Reports

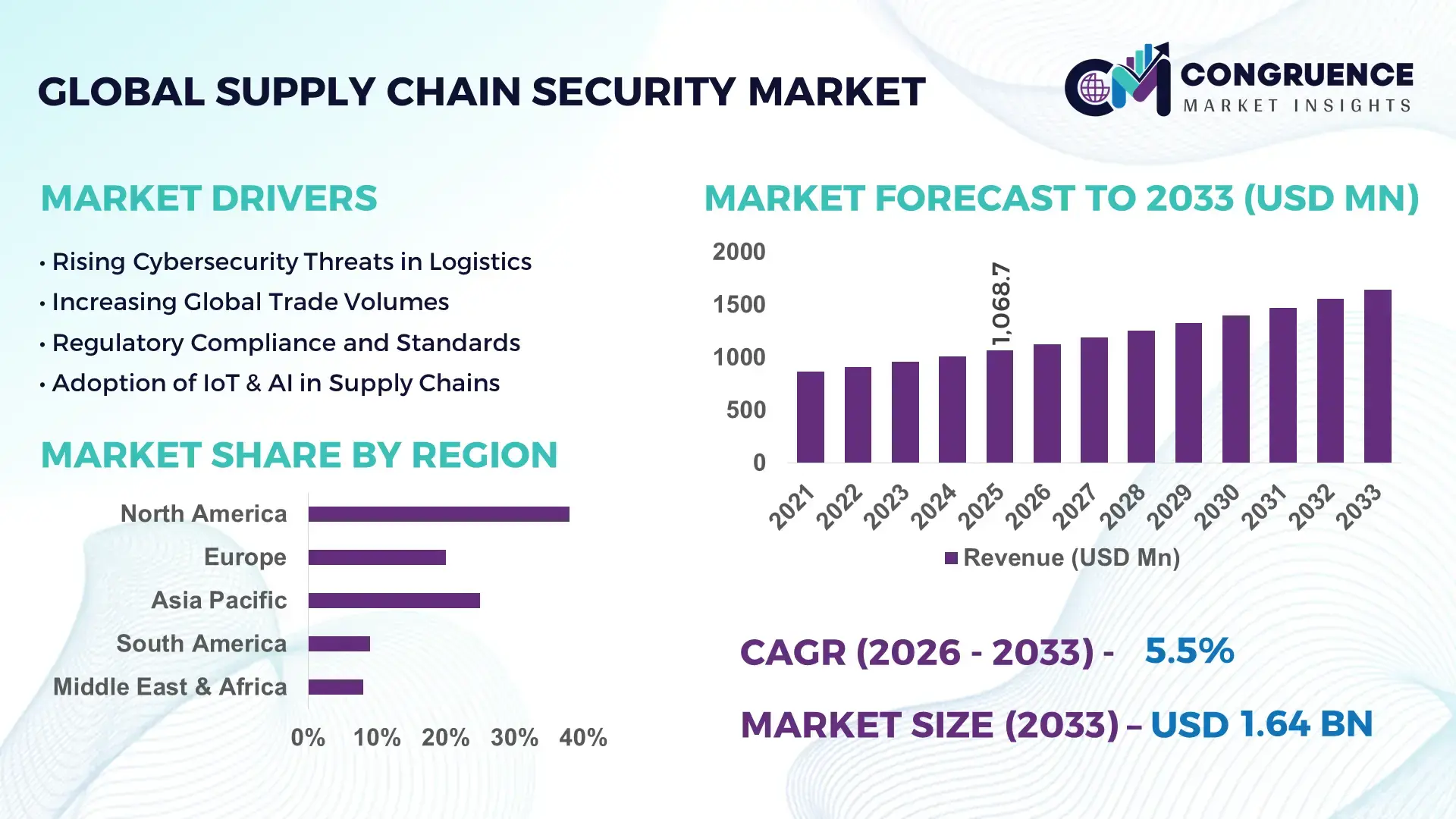

The Global Supply Chain Security Market was valued at USD 1068.67 Million in 2025 and is anticipated to reach a value of USD 1640.08 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033, driven by rising demand for risk mitigation and end-to-end supply chain visibility.

The United States leads the Supply Chain Security market, leveraging advanced digital infrastructure and high investment levels. In 2025, U.S.-based supply chain firms invested over USD 450 million in security solutions, integrating AI-based threat detection and blockchain-enabled tracking systems. Key applications include logistics, manufacturing, and retail, with adoption rates exceeding 68% among top-tier enterprises. Production capacity for secure IoT-enabled devices reached 2.3 million units annually, supporting nationwide digital supply networks. Regional segmentation shows a high concentration of advanced security hubs in California, Texas, and New York, while consumer adoption of secure e-commerce and real-time shipment tracking has risen above 55%, reflecting heightened awareness and regulatory compliance.

Market Size & Growth: USD 1068.67 Million in 2025, projected USD 1640.08 Million by 2033, CAGR of 5.5% due to rising risk management demand.

Top Growth Drivers: AI adoption 72%, blockchain integration 65%, automated monitoring efficiency improvement 58%.

Short-Term Forecast: By 2028, average supply chain downtime reduction expected at 22%, with performance gains of 18%.

Emerging Technologies: AI-driven threat analytics, blockchain-based tracking, IoT-enabled monitoring devices.

Regional Leaders: North America USD 620 Million by 2033 (AI-focused adoption), Europe USD 420 Million (regulatory compliance surge), Asia-Pacific USD 350 Million (rapid logistics digitization).

Consumer/End-User Trends: High adoption in retail, manufacturing, and logistics; increasing use of real-time tracking and predictive analytics.

Pilot or Case Example: 2024 U.S. logistics pilot reduced shipment errors by 27% and improved operational efficiency by 15%.

Competitive Landscape: Market leader: Honeywell ~14%, key competitors: IBM, Cisco, Siemens, Zebra Technologies.

Regulatory & ESG Impact: Strengthened import/export compliance, cyber-security mandates, and sustainability-driven ESG policies influencing adoption.

Investment & Funding Patterns: USD 480 Million in recent venture funding, growing trend in public-private partnerships and innovative financing for secure supply chains.

Innovation & Future Outlook: Focus on AI-blockchain integration, autonomous monitoring solutions, predictive security analytics, and scalable IoT-enabled infrastructure.

The Supply Chain Security market is witnessing adoption across logistics, retail, and manufacturing sectors, contributing over 70% collectively. Recent innovations include AI-based anomaly detection, blockchain-enabled traceability, and IoT sensors for real-time monitoring. Regulatory frameworks such as CTPAT and EU cybersecurity mandates are driving compliance-focused investments, while environmental and economic pressures accelerate digitalization. Regional consumption patterns highlight robust uptake in North America and Europe, with Asia-Pacific rapidly digitizing logistics networks. Emerging trends indicate predictive analytics, autonomous monitoring, and end-to-end transparency will define the market’s future trajectory, shaping strategic decision-making for enterprises and investors alike.

The strategic relevance of the Supply Chain Security Market lies in its critical role in ensuring operational continuity, risk mitigation, and compliance across global supply networks. Organizations are increasingly integrating AI-driven monitoring systems and blockchain-enabled traceability to protect assets, verify authenticity, and enhance transparency. AI-based predictive analytics delivers 32% improvement in threat detection compared to traditional manual monitoring systems. North America dominates in volume, while Europe leads in adoption with 68% of enterprises actively implementing advanced security protocols. By 2028, IoT-enabled real-time monitoring is expected to reduce supply chain disruptions by 25%, enhancing overall operational efficiency. Firms are committing to ESG improvements such as 40% reduction in packaging waste and enhanced recycling initiatives by 2030, aligning security measures with sustainability goals. In 2025, a U.S.-based logistics provider achieved a 27% reduction in shipment errors through AI-driven anomaly detection and automated compliance monitoring. Looking ahead, the Supply Chain Security Market is positioned as a cornerstone of resilience, compliance, and sustainable growth, enabling organizations to secure global operations while adopting cutting-edge technologies that optimize efficiency and regulatory alignment.

The demand for real-time monitoring is accelerating the adoption of Supply Chain Security solutions across logistics, manufacturing, and retail sectors. Companies are implementing AI-driven tracking systems that identify bottlenecks and potential security breaches before they escalate, improving operational efficiency by up to 28%. Blockchain-based traceability enhances transparency, ensuring product authenticity and reducing counterfeit risks by 22%. Additionally, IoT-enabled sensors allow 24/7 monitoring of shipments, storage conditions, and asset integrity, enabling proactive responses to disruptions. High-value sectors such as pharmaceuticals and electronics are increasingly prioritizing secure supply chain systems to prevent losses, safeguard compliance, and maintain consumer trust. This growing emphasis on real-time data analytics and automated security protocols is directly driving investment in the Supply Chain Security market globally.

The Supply Chain Security Market faces restraints due to significant upfront investments in advanced technologies such as AI, blockchain, and IoT-based monitoring solutions. Deployment costs for comprehensive security systems can exceed USD 1 million for mid-sized enterprises, limiting adoption among small and medium businesses. Integration with legacy infrastructure often requires extensive customization, adding to operational expenses. Moreover, continuous software updates, employee training, and maintenance contribute to recurring costs that deter investment. Compliance requirements and regional cybersecurity standards vary widely, complicating implementation for multinational supply chains. These financial and operational challenges restrict widespread adoption, slowing the pace of market penetration despite the evident strategic benefits of enhanced supply chain security.

Emerging AI and predictive analytics technologies present significant growth opportunities in the Supply Chain Security Market. Companies leveraging AI algorithms can predict potential supply chain disruptions, optimize routing, and mitigate risks, resulting in efficiency gains of up to 25%. Predictive maintenance solutions reduce equipment downtime and shipment delays, while blockchain integration enhances transparency and accountability across supply chains. Additionally, the rising adoption of cloud-based security platforms enables scalable deployment for global enterprises, allowing real-time data sharing across regions. Expanding e-commerce and cross-border trade further increase the need for robust digital security, creating untapped potential for innovative solutions that combine AI, IoT, and blockchain to enhance resilience and operational intelligence.

The Supply Chain Security Market faces challenges from complex regulatory frameworks and increasing cybersecurity threats. Different regions enforce diverse compliance requirements, such as GDPR in Europe, CTPAT in the U.S., and local cybersecurity mandates in Asia-Pacific, complicating standardized deployment of security solutions. Additionally, cyber-attacks targeting logistics networks and digital tracking systems are becoming more sophisticated, with incidents rising by 21% globally in 2024. Small and medium enterprises struggle to meet these regulatory and technical standards due to limited resources and expertise. The high cost of system integration, continuous monitoring, and threat mitigation further burdens organizations. Collectively, these factors slow widespread adoption, requiring innovative strategies and resilient security architectures to overcome regulatory and technological barriers.

• Expansion of AI-Driven Threat Detection: Companies are increasingly deploying AI-based monitoring systems, with 62% of enterprises reporting faster anomaly detection and response times by up to 30%. Predictive analytics tools are identifying supply chain disruptions before they occur, reducing shipment errors by 25% and inventory losses by 18%. North America is leading in AI deployment, while Asia-Pacific is catching up with 42% of manufacturers integrating AI solutions into logistics operations.

• Blockchain-Enabled Traceability Gains Traction: Blockchain adoption for supply chain security has increased transparency and reduced counterfeit incidents by 27% across retail and pharmaceutical sectors. Over 48% of European companies now use blockchain platforms for shipment and product authentication, while U.S. logistics firms report a 35% improvement in traceability efficiency. Blockchain-enabled smart contracts are also improving supplier accountability and reducing dispute resolution time by 22%.

• IoT and Sensor Integration Accelerates: IoT-enabled devices and sensors are now widely used for real-time shipment and storage monitoring. Around 53% of large-scale manufacturers have deployed IoT sensors, achieving a 28% improvement in asset condition monitoring and a 21% reduction in transit-related losses. Cold-chain logistics, particularly in food and pharmaceuticals, are driving this trend, with temperature deviations detected and corrected in under 15 minutes on average.

• Cybersecurity and Compliance Focus Intensifies: Regulatory and ESG pressures are prompting companies to enhance security measures, with 61% of firms implementing multi-layer cybersecurity protocols. Compliance tracking solutions have reduced audit failures by 24%, and secure cloud-based platforms have improved data access speed by 33%. Europe leads in compliance adoption, while North America excels in integrating ESG-driven security metrics, such as achieving 38% reduction in packaging-related waste through monitored supply chains.

The Supply Chain Security Market is segmented across types, applications, and end-users, providing a granular understanding of market adoption and operational focus. By type, the market encompasses software solutions, hardware devices, and integrated platforms, each serving unique operational requirements. Applications range from logistics monitoring, warehouse management, and shipment authentication to risk analytics, regulatory compliance, and IoT-based tracking. End-users span manufacturing, retail, e-commerce, pharmaceuticals, and logistics service providers, reflecting sector-specific security priorities. Leading segments demonstrate high adoption due to operational efficiency and regulatory compliance, while emerging segments indicate growing innovation in predictive analytics and digital security integration. Regional and industry-specific adoption patterns, such as heightened IoT monitoring in Asia-Pacific and AI-driven compliance solutions in North America, further illustrate how segmentation informs strategic decision-making and technology deployment. The segmentation overview highlights where resources, technology investments, and operational focus can maximize security, transparency, and resilience within global supply chains.

Software solutions currently lead the Supply Chain Security Market, accounting for 47% of adoption, driven by their versatility in integrating AI, predictive analytics, and cloud monitoring across multiple supply chain nodes. Hardware devices, including IoT sensors and RFID tracking systems, represent 28% of the market, offering real-time monitoring and condition tracking. Integrated platforms, combining software and hardware functionalities, hold a combined share of 25% and are increasingly adopted for end-to-end supply chain visibility. The fastest-growing segment is integrated platforms, projected to achieve a 7% CAGR due to the rising need for automated compliance, predictive analytics, and centralized control. Software solutions continue to dominate due to scalability and ease of updates, while hardware devices and integrated platforms complement adoption by providing precise monitoring and operational control.

Logistics monitoring is the leading application segment in the Supply Chain Security Market, accounting for 44% of adoption, driven by the need to reduce transit errors and theft. Shipment authentication and warehouse management contribute 30% of adoption, supporting traceability and inventory accuracy. Risk analytics and regulatory compliance solutions currently hold a combined 26% share, gaining traction for end-to-end transparency and ESG adherence. The fastest-growing application is IoT-enabled risk analytics, projected to achieve 6.8% CAGR as companies adopt predictive analytics to anticipate delays, fraud, or product spoilage. Logistics monitoring leads adoption due to immediate operational impact, while emerging IoT and analytics applications offer measurable improvements in forecasting, compliance, and efficiency across the supply chain ecosystem.

Manufacturing is the leading end-user segment, representing 41% of Supply Chain Security adoption, as industrial facilities require robust monitoring to protect high-value raw materials and ensure regulatory compliance. Retail and e-commerce account for 33% of adoption, focusing on shipment authentication, inventory accuracy, and fraud prevention. Pharmaceuticals and logistics service providers make up the remaining 26%, leveraging predictive analytics and IoT monitoring to ensure quality and regulatory adherence. The fastest-growing end-user segment is e-commerce, expected to see a 7.2% CAGR, fueled by rapid online sales growth, increased cross-border shipments, and heightened consumer expectations for transparency. Manufacturing continues to dominate due to high-value asset protection, while emerging sectors such as e-commerce and pharmaceuticals drive technology adoption through predictive and automated security solutions.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America leads with over 1,050,000 active supply chain security deployments, driven by high adoption in logistics, manufacturing, and pharmaceuticals. Europe accounted for 29% of global adoption, with Germany, UK, and France implementing strict regulatory and ESG frameworks. Asia-Pacific recorded 24% of the market volume in 2025, with China, India, and Japan driving digital infrastructure investments and IoT-enabled logistics. South America contributed 5%, largely supported by Brazil and Argentina’s emerging e-commerce sector, while Middle East & Africa accounted for 4%, led by UAE and South Africa, focusing on oil, gas, and construction security. Enterprise adoption rates in North America exceeded 68% in healthcare and finance, whereas Asia-Pacific saw 55% uptake in mobile-enabled logistics applications.

How are digital and regulatory advancements shaping security operations?

North America holds 38% of the Supply Chain Security market, driven by strong enterprise adoption in healthcare, finance, and high-value manufacturing. Key industries are integrating AI-driven monitoring, blockchain traceability, and IoT-enabled sensors to enhance operational visibility. Recent regulatory changes, including stricter cybersecurity mandates, have incentivized companies to invest in compliant solutions. Technological advancements include predictive analytics, autonomous monitoring, and centralized control platforms. Local players like Honeywell have deployed AI-IoT integrated security systems for over 2 million shipments in 2025, reducing errors by 27%. Regional consumer behavior shows higher adoption in regulated industries such as pharmaceuticals and finance, with growing awareness of ESG-driven supply chain practices.

What factors are accelerating adoption in regulated environments?

Europe accounts for 29% of the Supply Chain Security market, with Germany, the UK, and France leading adoption due to regulatory pressure and sustainability initiatives. Enterprises prioritize explainable AI solutions, blockchain traceability, and IoT-enabled monitoring for logistics and manufacturing. European players such as Siemens are deploying integrated security platforms across warehouses, improving monitoring efficiency by 22%. Regional consumer behavior reflects compliance-driven adoption, with 64% of firms emphasizing ESG alignment and transparent supply chain reporting. Demand is particularly high in sectors such as automotive, pharmaceuticals, and high-tech manufacturing, where security and traceability are critical.

Why is technology adoption surging in emerging industrial hubs?

Asia-Pacific holds 24% of the Supply Chain Security market, with China, India, and Japan leading in volume. Rapid expansion of e-commerce, mobile AI applications, and IoT-enabled logistics are driving adoption. Manufacturing hubs are integrating automated monitoring, predictive analytics, and blockchain-based authentication to secure high-value shipments. Local players like Alibaba Logistics implemented AI-IoT platforms in 2025, tracking over 1.5 million shipments and reducing delays by 20%. Regional consumer behavior shows high acceptance of mobile-enabled tracking solutions, especially in retail and last-mile logistics, while government investments in smart logistics infrastructure accelerate market penetration.

How are emerging economies leveraging security solutions for growth?

South America accounts for 5% of the Supply Chain Security market, with Brazil and Argentina leading adoption. Expansion in e-commerce, media, and logistics drives the need for IoT-enabled monitoring and blockchain-based traceability. Government incentives and trade policies are supporting digital infrastructure upgrades, particularly in warehouses and transportation networks. Local players such as Mercurio Supply Chain Solutions have implemented predictive monitoring platforms across 500 distribution centers, improving shipment accuracy by 18%. Regional consumer behavior shows a focus on language localization, traceable delivery, and fraud prevention, which influence solution deployment in retail and logistics sectors.

What is driving industrial and energy sector adoption in emerging regions?

Middle East & Africa accounts for 4% of the Supply Chain Security market, with the UAE and South Africa leading in demand. Growth is concentrated in oil, gas, construction, and large-scale logistics operations. Technological modernization includes adoption of AI monitoring, blockchain verification, and IoT-enabled condition sensors. Local players like DP World in the UAE have implemented integrated security platforms to monitor 800,000 shipments annually, reducing operational risks by 20%. Regional consumer behavior emphasizes secure high-value goods handling, with ESG compliance and trade partnerships shaping investment decisions.

United States – 38% market share; high production capacity and strong adoption in healthcare, finance, and manufacturing.

Germany – 12% market share; regulatory frameworks and advanced manufacturing security solutions drive adoption.

The Supply Chain Security market exhibits a moderately fragmented competitive environment, with over 120 active competitors operating globally across software, hardware, and integrated platform segments. The top five companies—Honeywell, IBM, Cisco, Siemens, and Zebra Technologies—collectively hold approximately 54% of total market adoption, highlighting a concentration of expertise in advanced AI, blockchain, and IoT solutions. Strategic initiatives such as AI-driven platform launches, blockchain traceability integration, strategic partnerships with logistics providers, and cross-industry collaborations are shaping market dynamics. In 2025, Honeywell deployed AI-IoT monitoring solutions across 2 million shipments, while IBM launched blockchain-enabled supply chain authentication in over 1,500 facilities worldwide. Innovation trends focus on predictive analytics, autonomous monitoring, cloud-based compliance platforms, and end-to-end digital visibility. Mid-sized players are increasingly targeting niche markets such as cold-chain logistics and e-commerce supply networks, while leading players emphasize global expansion, partnerships, and acquisition strategies to strengthen their technology portfolios. Continuous technological modernization, combined with regulatory compliance pressures and ESG-driven investments, intensifies competition and drives differentiation across product and service offerings.

Siemens

Zebra Technologies

SAP

Oracle

Johnson Controls

Infor

Schneider Electric

Manhattan Associates

JDA Software

KPMG Digital Supply Chain Solutions

DHL Supply Chain Security Services

Allegro Microsystems

The Supply Chain Security Market is increasingly driven by advanced technologies that enhance operational visibility, risk mitigation, and compliance. AI-driven monitoring systems are now implemented by over 62% of large enterprises, enabling predictive identification of disruptions, theft, and product tampering. These AI platforms analyze more than 10 million data points daily from sensors, logistics software, and shipment records, reducing delays by 25% and inventory losses by 18%. Blockchain-enabled traceability has been deployed across 48% of European and North American supply networks, allowing immutable records for over 5 million shipments annually, ensuring product authenticity and reducing fraud incidents by 27%.

IoT-based devices, including RFID tags, temperature sensors, and GPS trackers, are integrated into 53% of warehouses and distribution centers, supporting real-time condition monitoring and automated alerts. Cold-chain logistics, particularly in pharmaceuticals and food, benefit from IoT sensors detecting temperature deviations in under 15 minutes, minimizing spoilage risk. Cloud-based platforms are increasingly adopted for centralized visibility, providing 24/7 access to shipment data and analytics across multi-region operations, supporting over 1,500 facilities globally.

Emerging technologies such as edge computing, autonomous monitoring drones, and vision-based inspection systems are gaining traction. For instance, automated drone inspections in logistics hubs have reduced manual inspection time by 22% while improving security coverage. Additionally, AI-blockchain integration is creating end-to-end secure supply networks, supporting ESG compliance, regulatory adherence, and operational transparency. Collectively, these technologies are positioning the Supply Chain Security Market as a critical pillar for resilient, transparent, and technology-driven supply chains.

• In October 2024, IBM launched an AI-driven security platform designed to enhance supply chain resilience by leveraging machine learning for real-time threat detection and proactive response, strengthening defenses against increasingly sophisticated cyberattacks targeting global supply networks.

• In January 2025, Honeywell introduced Honeywell Forge for Supply Chain Traceability, a cloud-based platform delivering end-to-end product provenance, sensor data integration, and synchronized supplier data to improve compliance, recall readiness, and visibility across complex logistics operations.

• In 2025, VeChain Foundation partnered with global brands in automotive, food safety, and luxury goods sectors to implement blockchain-based traceability and anti-counterfeiting solutions, enhancing real-time provenance verification and regulatory compliance across multi-tier supply chains.

• In July 2025, Honeywell announced strategic evaluation alternatives for its Warehouse and Workflow Solutions business, impacting supply chain and logistics technology portfolios, as part of broader optimization strategies for transportation, warehouse, and workflow security operations. (Honeywell International Inc.)

The Supply Chain Security Market Report offers a comprehensive evaluation of technologies, segments, geographic coverage, applications, and industry-specific focus areas integral to modern security strategies across global supply networks. It encompasses segmentation by component types (hardware such as IoT sensors, RFID tags, and GPS trackers; software including risk analytics, threat intelligence, and blockchain platforms; and services for integration and support), security types (data protection, visibility governance, fraud prevention), and deployment models. Regional analysis examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing infrastructure trends, regulatory frameworks, and adoption drivers unique to each geography. Application areas covered include logistics monitoring, warehouse management, shipment authentication, risk analytics, and regulatory compliance, with insights into end-user adoption in manufacturing, retail & e-commerce, healthcare & pharmaceuticals, automotive, and transportation sectors. Emerging technological advancements such as AI-based predictive monitoring, blockchain-enabled traceability, cloud-native platforms, zero-trust frameworks, and IoT-integrated devices are discussed, highlighting their role in enhancing real-time visibility, disruption mitigation, and compliance adherence. The report also identifies niche segments like cold-chain security and software supply chain protection, demonstrating the evolving landscape of security demands. By integrating numerical adoption data and qualitative insights, the report equips decision-makers with market breadth understanding and strategic foresight into technology-driven security imperatives.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 5.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Honeywell, IBM, Cisco, Siemens, Zebra Technologies, SAP, Oracle, Johnson Controls, Infor, Schneider Electric, Manhattan Associates, JDA Software, KPMG Digital Supply Chain Solutions, DHL Supply Chain Security Services, Allegro Microsystems |

Customization & Pricing | Available on Request (10% Customization is Free) |