare and finance, with these sectors accounting for nearly 55% of regional deployments.

Europe represents nearly 27.8% of the global market, with Germany, the UK, and France collectively contributing over 61% of regional demand. Strong regulatory oversight and sustainability-driven data governance initiatives have increased adoption of transparent, explainable fraud detection systems. Enterprises increasingly prioritize audit-ready survey validation, with over 58% of large organizations implementing explainability layers within AI-based integrity tools. Emerging technologies such as privacy-preserving analytics and consent-based respondent verification are gaining traction. Local technology firms are focusing on compliance-first architectures aligned with regional data protection frameworks. Consumer behavior reflects regulatory pressure, with organizations favoring explainable and traceable survey validation mechanisms to reduce legal and reputational risk.

Asia-Pacific ranks as the second-largest growth region with approximately 23.6% market share, led by China, India, and Japan. The region processes some of the world’s largest online survey volumes, driven by e-commerce, fintech, and mobile app ecosystems. Infrastructure expansion and cloud adoption have enabled scalable fraud detection deployments, particularly for multilingual and mobile-based surveys. Innovation hubs across East and South Asia are integrating AI-driven anomaly detection and device intelligence tailored to high mobile penetration rates exceeding 75% in key markets. Local providers increasingly support real-time validation for consumer panels with millions of respondents. Consumer behavior highlights growth driven by e-commerce feedback systems and mobile AI applications, particularly among digitally native populations.

South America accounts for roughly 5.4% of global adoption, with Brazil and Argentina leading regional demand. Media, telecom, and public sector surveys are major drivers, as organizations seek accurate insights across diverse linguistic and socio-economic groups. Infrastructure modernization and digital public services have increased online survey usage, particularly in urban centers. Government initiatives supporting digital inclusion have indirectly expanded survey reach, increasing exposure to fraudulent responses. Regional solution providers focus on language-aware validation and regional IP intelligence. Consumer behavior shows demand closely tied to media measurement and localized content testing, where survey accuracy directly impacts advertising and programming decisions.

The region represents approximately 3.7% of global market activity, with the UAE and South Africa emerging as key growth countries. Demand is driven by oil & gas, construction, public administration, and smart city initiatives that rely on large-scale stakeholder surveys. Technological modernization, including cloud migration and national digital transformation programs, is increasing adoption of automated data integrity tools. Trade partnerships and regional data governance initiatives are shaping procurement standards. Local providers emphasize scalable validation for multilingual and cross-border surveys. Consumer behavior reflects rising trust in digital government and enterprise surveys, particularly where identity verification is embedded into data collection workflows.

United States – 34.2% Market Share: Strong enterprise demand, advanced analytics infrastructure, and large-scale digital survey volumes drive dominance.

Germany – 9.6% Market Share: High regulatory enforcement and widespread enterprise adoption of compliant, explainable survey validation systems support leadership.

The competitive environment in the Survey Fraud Detection and Data Integrity Solutions Market is dynamic and moderately fragmented, with 30+ active competitors globally, ranging from established analytics firms to specialized fraud tech startups. The top 5 companies collectively hold approximately 38–42% of the market, indicating that while there is concentration at the top, significant share remains spread across mid-tier and emerging players. Leading vendors are investing heavily in AI, machine learning, behavioral biometrics, device intelligence, and cloud-native architectures to enhance detection precision and reduce false positives. Strategic initiatives such as partnerships, acquisitions, and platform integrations are shaping positioning—major analytics companies are integrating fraud integrity modules with broader data platforms, while niche innovators focus on real-time anomaly detection and cross-survey identity resolution.

Innovation trends include deployment of advanced semantic analysis to counter AI-generated fraudulent survey responses and real-time cross-device fingerprinting for identity assurance. Competitive positioning varies: global SaaS and enterprise analytics brands emphasize scalability and ecosystem integration, while agile specialists target high-trust sector niches such as healthcare, government surveys, and AI training data pipelines. Market participants continually enhance capabilities through strategic alliances, API ecosystem expansion, and targeted technology upgrades that address hybrid human-bot fraudster tactics and deepfake-style contamination of survey data. Speed to market, model adaptability, and compliance alignment are critical differentiators in this evolving competitive landscape.

FICO

LexisNexis Risk Solutions

AU10TIX

IDfy

Feedzai

SentiLink

ClearSale

NICE Actimize

TransUnion Risk and Identity Solutions

Oracle Risk Management Cloud

SAP Intelligent Fraud Detection

Forter

Clari5 (by Perfios)

The technological landscape for Survey Fraud Detection and Data Integrity Solutions is characterized by rapid evolution, driven by the need to counter increasingly sophisticated fraud tactics and ensure robust data quality across digital survey channels. Current core technologies include machine learning-based anomaly detection engines that analyze patterns in response timing, interaction behavior, and multi-field consistency to flag suspect entries. These models typically process millions of data points per survey campaign to identify outliers and automated bots, enabling real-time filtering without manual review.

Behavioral biometrics is another critical technology, capturing device-level fingerprints, click patterns, typing dynamics, and navigation flows to differentiate between human and automated responses. Identity and device verification systems add a verification layer that checks IP intelligence, geolocation consistency, and anonymized identity proofs to reduce duplicate or spoofed respondent data. Cloud-native platforms enable these technologies to scale across high-volume survey deployments, improving throughput while maintaining low latency in fraud identification.

Emerging technologies include semantic content analysis, which examines open-text responses for coherence and plausibility, increasingly necessary with the rise of AI-generated text that can mimic legitimate answers. Graph analytics and network linkage models trace respondent interactions and shared attributes to uncover coordinated fraudulent behavior across panels. Privacy-enhancing computation techniques, such as differential privacy and homomorphic encryption, support compliance with stringent data protection regulations while preserving analytic utility.

Integrations with enterprise BI, CRM, and AI training data pipelines allow survey integrity insights to flow into broader decision-making systems, improving the overall quality of analytics outputs. Decision intelligence frameworks are now incorporating fraud risk scores directly into enterprise dashboards, enabling stakeholders to see the trustworthiness of survey insights alongside uptake metrics. These technology trends collectively strengthen the capability of organizations to detect, mitigate, and prevent fraud while safeguarding data integrity in complex digital environments.

• In July 2025, Experian released a data intelligence report showing that 35% of UK businesses were targeted by AI‑related fraud in Q1 2025, up from 23% the previous year, driven by deepfakes, synthetic identities, and identity theft techniques; 68% of businesses planned to increase fraud budgets and over 50% expected to enhance AI analytics and detection models to counter fraud. Source: www.experianplc.com

• In May 2025, FICO officially launched the FICO Marketplace, a B2B intelligence exchange that enables enterprise customers to access and integrate advanced AI decisioning tools, data assets, and analytics — including fraud and identity verification modules — significantly speeding model deployment and collaboration across fraud detection workflows. Source: www.fico.com

• In November 2025, Experian initiated the “Fraud Frontlines” podcast series during International Fraud Awareness Week, featuring industry experts and senior leaders discussing GenAI‑powered fraud risks, advanced strategies for threat mitigation, and evolving patterns of fraud across sectors. This initiative reflects heightened market focus on education and forward‑looking detection methodologies. Source: www.experian.com

• In September 2025, Nasdaq Verafin and BioCatch initiated a strategic partnership integrating behavioral biometrics into fraud detection workflows across 2,600+ financial institutions, enhancing real-time identification and prevention of suspicious payments. Source: www.reuters.com

The scope of the Survey Fraud Detection and Data Integrity Solutions Market Report encompasses a comprehensive examination of solution types, applications, end-user segments, and regional landscapes. It analyzes a wide range of product categories from rule-based validation systems and device verification tools to advanced AI-driven behavioral analytics and biometric authentication platforms, detailing their functionality, adoption dynamics, and relevance across organizational contexts. The report covers application areas including market research, healthcare outcomes measurement, public sector surveys, financial services risk evaluation, academic research, and customer experience programs, providing insights into how different industries approach survey data integrity and fraud mitigation.

End-user segmentation includes market research agencies, large enterprises, government bodies, academic institutions, and non-profit organizations, with detailed profiles of demand drivers, operational challenges, and adoption behavior. Geographic coverage spans major regions such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional infrastructure trends, regulatory influences, technological readiness, and consumer behavior variations that shape deployment strategies.

The report also explores integration with broader enterprise ecosystems such as CRM, BI, and AI training data pipelines, as well as emerging niche segments like semantic analysis for AI-generated fraud detection, graph-based respondent linkage models, and identity orchestration frameworks. Technology insights focus on current and emerging innovations including machine learning, cloud computing, privacy-enhancing computation, and real-time behavioral monitoring. The analysis further documents competitive dynamics, strategic collaborations, product enhancements, innovation trends, and use-case case studies that inform decision-makers, technology planners, and risk managers about evolving survey fraud threats and solutions. The scope ensures decision-makers are informed about both foundational functionalities and forward-looking capabilities within the survey fraud detection arena.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,340.0 Million |

| Market Revenue (2033) | USD 15,768.6 Million |

| CAGR (2026–2033) | 17.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Experian, IBM Corporation, SAS Institute, FICO, LexisNexis Risk Solutions, AU10TIX, IDfy, Feedzai, SentiLink, ClearSale, NICE Actimize, TransUnion Risk & Identity Solutions, Oracle Risk Management Cloud, SAP Intelligent Fraud Detection, Forter, Clari5 |

| Customization & Pricing | Available on Request (10% Customization Free) |