Reports

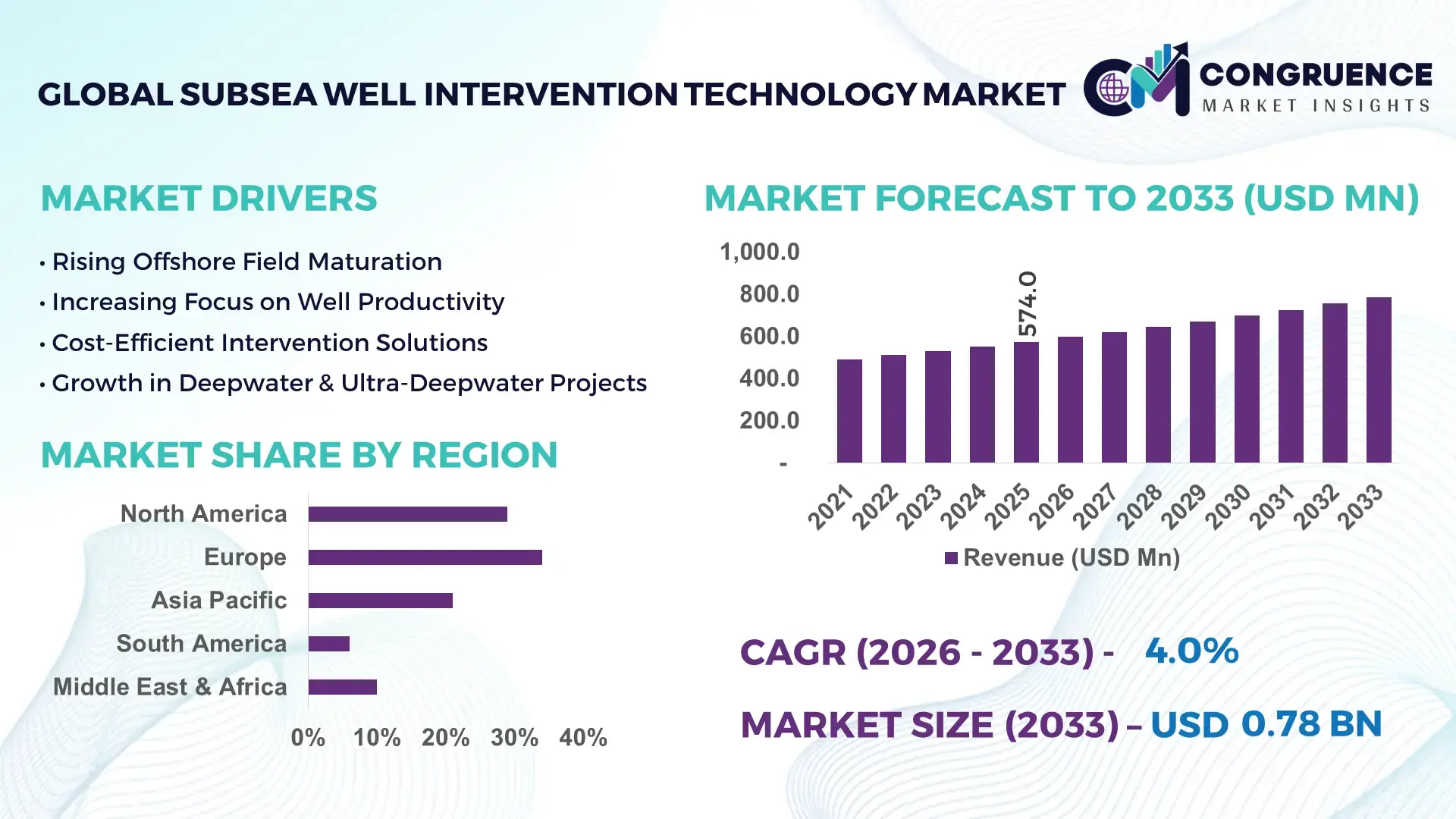

The Global Subsea Well Intervention Technology Market was valued at USD 574.0 Million in 2025 and is anticipated to reach a value of USD 785.0 Million by 2033 expanding at a CAGR of 3.99% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily supported by increasing offshore brownfield redevelopment and the need to enhance recovery rates from mature subsea reservoirs through cost-efficient light and heavy intervention systems.

