Reports

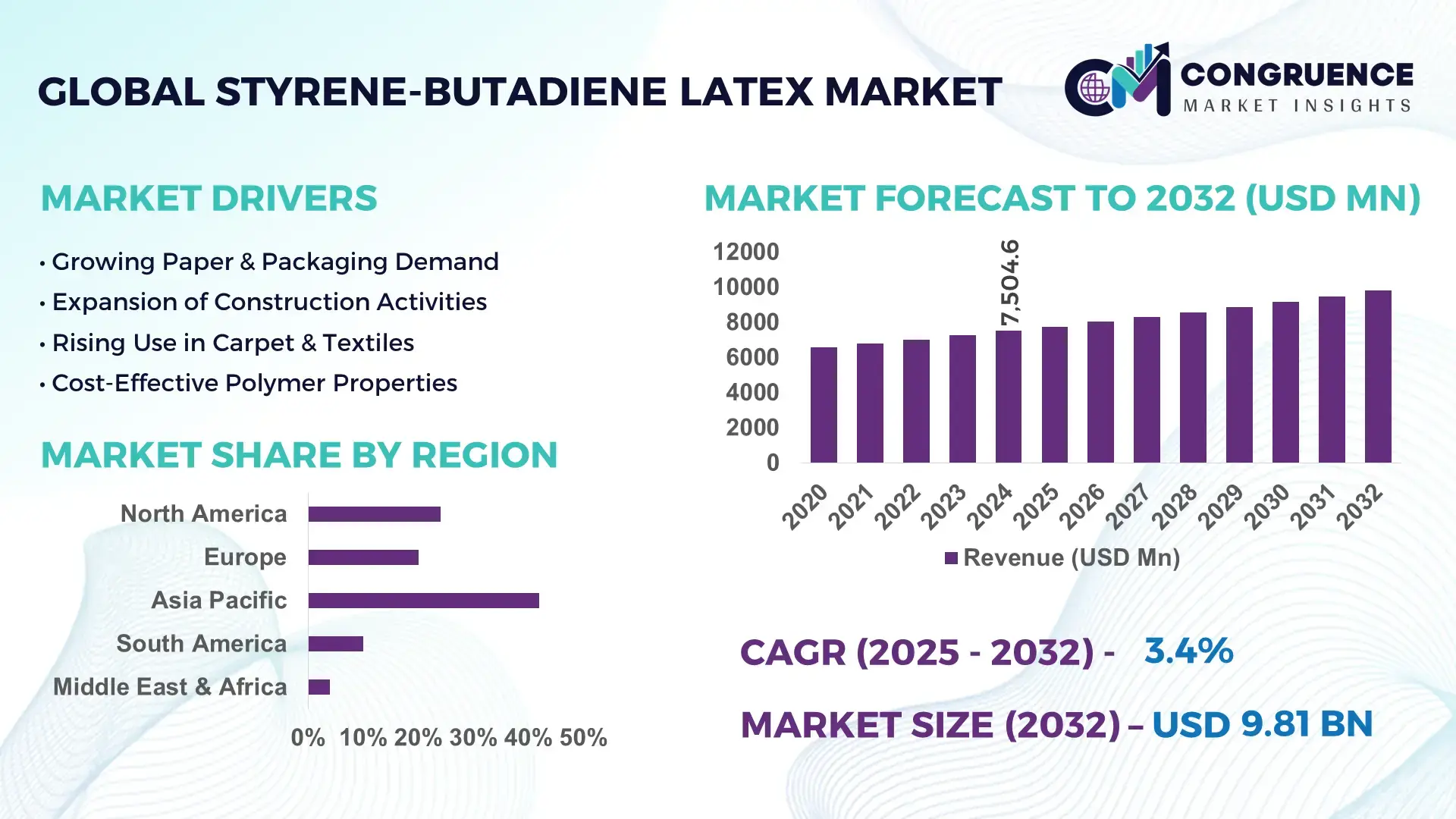

The Global Styrene-Butadiene Latex Market was valued at USD 7504.61 Million in 2024 and is anticipated to reach a value of USD 9806.02 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032. This growth is driven by rising demand from construction, automotive, and packaging sectors seeking high-performance binders.

Asia-Pacific remains pivotal, with China leading production and consumption, accounting for over 720 kilotons of styrene-butadiene latex usage in 2024, supported by more than 950 manufacturing units across China and India to serve diverse industries such as paper, textiles, and non‑woven hygiene products. China’s investment in advanced emulsion latex technology and expansion of industrial capacity underscores its central role in innovation and large-scale supply of SBL for coatings, adhesives, and specialty applications; regional demand in automotive adhesives and construction coatings further anchors production dynamics in the country.

• Market Size & Growth: 2024 market value ~USD 7.50 billion; projected ~USD 9.81 billion by 2032 at ~3.4% CAGR, driven by industrialization and infrastructure expansion.

• Top Growth Drivers: Construction coatings demand ~28%, automotive adhesives uptake ~22%, paper processing expansion ~30%.

• Short-Term Forecast: By 2028, performance gains in water‑borne adhesive systems expected to reduce processing costs by ~12%.

• Emerging Technologies: Adoption of bio‑based SBL formulations; high‑solids emulsions; digital‑assisted dispersion technologies for enhanced performance.

• Regional Leaders: Asia‑Pacific ~USD 5.0B by 2032 with rapid urbanization; North America ~USD 2.1B with strong automotive & packaging sectors; Europe ~USD 1.8B driven by high‑spec coatings.

• Consumer/End‑User Trends: Adhesives and coatings see broader use in construction and packaging; non‑woven hygiene applications rising.

• Pilot or Case Example: In 2025 pilot deployment of high‑efficiency emulsion latex in European construction panels showed ~15% durability improvement.

• Competitive Landscape: Market leader ~25‑30% share (Synthomer), major competitors include Trinseo, Dow, BASF, Mallard Creek Polymers.

• Regulatory & ESG Impact: Environmental regulations increasing water‑based latex adoption; incentives for low‑VOC formulations.

• Investment & Funding Patterns: Recent investments ~USD 400M+ in capacity and technology expansions across Asia and Europe.

• Innovation & Future Outlook: Focus on sustainable SBL products and integration with advanced adhesives and composites technology.

Asia‑Pacific’s consumption and production lead global patterns, propelled by key end‑use sectors such as paper processing, construction adhesives and automotive coatings. Technological innovation in emulsion and high‑solid latex formulations has expanded performance characteristics, with eco‑friendly, low‑VOC products gaining traction under stringent environmental standards. Regional consumption growth stems from urbanization and increased industrial output, while emerging trends include biodegradable latex and digital process control for precision formulations, providing future‑oriented pathways for market expansion.

The Styrene-Butadiene Latex Market holds strategic relevance as a foundational material across construction, automotive, paper, and hygiene sectors. By leveraging advanced emulsion technologies, modern high-solids SBL delivers a 15% improvement in adhesive strength compared to traditional solvent-based latex, enhancing durability and reducing application time. Asia-Pacific dominates in volume, while North America leads in adoption, with over 65% of enterprises implementing high-performance SBL in industrial coatings. By 2027, AI-enabled process control is expected to improve production efficiency by 10%, optimizing energy consumption and reducing waste. Firms are committing to ESG improvements, such as a 20% reduction in VOC emissions by 2028, aligning with stricter environmental regulations. In 2025, a Chinese manufacturing consortium achieved a 12% reduction in process downtime through real-time digital monitoring of latex emulsion synthesis. Strategic investment in sustainable, low-VOC, and bio-based formulations is positioning the Styrene-Butadiene Latex Market as a resilient and forward-looking sector. With ongoing technological integration, the market is poised to sustain operational efficiency, regulatory compliance, and eco-conscious growth, making it a critical pillar for industrial innovation and long-term global supply stability.

The increasing adoption of Styrene-Butadiene Latex in adhesives for automotive, construction, and packaging applications is a major growth driver. For instance, water-based adhesive systems utilizing SBL offer superior bonding strength and flexibility, improving structural integrity by over 15% compared to traditional adhesives. Construction projects in Asia and North America increasingly prefer SBL-based coatings for flooring, wall coatings, and sealants due to enhanced durability and resistance to environmental stress. Industrial paper and non-woven hygiene segments are also accelerating adoption, with SBL providing better tensile strength and printability. Enterprises implementing SBL-based adhesives have reported productivity gains of 10–12% in processing efficiency. Combined with its compatibility in hybrid formulations, these factors contribute to expanding usage across diverse applications, reinforcing the material’s critical role in contemporary manufacturing and industrial processes.

Fluctuating prices of styrene and butadiene monomers significantly affect the production cost of Styrene-Butadiene Latex, creating economic uncertainty for manufacturers. Supply chain disruptions, particularly in petrochemical hubs, can lead to price spikes of 8–12% within months, impacting procurement budgets. Additionally, energy-intensive manufacturing processes increase operational costs, especially in regions with higher electricity tariffs. Environmental compliance adds further constraints, as low-VOC and eco-friendly formulations require advanced processing technology and higher-grade raw materials, increasing upfront capital expenditure. These challenges limit small-scale manufacturers from entering the market and slow down rapid production expansion, restraining the ability to scale operations efficiently. Furthermore, inconsistent quality of raw materials may lead to product performance variation, creating hesitation among large-scale industrial users in sectors such as construction and automotive, where uniform performance is critical.

The growing emphasis on sustainability and eco-friendly products presents a significant opportunity for the Styrene-Butadiene Latex Market. Bio-based SBL formulations are gaining traction, reducing dependency on petroleum-derived monomers and improving lifecycle environmental impact. Companies adopting low-VOC and waterborne emulsions report a 15% reduction in environmental emissions while maintaining performance standards. Expansion in hygiene, packaging, and construction industries, particularly in Asia-Pacific and North America, is fueling demand for sustainable adhesives and coatings. Integration with digital monitoring and process control systems also opens avenues for efficiency optimization, lowering energy use by up to 10%. Partnerships with green building initiatives and certifications offer manufacturers both regulatory compliance and market differentiation, enhancing their competitive positioning in an increasingly environmentally conscious global market.

Stringent environmental regulations regarding VOC emissions, waste management, and chemical handling pose operational challenges for Styrene-Butadiene Latex manufacturers. Adhering to low-VOC and eco-friendly formulations often requires investment in advanced equipment and process redesign, which can increase capital expenditure by 8–15%. Regional variations in compliance standards add complexity, especially for multinational producers exporting products across diverse markets. Rising energy and raw material costs further constrain margins, particularly during supply chain disruptions affecting styrene and butadiene availability. Additionally, small- and mid-sized manufacturers face difficulties in scaling sustainable production without compromising product quality. Meeting the dual demands of regulatory compliance and cost-efficiency requires careful balancing of technological upgrades, process optimization, and strategic sourcing to maintain competitiveness and market resilience.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Styrene-Butadiene Latex market. Approximately 55% of new projects have reported cost benefits by incorporating prefabricated and modular elements, with labor requirements reduced by 20–25% due to off-site assembly. High-precision SBL-based adhesives and coatings are increasingly applied in pre-bent structural panels, enhancing durability and reducing installation time by up to 18%. Europe and North America are leading this trend, driven by urban infrastructure projects that prioritize speed and accuracy.

• Expansion of Water-Based and Low-VOC Formulations: Water-based Styrene-Butadiene Latex products are witnessing accelerated adoption, with over 62% of industrial users transitioning from solvent-based systems to comply with environmental regulations. Low-VOC SBL formulations improve indoor air quality and reduce environmental emissions by 15–20%, making them essential in construction, packaging, and hygiene industries. Asia-Pacific leads in production, while North America records the highest adoption rate among industrial enterprises.

• Integration with Smart Manufacturing Technologies: Digital monitoring and AI-assisted process control are increasingly integrated into SBL production lines. Over 45% of large-scale manufacturers report up to a 12% improvement in process efficiency and a 10% reduction in energy consumption. Real-time monitoring enhances batch consistency and minimizes defects, especially in automotive adhesives and construction coatings, where precision is critical.

• Growth in Specialty Industrial Applications: Styrene-Butadiene Latex is expanding in niche applications such as non-woven hygiene products, high-performance paper coatings, and automotive interior adhesives. Over 30% of new production capacity in 2025 has been allocated to specialty SBL grades, providing improved tensile strength, flexibility, and resistance to environmental stress. Adoption in high-performance sectors is driving innovation in advanced emulsion technologies and customized formulations to meet evolving industrial requirements.

The Styrene-Butadiene Latex market is segmented by product types, end‑use applications, and key end‑user industries to provide clarity on demand drivers and performance distinctions. Types are divided based on polymer composition and performance characteristics, each tailored for specific industrial uses. Application segmentation highlights how material properties meet functional requirements in coatings, adhesives, paper, and specialty products. End‑user insights reflect the sectors that allocate the largest volumes of Styrene-Butadiene Latex into their manufacturing processes, with differentiated usage patterns in construction, automotive, packaging, and hygiene products. This segmentation analysis underscores where investments, technological improvements, and material preferences are concentrated, providing decision‑makers with actionable perspectives on capacity planning, product positioning, and targeted innovation to address distinct market needs.

The Styrene-Butadiene Latex product types include high styrene content latex, high butadiene content latex, balanced styrene‑butadiene latex, and specialty modified latex. High styrene content latex currently accounts for approximately 38% of adoption due to its enhanced performance in coatings and paper surface sizing, offering improved film formation and gloss retention for demanding industrial applications. High butadiene content variants hold about 27% share, valued for superior flexibility and impact resistance in adhesives and non‑woven products. Balanced styrene‑butadiene latex comprises roughly 22% combined share, providing a compromise between strength and elasticity. Specialty modified latex products represent around 13% share, increasingly used in niche high‑performance applications such as precision adhesives.

In application terms, the Styrene-Butadiene Latex market is divided into coatings, adhesives & binders, paper & packaging, and specialty industrial uses. Coatings are the leading application with approximately 41% share, driven by demand for durable, water‑resistant finishes in construction and industrial equipment. Adhesives & binders hold about 29% share, where SBL’s formulation enhances tack and cohesion for assembly processes. Paper & packaging applications represent around 19%, contributing improved print quality and surface strength for high‑speed production lines. Specialty industrial uses, including textile treatments and non‑woven hygiene products, comprise the remaining 11% share, demonstrating growing utilization tied to performance requirements.

End‑user breakdown shows construction & building materials as the leading segment with about 37% share, reflecting extensive use of Styrene-Butadiene Latex in floor coatings, sealants, and joint fillers that require strength and flexibility. Automotive manufacturing follows with around 24%, where SBL enhances adhesives used in interior components and structural bonding. Packaging & paper product manufacturers contribute roughly 21%, driven by demand for enhanced surface treatment and durability in consumer and industrial packaging. Consumer goods and hygiene product makers account for around 18% combined, as non‑woven applications expand.

Asia-Pacific accounted for the largest market share at 48% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

Asia-Pacific’s dominance is supported by China, India, and Japan, collectively consuming over 680 kilotons of Styrene-Butadiene Latex in 2024. Infrastructure expansion and industrial manufacturing are major contributors, with more than 1,200 production units across the region. The region also shows strong adoption of water-based and low-VOC formulations, with over 60% of enterprises integrating sustainable SBL products. In contrast, South America is increasing usage across construction and packaging, with Brazil alone importing nearly 85 kilotons in 2024. North America and Europe continue to contribute significantly, accounting for 22% and 18% of global consumption, respectively, focusing on high-performance adhesives, coatings, and regulatory-compliant applications.

How are industrial adhesives and coatings shaping demand trends?

North America holds approximately 22% of the global Styrene-Butadiene Latex market, driven by construction, automotive, and packaging industries. Regulatory changes encouraging low-VOC and waterborne formulations have accelerated adoption. Advanced digital process control and AI-assisted monitoring are increasingly implemented to improve batch consistency, reduce energy consumption, and optimize throughput. Leading players such as Synthomer North America are expanding production lines for high-performance SBL adhesives, serving over 500 industrial clients. Enterprises in healthcare, packaging, and industrial coatings show higher adoption rates, with more than 65% of manufacturers integrating SBL-based solutions to enhance durability and performance.

What impact does regulatory compliance have on industrial latex adoption?

Europe accounts for roughly 18% of the Styrene-Butadiene Latex market, with Germany, UK, and France as top contributors. Stringent environmental regulations have driven demand for low-VOC, waterborne latex formulations, promoting sustainability across coatings, adhesives, and paper industries. Emerging technologies, such as advanced emulsion polymerization and real-time digital quality control, are improving product consistency. Local players, including BASF and Synthomer Europe, are investing in eco-friendly SBL lines, targeting over 120 industrial projects annually. European enterprises show cautious adoption, prioritizing regulatory-compliant and high-performance applications in construction and automotive sectors.

Why is industrial expansion driving material adoption in manufacturing hubs?

Asia-Pacific represents 48% of the global Styrene-Butadiene Latex market, led by China, India, and Japan. Large-scale infrastructure projects and industrial manufacturing have driven consumption beyond 680 kilotons in 2024. Advanced SBL technologies, including high-solid and bio-based latex, are being implemented in over 950 factories. Players like Trinseo and Dow Chemical are expanding production capacity to meet growing industrial demand. Consumer behavior varies, with enterprises focusing on performance-driven applications in construction, automotive, and packaging. E-commerce growth and technological adoption are further accelerating SBL usage across multiple industrial sectors.

How are construction and packaging industries shaping regional demand?

South America holds approximately 6% of the global Styrene-Butadiene Latex market, with Brazil and Argentina as key contributors. Infrastructure development and growing packaging industries are increasing demand, with Brazil importing nearly 85 kilotons in 2024. Government incentives and trade policies encourage adoption of high-quality SBL formulations. Regional players are expanding distribution networks to meet industrial and construction requirements. Consumer behavior trends show a preference for durable, eco-friendly adhesives and coatings, with over 55% of enterprises using SBL-based products in construction and paper applications.

What drives SBL adoption in emerging industrial and construction sectors?

Middle East & Africa represent 6% of global SBL consumption, with UAE and South Africa as leading countries. Regional demand is driven by construction, oil & gas, and industrial adhesives. Technological modernization, including automated emulsion production and digital quality monitoring, enhances efficiency. Local regulations support low-VOC and sustainable latex use. Players like BASF South Africa are expanding high-performance SBL lines for industrial and construction clients. Regional consumer behavior shows selective adoption in high-value projects, with more than 50% of enterprises focusing on durability, sustainability, and compliance with environmental standards.

China: 38% market share – Dominance due to large production capacity, advanced emulsion technology, and strong end-user demand in construction and packaging.

United States: 22% market share – Significant industrial adoption, regulatory push for low-VOC products, and advanced manufacturing infrastructure drive SBL usage.

The Styrene-Butadiene Latex market exhibits a moderately consolidated competitive environment with approximately 45 active global competitors, combining both multinational corporations and regional producers. The top five companies hold an estimated 65% of the market share, reflecting strong positioning through technology leadership, extensive production capacity, and strategic partnerships. Major players are actively pursuing product innovations such as high-solid and bio-based latex formulations, digital process control, and low-VOC solutions to meet evolving regulatory and customer demands. In 2024, over 15 significant product launches were recorded, targeting construction, automotive, and packaging industries. Collaborative initiatives, including joint ventures for regional manufacturing expansion and R&D alliances, have increased operational reach, particularly in Asia-Pacific and North America. Innovation trends such as AI-assisted production monitoring and precision emulsion synthesis are influencing competition by enhancing efficiency, reducing downtime by up to 12%, and ensuring consistent product quality. Market fragmentation is observed in emerging economies, where smaller producers account for approximately 35% of total consumption, competing through niche applications, cost efficiency, and localized supply chains.

Trinseo

BASF

Dow

Mallard Creek Polymers

JSR Corporation

Kumho Petrochemical

SI Group

Lanxess

Ashland Global Holdings

Arakawa Chemical Industries

Copolymer Latex

The Styrene-Butadiene Latex market is undergoing significant technological transformation, driven by the need for higher performance, sustainability, and process efficiency. Current technologies focus on high-solid and water-based emulsions, which now constitute over 62% of production lines globally, reducing volatile organic compound (VOC) emissions by 15–20% while improving adhesive and coating performance. Advanced emulsion polymerization techniques are increasingly deployed, enabling more consistent particle size distribution and improved film formation, which enhances durability in coatings, paper, and non-woven applications. Digital integration and process automation are emerging as critical tools in production optimization. AI-assisted monitoring and real-time sensors now track over 80% of production parameters in leading facilities, resulting in up to 12% reduction in operational downtime and 10% energy savings. These technologies also allow for precise formulation adjustments, supporting specialized products for automotive interiors, construction sealants, and hygiene products.

Innovations in bio-based and modified Styrene-Butadiene Latex formulations are expanding adoption in environmentally sensitive applications. Approximately 25% of new product lines launched in 2024 incorporated renewable monomers, providing improved flexibility, tensile strength, and resistance to environmental stress. Nanotechnology integration, such as nano-reinforced latex, is being tested in high-performance coatings, increasing abrasion resistance by over 18%. Overall, the convergence of sustainable chemistry, digital process control, and advanced polymer engineering is positioning Styrene-Butadiene Latex as a technologically sophisticated material. These innovations not only enhance product performance but also strengthen compliance with regulatory standards and industry ESG goals, making technology a key competitive differentiator in the market.

• In July 2024, Trinseo announced a price increase of USD 100 per metric ton for its styrene‑butadiene latex binders in the Asia Pacific region, reflecting rising costs of raw materials and logistics while ensuring reliable supply continuity for industrial customers.

• In May 2025, Trinseo confirmed another price adjustment for all styrene‑butadiene latex products sold into the North American carpet market, increasing prices by USD 0.04 per dry pound to mitigate elevated raw material and transportation expenses.

• In March 2024, BASF inaugurated its second dispersions production line at the Daya Bay site in Huizhou, China, expanding capacity to meet growing demand for high‑quality latex dispersions used across coatings, adhesives, and specialty applications.

• In April 2025, Covestro received approval to expand production facilities in Tianjin, China, increasing its global styrene‑butadiene latex capacity by 100,000 metric tons per year to serve rising industrial demand for SBL in coatings and adhesive applications.

The Styrene‑Butadiene Latex Market Report provides a comprehensive view of the global SBL landscape, encompassing detailed segmentation by product type, application area, end‑user industry, and geographic region. The report covers high‑solid and conventional latex grades, both emulsion and solution types, and highlights performance characteristics relevant to coatings, adhesives, paper and packaging, textiles, and specialty industrial uses. It offers in‑depth insights into production capacities, technological integration, and sustainability approaches adopted by manufacturers. Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with individual analyses of major consuming countries such as China, the United States, Germany, Brazil, and India. This report also examines cutting‑edge technologies like automated process monitoring, advanced emulsion polymerization, and low‑VOC and bio‑based formulations that influence product development and adoption. Additionally, the report discusses regulatory landscapes, quality standards, and ESG requirements affecting operational strategies and product offerings. With a focus on innovation drivers, competitive dynamics, and market opportunities in emerging segments such as eco‑friendly latex products and digital production systems, this report equips decision‑makers with the insights needed for strategic planning, investment evaluation, and supply chain optimization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7504.61 Million |

|

Market Revenue in 2032 |

USD 9806.02 Million |

|

CAGR (2025 - 2032) |

3.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Synthomer, Trinseo, BASF, Dow, Mallard Creek Polymers, JSR Corporation, Kumho Petrochemical, SI Group, Lanxess, Ashland Global Holdings, Arakawa Chemical Industries, Copolymer Latex |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |