Reports

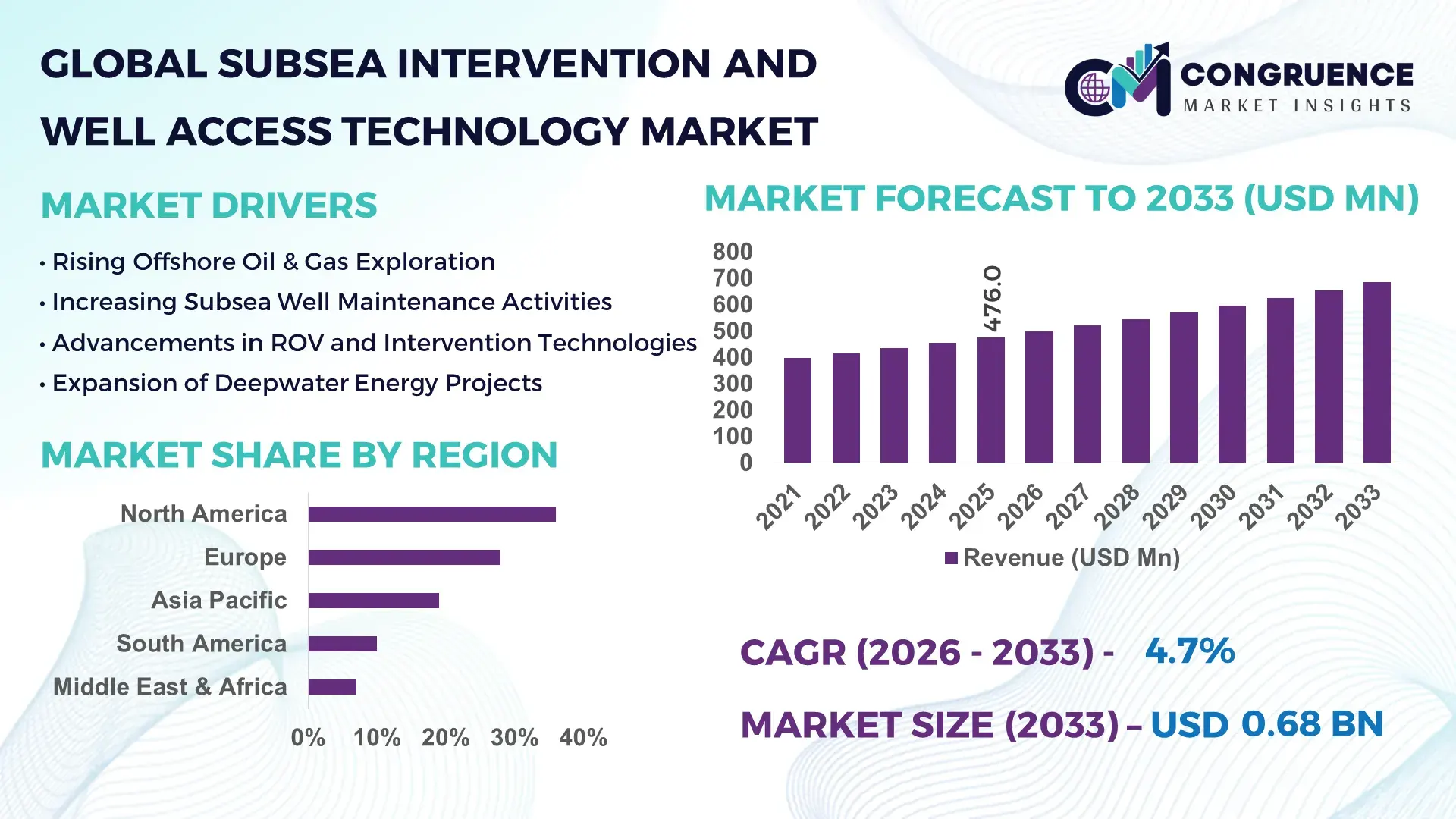

The Global Subsea Intervention and Well Access Technology Market was valued at USD 476.0 Million in 2025 and is anticipated to reach a value of USD 684.7 Million by 2033 expanding at a CAGR of 4.65% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market growth is primarily supported by increasing offshore oilfield maintenance activities and the rising deployment of advanced remote-operated subsea intervention systems to extend the operational life of deepwater wells.

The United States remains a major hub for subsea intervention and well access technologies due to extensive offshore production activities in the Gulf of Mexico. The country operates more than 2,000 active offshore platforms and produces nearly 15% of its crude oil from offshore fields. Over USD 8 billion has been invested in subsea infrastructure modernization since 2022, including robotic intervention systems and high-pressure subsea access equipment. Approximately 60% of new deepwater well projects in the Gulf region utilize advanced light well intervention vessels and remotely operated vehicles (ROVs), supporting efficient subsea inspection, maintenance, and well stimulation operations across large offshore assets.

Market Size & Growth:The market was valued at USD 476.0 Million in 2025 and is projected to reach USD 684.7 Million by 2033, expanding at a CAGR of 4.65%, driven by increased offshore field maintenance and deepwater well optimization programs.

Top Growth Drivers:Offshore exploration expansion (42%), improved intervention efficiency through robotics (35%), and aging subsea well maintenance requirements (28%).

Short-Term Forecast:By 2028, automated intervention systems are expected to reduce offshore maintenance costs by nearly 18% while improving operational uptime by approximately 22%.

Emerging Technologies:Robotic light well intervention systems, AI-enabled subsea monitoring platforms, and advanced remotely operated vehicles capable of performing multi-function subsea repair and inspection tasks.

Regional Leaders:North America is projected to reach approximately USD 260 Million by 2033 driven by Gulf of Mexico projects; Europe is expected to exceed USD 190 Million with strong North Sea intervention programs; Asia Pacific may approach USD 150 Million due to offshore developments in Southeast Asia.

Consumer/End-User Trends:Offshore oil and gas operators increasingly deploy digital subsea monitoring systems, with nearly 48% of new offshore wells integrating remote intervention capabilities to reduce manual intervention risks.

Pilot or Case Example:In 2024, a North Sea subsea intervention pilot reduced well intervention downtime by nearly 27% using robotic intervention systems integrated with real-time seabed sensors.

Competitive Landscape:Schlumberger holds roughly 18% share, followed by Halliburton, TechnipFMC, Baker Hughes, and Oceaneering International.

Regulatory & ESG Impact:Offshore regulatory bodies increasingly mandate subsea monitoring and leak detection technologies, leading to nearly 30% higher adoption of environmentally compliant intervention systems.

Investment & Funding Patterns:Over USD 3.5 billion has been invested globally in subsea infrastructure modernization and well intervention equipment between 2022 and 2025.

Innovation & Future Outlook:Integration of AI-driven seabed monitoring, digital twin offshore wells, and autonomous intervention vessels is expected to transform offshore asset maintenance strategies.

Subsea intervention and well access technologies support multiple offshore energy sectors including deepwater oil production (approximately 58%), offshore gas fields (around 27%), and subsea infrastructure inspection activities (about 15%). New robotic intervention tools and automated pressure control equipment are improving subsea repair accuracy and operational safety. Environmental regulations targeting offshore leakage monitoring and growing offshore production investments in the North Sea and Gulf of Mexico are shaping demand patterns, while digital monitoring platforms and autonomous subsea vehicles represent emerging technological trends.

The Subsea Intervention and Well Access Technology Market plays a critical role in maintaining the productivity and longevity of offshore oil and gas wells, particularly in deepwater and ultra-deepwater environments where direct human intervention is limited. Offshore energy infrastructure currently includes more than 12,000 subsea wells globally, with a significant portion requiring periodic maintenance, stimulation, or repair operations. As a result, intervention technologies that enable safe and efficient well access have become strategic assets for offshore operators seeking to optimize production while minimizing operational risks.

Modern robotic light well intervention systems represent a major technological advancement in this sector. Compared to traditional rig-based intervention operations, robotic subsea intervention platforms deliver nearly 35% improvement in operational efficiencyand can reduce intervention costs by approximately 25%. In addition, autonomous remotely operated vehicles equipped with high-precision sensors allow operators to conduct inspection and repair tasks at depths exceeding 3,000 meters, expanding the operational capability of subsea oilfields.

From a regional perspective, North America dominates in volume of subsea intervention operations due to the Gulf of Mexico’s extensive offshore infrastructure, while Europe leads in advanced adoption with nearly 62% of offshore operators in the North Sea integrating digital monitoring platforms into subsea intervention workflows. These digital systems enable predictive maintenance, which significantly reduces unplanned downtime in subsea production systems.

Technological innovation is expected to reshape operational strategies over the next few years. By 2028, AI-enabled subsea monitoring systems are projected to improve intervention response times by nearly 20%, enabling faster identification of subsea anomalies and optimizing maintenance schedules. Companies are also focusing on sustainability goals, with many offshore operators committing to 30% reduction in offshore methane leakage by 2030through enhanced subsea monitoring and automated intervention technologies.

A notable example occurred in 2024 when Norway deployed AI-enabled subsea inspection systems across several offshore fields, achieving approximately 24% reduction in maintenance downtimethrough predictive intervention planning. Such initiatives demonstrate how advanced digital technologies can improve offshore asset performance while maintaining environmental compliance.

Looking forward, the Subsea Intervention and Well Access Technology Market is expected to remain a pillar of offshore energy infrastructure, supporting operational resilience, regulatory compliance, and sustainable development across global deepwater energy projects.

The Subsea Intervention and Well Access Technology Market is shaped by evolving offshore exploration strategies, aging subsea infrastructure, and the increasing complexity of deepwater production environments. Offshore oil and gas fields require continuous monitoring and maintenance to ensure uninterrupted production, making subsea intervention systems essential for tasks such as well stimulation, equipment replacement, flowline repair, and subsea inspection. Globally, more than 40% of offshore wells are now located in deepwater environments exceeding 1,500 meters, creating demand for specialized intervention equipment capable of operating under extreme pressure and temperature conditions.

Technological innovation is also transforming the operational landscape of subsea maintenance. Remotely operated vehicles, autonomous underwater vehicles, and advanced pressure control equipment are enabling safer and more efficient well access operations. Operators are increasingly integrating digital monitoring systems with subsea intervention equipment to improve predictive maintenance capabilities and reduce operational downtime. Additionally, regulatory pressure related to offshore safety and environmental monitoring is pushing companies to adopt advanced subsea inspection technologies. As offshore energy production expands in regions such as the Gulf of Mexico, the North Sea, and Southeast Asia, the demand for efficient subsea intervention and well access solutions continues to strengthen.

Deepwater and ultra-deepwater exploration projects are significantly increasing the need for advanced subsea intervention and well access technologies. Offshore fields located at depths exceeding 1,500 meters require specialized equipment to perform maintenance, stimulation, and repair operations safely. Globally, deepwater oil production accounts for nearly 35% of offshore output, and several new projects are being developed in the Gulf of Mexico, Brazil’s pre-salt fields, and the North Sea. These projects rely heavily on robotic intervention systems and remotely operated vehicles to conduct subsea operations without deploying large drilling rigs. Light well intervention vessels are becoming increasingly popular because they reduce operational costs and provide rapid access to subsea wells. Nearly 50% of offshore operators have incorporated robotic intervention systems into their maintenance strategies, allowing for more efficient well stimulation and equipment repair tasks. Additionally, the expansion of subsea tie-back infrastructure and underwater pipelines is increasing the demand for specialized well access systems that can operate under high pressure conditions. These developments continue to strengthen the adoption of subsea intervention technologies across major offshore energy hubs.

Subsea intervention and well access operations require highly specialized equipment, skilled personnel, and sophisticated offshore vessels capable of operating in extreme marine environments. Establishing subsea intervention infrastructure involves complex logistics including remotely operated vehicles, pressure control equipment, and high-capacity intervention vessels. The cost of deploying a single light well intervention vessel can exceed several hundred thousand dollars per day, which significantly increases operational expenditure for offshore operators. In addition, subsea intervention operations are heavily influenced by weather conditions and ocean dynamics. Rough seas, deepwater pressure environments, and limited accessibility make intervention operations technically challenging and time-consuming. Offshore projects also require strict compliance with safety regulations, environmental monitoring protocols, and risk mitigation standards. These requirements often result in extended planning timelines and complex engineering procedures. Smaller offshore operators may find it difficult to invest in advanced intervention technologies due to these financial and operational barriers, limiting broader adoption in certain offshore regions.

Digital transformation in offshore operations is opening significant opportunities for the subsea intervention and well access technology sector. Advanced data analytics platforms, AI-enabled monitoring systems, and autonomous underwater vehicles are improving the efficiency of offshore inspection and maintenance activities. Digital monitoring technologies allow operators to track subsea equipment performance in real time, enabling predictive maintenance strategies that reduce unplanned intervention requirements. Robotic intervention systems are particularly promising in deepwater environments where human access is limited. Autonomous underwater vehicles equipped with high-precision sensors can inspect pipelines, valves, and subsea infrastructure while transmitting real-time data to offshore control centers. More than 40% of offshore operators are currently testing digital twin platforms for subsea wells, enabling engineers to simulate intervention procedures before deployment. These innovations reduce operational risk and improve maintenance accuracy. As offshore digitalization accelerates, the demand for integrated subsea intervention platforms that combine robotics, monitoring systems, and predictive analytics is expected to expand significantly.

Strict environmental and safety regulations present a significant challenge for companies operating in the subsea intervention and well access technology market. Offshore operations must comply with complex regulatory frameworks that address oil spill prevention, underwater ecosystem protection, and operational safety standards. Intervention systems must undergo rigorous certification processes before deployment, which can delay project timelines and increase engineering costs. Environmental monitoring requirements have also intensified in several offshore regions following past incidents related to subsea leaks and pipeline failures. Operators are required to install advanced monitoring systems capable of detecting even minor leaks in subsea infrastructure. While these regulations improve safety and environmental protection, they also require significant investment in new technologies and operational procedures. Furthermore, regulatory differences between offshore jurisdictions create additional compliance challenges for companies operating across multiple regions. These factors can slow technology deployment and create barriers for smaller companies attempting to enter the subsea intervention technology market.

• Expansion of robotic subsea intervention systems:Robotic intervention technologies are transforming offshore maintenance operations. Approximately 48% of offshore operatorsnow deploy remotely operated vehicles for well access and inspection activities. These systems can operate at depths exceeding 3,000 metersand reduce human intervention requirements by nearly 35%, improving operational safety and reducing offshore maintenance timelines.

• Integration of AI-driven subsea monitoring platforms:Offshore companies are increasingly implementing AI-based monitoring systems capable of analyzing thousands of sensor data points across subsea wells and pipelines. Digital monitoring solutions have improved early fault detection by approximately 28%and reduced emergency intervention requirements by nearly 20%, enabling more efficient predictive maintenance programs.

• Growing adoption of light well intervention vessels:Light well intervention vessels are becoming a preferred alternative to traditional drilling rigs for subsea maintenance. These vessels can complete intervention tasks up to 40% fasterand reduce operational costs by approximately 30%compared with conventional rig-based interventions, making them attractive for offshore operators managing multiple subsea wells.

• Deployment of autonomous underwater vehicles for inspection:Autonomous underwater vehicles are gaining momentum in subsea infrastructure monitoring. Nearly 37% of offshore inspection operationsnow involve autonomous underwater systems capable of mapping subsea pipelines and detecting structural anomalies with 95% inspection accuracy, improving the reliability of offshore asset management.

The Subsea Intervention and Well Access Technology Market is segmented by type, application, and end-user industries, reflecting the diverse operational requirements of offshore oil and gas infrastructure. Different intervention technologies are designed to perform specialized functions including well maintenance, inspection, and stimulation. Light well intervention systems and remotely operated vehicles have gained significant adoption due to their ability to perform complex operations in deepwater environments with minimal human presence. Applications primarily focus on offshore oilfield maintenance, pipeline inspection, and subsea infrastructure repair activities. End-users largely consist of offshore oil and gas operators, subsea service providers, and energy infrastructure management companies. The growing complexity of offshore exploration projects and the increasing number of aging subsea wells have expanded the demand for intervention technologies capable of extending the operational life of offshore assets while ensuring regulatory compliance and environmental safety.

The market includes several key technology types such as Light Well Intervention Systems, Remotely Operated Vehicles (ROVs), Subsea Lubricator Systems, and Through-Tubing Intervention Systems. Light well intervention systems currently represent the leading technology segment, accounting for approximately 38% of overall adoptiondue to their efficiency in conducting well stimulation, inspection, and repair operations without the need for large drilling rigs. These systems are widely used in mature offshore fields where frequent well maintenance is required. Remotely operated vehicles account for nearly 27% of the technology adoption landscapeand play a critical role in subsea inspection and equipment repair tasks. However, through-tubing intervention systems are experiencing the fastest adoption growth with an estimated CAGR of around 6.8%, as offshore operators increasingly seek cost-effective methods for performing well maintenance operations without full well shutdowns. Subsea lubricator systems and specialized pressure control equipment collectively contribute approximately 35% of the technology landscape, supporting safe well access operations in high-pressure offshore environments.

• In 2025, a large offshore operator deployed advanced robotic intervention tools integrated with remotely operated vehicles across multiple deepwater wells, improving inspection efficiency for more than 120 subsea installations.

Key applications in the Subsea Intervention and Well Access Technology Market include well maintenance and stimulation, pipeline and subsea infrastructure inspection, subsea equipment repair, and reservoir monitoring operations. Well maintenance and stimulation represent the dominant application segment with approximately 41% share, as offshore wells require periodic intervention to maintain production efficiency and manage reservoir pressure conditions. Subsea infrastructure inspection accounts for nearly 29% of operational demand, supported by increasing deployment of underwater monitoring systems capable of identifying pipeline corrosion, valve malfunctions, and structural anomalies. However, subsea equipment repair applications are expanding rapidly with an estimated CAGR of around 6.5%, driven by aging offshore infrastructure and the need for cost-efficient repair solutions. Other applications including reservoir monitoring and subsea flow assurance collectively contribute roughly 30% of the market landscape.

In 2025, about 44% of offshore operators globally reported deploying automated subsea inspection systems to monitor pipelines and valves in real time, significantly improving maintenance planning.

• In 2024, a major offshore energy project implemented advanced robotic inspection systems to monitor more than 800 kilometers of subsea pipelines, significantly improving anomaly detection accuracy.

Offshore oil and gas companies represent the primary end-user segment in the Subsea Intervention and Well Access Technology Market, accounting for approximately 62% of total adoptiondue to their extensive subsea infrastructure and ongoing need for well maintenance operations. These companies rely heavily on robotic intervention systems, remote monitoring platforms, and specialized well access technologies to maintain production continuity in deepwater fields. Subsea service providers constitute the fastest-growing end-user segment with an estimated CAGR of around 6.9%, as oil and gas operators increasingly outsource specialized intervention tasks to companies with dedicated offshore vessels and robotic systems. These service providers deliver inspection, repair, and maintenance operations across multiple offshore assets. Other end-users including offshore engineering companies and energy infrastructure management firms contribute approximately 38% of combined adoption, supporting subsea pipeline monitoring and infrastructure maintenance projects.

In 2025, more than 46% of offshore operators globally reported outsourcing subsea inspection and intervention services to specialized service providers, reflecting the growing complexity of offshore maintenance operations.

• In 2025, a consortium of offshore energy operators implemented robotic intervention programs across several North Sea platforms, improving subsea maintenance efficiency across more than 90 offshore wells.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America’s leadership is largely supported by extensive offshore oil production infrastructure, particularly in the Gulf of Mexico where more than 2,000 offshore platforms and over 1,600 subsea wellsrequire periodic intervention operations. Europe follows with approximately 28% market share, driven by large-scale subsea operations across the North Sea and Norwegian Continental Shelf, where more than 9,000 km of subsea pipelinesrequire regular inspection and maintenance. Asia-Pacific accounts for nearly 19% of the global market, supported by growing offshore developments in China, India, Malaysia, and Australia, where over 350 offshore fieldsare actively producing hydrocarbons. South America contributes roughly 10% share, largely driven by Brazil’s deepwater pre-salt oilfields that include over 150 subsea wellsrequiring advanced intervention systems. Meanwhile, the Middle East & Africa region represents around 7%, supported by offshore exploration projects in Saudi Arabia, UAE, Nigeria, and Angola, where subsea infrastructure modernization and digital monitoring systems are gaining traction to enhance offshore production reliability and environmental monitoring.

North America represents approximately 36% of global demandfor subsea intervention and well access technology, driven primarily by the offshore oil and gas industry. The United States and Mexicoplay critical roles due to extensive production activity in the Gulf of Mexico, which contains more than 3,200 offshore oil and gas wellsand over 30,000 km of subsea pipelinesrequiring regular inspection and intervention operations. Offshore operators in this region increasingly adopt robotic intervention systems and remotely operated vehicles capable of performing maintenance at depths exceeding 2,500 meters. Regulatory frameworks enforced by offshore safety authorities require strict monitoring of subsea infrastructure to prevent leaks and environmental incidents, which further increases the deployment of advanced monitoring systems. Technological innovation also drives the regional market landscape. Companies are integrating AI-driven seabed monitoring and predictive maintenance tools that can analyze thousands of sensor data points across subsea assets. For example, Oceaneering Internationalhas expanded its fleet of remotely operated vehicles and robotic intervention platforms capable of performing subsea repairs and inspections across multiple offshore fields. Regional consumer behavior also reflects strong technology adoption patterns, where offshore operators in North America prioritize automation, digital monitoring, and roboticsto reduce human risk exposure and improve operational efficiency in deepwater environments.

Europe accounts for approximately 28% of the global subsea intervention and well access technology market, supported by extensive offshore oil production activities across the United Kingdom, Norway, and Denmarkin the North Sea region. The North Sea hosts more than 500 offshore production installationsand thousands of subsea wells that require continuous inspection and maintenance to maintain operational efficiency. European offshore operators have increasingly invested in advanced subsea intervention equipment such as robotic inspection tools and automated pressure control systems. The regulatory landscape in this region is shaped by strict environmental compliance policies and sustainability initiatives introduced by regional energy regulators. Offshore operators are required to deploy advanced leak detection technologies and digital monitoring platforms capable of detecting anomalies in subsea pipelines and valves. The region also leads in the adoption of digital twin technology to simulate offshore well conditions and predict maintenance requirements. Companies such as TechnipFMCare actively developing integrated subsea intervention systems designed to improve well access efficiency in deepwater environments. Consumer behavior in the region reflects strong regulatory influence, where offshore operators prioritize environmentally compliant intervention technologiescapable of minimizing environmental risk while maintaining operational productivity.

Asia-Pacific ranks among the fastest expanding regions for subsea intervention and well access technologies and represents approximately 19% of the global market volume. Countries such as China, India, Malaysia, and Australiaare actively expanding offshore exploration and production infrastructure, which requires advanced intervention systems to maintain subsea wells and pipelines. China alone operates more than 200 offshore oil and gas fields, while India has over 100 offshore installationsacross the Arabian Sea and Bay of Bengal. Infrastructure development remains a key growth driver in this region. Several countries are investing heavily in subsea pipeline networks and offshore production systems capable of supporting long-distance hydrocarbon transportation. Technological innovation is also expanding rapidly, with offshore operators integrating robotic intervention systems and autonomous underwater vehicles capable of conducting pipeline inspections and equipment maintenance in deepwater conditions. Regional technology hubs such as Singapore and South Koreaplay an important role in manufacturing advanced subsea equipment and robotics. Consumer behavior across Asia-Pacific indicates strong adoption of digital monitoring platforms and automation technologiesdesigned to reduce offshore operational risks and enhance subsea asset performance.

South America contributes approximately 10% of global demandfor subsea intervention and well access technology, largely driven by offshore oil production in Brazil and Argentina. Brazil remains the dominant regional player due to its extensive deepwater pre-salt reserves located in the Atlantic Ocean. The country operates more than 150 subsea wellsacross its offshore fields, many located at depths exceeding 2,000 meters, which require specialized intervention equipment for inspection and maintenance operations. Government policies promoting offshore exploration and foreign investment in energy infrastructure have accelerated subsea technology adoption in the region. National energy authorities have introduced regulatory frameworks encouraging modernization of offshore infrastructure and the deployment of advanced subsea monitoring technologies. Companies such as Petrobrasare heavily investing in robotic intervention systems and autonomous underwater vehicles to support inspection of subsea pipelines and wellheads. Consumer demand in the region remains strongly tied to offshore oil production activities, where operators prioritize technologies capable of improving operational efficiency in challenging deepwater environments.

The Middle East & Africa region represents approximately 7% of the global subsea intervention and well access technology market, supported by offshore oil production projects in countries such as Saudi Arabia, UAE, Nigeria, and Angola. Offshore exploration activities are expanding across the Persian Gulf and West African coastlines, where several deepwater fields require advanced intervention technologies to maintain production infrastructure. Energy companies in the region are increasingly investing in subsea digital monitoring platforms and robotic intervention systems capable of detecting equipment faults and performing remote repairs. Offshore projects in Nigeria and Angola alone include more than 120 subsea wells, requiring regular inspection and maintenance to ensure safe operations. Technological modernization is supported by international partnerships between regional energy companies and global subsea technology providers. Consumer adoption patterns show strong demand for high-performance inspection systems and remotely operated vehicles, particularly in offshore oil and gas operations where reliability and safety remain critical priorities.

United States – 31% market share: It leads globally due to extensive offshore infrastructure in the Gulf of Mexico and high deployment of robotic intervention systems for deepwater wells.

Norway – 14% market share: It remains highly advanced due to strong North Sea offshore production activities and widespread adoption of digital subsea monitoring technologies.

The Subsea Intervention and Well Access Technology Market is characterized by a moderately consolidated competitive environment where a combination of global oilfield service companies and specialized subsea engineering firms compete to deliver advanced intervention systems and well access solutions. The market currently includes more than 70 active technology providers and offshore service companiesoperating across various segments including robotic intervention systems, remotely operated vehicles, pressure control equipment, and light well intervention vessels.

The top five companies collectively control approximately 48% of the global market, reflecting strong industry consolidation among established offshore service providers with large operational fleets and integrated subsea technology capabilities. Major companies compete by expanding robotic intervention fleets, investing in digital monitoring platforms, and launching advanced pressure control systems capable of operating in ultra-deepwater conditions exceeding 3,000 meters depth.

Strategic partnerships and joint ventures are common across the market, particularly between offshore operators and subsea technology firms seeking to develop integrated well access platforms. Companies are also focusing heavily on innovation, including the deployment of autonomous underwater vehicles, AI-driven seabed monitoring systems, and digital twin technology that can simulate offshore well operations. Mergers and acquisitions have also accelerated in recent years as larger service providers seek to strengthen their technological capabilities and expand global service networks across offshore energy hubs.

Halliburton

Baker Hughes

TechnipFMC

Oceaneering International

Subsea 7

Saipem

Helix Energy Solutions Group

Aker Solutions

NOV Inc.

Fugro

Expro Group

DOF Subsea

Vallourec

Technological advancement is rapidly transforming the subsea intervention and well access technology landscape, enabling offshore operators to perform complex maintenance operations with greater efficiency and safety. Modern subsea intervention systems now rely heavily on robotic technologies, digital monitoring platforms, and autonomous underwater vehiclescapable of performing inspection, repair, and well stimulation tasks at extreme depths. Offshore oil and gas wells often operate at depths exceeding 2,000–3,000 meters, requiring highly specialized equipment designed to withstand intense pressure and temperature conditions.

Remotely operated vehicles represent one of the most widely adopted technologies in subsea intervention operations. Globally, more than 70% of offshore inspection and maintenance tasksinvolve remotely operated vehicles equipped with advanced cameras, robotic arms, and high-precision sensors capable of detecting structural anomalies in subsea infrastructure. These systems significantly reduce the need for human divers and improve operational safety.

Another major technological innovation is the integration of digital twin platformsfor subsea wells. Digital twins allow engineers to create virtual replicas of subsea assets and simulate various intervention scenarios before deploying equipment offshore. This technology improves maintenance planning and reduces operational downtime. Offshore operators utilizing digital twin systems have reported improvements in predictive maintenance accuracy by approximately 30%.

Automation and artificial intelligence are also increasingly integrated into subsea monitoring systems. AI-driven platforms can process thousands of real-time sensor readings from subsea valves, pipelines, and wellheads, enabling early detection of leaks or equipment failures. Additionally, the development of autonomous intervention vesselscapable of performing subsea operations without direct human control is gaining traction in offshore energy projects.

Advanced pressure control equipment and modular subsea intervention systems are also improving well access efficiency. These technologies allow operators to conduct well maintenance without shutting down entire production systems, enabling faster intervention cycles and improved productivity. As offshore exploration expands into deeper and more technically challenging environments, the continued evolution of robotic and digital technologies will play a crucial role in enhancing the reliability and performance of subsea intervention operations.

• In July 2024, SLB OneSubsea (SLB)announced that its OneSubsea joint venture was awarded an integrated engineering, procurement, construction, and installation contract by bp for the Murlach subsea development in the UK North Sea, including delivery of two vertical monobore subsea trees, a two-slot manifold, and 8 km of rigid flowlines, aimed at improving installation efficiency and reducing offshore rig days. Source: www.slb.com

• In August 2024, SLB OneSubsea secured a major contract from Petrobrasto deliver standardized pre-salt subsea production systems for the Atapu and Sépia fields in Brazil’s Santos Basin, including subsea control systems, vertical trees, and distribution units designed for ultra-deepwater operations.

• In December 2024, Oceaneering Internationalannounced that its Freedom™ Autonomous Underwater Vehicle (AUV)received the Innovation Award at TotalEnergies’ Supplier Day, recognizing its subsea robotics technology that improves offshore inspection efficiency while reducing operational emissions during subsea monitoring missions.

• In September 2025, Oceaneering Asset Integrity ASsigned a framework agreement with Equinorfor fabric maintenance and subsea asset integrity services supporting offshore infrastructure in Norway. The agreement runs from 2025 to 2027 with extension options, strengthening subsea maintenance capabilities across North Sea assets.

The Subsea Intervention and Well Access Technology Market Report provides a comprehensive analysis of the global market landscape, covering technology developments, industry applications, and regional market trends across major offshore energy hubs. The report examines multiple technology segments including robotic intervention systems, remotely operated vehicles, subsea lubricator systems, pressure control equipment, and through-tubing intervention technologies used in offshore well maintenance operations.

The scope of the report includes a detailed assessment of market segmentation by technology type, application, end-user industry, and geographic region, offering insights into operational trends across offshore oil and gas production environments. The study evaluates the performance of intervention systems used for well inspection, maintenance, repair, and reservoir stimulation activities across thousands of subsea wells globally. Offshore oil production currently accounts for nearly 30% of global crude output, making subsea infrastructure maintenance a critical aspect of energy supply stability.

Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting offshore production activities, subsea infrastructure development, and technological adoption patterns within each region. The report also evaluates the role of emerging digital technologies such as AI-enabled monitoring platforms, digital twin systems, and autonomous underwater vehicles that are increasingly being deployed to enhance offshore maintenance efficiency.

In addition, the report analyzes industry trends related to offshore infrastructure modernization, environmental monitoring technologies, and regulatory compliance requirements affecting subsea operations. The study further explores the competitive landscape, identifying key market participants and strategic initiatives shaping technological innovation and service capabilities. By examining operational data across offshore energy projects and subsea infrastructure networks, the report provides decision-makers with actionable insights to support investment planning, technology adoption, and long-term offshore asset management strategies.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 476.0 Million |

| Market Revenue (2033) | USD 684.7 Million |

| CAGR (2026–2033) | 4.65% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Schlumberger; Halliburton; Baker Hughes; TechnipFMC; Oceaneering International; Subsea 7; Saipem; Helix Energy Solutions Group; Aker Solutions; NOV Inc.; Fugro; Expro Group; DOF Subsea; Vallourec |

| Customization & Pricing | Available on Request (10% Customization Free) |