Norway continues to demonstrate strong operational depth in subsea well intervention, with over 9,000 km of subsea pipelines and more than 500 subsea wells installed across the Norwegian Continental Shelf. In 2024 alone, investments in subsea tie-backs and intervention-ready infrastructure exceeded USD 8.5 billion, with digitalized intervention vessels supporting up to 35% faster campaign turnaround compared to traditional rigs. Approximately 60% of new field developments in Norwegian waters utilize light well intervention (LWI) vessels, and electrified subsea systems are reducing operational emissions by nearly 30% per project. The country’s integration of autonomous underwater vehicles (AUVs) and real-time subsea monitoring platforms has increased predictive maintenance accuracy by 25%, reinforcing its advanced production and technology deployment capacity.

Market Size & Growth: Valued at USD 574.0 Million in 2025, projected to reach USD 785.0 Million by 2033 at a CAGR of 3.99%, driven by rising subsea asset life-extension projects and offshore production optimization.

Top Growth Drivers: 42% increase in mature offshore field redevelopment, 35% efficiency improvement via light well intervention vessels, 28% rise in subsea digital monitoring adoption.

Short-Term Forecast: By 2028, integrated digital intervention systems are expected to reduce offshore intervention costs by 18% and improve well uptime by 22%.

Emerging Technologies: Deployment of autonomous underwater vehicles (AUVs), real-time fiber-optic subsea monitoring, and electrically powered intervention control systems.

Regional Leaders: North America projected at USD 240.0 Million by 2033 with deepwater Gulf projects; Europe at USD 210.0 Million supported by North Sea electrification; Asia-Pacific at USD 165.0 Million driven by offshore gas expansion.

Consumer/End-User Trends: Offshore operators prioritize light well intervention (LWI) systems, representing over 48% of interventions due to lower vessel dependency and reduced downtime.

Pilot or Case Example: In 2024, a North Sea operator achieved 27% downtime reduction using digitally integrated LWI vessels with predictive analytics.

Competitive Landscape: Schlumberger leads with approximately 18% share, followed by Halliburton, Baker Hughes, TechnipFMC, and Oceaneering International.

Regulatory & ESG Impact: Offshore methane reduction mandates and 30% emission cut targets across EU waters are accelerating adoption of electric subsea intervention technologies.

Investment & Funding Patterns: Over USD 22.0 billion allocated globally (2023–2025) toward subsea production enhancement, with hybrid vessel retrofits and digital twin platforms attracting private capital.

Innovation & Future Outlook: Integration of AI-driven reservoir analytics, remote-operated intervention vessels, and carbon-neutral subsea production frameworks will define next-phase asset optimization strategies.

Subsea well intervention demand is primarily led by offshore oil (approx. 62%) and offshore gas (38%) projects, with light well intervention systems accounting for nearly half of operational deployments. Recent innovations in electrically actuated subsea trees and fiber-optic diagnostics are improving well integrity monitoring accuracy by 20–25%. Stricter methane emission frameworks and electrification mandates in Europe and North America are reshaping procurement patterns, while Asia-Pacific offshore gas developments are strengthening long-term deployment pipelines.

The Subsea Well Intervention Technology Market plays a strategic role in extending the productive life of offshore reservoirs while optimizing capital allocation in mature fields. Operators are increasingly prioritizing intervention-based production enhancement, where light well intervention (LWI) delivers up to 35% lower operational expenditure compared to conventional drilling rigs. Electrified subsea control systems deliver 20% energy efficiency improvement compared to hydraulic control standards, significantly reducing lifecycle operating intensity.

From a regional standpoint, North America dominates in intervention volume due to deepwater Gulf projects, while Europe leads in technology adoption with nearly 65% of offshore operators integrating digital subsea monitoring platforms. By 2028, AI-enabled predictive maintenance systems are expected to improve well uptime by 25% and reduce unplanned intervention campaigns by 18%. Firms are committing to ESG targets including 30% operational emission reduction by 2030 through electrified subsea infrastructure and hybrid-powered intervention vessels.

In 2024,Equinor achieved a 26% improvement in intervention turnaround time by deploying integrated digital twin simulations and remotely operated subsea tooling across North Sea assets. Over the next decade, capital allocation will increasingly favor modular, vessel-based LWI systems capable of supporting multi-well campaigns in a single deployment cycle, improving asset resilience.

As offshore operators balance decarbonization commitments with production stability, the Subsea Well Intervention Technology Market will remain a pillar of operational resilience, regulatory compliance, and sustainable offshore energy development.

The Subsea Well Intervention Technology Market is shaped by offshore production optimization strategies, aging subsea infrastructure, and regulatory pressure for safer and lower-emission operations. Over 60% of global offshore wells are classified as mature, requiring periodic stimulation, logging, and maintenance interventions to sustain output levels. Light well intervention vessels have increased deployment frequency by approximately 30% in deepwater fields due to lower mobilization costs and improved safety metrics. Technological integration such as real-time data acquisition, remote operations centers, and AI-driven diagnostics is transforming intervention planning cycles, reducing vessel idle time and improving campaign predictability. Simultaneously, environmental compliance requirements are pushing operators toward electrified subsea systems and reduced-flaring intervention techniques.

More than half of global offshore wells have been operational for over 15 years, leading to rising requirements for well stimulation, scale removal, and integrity diagnostics. Mature fields typically experience 6–8% annual natural production decline, prompting operators to deploy intervention solutions to restore output. Light well intervention systems reduce campaign costs by nearly 25% compared to conventional drilling-based methods, while enabling multi-well servicing within a single mobilization cycle. Offshore operators report up to 20% incremental recovery improvements following structured intervention programs. Growing subsea tie-back developments and satellite field connections are further expanding demand for rapid-response intervention technologies, particularly in deepwater basins exceeding 1,500 meters depth.

Subsea intervention campaigns require specialized vessels, remotely operated vehicles (ROVs), and high-pressure control systems, with daily vessel charter rates often exceeding USD 150,000. Weather volatility in offshore regions can reduce operational windows by up to 20% annually, impacting scheduling efficiency. Equipment mobilization and compliance testing add additional lead time, while subsea system compatibility challenges across legacy installations complicate tool standardization. Furthermore, skilled subsea engineering personnel shortages—estimated at nearly 15% workforce gap in key offshore hubs—limit project scalability. These structural and financial barriers constrain smaller operators from adopting advanced intervention technologies despite clear performance benefits.

Digital twin modeling and AI-enabled diagnostics present measurable improvements in intervention planning accuracy, reducing non-productive time by up to 22%. Electrified subsea production systems lower hydraulic fluid dependency and reduce carbon intensity by nearly 30% per installation. Remote-operated intervention vessels minimize offshore crew size by approximately 18%, improving safety and compliance metrics. Emerging offshore gas developments in Asia-Pacific and West Africa are incorporating intervention-ready infrastructure at the design stage, creating long-term equipment demand. Autonomous underwater inspection platforms capable of operating beyond 3,000 meters depth further expand operational reach and enable predictive maintenance cycles.

Offshore operators must comply with stringent well integrity verification standards, environmental discharge regulations, and methane emission monitoring frameworks. In European waters, operators are required to conduct periodic integrity testing at defined intervals, increasing procedural workload by nearly 20%. Decommissioning obligations for aging subsea wells add further financial pressure, with abandonment costs sometimes exceeding 40% of original installation expenditure. Cross-border licensing requirements and safety certification standards can delay project approvals by several months. Additionally, stricter ESG reporting obligations demand real-time operational transparency, necessitating costly digital integration upgrades across legacy assets.

Accelerated Deployment of Light Well Intervention (LWI) Vessels: Over 48% of subsea interventions are now conducted using LWI vessels, reducing campaign costs by 25% and shortening mobilization time by 30% compared to rig-based operations. Deepwater operators report up to 22% improvement in well uptime through vessel-based multi-well servicing programs.

Integration of Digital Twin and Predictive Analytics Platforms: Nearly 55% of offshore operators have implemented real-time subsea monitoring solutions, improving failure prediction accuracy by 25% and lowering unplanned shutdown incidents by 18%. AI-based analytics platforms reduce diagnostic time by approximately 20%.

Electrification of Subsea Production Systems: Around 40% of new North Sea developments utilize electrically actuated subsea trees, cutting hydraulic fluid usage by 35% and lowering operational emissions by nearly 30%. Electrified intervention tooling enhances energy efficiency and reliability in high-pressure environments.

Expansion into Ultra-Deepwater Projects: Intervention systems rated beyond 3,000 meters water depth have grown by 28% in deployment over the past three years. Advanced remotely operated vehicles (ROVs) now support 24-hour continuous monitoring cycles, improving operational safety by 15% and enabling high-pressure well diagnostics in extreme subsea environments.

The Subsea Well Intervention Technology Market is segmented by type, application, and end-user, reflecting the operational diversity of offshore production environments. Technology selection is largely influenced by water depth, well complexity, reservoir maturity, and regulatory requirements. Light well intervention systems are widely adopted in mature offshore basins where cost optimization and rapid mobilization are critical, while heavy well intervention systems remain essential for complex recompletion and deepwater mechanical operations.

From an application standpoint, well stimulation and integrity management represent core demand centers, particularly in aging offshore assets experiencing 6–8% natural production decline annually. Inspection, repair, and maintenance (IRM) operations are expanding as operators prioritize predictive diagnostics and regulatory compliance. End-user segmentation highlights offshore oil operators as primary adopters, with national oil companies and integrated energy majors investing heavily in digitalized and electrified intervention infrastructure. Independent offshore operators are increasingly leveraging modular vessel-based solutions to reduce capital exposure while maintaining asset performance benchmarks.

The Subsea Well Intervention Technology Market by type includes Light Well Intervention (LWI) Systems, Heavy Well Intervention (HWI) Systems, Through-Tubing Intervention Tools, and Coiled Tubing & Wireline Systems. Light Well Intervention systems currently account for approximately 46% of total adoption due to their lower mobilization costs and ability to service multiple wells during a single campaign. Compared to heavy systems, LWI vessels reduce operational expenditure by nearly 25% and improve turnaround time by 30%, making them the preferred option for mature offshore fields. Heavy Well Intervention systems hold close to 28% share, primarily deployed for complex recompletion tasks and deepwater mechanical repairs requiring rig-based infrastructure. Through-tubing intervention tools represent about 16% of deployments, enabling scale removal, logging, and zonal isolation without retrieving production tubing. Coiled tubing and wireline systems collectively contribute nearly 10%, supporting high-pressure well diagnostics and targeted stimulation in niche environments. Heavy Well Intervention is projected to grow at approximately 4.8% CAGR, driven by increasing ultra-deepwater developments exceeding 2,000 meters and the need for complex well integrity restoration.

In 2024, the Norwegian Offshore Directorate reported that more than 60% of intervention campaigns on the Norwegian Continental Shelf utilized light well intervention vessels, improving campaign efficiency across over 120 subsea wells.

By application, the market includes Well Stimulation, Inspection, Repair & Maintenance (IRM), Sand Control & Scale Removal, and Well Logging & Diagnostics. Well Stimulation leads with nearly 38% share, as operators seek to counteract reservoir pressure decline and restore production capacity. Intervention-led stimulation programs have demonstrated up to 20% incremental recovery improvements in mature subsea fields. Inspection, Repair & Maintenance accounts for approximately 27% of total activity, supported by increasingly stringent offshore integrity regulations and digital monitoring adoption. Sand control and scale removal contribute around 18%, particularly in high-sediment offshore environments. Well logging and diagnostics represent roughly 17%, benefiting from fiber-optic and real-time reservoir data integration. Inspection, Repair & Maintenance is the fastest-growing application, expanding at an estimated 5.1% CAGR due to predictive analytics integration and mandatory periodic integrity testing in European and North American waters. In 2025, more than 44% of offshore operators globally reported piloting digital subsea monitoring systems to enhance intervention planning accuracy. Additionally, nearly 52% of deepwater projects incorporated predictive maintenance analytics into IRM workflows.

In 2024, the U.S. Bureau of Safety and Environmental Enforcement confirmed increased integrity verification activities across Gulf of Mexico subsea wells, covering more than 1,800 active offshore completions.

End-user segmentation includes Offshore Oil Operators, Offshore Gas Producers, National Oil Companies (NOCs), and Independent Offshore Operators. Offshore Oil Operators represent the leading segment with approximately 58% share, driven by the higher number of mature oil fields requiring frequent stimulation and integrity interventions. Offshore Gas Producers account for around 24%, particularly in Asia-Pacific where new gas tie-back projects are expanding subsea infrastructure. National Oil Companies collectively contribute nearly 12%, leveraging state-backed capital to deploy electrified subsea intervention systems. Independent Offshore Operators make up the remaining 6%, often prioritizing vessel-based light intervention models to minimize capital commitment. Offshore Gas Producers are the fastest-growing end-user segment, expanding at an estimated 5.4% CAGR due to rising LNG-linked offshore gas developments and intervention-ready infrastructure investments. In 2025, approximately 47% of offshore energy enterprises globally indicated plans to increase spending on digital well integrity monitoring platforms. Additionally, nearly 39% of national oil companies reported transitioning toward electrified subsea systems to align with emission reduction targets.

In 2024, Equinor confirmed expanded deployment of digitally enabled light well intervention vessels across multiple North Sea assets, covering over 30 active subsea fields to enhance production continuity and integrity compliance.

Europe accounted for the largest market share at 34% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Europe’s leadership is supported by more than 1,500 active offshore wells across the North Sea and Norwegian Continental Shelf, where over 60% of subsea fields require periodic intervention to sustain output. North America follows with 29% share, driven by deepwater Gulf of Mexico projects exceeding 1,800 meters water depth. Asia-Pacific holds approximately 21% share, with expanding offshore gas developments in China, Australia, and India. The Middle East & Africa represent 10%, while South America contributes nearly 6%, led by Brazil’s pre-salt basins. Across regions, nearly 48% of intervention campaigns utilize light well intervention vessels, and over 52% of offshore operators are integrating digital subsea monitoring to improve uptime and integrity compliance.

North America accounts for approximately 29% of the global Subsea Well Intervention Technology Market, supported primarily by deepwater and ultra-deepwater projects in the Gulf of Mexico. More than 1,800 active offshore wells operate in water depths beyond 1,500 meters, creating sustained demand for light and heavy intervention systems. Offshore oil production exceeding 1.7 million barrels per day reinforces consistent intervention cycles for well stimulation and integrity management. Regulatory oversight from federal offshore authorities has intensified integrity testing requirements, increasing inspection activity by nearly 18% over the past three years. Digital transformation trends show that over 55% of offshore operators in this region deploy predictive analytics platforms for intervention scheduling. Schlumberger has expanded remotely operated intervention capabilities in the Gulf, integrating AI-based diagnostics that reduced non-productive time by 20% during multi-well campaigns. Regional enterprise behavior indicates strong adoption of high-specification vessels and hybrid-powered systems to meet environmental compliance benchmarks.

Europe leads the Subsea Well Intervention Technology Market with a 34% share, supported by extensive North Sea infrastructure across the UK and Norway. Over 500 subsea fields operate in the region, and nearly 60% are classified as mature assets requiring routine intervention. The UK and Norway collectively account for more than 70% of regional offshore intervention activity. Sustainability mandates across European waters require methane emission reductions of up to 30% by 2030, accelerating adoption of electrically actuated subsea systems. Approximately 40% of new developments now integrate electrified subsea trees to reduce hydraulic fluid dependency. Digital twin modeling adoption exceeds 50% among operators, improving predictive maintenance efficiency by 25%. Equinor has deployed integrated light well intervention vessels across more than 30 offshore assets, improving intervention turnaround by 26%. Regional operator behavior reflects strong compliance-driven procurement, with preference for low-emission and digitally enabled intervention technologies.

Asia-Pacific represents approximately 21% of global market share and ranks as the fastest-growing region in the Subsea Well Intervention Technology Market. China, Australia, and India collectively account for over 65% of regional offshore gas development activity. Offshore gas output in the region has expanded by nearly 12% over the past five years, increasing demand for intervention-ready subsea infrastructure. More than 45% of new offshore projects in Asia-Pacific are designed with integrated monitoring systems at installation stage, enabling predictive maintenance. China leads regional subsea equipment manufacturing, contributing significantly to localized production capacity. CNOOC has expanded deepwater intervention programs in the South China Sea, deploying advanced remotely operated vehicles rated beyond 3,000 meters. Regional adoption trends highlight cost-sensitive procurement strategies, with nearly 50% of operators prioritizing modular light well intervention vessels for multi-well servicing efficiency.

South America contributes roughly 6% of global market share, with Brazil accounting for over 80% of regional subsea activity. Brazil’s pre-salt basins host more than 120 deepwater fields, many exceeding 2,000 meters water depth, creating sustained intervention demand for high-pressure systems. Argentina’s offshore gas exploration initiatives are gradually increasing regional diversification. Government-backed offshore licensing rounds have expanded subsea development commitments, while local content requirements encourage domestic equipment partnerships. Intervention demand is heavily linked to production enhancement programs, as pre-salt wells often require periodic stimulation and sand control measures. Petrobras has implemented digital subsea monitoring platforms across multiple pre-salt fields, improving production stability by nearly 15%. Regional operator behavior reflects strong reliance on heavy intervention systems due to complex geological conditions.

The Middle East & Africa region holds approximately 10% of the global Subsea Well Intervention Technology Market, driven by offshore developments in the UAE, Angola, and Nigeria. Offshore oil production in this region exceeds 6 million barrels per day, supporting periodic intervention requirements for integrity and stimulation operations. Technological modernization initiatives are accelerating, with nearly 35% of new offshore projects integrating digital well monitoring platforms. Trade partnerships and offshore investment frameworks are expanding subsea engineering collaborations. ADNOC has advanced offshore field optimization programs incorporating predictive analytics and remote intervention tools, improving well uptime by 18%. Regional adoption behavior reflects increasing emphasis on operational reliability and infrastructure modernization to extend offshore asset life cycles.

Norway – 18% Market Share: It leads due to extensive North Sea subsea infrastructure exceeding 500 active wells and advanced electrified intervention deployment.

United States – 16% Market Share: It maintains strong positioning in the Subsea Well Intervention Technology Market driven by large-scale deepwater Gulf of Mexico production and high adoption of digitally integrated intervention vessels.

The Subsea Well Intervention Technology Market is moderately consolidated, characterized by a mix of integrated oilfield service majors and specialized subsea engineering firms. Approximately 35–40 active global competitors operate across light well intervention (LWI), heavy well intervention (HWI), through-tubing services, and digital subsea diagnostics. The top five companies collectively account for nearly 58% of total market share, reflecting strong technical barriers to entry, vessel ownership requirements, and proprietary tooling systems.

Competition is driven by fleet capability, water-depth ratings exceeding 3,000 meters, and integration of AI-enabled predictive maintenance platforms. Over 48% of intervention campaigns globally are now executed via vessel-based LWI systems, intensifying competition among operators with hybrid-powered and dynamically positioned fleets. Strategic initiatives include multi-year offshore framework agreements, cross-border technology partnerships, and subsea digital twin deployments. In the past three years, more than 20 offshore service alliances have been formalized to enhance regional footprint and cost efficiency.

Innovation trends focus on electrified subsea trees, real-time fiber-optic diagnostics, and remotely operated intervention tooling that reduces offshore crew requirements by up to 18%. Companies are also retrofitting vessels with lower-emission propulsion systems to meet 2030 carbon intensity reduction targets of 25–30% across European waters. Competitive differentiation increasingly depends on integrated service portfolios combining inspection, repair, stimulation, and data analytics in a single intervention campaign.

TechnipFMC

Oceaneering International

Aker Solutions

Subsea 7

Saipem

Helix Energy Solutions Group

Weatherford International

Expro Group

Technip Energies

DeepOcean

COSL (China Oilfield Services Limited)

Welltec

Technological advancement is central to performance optimization in the Subsea Well Intervention Technology Market. Light well intervention vessels equipped with dynamic positioning systems now support operations in water depths exceeding 3,000 meters, reducing rig dependency by nearly 25%. Electrically actuated subsea trees are replacing hydraulic systems in nearly 40% of new North Sea developments, lowering fluid leakage risk and reducing carbon intensity by approximately 30% per installation.

Digital twin technology has been adopted by over 50% of major offshore operators, enabling simulation-based intervention planning that reduces non-productive time by up to 22%. Fiber-optic sensing integrated into subsea infrastructure enhances pressure and temperature monitoring accuracy by 20–25%, strengthening well integrity management. Autonomous underwater vehicles (AUVs) capable of 24-hour continuous inspection cycles have improved subsea inspection efficiency by 15% while minimizing human exposure to high-risk offshore environments.

AI-driven predictive maintenance tools analyze operational datasets exceeding 1 terabyte per field annually, identifying early-stage anomalies and lowering unexpected shutdowns by nearly 18%. Remote operations centers allow onshore control of intervention tooling, reducing offshore personnel deployment by approximately 12–18%. Hybrid-powered intervention vessels equipped with battery-assisted propulsion systems decrease fuel consumption by up to 20%, aligning with regulatory emission reduction targets.

Emerging trends include subsea robotics integration, modular intervention riser systems, and high-pressure/high-temperature (HPHT) rated tooling capable of operating above 15,000 psi, enabling safe access to complex reservoirs. These technologies collectively enhance production resilience, regulatory compliance, and lifecycle cost optimization.

• In August 2025, SLB acquired Stimline Digital AS, a cloud-based software provider specializing in well intervention planning and execution. The acquisition integrates Stimline’s IDEX™ platform with SLB’s digital ecosystem to enhance data-driven workflows and improve consistency, efficiency, and performance across well intervention projects globally. Source: www.slb.com

• In September 2025, SLB secured a major completions and advanced technology contract from Petrobras for up to 35 ultra-deepwater wells in the Santos Basin. The agreement includes deployment of advanced electric completions technologies such as Electris™ high-flow-rate interval control valves, enhancing production intelligence and reservoir management in complex subsea environments. Source: www.slb.com

• In October 2025, Oceaneering International announced the award of a riserless light well intervention (RLWI) services contract by bp Exploration Caspian Sea Ltd. for multi-well mechanical wireline intervention campaigns in the Azeri-Chirag-Deepwater Gunashli (ACG) oilfield, with engineering and pre-mobilization underway ahead of Q4 2025 operations. Source: www.investors.oceaneering.com

• In December 2025, SLB entered a strategic collaboration agreement with Shell to accelerate the development of digital and agentic AI solutions for upstream operations. The initiative aims to unify data and workflows across subsurface, well construction, and production using SLB’s Lumi™ AI platform. Source: www.slb.com

The Subsea Well Intervention Technology Market Report provides a structured assessment of offshore intervention systems across multiple dimensions, including technology type, operational depth, application category, and end-user deployment. The scope encompasses light well intervention vessels, heavy well intervention rigs, through-tubing tools, coiled tubing systems, digital monitoring platforms, and electrically actuated subsea components rated for pressures exceeding 15,000 psi.

Geographically, the report evaluates performance across five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—covering more than 3,000 active offshore wells globally that require periodic intervention. It analyzes mature field redevelopment trends, deepwater and ultra-deepwater (>1,500 meters) expansion projects, and offshore gas tie-back developments.

Application analysis includes well stimulation, inspection and integrity verification, sand control, scale removal, logging, and recompletion activities. The report further examines digital transformation metrics such as predictive maintenance adoption rates exceeding 50% among major operators, and electrified subsea tree integration in nearly 40% of new European offshore projects.

Industry focus areas extend to regulatory compliance frameworks, emission reduction commitments targeting 30% operational carbon cuts by 2030, hybrid-powered vessel retrofits, and AI-enabled subsea data analytics platforms. The study also addresses niche segments such as high-pressure/high-temperature intervention tooling and autonomous underwater inspection systems. Overall, the report offers a comprehensive strategic framework supporting investment decisions, procurement planning, technology benchmarking, and long-term offshore asset optimization.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 574.0 Million |

| Market Revenue (2033) | USD 785.0 Million |

| CAGR (2026–2033) | 3.99% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Schlumberger; Halliburton; Baker Hughes; TechnipFMC; Oceaneering International; Aker Solutions; Subsea 7; Saipem; Helix Energy Solutions Group; Weatherford International; Expro Group; Technip Energies; DeepOcean; COSL; Welltec |

| Customization & Pricing | Available on Request (10% Customization Free) |