Reports

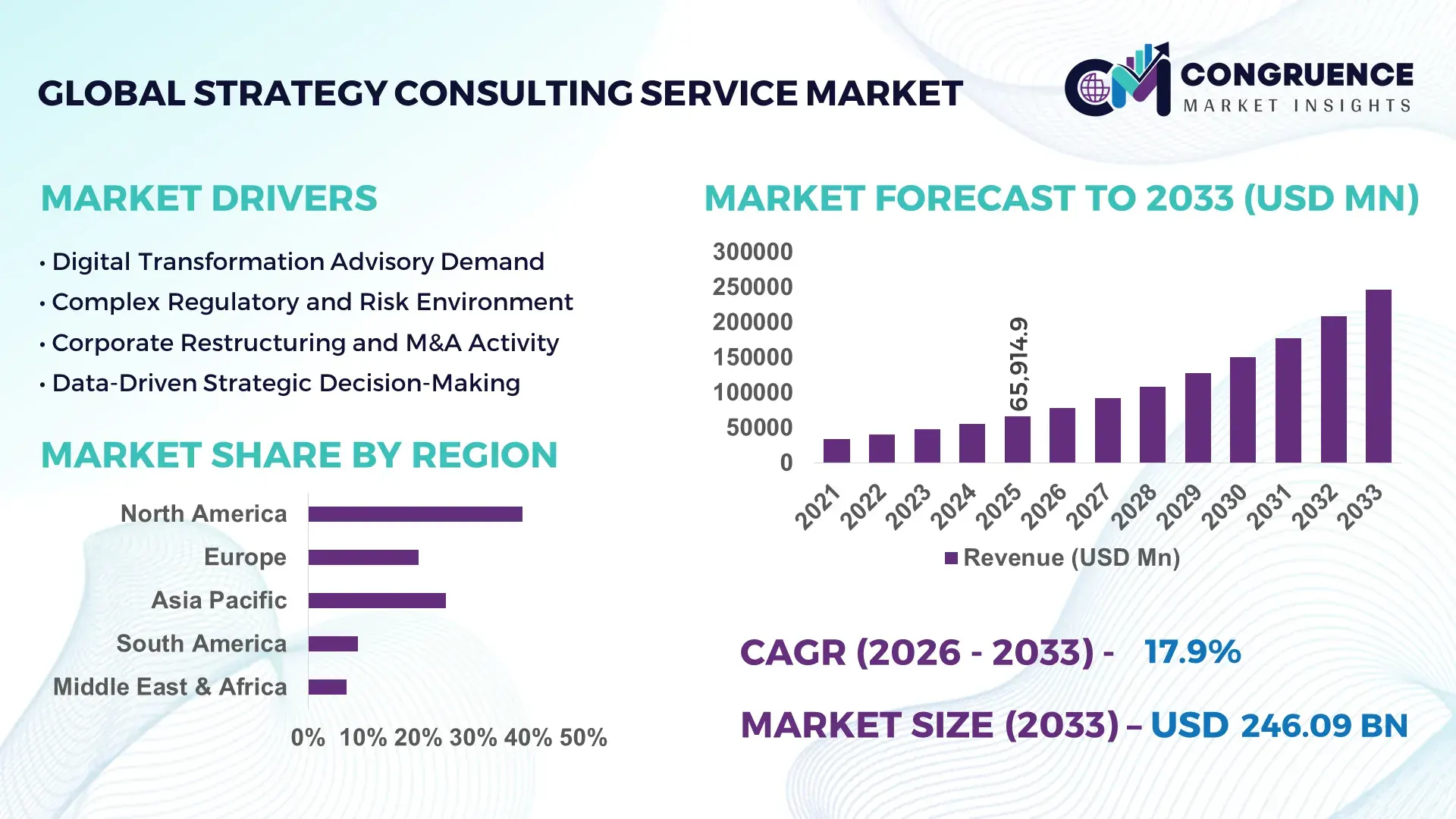

The Global Strategy Consulting Service Market was valued at USD 65914.88 Million in 2025 and is anticipated to reach a value of USD 246089.97 Million by 2033 expanding at a CAGR of 17.9% between 2026 and 2033. This expansion is driven by enterprise-wide digital transformation programs, portfolio rationalization initiatives, and rising demand for data-led strategic decision support across industries.

The United States dominates the Strategy Consulting Service marketplace in terms of capacity and scale of service delivery. Over 65% of the world’s top-tier consulting firms have their global headquarters or largest delivery centers in the U.S., employing more than 420,000 strategy and management consultants. Annual corporate spending on management and strategy advisory in the U.S. exceeds USD 120 billion, with strong demand from BFSI, healthcare, defense, and technology sectors. The country also leads in AI-enabled consulting platforms, with over 70% of large consulting firms integrating advanced analytics, scenario modeling, and generative AI tools into their strategy workflows. Adoption of cloud-based consulting solutions among Fortune 1000 firms in the U.S. has surpassed 80%, supporting high-volume, high-complexity strategic engagements.

• Market Size & Growth: USD 65.9 billion in 2025, projected to reach USD 246.1 billion by 2033 at a CAGR of 17.9%, driven by enterprise digitalization and complex transformation needs

• Top Growth Drivers: Digital transformation adoption 78%, operational efficiency programs 64%, data-driven decision-making uptake 71%

• Short-Term Forecast: By 2028, client organizations are expected to achieve an average 22% reduction in strategic planning cycle time through consulting-led automation and analytics

• Emerging Technologies: Generative AI for scenario planning, advanced analytics platforms, digital twin–based business modeling

• Regional Leaders: North America USD 96 billion by 2033 with strong AI adoption, Europe USD 72 billion with ESG-driven consulting demand, Asia-Pacific USD 61 billion with rapid enterprise modernization

• Consumer/End-User Trends: Large enterprises account for over 60% of demand, with rising mid-market adoption of modular and subscription-based consulting services

• Pilot or Case Example: A 2024 global manufacturing transformation program reduced operational costs by 18% and improved decision speed by 25% within 12 months

• Competitive Landscape: McKinsey ~14%, followed by BCG, Bain & Company, Accenture, Deloitte, and PwC

• Regulatory & ESG Impact: Sustainability reporting mandates and digital governance regulations are accelerating ESG and compliance-focused consulting adoption

• Investment & Funding Patterns: Over USD 18 billion invested globally in consulting technology platforms and digital delivery models since 2022

• Innovation & Future Outlook: Integration of AI-driven advisory, industry-specific digital playbooks, and outcome-based pricing models is shaping next-generation consulting services

The Strategy Consulting Service Market is primarily driven by BFSI, healthcare, manufacturing, energy, and technology sectors, which together contribute over 70% of total demand due to ongoing transformation, regulatory compliance, and competitive repositioning initiatives. Financial services alone account for approximately 25% of engagements, followed by manufacturing at 18% and healthcare at 14%. Innovations such as AI-powered strategic modeling tools, automated benchmarking platforms, and virtual collaboration environments are reshaping service delivery. Regulatory requirements related to data protection, ESG disclosures, and risk management are increasing demand for specialized advisory. Regionally, North America and Europe lead in high-value engagements, while Asia-Pacific shows the fastest growth due to rapid enterprise digitization. Future trends include outcome-based consulting, platform-enabled advisory, and deeper integration of technology and strategy services.

The Strategy Consulting Service Market plays a central role in enabling enterprises to navigate structural change, digital transformation, regulatory complexity, and competitive realignment. Organizations increasingly depend on external strategy advisors to integrate corporate strategy with data analytics, operational redesign, and technology roadmaps. For example, AI-driven scenario modeling delivers 35% improvement in strategic forecasting accuracy compared to spreadsheet-based planning models. North America dominates in volume, while Asia-Pacific leads in adoption with 68% of large enterprises actively using external strategy consulting for transformation and innovation initiatives.

Over the next two to three years, the market will be shaped by deeper integration of artificial intelligence, automation, and sector-specific digital frameworks into consulting workflows. By 2028, generative AI–enabled strategy platforms are expected to reduce strategic planning cycle time by 30% and improve decision-making speed by 25%. Firms are also committing to ESG performance improvements such as 40% carbon footprint reduction and 50% recyclable resource usage by 2030, supported by consulting-led sustainability and compliance programs.

In 2024, a global automotive manufacturer in Germany achieved a 20% improvement in supply chain resilience and a 15% reduction in inventory costs through AI-driven network optimization developed with external strategy consultants. Similar micro-scenarios are emerging across energy, healthcare, and financial services as organizations seek quantifiable business outcomes. Looking ahead, the Strategy Consulting Service Market will function as a pillar of organizational resilience, regulatory compliance, and sustainable growth, enabling enterprises to translate complexity into structured, data-driven, and future-ready strategic action.

Enterprise digital transformation is a primary driver of the Strategy Consulting Service Market as organizations modernize legacy systems, redesign operating models, and adopt data-driven decision frameworks. More than 70% of large enterprises are currently running multi-year transformation programs, and over 60% report reliance on external strategy advisors to define digital roadmaps and governance structures. Strategy consultants support platform migration, organizational redesign, and capability building, reducing execution risks and aligning investments with long-term business goals. Companies implementing structured digital strategies report up to 25% improvement in operational efficiency and 20% faster time-to-market for new products and services. This strong linkage between strategy formulation and transformation execution continues to sustain demand across sectors.

High consulting fees and growing internal strategy teams are moderating market expansion in some regions. Large organizations increasingly invest in internal analytics, corporate strategy units, and digital centers of excellence to reduce dependency on external advisors. Surveys indicate that nearly 35% of global enterprises plan to internalize parts of their strategy and transformation functions over the next three years. Additionally, budget constraints during economic slowdowns lead companies to postpone or scale down discretionary consulting engagements. This cost sensitivity, combined with procurement scrutiny and outcome-based pricing demands, creates pressure on traditional consulting models and limits short-term market growth in price-conscious industries.

AI-enabled consulting platforms and sector-focused strategy offerings present major growth opportunities. Automated diagnostics, predictive modeling, and digital twins enable consultants to deliver faster, more measurable outcomes, increasing client value. Industry-specific frameworks for healthcare compliance, energy transition, and financial risk management are driving differentiated demand. Mid-sized enterprises, which historically underutilized consulting services, are adopting modular and subscription-based advisory solutions, expanding the addressable market. The integration of technology, strategy, and ESG advisory also opens new engagement areas in sustainability transformation and regulatory compliance, positioning the market for structurally higher long-term demand.

The market faces challenges related to talent availability and regulatory complexity. Demand for consultants with combined expertise in strategy, data science, cybersecurity, and sustainability exceeds supply, increasing labor costs and limiting project scalability. At the same time, region-specific regulations on data privacy, AI governance, and cross-border service delivery complicate engagement models and raise compliance burdens. Firms must invest heavily in training, certification, and risk management to operate globally, which increases operating costs and reduces margin flexibility. These structural challenges require continuous adaptation of business models and delivery approaches within the Strategy Consulting Service Market.

• Rapid shift toward modular, subscription-based consulting models with 48% enterprise uptake

Enterprises are moving away from large, one-time strategy projects toward modular, on-demand consulting formats. Around 48% of large organizations now use subscription or retainer-based strategy services, compared to 29% three years ago. This model reduces engagement setup time by 35% and improves budget predictability by 27%. Modular strategy toolkits covering market entry, digital transformation, and ESG allow firms to access targeted expertise without full-scale projects, increasing utilization rates and expanding adoption among mid-sized enterprises by nearly 22%.

• Accelerated integration of AI and analytics into strategy workflows with 62% penetration

Approximately 62% of global consulting engagements now involve advanced analytics, predictive modeling, or AI-driven scenario planning. These tools improve forecast accuracy by 30% and reduce strategic analysis time by 40%. More than 70% of consulting firms have embedded data science teams into core strategy practices, while 58% of clients report improved strategic alignment between finance, operations, and technology through analytics-enabled advisory. This shift is transforming strategy consulting from advisory-led to insight-led engagement models.

• Rising demand for ESG and regulatory advisory with 45% increase in compliance-led projects

ESG and regulatory strategy projects have increased by 45% over the last two years as enterprises respond to sustainability mandates and digital governance requirements. Around 52% of corporations now integrate ESG targets into corporate strategy, and 38% use external consultants to design carbon reduction and reporting frameworks. These initiatives have enabled firms to achieve up to 25% improvement in regulatory readiness and 18% faster compliance implementation across regions with complex policy environments.

• Expansion of cross-border and near-shore delivery centers with 33% growth in offshore strategy teams

Global consulting firms have expanded near-shore and offshore strategy delivery capacity by 33% to address talent shortages and cost pressures. Over 40% of analytical and research-intensive strategy work is now performed outside client geographies, reducing delivery costs by 28% and improving turnaround times by 20%. This distributed model enhances scalability, supports continuous advisory, and allows firms to service a larger client base without proportional increases in onshore staffing.

The Strategy Consulting Service Market is segmented by type, application, and end-user, reflecting how enterprises consume advisory services across different strategic needs. By type, firms differentiate between corporate strategy, digital and transformation strategy, operational strategy, and sustainability and regulatory strategy, with digital-led offerings gaining prominence due to enterprise technology adoption. By application, demand is driven by business transformation, market entry and expansion, mergers and acquisitions, and risk and compliance planning, each addressing different stages of the corporate lifecycle. End-user segmentation highlights large enterprises as the primary consumers due to scale and complexity, while mid-sized firms are rapidly increasing adoption through modular and subscription-based consulting formats. This segmentation structure illustrates a shift from traditional episodic advisory toward continuous, technology-enabled, and outcome-oriented strategy services aligned with organizational performance and governance priorities.

Corporate and business strategy consulting currently accounts for about 38% of total adoption, making it the leading type due to its central role in portfolio management, competitive positioning, and long-term planning. Digital and transformation strategy follows with around 31%, driven by enterprise cloud migration, automation, and data modernization programs. However, sustainability and ESG strategy is the fastest-growing type, expanding at approximately 21% annually as firms integrate carbon reduction, regulatory reporting, and social impact into corporate agendas. Operational and cost optimization strategy, along with innovation and growth strategy, together contribute the remaining 31%, serving niche needs such as productivity improvement, product innovation, and organizational redesign.

Business transformation is the leading application, representing roughly 36% of engagements, as organizations restructure operations, digitize processes, and redesign operating models. Market entry and expansion accounts for around 24%, particularly in emerging economies and digital services. Mergers and acquisitions strategy represents 21%, driven by portfolio consolidation and cross-border deals. Risk, compliance, and governance strategy is the fastest-growing application, increasing at about 19% annually due to tightening data protection, financial, and sustainability regulations. The remaining 19% includes innovation strategy, workforce transformation, and turnaround advisory, which address specific organizational challenges.

Large enterprises dominate the market with approximately 58% share, reflecting their complex structures, global operations, and continuous transformation requirements. Multinational corporations and regulated industries such as banking, energy, and pharmaceuticals are particularly heavy users of strategy consulting. Mid-sized enterprises represent about 27% and are the fastest-growing end-user group, expanding at roughly 20% annually as modular consulting and digital delivery reduce cost and access barriers. Public sector and non-profit organizations contribute the remaining 15%, mainly for policy design, infrastructure planning, and governance reform. Industry adoption rates exceed 65% in financial services, 60% in technology, and 52% in manufacturing, highlighting sectoral concentration.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 21% between 2026 and 2033.

Europe followed with 32% share, while Asia-Pacific represented 21% and the rest of the world, including South America and Middle East & Africa, accounted for 8%. More than 68% of global Fortune 1000 enterprises currently engage external strategy consultants, with penetration exceeding 75% in financial services and 72% in healthcare. Over 60% of digital transformation programs and 58% of ESG integration initiatives globally are supported by strategy consulting services. Enterprise adoption exceeds 80% in developed economies and 55% in emerging markets, reflecting regional maturity gaps. More than 45% of consulting engagements now involve cross-border or near-shore delivery models, and over 62% integrate analytics or AI-driven insights, indicating strong convergence between regional digital readiness and consulting consumption patterns.

This region accounts for approximately 39% of the Strategy Consulting Service Market, driven by high enterprise density and complex regulatory environments. Financial services, healthcare, technology, and defense together generate more than 70% of demand. New digital governance and cybersecurity frameworks have increased advisory needs related to compliance and risk. Over 78% of large enterprises here integrate AI and analytics into strategy workflows, and 65% have ongoing multi-year transformation programs. A leading consulting firm in the region launched an AI-powered strategy platform in 2024, reducing client planning cycles by 28%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, with usage rates exceeding 80% in these sectors.

Europe represents around 32% of the global market, with Germany, the UK, and France accounting for nearly 60% of regional demand. Sustainability directives, data protection regulations, and digital market rules are major drivers of consulting engagement. More than 55% of European enterprises use external advisors for ESG and compliance strategy. Adoption of explainable AI and transparent analytics tools has reached 48%, supporting regulatory alignment. A major European consultancy expanded its sustainability strategy practice in 2024, supporting over 120 industrial firms in decarbonization planning. Regional behavior reflects strong demand for compliance-oriented and explainable strategy frameworks.

Asia-Pacific holds about 21% of the market and ranks as the fastest-expanding region by adoption volume. China, India, and Japan together contribute over 65% of regional demand. Rapid industrial automation, smart manufacturing, and e-commerce expansion are key drivers. More than 58% of enterprises are undertaking digital modernization initiatives, and 46% use external strategy advisors. Regional innovation hubs in Singapore, Bangalore, and Shenzhen are accelerating analytics and AI integration into strategy services. Consumer behavior shows growth driven by e-commerce platforms, fintech, and mobile-first enterprises.

South America accounts for approximately 5% of the global market, led by Brazil and Argentina. Infrastructure modernization, renewable energy projects, and digital media expansion drive demand. Government incentives for foreign investment and regional trade integration increase the need for market entry and regulatory strategy. About 42% of large enterprises in the region engage external consultants for transformation and expansion planning. Regional behavior shows demand tied to media localization, cross-border trade strategy, and infrastructure development.

This region contributes roughly 3% of the global market, led by the UAE, Saudi Arabia, and South Africa. National diversification programs, smart city initiatives, and digital government projects are major demand drivers. Over 50% of large organizations in the Gulf states use strategy consultants for transformation and public sector reform. Technology modernization and public-private partnerships are expanding advisory opportunities. Consumer behavior reflects strong demand in oil and gas diversification, construction, and government digitization.

• Strategy Consulting Service Market in the United States – 31% share – driven by high enterprise density, advanced digital transformation programs, and strong regulatory advisory demand

• Strategy Consulting Service Market in Germany – 14% share – supported by industrial modernization, sustainability mandates, and cross-border enterprise operations

The Strategy Consulting Service Market is moderately consolidated, with the top five firms collectively accounting for approximately 52% of total global engagements, while more than 4,500 active consulting firms operate worldwide across different tiers and specializations. Large global players dominate high-value, multi-country transformation programs, while mid-sized and boutique firms focus on niche domains such as digital transformation, ESG strategy, healthcare systems, and supply chain optimization. Over 68% of the top-tier firms have expanded their capabilities through technology partnerships, acquisitions of analytics startups, and development of proprietary AI-based strategy platforms.

More than 60% of competitive differentiation now depends on digital capabilities, including scenario simulation, advanced benchmarking, and automation of strategic diagnostics. Around 58% of consulting firms have launched or upgraded digital strategy platforms in the last two years, enabling up to 35% faster project delivery and 28% lower engagement costs. Strategic alliances between consulting firms and cloud, data, and AI providers have increased by 42%, improving scalability and access to advanced tools.

The market also shows strong activity in mergers and talent acquisitions, with over 120 consulting-related mergers and acquisitions completed globally between 2023 and 2025, primarily focused on sustainability advisory, cybersecurity strategy, and industry-specific expertise. Innovation trends include outcome-based pricing models adopted by 26% of large firms, subscription-based advisory models used by 31%, and near-shore strategy delivery centers expanded by 33%, intensifying competition on efficiency, specialization, and measurable business impact.

Advanced digital technologies are reshaping how strategy consulting services are designed, delivered, and consumed across industries. Artificial intelligence is now embedded in more than 62% of consulting engagements, enabling automated diagnostics, predictive scenario modeling, and real-time performance benchmarking. AI-driven strategy platforms improve forecast accuracy by approximately 30% and reduce analysis time by nearly 40%, allowing consultants and clients to move faster from insight to execution. Generative AI is increasingly used to synthesize large volumes of market, operational, and customer data, supporting faster strategic option evaluation and more consistent decision frameworks across large enterprises.

Cloud-based collaboration platforms have become standard, with over 70% of consulting firms using secure cloud environments to manage strategy projects, data exchange, and client interactions. These platforms enable distributed delivery models, with about 45% of analytical and research-intensive work now performed through near-shore and offshore centers. This shift reduces delivery costs by around 28% and improves turnaround times by 20%, while maintaining governance and data security through encryption, access control, and compliance monitoring tools.

Digital twin technology and simulation engines are gaining traction in manufacturing, energy, and logistics strategy projects. Approximately 35% of industrial strategy engagements now use digital twins to test operational scenarios, supply chain resilience, and investment outcomes before execution. In parallel, advanced analytics and visualization tools are helping executives interpret complex datasets, improving strategic alignment across finance, operations, and technology functions. Cybersecurity, privacy engineering, and regulatory technology are also becoming integral to strategy consulting, particularly in finance, healthcare, and public sector projects. More than 50% of strategy programs now include cyber and data governance components. These technologies collectively position the Strategy Consulting Service Market as a data-intensive, technology-enabled advisory ecosystem focused on measurable impact, risk mitigation, and long-term organizational resilience.

• In June 2025, Accenture acquired UK AI start-up Faculty in a deal valued at over $1 billion, marking its largest purchase of a private AI firm, with Faculty’s leadership joining Accenture’s global management committee to accelerate AI-enabled strategy consulting. (Financial Times)

• In 2025, McKinsey & Company expanded its workforce to 60,000, including 25,000 AI agents now integral to service delivery, reflecting a substantial shift toward AI-embedded consulting and improved operational efficiency across major strategic advisory functions. (Business Insider)

• In 2025, EY reported a 30% increase in AI-related consulting revenue, driven by demand for enterprise transformation and AI governance frameworks, backed by over 1,000 internal AI agents supporting operational and strategic engagements. (Business Insider)

• In May 2025, Boston Consulting Group (BCG) partnered with Pencil, an AI advertising platform, to jointly develop AI-driven content and strategy solutions for enterprise clients, underlining growing demand for integrated AI and marketing strategy consulting. (Consultancy)

The Strategy Consulting Service Market Report offers a comprehensive and structured overview of the industry’s breadth, illuminating segmentation by advisory type, application area, and end-user profile. It covers core service categories, including corporate strategy, digital and transformation strategy, sustainability and regulatory consulting, and operational optimization frameworks. The report examines adoption patterns across 10+ major global regions, detailing regional service preferences, technology readiness, and sectoral demand drivers in markets such as North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It includes analysis of strategic applications such as business transformation, market entry and expansion, mergers and acquisitions support, risk and compliance planning, and performance acceleration programs.

The scope extends into emerging niche domains like ESG strategy integration, AI-enabled strategic platforms, outcome-based consulting models, and modular advisory offerings tailored to mid-market enterprise segments. It assesses technological enablers reshaping delivery models — from advanced analytics, cloud collaboration, and digital twin scenario planning to predictive consumer insights and data-driven strategic diagnostics. The report also provides end-user insights across industries such as financial services, healthcare, energy, manufacturing, and technology, detailing consumption patterns, service maturity, and strategic priorities. Additionally, it incorporates competitive dynamics, innovation trends, and strategic responses of leading firms, while highlighting evolving client expectations and the interplay of regulatory, economic, and technological change in shaping future strategy consulting engagements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

McKinsey & Company, Boston Consulting Group, Bain & Company, Accenture, Deloitte, PwC, EY, KPMG, Roland Berger, Oliver Wyman, Capgemini Invent, L.E.K. Consulting, Strategy&, A.T. Kearney |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |