Reports

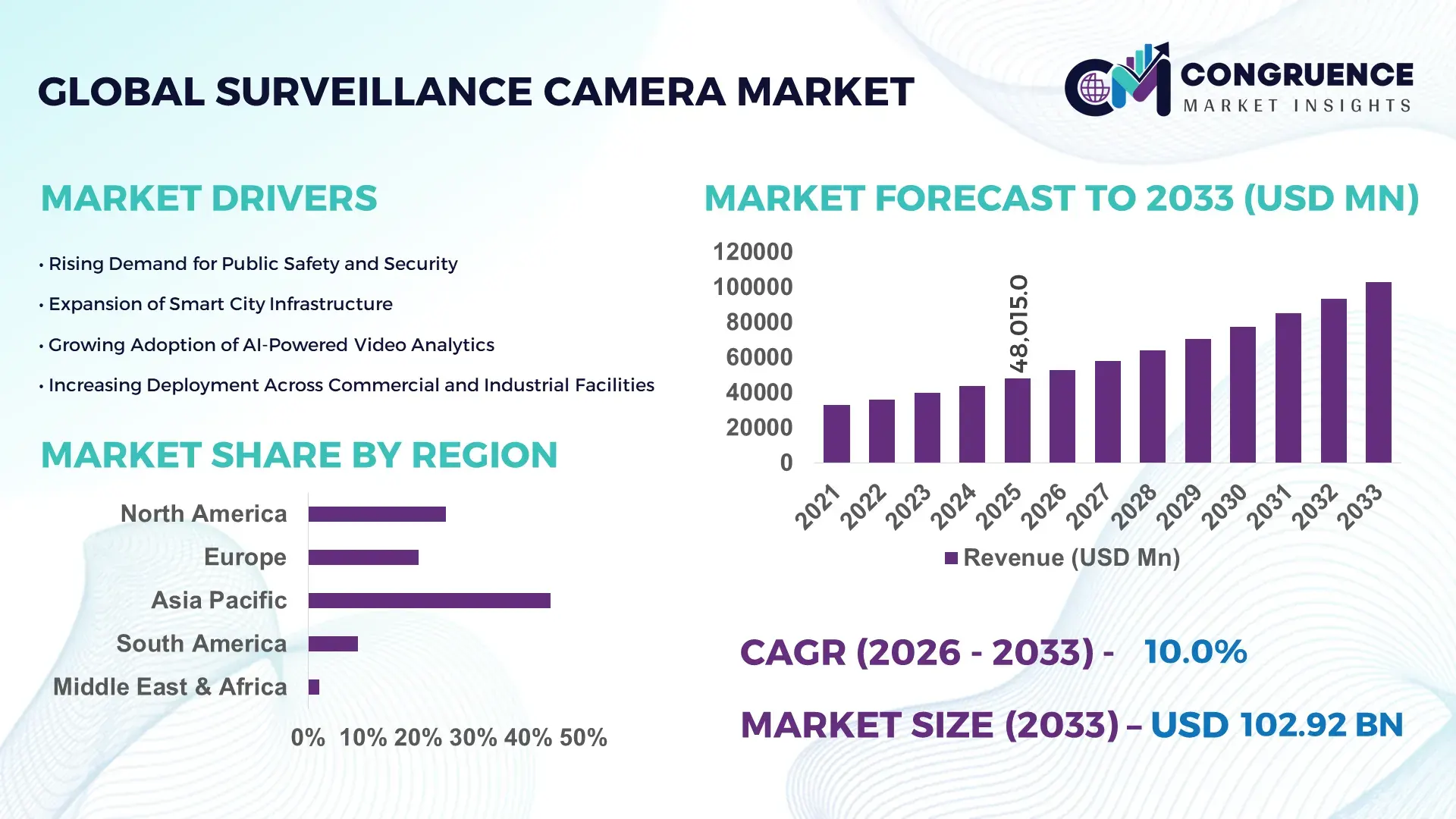

The Global Surveillance Camera Market was valued at USD 48015 Million in 2025 and is anticipated to reach a value of USD 102924 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033. Rapid urbanization, rising public safety initiatives, and the integration of artificial intelligence–enabled monitoring systems across commercial and municipal infrastructures are major factors supporting long-term market expansion.

China continues to operate as the largest production and deployment hub for surveillance cameras globally, with manufacturing clusters in Shenzhen and Hangzhou producing over 40% of the world’s IP camera units annually. The country has deployed more than 700 million surveillance cameras across transportation networks, public facilities, and smart city infrastructure projects. Government-backed investment in digital security infrastructure has exceeded USD 15 billion over the last five years, accelerating adoption in traffic monitoring, retail analytics, and industrial security management systems. Chinese technology vendors have also introduced advanced AI-driven facial recognition and behavior analytics cameras capable of processing up to 25 video streams simultaneously using edge computing processors.

Market Size & Growth: The surveillance camera market is valued at USD 48.0 billion in 2025 and projected to reach USD 102.9 billion by 2033, expanding at a 10% CAGR driven by rapid smart city deployments and advanced AI video analytics integration.

Top Growth Drivers: Smart city infrastructure adoption improving security monitoring by 35%; AI-based video analytics improving threat detection accuracy by 40%; expansion of retail and logistics surveillance improving operational visibility by 28%.

Short-Term Forecast: By 2028, AI-powered surveillance platforms are expected to reduce security response time by 30% and improve real-time monitoring efficiency by nearly 25% across enterprise facilities.

Emerging Technologies: Edge AI cameras, cloud-based video surveillance platforms, and deep-learning powered object recognition systems are transforming intelligent monitoring capabilities.

Regional Leaders: Asia-Pacific projected to reach USD 42 billion by 2033 driven by smart city surveillance expansion; North America estimated at USD 28 billion with strong enterprise security adoption; Europe forecast at USD 21 billion supported by public transport and urban monitoring infrastructure.

Consumer/End-User Trends: Retail chains, transportation hubs, manufacturing facilities, and public infrastructure agencies account for over 65% of enterprise surveillance deployments, with growing adoption of AI-enabled behavioral analytics.

Pilot or Case Example: In 2024, Singapore deployed AI-based urban surveillance cameras across major transit routes, improving traffic incident detection efficiency by 32% and reducing response time by 20%.

Competitive Landscape: Hikvision leads with approximately 18% market presence, followed by Dahua Technology, Axis Communications, Bosch Security Systems, and Honeywell International.

Regulatory & ESG Impact: Governments are introducing data protection and responsible AI surveillance regulations while promoting energy-efficient camera systems reducing power consumption by nearly 15%.

Investment & Funding Patterns: Global investment in smart surveillance infrastructure exceeded USD 8 billion in 2024, with venture capital increasingly targeting AI video analytics and cloud surveillance software providers.

Innovation & Future Outlook: Integration of edge computing, 8K resolution cameras, biometric identification, and AI-powered predictive monitoring systems is expected to reshape intelligent security ecosystems worldwide.

Enterprise adoption of advanced surveillance cameras is expanding across key sectors including transportation, manufacturing, retail, banking, and critical infrastructure monitoring. Transportation and smart mobility systems account for nearly 30% of surveillance deployments, followed by commercial retail security and loss-prevention solutions. Modern cameras increasingly integrate machine learning algorithms capable of object recognition, behavioral tracking, and real-time anomaly detection. Governments are implementing stricter data privacy frameworks while encouraging secure digital infrastructure development. Additionally, growing demand for cloud-based video management systems and edge-processing cameras is reshaping surveillance architecture, enabling scalable security ecosystems capable of processing high-volume video streams in real time.

The surveillance camera market has become strategically significant for governments, enterprises, and infrastructure operators seeking data-driven security and operational intelligence. AI-powered video analytics platforms are transforming surveillance from passive recording systems into proactive monitoring solutions capable of automated threat detection, crowd analysis, and predictive security management. Advanced edge-AI surveillance cameras deliver nearly 35% faster object recognition compared to traditional analog CCTV systems, enabling real-time response capabilities across high-traffic environments.

Asia-Pacific dominates in deployment volume due to extensive smart city surveillance programs, while North America leads in enterprise adoption with nearly 62% of large corporations integrating cloud-connected security monitoring platforms. By 2028, AI-enabled surveillance analytics systems are expected to improve incident detection accuracy by approximately 30%, significantly enhancing operational safety across transportation networks and urban infrastructure.

Compliance requirements surrounding privacy protection and ethical AI monitoring are shaping surveillance technology strategies, with firms committing to improved data governance standards and up to 20% reductions in system energy consumption through low-power AI camera designs by 2030. In 2024, a municipal security project in South Korea implemented intelligent video analytics across urban transport corridors and achieved a 27% reduction in traffic-related incidents. These developments position the surveillance camera market as a critical pillar supporting security resilience, regulatory compliance, and sustainable digital infrastructure growth.

Global smart city programs are significantly increasing the deployment of surveillance cameras across transportation networks, public spaces, and municipal infrastructure. More than 1,000 smart city initiatives worldwide now integrate intelligent video monitoring systems for traffic management, public safety, and environmental monitoring. AI-enabled surveillance cameras can analyze up to 30 video frames per second while detecting abnormal behavior, crowd density, or vehicle movement patterns in real time. Governments are increasingly installing network-connected surveillance cameras across highways, metro stations, and airports to enhance situational awareness. These systems also support predictive policing models and automated traffic enforcement, improving urban security efficiency and enabling authorities to respond to potential incidents more quickly and accurately.

Data privacy concerns and regulatory oversight are creating challenges for surveillance camera expansion in several developed markets. Regulations such as strict biometric data protection laws restrict the use of facial recognition and behavioral monitoring technologies. Public resistance to large-scale surveillance programs has also led to stricter compliance frameworks governing video storage, consent management, and personal data processing. Some regions require encrypted video transmission and limited retention periods for recorded footage, increasing operational complexity for surveillance operators. Additionally, compliance costs related to secure data storage infrastructure and cybersecurity protection can increase system implementation costs by nearly 20%, slowing adoption among small and medium enterprises that lack advanced IT security resources.

Artificial intelligence and machine learning technologies are unlocking new opportunities for intelligent surveillance applications across industries. Modern AI-enabled cameras can automatically identify objects, detect suspicious activities, and generate predictive alerts without continuous human monitoring. Retail chains are adopting AI video analytics to track customer movement patterns and improve store security, while manufacturing facilities deploy cameras for automated workplace safety monitoring. Edge computing capabilities allow surveillance cameras to process data locally, reducing bandwidth consumption by up to 40%. The rapid expansion of cloud-based video management systems also enables centralized monitoring of thousands of cameras across distributed facilities, creating scalable security ecosystems that support large enterprise operations and critical infrastructure protection.

Cybersecurity vulnerabilities represent a major challenge for modern surveillance camera networks connected to enterprise and public internet infrastructures. Network-connected cameras can become entry points for cyberattacks if not properly secured with encryption, authentication protocols, and firmware updates. Large-scale surveillance systems often require integration with access control systems, IoT sensors, and data analytics platforms, increasing system complexity and implementation time. Enterprises deploying thousands of cameras across distributed facilities must maintain secure network architecture and continuous software updates to prevent unauthorized access. Additionally, the growing volume of high-resolution video data requires significant storage infrastructure and high-bandwidth networks, creating operational challenges for organizations managing large surveillance deployments.

• Rapid Expansion of AI-Powered Video Analytics:

Artificial intelligence integration is significantly transforming surveillance camera capabilities, enabling automated threat detection, facial recognition, and behavioral analytics. More than 65% of newly installed surveillance cameras globally now include embedded AI analytics processors capable of analyzing 25–30 video frames per second in real time. Smart detection technologies improve anomaly recognition accuracy by nearly 40% compared to conventional motion-detection systems. Enterprises deploying AI-enabled surveillance cameras report a 28% improvement in security incident identification speed. Additionally, nearly 48% of metropolitan surveillance networks are integrating deep-learning algorithms for automated vehicle tracking, license plate recognition, and crowd density monitoring, allowing authorities to process thousands of video streams simultaneously while reducing manual monitoring workloads by approximately 35%.

• Transition Toward Cloud-Based Video Surveillance Systems:

Cloud video surveillance infrastructure is becoming a core architecture in modern surveillance deployments. Around 52% of new enterprise surveillance installations now rely on cloud-based video management platforms that enable centralized monitoring of distributed facilities. These platforms allow organizations to store up to 90 days of high-definition video footage while reducing on-site hardware infrastructure by nearly 30%. Cloud surveillance solutions also improve remote monitoring capabilities, enabling security teams to access live camera feeds across multiple locations via secure digital dashboards. Businesses adopting cloud-based surveillance solutions report operational efficiency improvements of nearly 22%, while automated system updates and AI analytics integration improve system reliability by more than 25% across large-scale surveillance networks.

• Growing Deployment of 4K and Ultra-High-Resolution Surveillance Cameras:

The adoption of ultra-high-definition imaging technology is rapidly increasing within modern surveillance systems. More than 45% of newly deployed enterprise surveillance cameras now support 4K resolution imaging, delivering four times the pixel density of traditional 1080p cameras. High-resolution cameras significantly enhance identification accuracy, enabling security teams to detect facial details, license plates, and object movements from distances exceeding 30 meters. In transportation hubs and public infrastructure facilities, ultra-high-definition cameras improve monitoring coverage by approximately 35%, reducing the number of cameras required per facility. Industrial facilities deploying high-resolution surveillance systems have reported up to 20% improvements in asset protection and operational monitoring efficiency.

• Rising Integration of Edge Computing in Smart Surveillance Systems:

Edge computing technology is reshaping surveillance camera architecture by allowing real-time data processing directly within camera devices. Approximately 40% of next-generation surveillance cameras now include built-in edge processors capable of executing AI algorithms locally without sending raw video data to central servers. This approach reduces network bandwidth usage by nearly 45% and lowers video transmission latency by more than 30%. Edge-enabled cameras can instantly detect suspicious activities, crowd movements, or restricted-area intrusions and generate automated alerts. In large smart city deployments, edge computing surveillance networks have demonstrated a 27% improvement in response times for security incidents while significantly lowering cloud storage requirements.

The surveillance camera market is segmented by type, application, and end-user industries, each reflecting evolving security requirements across commercial and public infrastructure environments. IP cameras dominate the technology landscape due to their advanced connectivity and high-resolution capabilities, while analog and hybrid systems remain in operation across legacy installations. Application demand is highest in public infrastructure and transportation monitoring, accounting for a substantial portion of global deployments due to urban safety initiatives. Retail security and industrial asset monitoring also represent key growth areas as businesses increasingly adopt AI-powered video analytics. From an end-user perspective, government agencies, commercial enterprises, and transportation authorities account for the majority of surveillance camera adoption, driven by security modernization programs and digital infrastructure investments.

The surveillance camera market is segmented into IP cameras, analog cameras, wireless cameras, and hybrid surveillance systems. IP cameras currently represent the leading segment, accounting for nearly 48% of global surveillance camera deployments due to their advanced networking capabilities, high-resolution imaging, and integration with AI-powered analytics platforms. These cameras support remote monitoring and cloud connectivity, allowing organizations to manage thousands of camera feeds simultaneously through centralized video management systems. Analog cameras still account for approximately 27% of active installations, primarily within legacy surveillance infrastructure in industrial facilities and small commercial establishments where upgrading network architecture may be costly. Wireless surveillance cameras represent another rapidly expanding category as enterprises increasingly demand flexible monitoring solutions that reduce installation complexity.

Among all product types, wireless surveillance cameras are the fastest-growing segment with an estimated growth rate of around 13% annually, driven by rapid adoption in residential security systems, small retail businesses, and temporary monitoring installations such as construction sites and outdoor events. These devices support quick deployment and mobile connectivity while maintaining high-definition video streaming capabilities. Hybrid surveillance systems combining analog infrastructure with IP-based analytics account for the remaining 25% of installations, offering cost-effective modernization for organizations transitioning from legacy systems to digital monitoring environments.

The surveillance camera market is widely deployed across multiple application environments including public infrastructure monitoring, commercial security, residential safety systems, and industrial asset protection. Public infrastructure surveillance currently accounts for approximately 38% of total camera deployments, driven by increasing investments in urban safety programs, traffic monitoring systems, and smart city security networks. Large metropolitan transit systems rely heavily on advanced surveillance cameras capable of monitoring passenger movement, crowd density, and emergency situations in real time. Commercial surveillance applications represent nearly 28% of total installations, with retail chains, corporate campuses, and logistics facilities using intelligent cameras to prevent theft, monitor operational efficiency, and improve workplace safety. Retail environments are increasingly integrating AI-powered surveillance analytics capable of tracking customer behavior and identifying suspicious activity within seconds.

The residential security segment is the fastest-growing application area with an estimated growth rate of around 14% annually, fueled by the expansion of smart home ecosystems and consumer demand for remote property monitoring. Connected home surveillance cameras allow homeowners to monitor live footage through mobile devices while receiving automated alerts for unusual activities. Industrial facilities and manufacturing plants account for the remaining 34% of deployments, where cameras are used for equipment monitoring, workplace safety compliance, and perimeter protection.

Government and public sector organizations represent the largest end-user segment, accounting for approximately 41% of surveillance camera deployments worldwide. Municipal authorities, transportation agencies, and law enforcement organizations rely heavily on surveillance infrastructure to monitor urban traffic, maintain public safety, and manage large-scale infrastructure systems. Public surveillance networks increasingly incorporate AI analytics capable of processing thousands of live video streams simultaneously. Commercial enterprises represent around 31% of total end-user adoption, with retail chains, financial institutions, and corporate campuses deploying surveillance cameras for asset protection, fraud prevention, and operational monitoring. Large retail stores often operate more than 100 surveillance cameras per facility to monitor store activity, inventory areas, and customer traffic patterns.

The residential sector is the fastest-growing end-user segment with an estimated growth rate of approximately 15% annually, supported by rapid expansion in smart home technology adoption. Modern residential surveillance systems allow homeowners to remotely monitor properties through smartphone applications while integrating with other smart home devices such as motion sensors and alarm systems. Industrial facilities, manufacturing plants, and logistics warehouses collectively account for the remaining 28% of market adoption, where surveillance cameras support workplace safety monitoring, automated production oversight, and supply chain security.

Region Asia-Pacific accounted for the largest market share at 44% in 2025 however, Region North America is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2026 and 2033.

Asia-Pacific leads global deployment with more than 350 million active surveillance cameras across urban infrastructure, transportation networks, and commercial facilities. China alone operates over 200 million cameras in public monitoring systems, while India has installed more than 5 million urban security cameras across major smart city initiatives. North America holds nearly 26% of global installations, driven by enterprise security modernization and AI-enabled monitoring adoption. Europe represents about 20% of the market, supported by transport infrastructure surveillance and strict compliance frameworks. Meanwhile, South America and the Middle East & Africa together account for approximately 10%, with rising deployment in airports, oil infrastructure, and urban development projects.

How are advanced enterprise security systems transforming surveillance infrastructure adoption?

North America accounts for approximately 26% of global surveillance camera deployments, driven primarily by strong demand from enterprise security, transportation infrastructure, and financial institutions. The United States represents nearly 80% of regional installations, with more than 85 million surveillance cameras deployed across commercial buildings, retail chains, airports, and logistics facilities. Federal infrastructure modernization programs and updated data protection regulations have accelerated adoption of encrypted cloud surveillance systems and AI-based video analytics. Financial institutions and healthcare facilities operate surveillance networks averaging 120–150 cameras per facility for security compliance. A leading regional player, Axis Communications, has expanded AI-enabled edge cameras capable of analyzing 30 video streams simultaneously, improving automated security detection. Regional consumer behavior shows higher enterprise adoption, particularly across healthcare and financial sectors.

What regulatory frameworks are shaping next-generation intelligent surveillance adoption?

Europe represents roughly 20% of global surveillance camera installations, supported by strong adoption in transportation hubs, government infrastructure, and retail environments. Key markets including Germany, the United Kingdom, and France collectively account for nearly 65% of regional deployments, with over 40 million surveillance cameras operating across these countries. Strict data protection regulations have encouraged adoption of privacy-focused surveillance technologies including encrypted storage and anonymized video analytics. Transportation networks across Europe deploy cameras for crowd monitoring and automated traffic management, particularly in metropolitan rail systems and airports. A European technology leader, Bosch Security Systems, has introduced AI-powered cameras capable of identifying 16 different object categories in real time. Regional consumer behavior reflects regulatory pressure, driving demand for privacy-compliant surveillance solutions with explainable AI monitoring capabilities.

How are large-scale smart city projects accelerating intelligent video monitoring deployment?

Asia-Pacific ranks as the largest surveillance camera market globally, accounting for more than 44% of worldwide installations and operating over 350 million surveillance cameras across urban and commercial infrastructure. Major consuming countries include China, India, Japan, and South Korea, with China alone deploying more than 200 million cameras in smart city monitoring systems. India has installed surveillance networks across 100 smart cities, with some metropolitan regions operating 20,000–30,000 cameras for traffic and public safety monitoring. The region benefits from strong manufacturing clusters producing over 40% of global surveillance hardware units annually. A major regional technology company, Hikvision, produces millions of AI-enabled cameras each year featuring edge processing capabilities and automated behavioral detection. Regional consumer behavior shows rapid growth driven by expanding urban infrastructure, e-commerce logistics facilities, and mobile-connected security applications.

How are urban safety initiatives and infrastructure upgrades expanding surveillance deployments?

South America accounts for approximately 6% of global surveillance camera installations, with Brazil and Argentina representing the largest national markets. Brazil operates more than 3 million surveillance cameras across municipal security systems, transportation networks, and retail centers. Urban safety programs in major cities have accelerated deployment of high-definition traffic monitoring cameras capable of processing 25 frames per second for real-time incident detection. Government-supported infrastructure development projects have also expanded surveillance installations across airports, seaports, and public transportation systems. A regional technology integrator, Intelbras, has deployed large-scale IP surveillance networks across municipal safety projects and commercial facilities. Regional consumer behavior shows strong demand in retail and public infrastructure sectors, where surveillance systems help reduce theft incidents and improve operational monitoring across urban environments.

How are infrastructure megaprojects driving demand for intelligent security monitoring systems?

The Middle East & Africa surveillance camera market represents nearly 4% of global deployments, supported by rapid infrastructure expansion across UAE, Saudi Arabia, and South Africa. Large-scale urban development initiatives and international event infrastructure projects have accelerated the installation of advanced surveillance systems across airports, commercial centers, and transportation corridors. Dubai operates more than 300,000 connected surveillance cameras as part of its smart city monitoring network. Oil and gas facilities across the Gulf region deploy high-resolution surveillance cameras for pipeline monitoring and industrial security compliance. A regional security technology provider, G4S Middle East, has implemented integrated surveillance systems across several infrastructure megaprojects using AI-based video analytics. Consumer behavior in the region shows strong demand from government and construction sectors seeking advanced monitoring systems to secure high-value infrastructure assets.

China – 34% market share: China dominates the surveillance camera market due to large-scale manufacturing capacity and extensive deployment of public security monitoring systems across urban infrastructure.

United States – 22% market share: The United States leads in enterprise surveillance adoption with strong demand from financial institutions, transportation hubs, and commercial security infrastructure.

The surveillance camera market features a moderately consolidated competitive landscape with more than 120 active global manufacturers and technology providers competing across hardware, software analytics, and integrated security solutions. The top five companies collectively account for approximately 48% of global market presence, reflecting strong competition among major surveillance technology vendors and emerging AI analytics firms. Market leaders continue to invest heavily in research and development to integrate artificial intelligence, edge computing, and high-resolution imaging capabilities into modern surveillance systems.

Product innovation remains the primary competitive strategy, with manufacturers launching cameras capable of processing 25–30 frames per second while performing real-time object detection, facial recognition, and behavior analysis. Strategic partnerships between surveillance hardware providers and cloud technology companies are also increasing, enabling scalable video management platforms capable of supporting thousands of camera feeds simultaneously. Over the past three years, more than 35 technology partnerships and system integration agreements have been announced to support smart city security infrastructure.

Competition is also intensifying in software-driven surveillance analytics, where vendors are developing AI-powered monitoring systems capable of identifying over 20 different security events automatically. Additionally, mergers and acquisitions within the security technology sector have increased by nearly 18% since 2022, as companies seek to expand their surveillance analytics capabilities and global distribution networks.

Hikvision

Dahua Technology

Axis Communications

Bosch Security Systems

Honeywell International

Hanwha Vision

Avigilon

Panasonic i-PRO

Uniview Technologies

Vivotek

Pelco

Tiandy Technologies

CP Plus

Intelbras

Zhejiang Uniview Technologies

Technological innovation is transforming the surveillance camera market as intelligent video systems evolve from basic monitoring tools into advanced data-driven security platforms. Modern IP surveillance cameras increasingly integrate artificial intelligence processors capable of performing object detection, facial recognition, and behavioral analysis directly at the device level. More than 60% of newly deployed enterprise surveillance cameras now support embedded AI analytics that can identify over 20 object categories, including vehicles, people, and restricted-area intrusions. Edge computing technology is also gaining traction, enabling cameras to process video locally and reduce network bandwidth consumption by nearly 40% while lowering response latency by approximately 30%.

High-resolution imaging technologies are another major development. Over 45% of newly installed surveillance systems now deploy 4K resolution cameras capable of capturing four times more image detail than standard 1080p cameras, improving identification accuracy in crowded environments such as airports and transportation hubs. Cloud-based video management platforms are expanding rapidly, allowing centralized monitoring of thousands of cameras across distributed locations. In addition, thermal imaging cameras are increasingly used in industrial and infrastructure monitoring, capable of detecting temperature variations within ±0.5°C for predictive maintenance and safety applications. Integration with IoT sensors, biometric authentication systems, and automated incident response software is further strengthening the technological capabilities of modern surveillance ecosystems.

• In April 2025, Axis Communications introduced the ARTPEC-9 system-on-chip platform designed for next-generation surveillance cameras. The processor enables advanced AI-driven analytics, including deep learning object classification and improved image processing for multi-stream video analytics, supporting high-resolution surveillance deployments across smart city and enterprise security infrastructure. Source: www.axis.com

• In October 2024, Bosch Security Systems launched a new generation of AI-enabled FLEXIDOME 8100i cameras featuring built-in deep learning analytics capable of recognizing multiple object classes simultaneously. The cameras support automated incident detection, traffic monitoring, and perimeter protection for transportation and critical infrastructure facilities. Source: www.boschsecurity.com

• In January 2024, Hanwha Vision introduced its Wisenet 9 AI-powered chipset designed for intelligent surveillance cameras. The technology improves image clarity in low-light conditions and enables on-device AI analytics capable of identifying objects and behavior patterns while reducing false alarm rates in high-density urban monitoring environments. Source: www.hanwhavision.com

• In September 2024, Hikvision released the AcuSense 3.0 smart video analytics platform integrated into new surveillance camera models. The system uses deep learning algorithms to differentiate human and vehicle movement from background activity, improving alarm accuracy by over 40% and enhancing automated perimeter monitoring capabilities. Source: www.hikvision.com

The Surveillance Camera Market Report provides a comprehensive evaluation of the global surveillance ecosystem, covering a wide range of technologies, deployment environments, and industry applications. The report analyzes more than 10 key product categories including IP cameras, analog systems, wireless cameras, hybrid surveillance platforms, thermal imaging cameras, and AI-enabled edge devices. It examines over 15 major application sectors such as public infrastructure monitoring, transportation security, retail surveillance, industrial facility protection, and residential smart security systems.

The report also evaluates technology trends across advanced imaging sensors, AI-driven video analytics, cloud-based video management platforms, and edge computing surveillance architecture. Geographic coverage spans more than 20 key national markets across five major regions, assessing deployment levels across urban security networks, enterprise infrastructure, and industrial monitoring systems. Additionally, the report reviews evolving regulatory frameworks related to data privacy, biometric identification, and secure video storage requirements.

Strategic analysis within the report includes market competition dynamics, technology innovation pipelines, and surveillance infrastructure modernization initiatives. The study further highlights emerging niche segments such as AI-enabled behavioral analytics cameras, smart traffic monitoring systems, and integrated IoT-based surveillance networks designed to support next-generation smart city and digital security ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

10% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hikvision, Dahua Technology, Axis Communications, Bosch Security Systems, Honeywell International, Hanwha Vision, Avigilon, Panasonic i-PRO, Uniview Technologies, Vivotek, Pelco, Tiandy Technologies, CP Plus, Intelbras, Zhejiang Uniview Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |