Reports

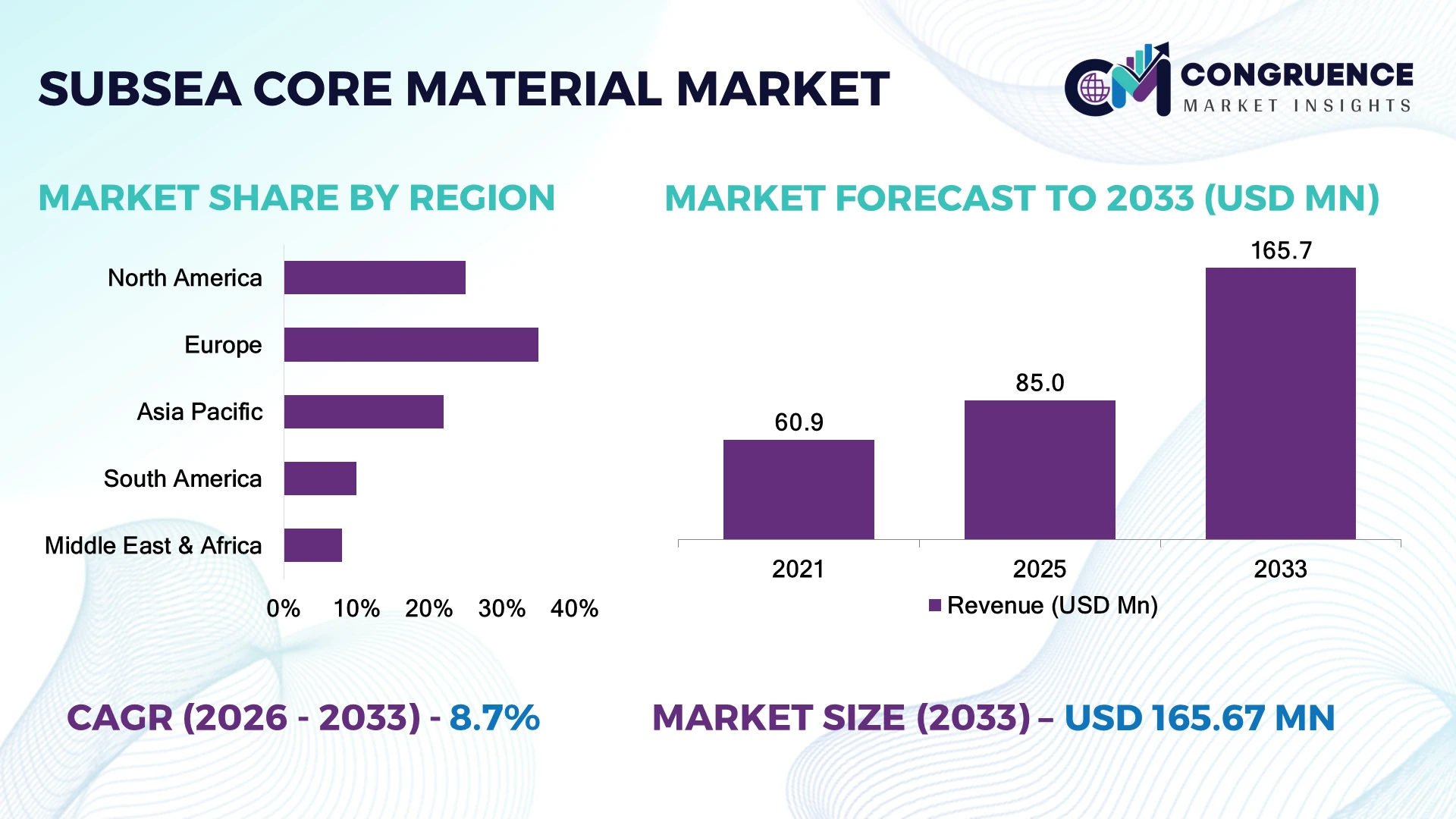

The Global Subsea Core Material Market was valued at USD 85.0 Million in 2025 and is anticipated to reach a value of USD 165.7 Million by 2033 expanding at a CAGR of 8.7% between 2026 and 2033. Growth is driven by increasing use of lightweight composite core materials in subsea pipelines, offshore wind foundations, buoyancy modules, and deepwater energy infrastructure requiring corrosion resistance and extended service life.

Norway leads subsea core material adoption with approximately 28% market share, supported by offshore oil & gas expertise and investments exceeding USD 20 billion in offshore energy projects. The United States follows with around 22% share, driven by Gulf of Mexico subsea developments and offshore wind expansion. Norway’s advanced composite deployment exceeds traditional steel-based solutions by improving structural efficiency by nearly 30%, strengthening regional competitiveness.

Strategic implication Companies prioritizing advanced composite manufacturing and localized supply chains are positioned to capture high-value subsea infrastructure opportunities.

Market Size & Growth: USD 85.0 Million in 2025 to USD 165.7 Million by 2033 at 8.7% CAGR, driven by offshore wind and deepwater infrastructure upgrades.

Top Growth Drivers: Offshore wind expansion 35%, subsea pipeline modernization 30%, lightweight composite adoption 25%.

Short-Term Forecast: By 2028, composite core material adoption increases by 20% as operators target weight reduction and durability improvements.

Emerging Technologies: Advanced PET/PVC foam cores, AI-assisted material design, and automated composite manufacturing accelerate innovation.

Regional Leaders: Europe reaches USD 70 Million with offshore wind growth; North America reaches USD 45 Million with Gulf projects; Asia-Pacific reaches USD 35 Million through marine infrastructure expansion.

Consumer/End-User Trends: Over 60% of subsea operators prioritize corrosion-resistant composite solutions for long-life assets.

Pilot/Case Example: 2024 offshore composite buoyancy projects achieved approximately 25% weight reduction compared with conventional materials.

Competitive Landscape: Leading suppliers include Diab Group, Gurit, 3A Composites, Evonik, and Armacell, with major players controlling around 45% of specialized core material supply.

Regulatory & ESG Impact: Offshore sustainability policies are driving 30% higher adoption of recyclable and lower-carbon composite materials.

Investment & Funding: Over USD 5 billion is being directed into offshore wind and subsea infrastructure partnerships, supporting material innovation.

Innovation & Future Outlook: Next-generation recyclable cores, digital monitoring, and hybrid composite structures are reshaping subsea asset strategies.

Subsea core materials are becoming essential for offshore energy, marine engineering, and deepwater applications as operators seek stronger, lighter, and longer-lasting structures. Recent innovations in recyclable foam cores and hybrid composite systems are improving performance by nearly 20%, while supply-chain diversification following global offshore infrastructure expansion is encouraging regional manufacturing investments. The market is increasingly shifting toward sustainable composite solutions with improved lifecycle efficiency.

The Subsea Core Material Market is becoming strategically important as offshore energy operators and marine infrastructure developers focus on reducing structural weight, improving asset durability, and lowering maintenance complexity. The transition toward offshore wind, deeper subsea exploration, and infrastructure modernization is reshaping material selection strategies across global projects.

Supply-chain restructuring and regional manufacturing expansion are influencing procurement decisions as companies reduce dependence on limited composite material suppliers. Advanced foam core materials now provide up to 30% weight savings compared with traditional metal-intensive structures while improving corrosion resistance and operational lifespan. Digital material simulation and automated fabrication are also reducing development cycles by nearly 25%.

Europe maintains leadership through offshore wind deployment, while North America emphasizes deepwater oil and gas modernization and Asia-Pacific accelerates marine infrastructure investment. For example, offshore wind developers are increasingly adopting composite buoyancy and support components to improve installation efficiency and reduce maintenance requirements.

Companies are expanding partnerships with composite manufacturers, investing in recyclable material technologies, and strengthening regional production capabilities. The strategic advantage will belong to organizations combining advanced materials, resilient supply chains, and sustainable engineering practices to secure long-term competitiveness in subsea infrastructure markets.

The expansion of offshore wind, subsea pipelines, and deepwater energy projects is accelerating adoption of lightweight core materials, with composite structures reducing component weight by 25–35% compared with conventional metal-based systems. Norway and the United States are increasing investments in offshore infrastructure modernization, driving demand for PET foam, PVC foam, and syntactic core solutions. Global offshore wind installations are pushing operators toward corrosion-resistant materials that extend asset life by over 20%. Companies are responding through advanced material development, manufacturing capacity expansion, and partnerships with offshore engineering firms to improve structural performance and reduce lifecycle maintenance costs.

High production costs, limited supplier concentration, and complex certification requirements restrict wider deployment of subsea core materials. Advanced composite cores can account for 15–25% of structural component costs, creating pricing pressure for offshore contractors. Germany and Japan remain dependent on specialized material suppliers for high-performance marine composites, increasing procurement complexity. Raw material volatility for polymers and resin systems has affected manufacturing stability, with some suppliers experiencing 10–15% cost fluctuations. Companies are mitigating these challenges through localized production facilities, long-term supply agreements, recycled material integration, and diversified sourcing strategies to improve cost control and delivery reliability.

Emerging opportunities are developing through recyclable core materials, automated composite manufacturing, and digital engineering platforms that improve subsea structure optimization. Next-generation PET foam and hybrid core technologies can deliver 30% higher durability while reducing material waste by nearly 20%. The United Kingdom and South Korea are advancing offshore energy projects that require improved buoyancy and structural solutions. Companies are investing in R&D collaborations, simulation-based design tools, and strategic partnerships to develop customized subsea materials. A key opportunity lies in combining lightweight composites with predictive monitoring systems, enabling operators to optimize maintenance schedules and reduce unplanned offshore interventions.

Subsea core material adoption faces execution challenges related to deepwater installation conditions, engineering compatibility, and workforce specialization. More than 40% of offshore asset failures are linked to structural integrity and maintenance complexities, increasing demand for reliable material qualification processes. Brazil and Australia are expanding offshore developments but require advanced engineering capabilities for harsh marine environments. Integration of composite materials with existing subsea systems requires extensive testing, certification, and specialized installation expertise. Companies must address these barriers through digital inspection technologies, skilled workforce development, and collaborative engineering partnerships to ensure consistent deployment performance and long-term asset reliability.

Recyclable Composite Adoption Growth: Subsea operators are increasingly shifting toward recyclable PET foam and hybrid composite cores, with adoption rising by approximately 20% as sustainability targets influence offshore procurement. Companies in Norway and the United Kingdom are expanding low-carbon material portfolios, while improved recyclability and reduced processing waste are lowering lifecycle impacts by nearly 15%.

Automated Manufacturing Integration: Composite core manufacturers are adopting automated cutting, bonding, and inspection systems, improving production efficiency by 25–30% and reducing fabrication errors by around 18%. Suppliers in Germany and Japan are restructuring workflows through robotics and digital quality monitoring to address skilled labor shortages and improve delivery consistency for offshore projects.

Deepwater Asset Optimization Shift: Operators are deploying advanced core materials in subsea buoyancy modules, risers, and protection systems, with lightweight composite structures achieving 25% lower installation loads. The expansion of offshore wind projects in Europe and Asia is accelerating demand, while companies are forming engineering partnerships to customize materials for deeper and harsher operating environments.

Localized Supply Chain Expansion: Global supply-chain disruptions have encouraged material producers to establish regional manufacturing hubs, reducing lead times by 20% and improving inventory reliability by 30%. Companies are increasing local production capabilities in the United States, South Korea, and Norway to secure critical composite inputs and strengthen offshore infrastructure resilience.

Foam core materials dominate the Subsea Core Material Market, accounting for approximately 55% share due to their lightweight structure, buoyancy performance, corrosion resistance, and compatibility with large-scale subsea components. PVC foam and PET foam cores are widely adopted in offshore pipelines, buoyancy modules, and marine composite structures because they provide high strength-to-weight ratios and easier fabrication compared with traditional alternatives. Companies are increasing investments in recyclable foam technologies, with sustainable variants gaining nearly 20% higher adoption among offshore engineering firms. Syntactic foam and honeycomb cores represent emerging segments, with syntactic foam growing fastest due to superior pressure resistance in deepwater applications. Adoption is increasing as operators move toward deeper offshore installations requiring enhanced durability. Balsa and other specialized cores maintain relevance in cost-sensitive marine applications, while manufacturers are prioritizing hybrid core solutions to balance performance, weight, and environmental requirements.

Subsea buoyancy modules represent the leading application segment with approximately 40% market share, supported by rising deployment of offshore pipelines, risers, and floating infrastructure requiring lightweight and pressure-resistant materials. These systems benefit from advanced foam and syntactic cores that improve buoyancy performance while reducing installation complexity. Companies are expanding specialized production capabilities to support offshore energy projects requiring longer operational lifecycles. Subsea pipeline insulation and protection applications are the fastest-growing segment, driven by deepwater exploration and offshore wind infrastructure expansion. Demand is increasing as operators seek materials capable of reducing thermal losses and protecting critical assets, with composite-based solutions improving operational efficiency by nearly 25%. Other applications, including underwater vehicles and marine structures, are adopting advanced core materials gradually as manufacturers develop customized solutions for specialized operating conditions.

Offshore oil and gas companies represent the dominant end-user segment with approximately 50% share due to extensive use of subsea pipelines, risers, and deepwater infrastructure. Major operators are adopting advanced core materials to reduce maintenance requirements and improve asset longevity, with composite-based systems enabling weight reductions of 25–30% compared with conventional structures. Companies are strengthening partnerships with composite suppliers to develop application-specific materials for challenging offshore environments. Offshore wind developers are the fastest-growing end-user group as global renewable infrastructure expands and requires lightweight marine components. Adoption among offshore wind projects is increasing by nearly 25% as developers prioritize corrosion-resistant materials and reduced installation complexity. Marine engineering firms and defense organizations continue adopting specialized core materials for vessels, underwater systems, and research platforms, creating additional demand diversification.

Europe accounted for the largest market share at 35% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America accounted for approximately 25% of the global subsea core material market in 2025, supported by deepwater oil and gas operations, offshore wind development, and advanced marine engineering capabilities. The United States represents the majority of regional demand due to Gulf of Mexico subsea activities and increasing offshore energy investments. Composite core materials are increasingly integrated into buoyancy modules, risers, and subsea protection systems, improving structural efficiency by nearly 30%. Growing collaboration between offshore operators and composite manufacturers is strengthening domestic supply capabilities. Companies are expanding localized production and investing in automated fabrication technologies to reduce dependence on international supply chains and improve project execution timelines.

United States Market Outlook: The United States remains the strategic hub for subsea core material adoption, driven by Gulf of Mexico infrastructure and emerging offshore wind projects along the Atlantic coast. More than 70 offshore energy operators are integrating advanced composite solutions to improve asset durability and reduce maintenance requirements. Strong engineering capabilities and domestic manufacturing expansion position the country as a key innovation center.

Europe held the leading position in subsea core material adoption with approximately 35% market share in 2025, driven by offshore wind expansion, mature subsea engineering networks, and sustainability-focused infrastructure development. Countries such as Norway, the United Kingdom, and Germany are accelerating deployment of lightweight composite materials for offshore structures and marine applications. European operators are prioritizing recyclable core materials, with sustainable composite adoption increasing by nearly 20% across new offshore projects. Strong regulatory focus on emissions reduction and asset efficiency is encouraging manufacturers to develop advanced PET foam, PVC foam, and hybrid core technologies. Companies are strengthening partnerships with offshore developers to support large-scale renewable infrastructure deployment.

Norway Market Outlook: Norway leads European subsea core material deployment due to its established offshore energy ecosystem, advanced marine technology capabilities, and extensive deepwater operations. The country contributes nearly 28% of global subsea core material demand and continues expanding composite applications across offshore platforms, pipelines, and floating energy systems. Its strong engineering expertise supports next-generation material adoption.

Asia-Pacific represented approximately 22% of the global subsea core material market in 2025 and is becoming the fastest-expanding market due to offshore energy development, marine infrastructure investments, and composite manufacturing growth. China, South Korea, Japan, and Australia are increasing adoption of advanced core materials across offshore wind foundations, subsea equipment, and marine structures. Regional manufacturers are expanding production capacity, with composite processing output increasing by nearly 25% in key industrial hubs. Offshore wind expansion in China and South Korea is creating new demand for lightweight, corrosion-resistant materials. Companies are establishing regional partnerships and localized manufacturing networks to improve supply reliability and reduce project delivery constraints.

China Market Outlook: China represents the largest Asia-Pacific opportunity due to its extensive offshore wind installations, marine manufacturing base, and composite production capabilities. The country accounts for more than 40% of regional offshore wind capacity additions, creating strong demand for advanced subsea materials. Domestic suppliers are increasing investments in automated composite manufacturing to support large infrastructure projects.

South America accounted for approximately 10% of global subsea core material demand in 2025, supported primarily by Brazil’s offshore oil and gas sector. Deepwater exploration activities in the Santos and Campos basins are increasing requirements for lightweight buoyancy systems, subsea insulation, and corrosion-resistant composite structures. Brazil’s offshore operators are adopting advanced materials to improve operational reliability, with composite solutions reducing structural weight by nearly 25% compared with conventional systems. However, limited regional manufacturing capacity creates reliance on imported specialized materials. Companies are responding through supplier partnerships, regional distribution expansion, and technology transfer initiatives to strengthen local availability.

Brazil Market Outlook: Brazil dominates South America’s subsea core material market due to its large deepwater production infrastructure and offshore engineering expertise. The country operates one of the world’s largest deepwater oil production networks, creating continuous demand for advanced subsea components. Investments in offshore modernization are encouraging greater adoption of composite-based solutions.

The Middle East & Africa region represented approximately 8% of the global subsea core material market in 2025, supported by offshore oil and gas modernization projects and expanding marine infrastructure investments. Countries including Saudi Arabia, the United Arab Emirates, and Angola are improving subsea asset performance through advanced composite materials. Offshore operators are increasingly adopting lightweight core structures to enhance installation efficiency and extend equipment service life by nearly 20%. Infrastructure expansion and localization initiatives are encouraging partnerships between international material suppliers and regional engineering companies. Companies are focusing on customized solutions, local technical support, and supply-chain development to improve deployment efficiency.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic subsea materials market due to large-scale offshore energy investments and industrial localization programs. The country is strengthening marine engineering capabilities through domestic manufacturing initiatives and partnerships with global technology providers. Growing offshore infrastructure requirements are supporting increased adoption of advanced composite materials for durable subsea applications.

The Subsea Core Material Market features global composite material leaders such as Diab Group, Gurit, and 3A Composites competing against specialized marine suppliers and regional manufacturers focused on cost efficiency and customization. The top five players collectively account for approximately 45% of specialized subsea core material supply, creating a moderately consolidated structure. Competition centers on advanced material performance, supply reliability, customization capability, and production scalability. Technology-focused suppliers achieve 20–30% performance advantages through recyclable foam cores and hybrid structures, while cost-focused manufacturers compete through localized production and streamlined logistics. Players are expanding manufacturing capacity, forming offshore engineering partnerships, and integrating automated fabrication systems. The market is shifting toward sustainable composites, digital material design, and regional supply-chain control. High certification requirements, technical expertise, and offshore qualification processes create strong entry barriers. Winning companies must combine material innovation, reliable delivery networks, and application-specific engineering capabilities.

Gurit Holding AG

3A Composites Core Materials

Armacell International S.A.

Evonik Industries AG

CoreLite Inc.

Maricell S.r.l.

BASF SE

Solvay S.A.

Hexcel Corporation

Plascore Incorporated

The Gill Corporation

Advanced foam core technologies are reshaping subsea structures through improved strength-to-weight performance, with PET and PVC foam cores replacing heavier conventional materials. These solutions deliver approximately 25–35% weight reduction while improving corrosion resistance and lifecycle durability. Adoption is increasing across buoyancy modules, subsea pipelines, and offshore wind components as operators prioritize efficient installation and reduced maintenance requirements.

Digital engineering, automated manufacturing, and AI-assisted material simulation are becoming important competitive differentiators. Automated composite fabrication improves production consistency by nearly 20% and reduces processing delays compared with traditional manual methods. Leading suppliers are integrating predictive design tools to customize materials faster for deepwater applications, creating advantages for technology-driven manufacturers.

Between 2026 and 2028, recyclable composites and hybrid core structures will gain stronger adoption as sustainability requirements influence offshore procurement. New-generation materials provide improved environmental performance while maintaining structural reliability. Companies investing in automation, material recycling, and localized production networks will gain advantages through faster delivery, lower operational costs, and stronger positioning in offshore infrastructure projects.

September 2025 Gurit secured a multi-year subsea supply contract for Corecell structural foam core materials and announced expansion of its Australia operations to support demand. The project strengthens subsea supply capability and supports additional production capacity for advanced composite applications. Source: www.gurit.com

May 2025 3A Composites Core Materials officially declared BALTEK® SBC products as FSC™ MIX certified in selected markets, improving traceability across its balsa core supply chain. The sustainability initiative strengthens customer compliance capabilities and supports responsible material sourcing strategies. Source: www.3accorematerials.com

June 2025 Armacell opened a new aerogel insulation manufacturing facility in Pune, India, doubling available ArmaGel XG production capacity. The expansion improves global supply flexibility for advanced foam-based applications and strengthens localized manufacturing capabilities. Source: www.armacell.com

January 2026 Diab Group partnered with Starboard to apply Divinycell PVC core materials in high-performance marine composite structures. The collaboration highlights increased adoption of lightweight sandwich materials, improving strength-to-weight performance and supporting sustainable marine product development.

The Subsea Core Material Market Report covers comprehensive analysis across material types including foam cores, syntactic foam, honeycomb cores, balsa cores, and hybrid structures. The study evaluates applications such as subsea buoyancy systems, pipeline protection, offshore structures, underwater vehicles, and marine engineering components. It includes analysis of offshore energy operators, marine engineering firms, and specialized composite manufacturers across major global markets.

The report provides strategic insights into regional dynamics covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines technology adoption patterns, supplier positioning, manufacturing expansion, sustainability trends, and emerging composite innovations. The analysis supports investment decisions, partnership strategies, market expansion planning, and competitive positioning through 2033 by identifying high-potential segments and evolving industry priorities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 85.0 Million |

| Market Revenue (2033) | USD 165.7 Million |

| CAGR (2026–2033) | 8.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Diab Group; Gurit Holding AG; 3A Composites Core Materials; Armacell International S.A.; Evonik Industries AG; CoreLite Inc.; Maricell S.r.l.; BASF SE; Solvay S.A.; Hexcel Corporation; Plascore Incorporated; The Gill Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |