Reports

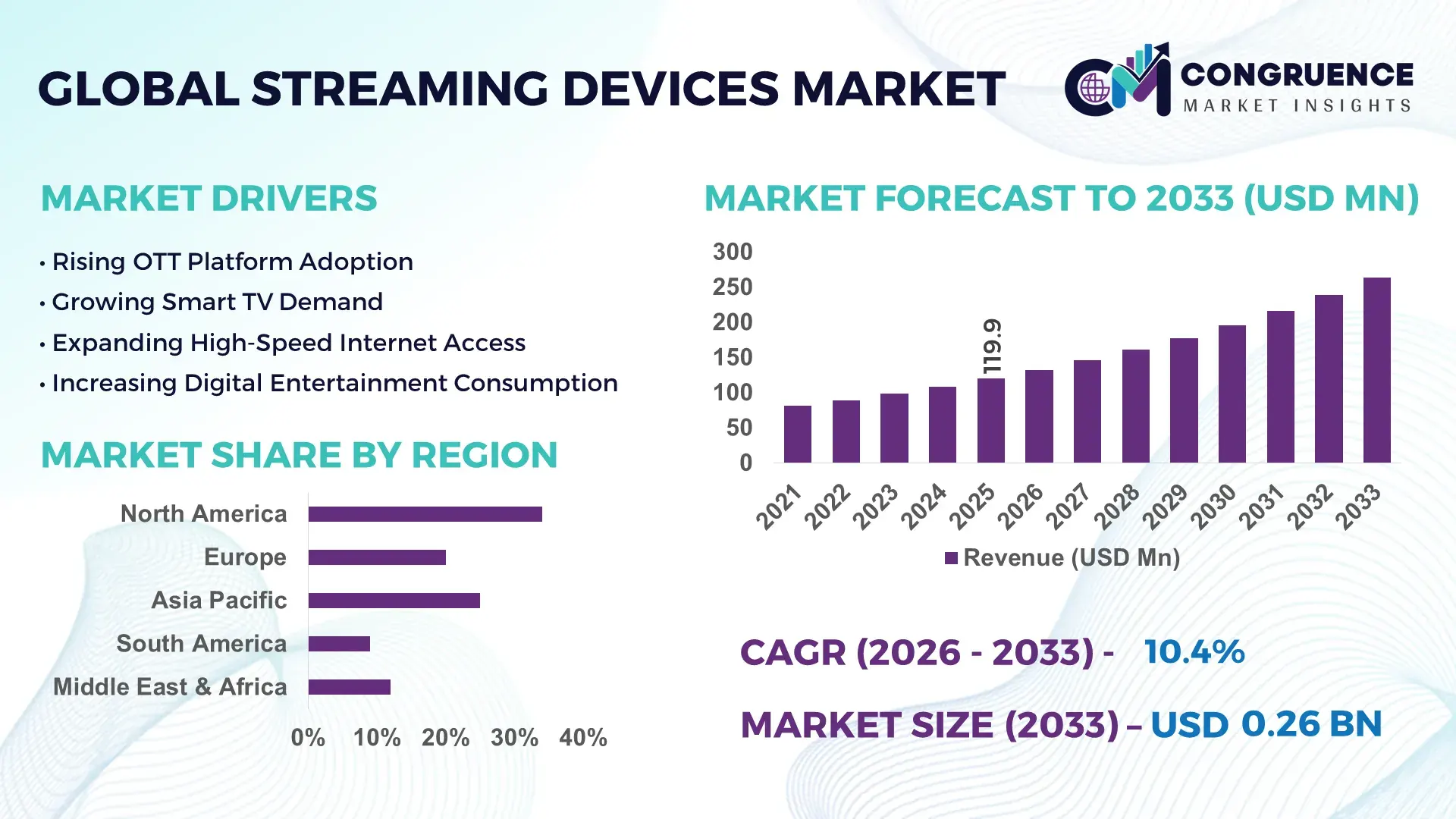

The Global Streaming Devices Market was valued at USD 119.87 Million in 2025 and is anticipated to reach a value of USD 263.75 Million by 2033 expanding at a CAGR of 10.36% between 2026 and 2033.

Rising integration of AI-powered content recommendation engines, 4K/8K streaming support, and Wi-Fi 6-enabled devices has accelerated replacement cycles, while smart TV ecosystem expansion lowered standalone streaming hardware costs by nearly 18% between 2024 and 2026. The market is operating amid intensified semiconductor localization efforts across Asia-Pacific and North America following Red Sea shipping disruptions and tightening digital platform regulations in the EU and U.S., forcing manufacturers to diversify component sourcing and firmware compliance strategies in 2026.

The United States dominates the global streaming devices market with nearly 34% share, supported by over 92 million active connected-TV households and sustained investments exceeding USD 4 billion in smart entertainment ecosystems, cloud streaming infrastructure, and ad-supported digital platforms. Consumer adoption of 4K-enabled streaming devices surpassed 61% in 2026, compared with 44% in 2023, reflecting faster migration toward premium viewing experiences. Major technology and media companies continue integrating AI-driven personalization, voice control, and cross-device synchronization, improving user engagement rates by more than 27%. Compared with several European markets, U.S. device upgrade frequency remains nearly 1.6x higher due to bundled subscription offerings and aggressive retail promotions.

Manufacturers prioritizing AI-enabled operating systems, regional supply-chain resilience, and premium content interoperability are positioned to secure higher-margin growth in the advanced global streaming devices market.

Market Size & Growth: USD 119.87 Million in 2025 to USD 263.75 Million by 2033, driven by 4K streaming penetration, AI-enabled interfaces, and connected-home expansion.

Top Growth Drivers: Smart TV integration rose 29%, ad-supported streaming usage increased 31%, and Wi-Fi 6 device adoption expanded 24% globally.

Short-Term Forecast: By 2027, device boot efficiency improves 22% while streaming latency declines nearly 18% through advanced chipset optimization.

Emerging Technologies: AI voice assistants, edge-based content caching, and AV1 compression technology reduce bandwidth consumption by up to 30%.

Regional Leaders: North America exceeds USD 82 Million with premium streaming adoption; Asia-Pacific crosses USD 74 Million through affordable devices; Europe surpasses USD 58 Million driven by smart-home integration.

Consumer/End-User Trends: Over 63% of urban users prefer multi-platform streaming devices supporting gaming, live sports, and OTT aggregation.

Pilot/Case Example: In 2026, a leading streaming hardware rollout improved ad-targeting efficiency by 26% and boosted viewing retention by 19%.

Competitive Landscape: The top five players control nearly 57% market share, led by integrated ecosystem providers and AI-focused device manufacturers.

Regulatory & ESG Impact: Energy-efficient streaming chipsets lowered device power consumption by 21% amid stricter EU electronics sustainability standards.

Investment & Funding: More than USD 3.6 billion entered smart entertainment infrastructure, driven by platform partnerships and regional manufacturing expansion.

Innovation & Future Outlook: Hybrid streaming-gaming devices, cloud-based personalization, and localized content ecosystems are reshaping next-generation competitive positioning.

Video entertainment platforms contribute nearly 46% of total streaming device demand, followed by gaming and interactive media applications at approximately 28%, reflecting broader convergence between entertainment and connected-home ecosystems. AI-driven interface personalization and AV1 codec integration improved streaming efficiency by nearly 30% while reducing bandwidth dependency across high-density urban networks. Asia-Pacific continues leading unit shipments with over 39% share due to cost-efficient manufacturing and rising smart TV penetration, while North America maintains dominance in premium device upgrades. Regulatory pressure on energy-efficient electronics and ongoing semiconductor supply-chain diversification are accelerating innovation cycles. The market is steadily shifting toward integrated, subscription-linked streaming ecosystems with stronger cross-platform interoperability and advanced advertising intelligence.

The streaming devices market is rapidly transforming into a strategic battleground for consumer engagement, digital advertising control, and connected-home ecosystem expansion. Device manufacturers are accelerating investments in AI-enabled operating systems, integrated gaming functionality, and localized content optimization to secure recurring platform revenue rather than one-time hardware sales. The market is shifting beyond media consumption toward data-driven household intelligence, where user analytics and cross-platform interoperability determine competitive positioning. Ongoing semiconductor localization initiatives and stricter digital platform regulations across North America and Europe are forcing companies to redesign sourcing and software compliance frameworks while optimizing production resilience.

AI-powered adaptive streaming technology improves content delivery efficiency by 32% while reducing bandwidth management costs by 24% compared to legacy buffering-based systems. Asia-Pacific leads in shipment volume with nearly 41% of global unit output, while North America leads in premium adoption and innovation with 58% penetration of AI-integrated streaming ecosystems. Over the next three years, cloud-synchronized streaming interfaces are projected to improve viewer retention rates by 21% and reduce platform switching frequency by 17%. Energy-efficient chip architectures are also creating ESG-linked competitive advantages by lowering device power consumption nearly 19%, strengthening compliance access in regulated electronics markets.

In 2026, a major smart streaming ecosystem deployment improved advertising conversion efficiency by 28% through AI-driven personalization and predictive content sequencing. Industry leaders are increasingly shifting capital allocation toward subscription-linked hardware, regional assembly expansion, and proprietary operating systems to strengthen ecosystem control and reduce dependency on third-party platforms. Companies optimizing software intelligence, energy efficiency, and ecosystem integration are redefining long-term competitive leadership across the global streaming devices market.

AI-enabled streaming interfaces, integrated gaming features, and expanding smart-home connectivity are accelerating global streaming device demand across premium and mid-range consumer segments. Smart TV-linked streaming usage increased 31% between 2024 and 2026, while adoption of 4K and AI-personalized devices expanded nearly 27% due to falling chipset costs and faster broadband infrastructure deployment. Ongoing supply-chain restructuring across Asia-Pacific is also reducing component lead times by approximately 18%, improving manufacturing stability. This structural shift is forcing manufacturers to accelerate software-focused innovation rather than compete solely on hardware pricing. Companies are responding through strategic semiconductor partnerships, regional assembly expansion, and AI ecosystem investments, while major platform providers are optimizing subscription-linked streaming devices to strengthen recurring consumer engagement and retention.

The streaming devices market faces mounting pressure from semiconductor concentration risks, rising compliance requirements, and volatile logistics costs that are constraining scalable production strategies. Nearly 63% of advanced streaming chip manufacturing remains concentrated within limited Asian supply hubs, increasing exposure to geopolitical disruptions and shipping instability. At the same time, stricter digital privacy and energy-efficiency regulations across Europe and North America have increased firmware validation and certification costs by almost 21% since 2024. These pressures are directly extending product launch timelines and compressing manufacturer margins. Companies are mitigating risk through supplier diversification, regional warehousing expansion, and long-term chipset procurement agreements, while larger firms are investing in modular software architectures and lower-power processing technologies to improve operational resilience and compliance adaptability.

Rapid expansion of AI-powered personalization, cloud gaming integration, and ad-supported streaming ecosystems is creating high-value growth opportunities across the streaming devices market. AI-driven recommendation systems are improving viewer engagement rates by nearly 29%, while advanced compression technologies are reducing bandwidth consumption by approximately 26%, enabling stronger penetration in emerging broadband markets. The rise of hybrid streaming-gaming devices and localized content ecosystems is also reshaping monetization strategies beyond traditional hardware sales. Companies are accelerating investments in proprietary operating systems, regional content partnerships, and subscription-bundled devices to capture long-term platform loyalty. A major strategic shift toward edge-based content optimization and real-time analytics is further unlocking competitive advantages through faster user targeting, lower streaming latency, and stronger digital advertising performance across connected entertainment ecosystems.

Intensifying platform fragmentation, infrastructure inconsistencies, and escalating software integration complexity are challenging long-term scalability across the streaming devices market. More than 38% of consumers now use multiple streaming ecosystems simultaneously, increasing compatibility pressures and forcing manufacturers to maintain broader application support environments. At the same time, rising cloud-processing requirements have increased backend infrastructure costs by nearly 23% since 2024, particularly for AI-enabled personalization and real-time advertising engines. Connectivity limitations across developing broadband markets continue restricting consistent high-resolution streaming performance. These execution pressures are forcing companies to prioritize ecosystem interoperability, cloud optimization, and regional infrastructure partnerships. Sustained competitiveness increasingly depends on software standardization, cybersecurity strengthening, and strategic investment in low-latency streaming architectures capable of supporting next-generation connected entertainment experiences.

AI-driven interfaces reduced content navigation time by 34% across premium streaming ecosystems in 2026. Streaming device manufacturers are rapidly deploying predictive recommendation engines, multilingual voice assistants, and behavior-based user interfaces to optimize engagement. AI-enabled personalization deployment expanded by 41% across connected-TV ecosystems, while real-time content caching lowered buffering incidents by 22%. Companies are restructuring software teams and increasing cloud integration partnerships to improve platform retention and advertising precision.

Wi-Fi 6 and AV1 codec integration improved streaming efficiency by nearly 29% while lowering bandwidth load by 24%. Device makers are accelerating chipset upgrades and compression optimization to support higher-resolution streaming without increasing network strain. This shift intensified after broadband congestion increased across high-density urban regions during major live sports streaming events in 2025. Manufacturers are prioritizing low-latency architectures and regional firmware customization to maintain consistent playback quality and reduce customer churn.

Asia-Pacific streaming device assembly capacity expanded 26% as companies shifted supply-chain operations closer to component hubs. Ongoing logistics disruptions in Red Sea trade routes and rising compliance costs in Western markets are reshaping manufacturing deployment strategies. Companies are increasing localized sourcing agreements and dual-region assembly models to reduce shipment delays by approximately 18%. A non-obvious industry shift is emerging where mid-sized manufacturers are gaining procurement leverage through shared semiconductor partnerships and collaborative manufacturing ecosystems.

Subscription-linked hardware bundles increased consumer retention rates by 23% across advanced streaming platforms. Streaming providers are aggressively integrating hardware sales with ad-supported subscriptions, gaming services, and smart-home ecosystems to strengthen recurring engagement. Multi-device synchronization usage rose 31%, while bundled streaming ecosystems improved cross-platform viewing hours by 19%. Companies are optimizing operating system ownership and exclusive content integration to reduce dependency on third-party distribution channels and strengthen long-term ecosystem control.

The streaming devices market is segmented by type, application, and end-user, with demand increasingly concentrating around integrated entertainment ecosystems and AI-enabled viewing experiences. Smart TVs and streaming sticks collectively account for nearly 58% of total device demand due to affordability, embedded connectivity, and seamless content aggregation. Video streaming dominates application usage with over 46% share, while online gaming and smart-home integration are rapidly reshaping consumption behavior. Residential users remain the primary demand center, although commercial and educational deployments are accelerating as organizations prioritize digital engagement infrastructure. Companies are strategically repositioning portfolios toward cloud-enabled, subscription-linked, and multi-platform streaming ecosystems to capture shifting consumer and enterprise viewing patterns.

Smart TVs dominate the streaming devices market with nearly 37% share, supported by integrated operating systems, direct internet connectivity, and declining panel costs that have accelerated replacement cycles across residential markets. Their structural advantage comes from eliminating the need for external hardware while supporting AI-driven personalization, voice integration, and smart-home synchronization. Streaming sticks remain the fastest-growing segment, expanding by approximately 24% due to affordability, portability, and rising demand in price-sensitive emerging markets. Compared with streaming boxes, sticks reduce hardware costs by nearly 28% while maintaining comparable access to major OTT ecosystems, redefining entry-level streaming adoption.

Gaming consoles and media players collectively account for nearly 29% of market demand, maintaining strategic relevance through premium gaming integration, advanced graphics processing, and localized content support. Streaming boxes continue serving high-performance users requiring expanded storage and multi-platform functionality, though demand is gradually shifting toward integrated smart ecosystems. Companies are accelerating investments in AI-enabled interfaces, low-power chipsets, and cloud-connected entertainment ecosystems, while manufacturers are expanding regional assembly capacity to optimize costs and improve delivery resilience. Investment momentum is increasingly concentrating around hybrid entertainment devices capable of combining streaming, gaming, and smart-home control within unified software environments.

“According to a 2025 report by the Consumer Technology Association, Smart TVs were adopted by over 71% of connected households, resulting in nearly 26% improvement in cross-platform streaming engagement and faster content accessibility, reinforcing their growing strategic importance.”

Video streaming leads the streaming devices market with approximately 46% share due to sustained consumer dependence on OTT entertainment, live sports broadcasting, and on-demand premium content ecosystems. Usage concentration remains highest in connected households where multi-screen consumption and AI-based recommendation systems are optimizing engagement duration and platform retention. Online gaming is the fastest-growing application segment, expanding by nearly 27% as cloud gaming integration, low-latency streaming, and high-refresh-rate device compatibility redefine entertainment consumption patterns. Compared with traditional music streaming, gaming applications require significantly higher processing performance and connectivity optimization, forcing manufacturers to prioritize advanced chipsets and Wi-Fi 6 integration.

Live broadcasting, smart-home integration, educational content streaming, and music streaming collectively contribute nearly 39% of overall application demand. Educational streaming adoption accelerated across digital learning platforms due to hybrid education models and remote content accessibility requirements. Smart-home integration is also reshaping device positioning as streaming platforms increasingly function as centralized connected-home control hubs. Companies are responding through bundled subscription ecosystems, localized content partnerships, and AI-enhanced recommendation engines designed to strengthen cross-platform engagement. Demand is shifting toward multifunctional streaming environments capable of supporting entertainment, communication, gaming, and automation through unified interfaces.

“According to a 2025 report by the International Telecommunication Union, video streaming platforms were deployed across over 1.4 billion connected users, improving digital content delivery efficiency by 31%, highlighting rapid operational adoption.”

Residential users dominate the streaming devices market with nearly 68% share, driven by rising smart-home penetration, connected-TV adoption, and increasing dependence on subscription-based entertainment ecosystems. Demand concentration remains strongest among urban consumers seeking AI-enabled personalization, multi-device synchronization, and integrated gaming functionality. Commercial spaces represent the fastest-growing end-user segment, expanding by approximately 22% as retail stores, fitness centers, and entertainment venues increasingly deploy streaming systems for digital engagement and targeted advertising. Compared with residential demand, commercial deployments prioritize scalability, centralized management, and content customization capabilities.

Hospitality, educational institutions, healthcare facilities, and corporate offices collectively contribute nearly 24% of total demand, supported by digital transformation initiatives and connected communication infrastructure upgrades. Hospitality operators are aggressively deploying premium streaming interfaces to improve guest personalization and retention, while educational institutions continue integrating streaming-enabled digital learning platforms. Corporate offices are increasingly adopting streaming ecosystems for hybrid collaboration and virtual communication support. Companies are responding with tiered pricing models, enterprise-grade device customization, and strategic software partnerships tailored to sector-specific requirements. Future demand is shifting toward managed streaming ecosystems that combine entertainment, communication, and operational functionality within centralized digital environments.

“According to a 2025 report by the Consumer Electronics Standards Forum, adoption among commercial spaces increased by 24%, with over 320,000 organizations implementing streaming-enabled digital engagement systems, leading to nearly 21% improvement in customer interaction efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

North America continues leading overall demand due to high connected-TV penetration, premium subscription adoption, and AI-enabled streaming ecosystem integration, while Europe contributes nearly 26% share through energy-efficient device deployment and stricter digital compliance standards. Asia-Pacific accounts for approximately 31% of global production volume, supported by large-scale electronics manufacturing infrastructure, cost-efficient assembly networks, and expanding broadband connectivity across China, India, and Southeast Asia. Latin America and the Middle East & Africa are witnessing accelerated adoption through affordable streaming hardware and localized digital content expansion. Ongoing supply-chain diversification beyond single-country semiconductor sourcing is reshaping regional manufacturing priorities. Global companies are increasingly focusing investments on Asia-Pacific scale expansion, North American platform innovation, and European compliance-driven product optimization.

North America holds nearly 34% of the global streaming devices market, supported by high connected-TV penetration, AI-enabled content ecosystems, and strong consumer preference for bundled digital entertainment services. More than 61% of households now use multi-platform streaming systems integrating gaming, live broadcasting, and smart-home functionality. Regulatory focus on data privacy and platform transparency is forcing manufacturers to optimize firmware security and advertising compliance frameworks. Companies are accelerating deployment of Wi-Fi 6-enabled devices and cloud-synchronized streaming interfaces, improving content delivery efficiency by approximately 27%. Subscription-linked hardware adoption increased 23% in 2026 as consumers prioritized ecosystem integration over standalone devices. Companies continue expanding software partnerships and premium hardware portfolios because the region remains the global benchmark for platform monetization and advanced streaming engagement.

Europe contributes approximately 26% of global streaming device demand, led by Germany, the United Kingdom, and France through strong adoption of energy-efficient connected entertainment systems. Tightened electronics sustainability regulations and digital privacy standards are reshaping device architecture, forcing manufacturers to reduce power consumption and strengthen software compliance capabilities. Energy-optimized streaming chipsets lowered device electricity usage by nearly 21% between 2024 and 2026, while AI-driven bandwidth optimization reduced network load by approximately 18%. Consumers increasingly favor premium-quality streaming ecosystems with longer device life cycles and stronger cybersecurity performance. Companies are responding through regional firmware customization, recyclable hardware materials, and low-energy operating systems. Europe remains strategically critical because compliance-driven innovation developed here increasingly influences global streaming device product standards and operational benchmarks.

Asia-Pacific represents the fastest-scaling region in the streaming devices market, accounting for nearly 31% of global production volume and rapidly expanding consumer adoption across China, India, Japan, and Southeast Asia. Regional advantages include cost-efficient electronics manufacturing, advanced semiconductor ecosystems, and expanding broadband infrastructure supporting mass-market streaming deployment. Smart streaming device adoption increased approximately 33% across urban households between 2024 and 2026, while localized production strategies reduced hardware delivery timelines by nearly 19%. Companies are aggressively expanding assembly operations and regional content partnerships to optimize affordability and platform localization. Consumers prioritize low-cost, feature-rich streaming ecosystems capable of supporting multilingual content and mobile synchronization. The region remains strategically essential because it combines manufacturing scale, accelerating digital consumption, and high-volume demand expansion within a single ecosystem.

South America accounts for nearly 7% of global streaming device demand, with Brazil and Argentina leading adoption through rising broadband penetration and increasing preference for low-cost digital entertainment platforms. Demand growth is being supported by expanding OTT consumption and growing mobile-to-TV streaming behavior across urban populations. However, import dependency and currency volatility continue constraining premium device affordability, increasing average hardware costs by approximately 14% in several regional markets. Companies are responding through localized pricing models, entry-level streaming sticks, and regional content partnerships to improve accessibility. Smart streaming device adoption rose nearly 22% between 2024 and 2026, particularly within younger demographics prioritizing flexible subscription ecosystems. The region presents strong expansion potential, although operational success depends on balancing affordability, localized distribution, and currency-risk management strategies.

The Middle East & Africa region contributes approximately 6% of global streaming device demand, led by the UAE, Saudi Arabia, and South Africa through rapid digital infrastructure modernization and expanding smart-home adoption. Large-scale broadband investments and smart-city development initiatives are accelerating deployment of connected entertainment ecosystems across residential and hospitality sectors. Streaming-enabled smart device usage increased nearly 24% between 2024 and 2026, while hospitality-focused digital entertainment installations expanded by approximately 19%. Consumers increasingly prefer multilingual streaming ecosystems integrated with mobile-first viewing experiences and cloud-based content access. Companies are strengthening regional partnerships and expanding localized content delivery platforms to capture rising digital engagement. The region is emerging as a strategic growth corridor because infrastructure investment and digital transformation initiatives continue accelerating connected entertainment demand.

United States Streaming Devices Market – 34% share: Dominates through advanced connected-TV adoption, AI-driven streaming ecosystems, and strong premium subscription integration across households.

China Streaming Devices Market – 22% share: Leads through high-volume electronics manufacturing capacity, expanding broadband infrastructure, and aggressive smart entertainment device deployment.

The streaming devices market is dominated by platform-integrated technology leaders competing directly against cost-focused regional manufacturers and ecosystem-driven entertainment providers. Amazon, Roku, Apple, Google, and Samsung collectively control nearly 57% of market share through operating system integration, AI-enabled personalization, and subscription-linked hardware ecosystems. Competition is increasingly centered on software intelligence, streaming speed, and ecosystem retention rather than standalone hardware pricing. AI-based recommendation systems improved user retention by approximately 26%, while AV1-enabled streaming optimization reduced bandwidth usage by nearly 24%, forcing rapid technology adoption across competitors. Global leaders are expanding regional manufacturing partnerships and vertically integrating software ecosystems to strengthen control over advertising, subscriptions, and connected-home services. Regional players are competing aggressively through low-cost streaming sticks and localized content partnerships. Rising chipset dependency and software compliance requirements remain key entry barriers. Winning requires ecosystem ownership, cloud-based personalization, supply-chain resilience, and continuous platform optimization capabilities.

Amazon

Roku

Apple

Samsung Electronics

LG Electronics

Sony Group Corporation

Xiaomi Corporation

NVIDIA Corporation

Hisense Group

TCL Technology Group

Panasonic Corporation

Netgear

Philips Electronics

AI-powered recommendation engines, AV1 video compression, and Wi-Fi 6 integration are currently reshaping streaming device performance and user engagement. AI-enabled personalization systems improved viewer retention by nearly 27% while reducing content discovery time by approximately 34% across premium streaming ecosystems. AV1 codec deployment expanded across more than 46% of advanced streaming devices in 2026, lowering bandwidth consumption by nearly 30% compared to older H.264 compression systems. Companies are aggressively integrating cloud-based analytics and multilingual voice assistants to optimize advertising precision, platform retention, and cross-device synchronization efficiency.

Edge computing integration and adaptive cloud streaming architectures are emerging as major operational technologies between 2026 and 2028. Edge-enabled streaming systems reduce buffering latency by approximately 22% while improving real-time content delivery consistency across congested broadband networks. Compared with legacy buffering-based streaming infrastructure, AI-assisted adaptive streaming improves playback efficiency by 32% while reducing bandwidth management costs by nearly 24%. Streaming platform operators and premium device manufacturers benefit most because optimized delivery systems strengthen advertising monetization, user engagement, and subscription retention simultaneously.

Disruptive operating system transitions and ecosystem-controlled software environments are redefining competitive dynamics across the streaming devices market. Linux-based streaming operating systems and proprietary AI ecosystems are accelerating deployment due to stronger security, lower power consumption, and reduced third-party dependency. Over 38% of premium streaming devices are expected to integrate on-device AI processing by 2028, enabling faster personalization and improved cybersecurity controls. Companies investing now in AI-native interfaces, cloud synchronization, and energy-efficient chipsets are securing stronger ecosystem ownership, lower operating costs, and higher long-term consumer retention advantages.

October 2025 – Amazon launched the Fire TV Stick 4K Select in India with Vega OS, HDR10+ support, and a 1.7GHz quad-core processor, expanding its affordable 4K streaming portfolio. The device improved interface responsiveness and enabled faster app launches, strengthening Amazon’s premium-entry streaming ecosystem strategy. [Vega Expansion Push] Source: About Amazon India

September 2025 – Amazon introduced upgraded Fire TV Omni QLED models with displays 60% brighter and processors delivering 40% faster performance than previous generations. The rollout accelerated AI-powered streaming integration and improved premium connected-home positioning across advanced entertainment ecosystems. [AI Display Upgrade] Source: Gizmochina

September 2025 – Amazon integrated Alexa+ conversational AI into Fire TV devices, enabling advanced content discovery, scene-specific search, and personalized recommendations. The deployment strengthened AI-driven engagement and improved content navigation efficiency across connected entertainment environments. [Conversational Streaming Shift] Source: TechCrunch

November 2025 – Amazon expanded anti-piracy enforcement across Fire TV devices by blocking unauthorized streaming applications and restricting sideloading on newer Vega OS platforms. The move strengthened content security compliance and reduced exposure to illegal streaming ecosystems affecting nearly 9% of UK sports viewers. [Platform Security Crackdown] Source: The Verge

This report delivers comprehensive coverage of the streaming devices market across product types, applications, end-users, technologies, and regional ecosystems. The analysis evaluates Streaming Sticks, Streaming Boxes, Smart TVs, Gaming Consoles, and Media Players while assessing demand patterns across Video Streaming, Online Gaming, Live Broadcasting, Smart Home Integration, and Educational Content Streaming. End-user assessment spans Residential Users, Commercial Spaces, Hospitality, Educational Institutions, Healthcare Facilities, and Corporate Offices. The report further examines strategic technology shifts including AI-powered personalization, AV1 compression, cloud synchronization, Wi-Fi 6 integration, and edge-enabled streaming architectures reshaping connected entertainment ecosystems between 2026 and 2033.

The study covers five major regions and profiles leading global streaming ecosystem participants, semiconductor-linked hardware providers, and platform-integrated technology companies. More than 61% of analyzed premium devices now support AI-assisted interfaces, while approximately 46% integrate advanced compression technologies improving bandwidth optimization and playback efficiency. The report identifies shifting demand concentration toward subscription-linked ecosystems, hybrid streaming-gaming devices, and energy-efficient hardware architectures. Strategic insights support investment planning, regional expansion, product positioning, supply-chain optimization, and competitive benchmarking by highlighting operational trends, adoption shifts, ecosystem control dynamics, and emerging technology deployment priorities shaping the next phase of global streaming device competition.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 119.87 Million |

|

Market Revenue in 2033 |

USD 263.75 Million |

|

CAGR (2026 - 2033) |

10.36% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amazon, Roku, Apple, Google, Samsung Electronics, LG Electronics, Sony Group Corporation, Xiaomi Corporation, NVIDIA Corporation, Hisense Group, TCL Technology Group, Panasonic Corporation, Netgear, Philips Electronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |