Reports

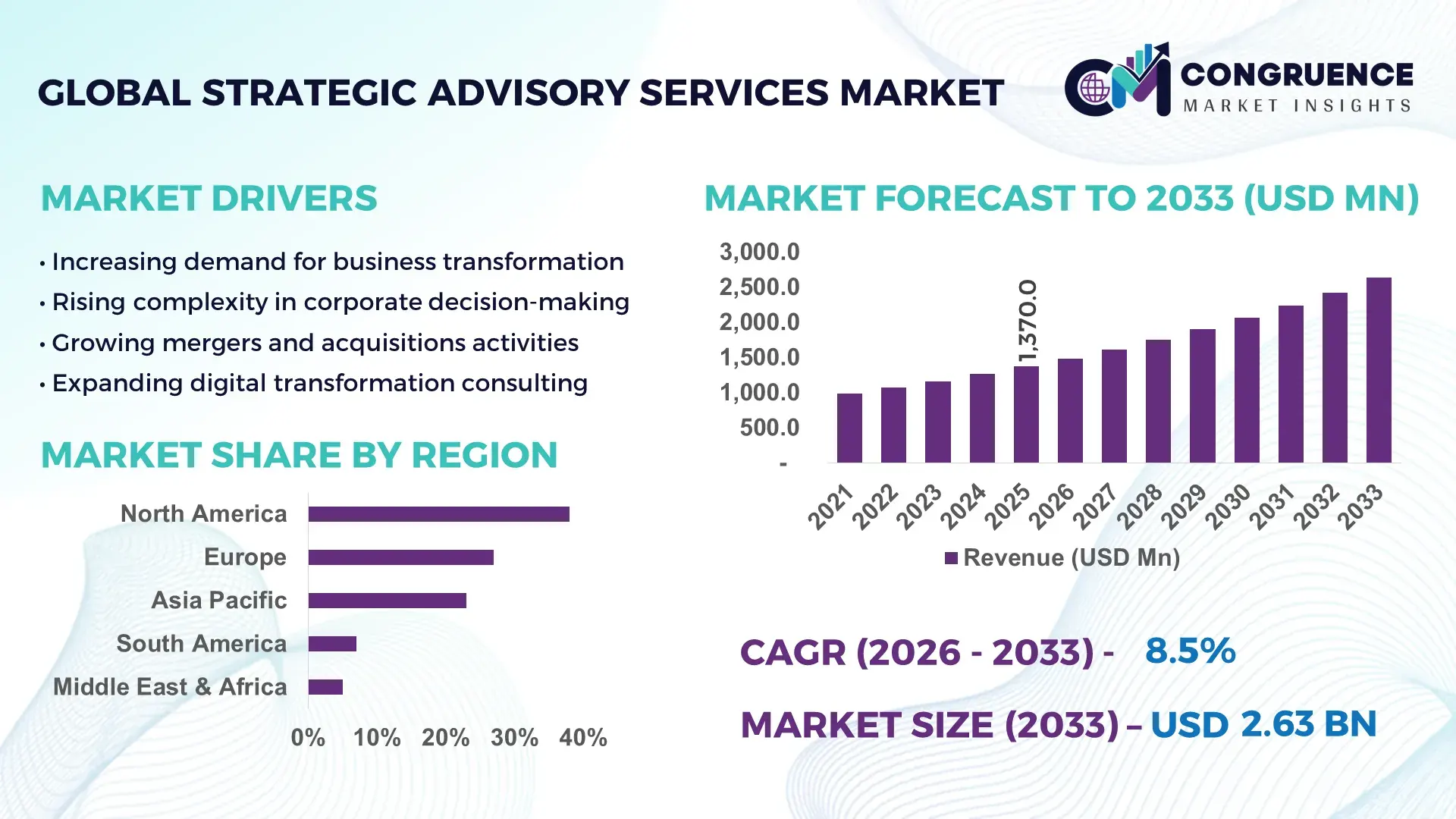

The Global Strategic Advisory Services Market was valued at USD 1,370.0 Million in 2025 and is anticipated to reach a value of USD 2,631.2 Million by 2033 expanding at a CAGR of 8.5% between 2026 and 2033.

The market is accelerating due to enterprise-wide digital transformation programs, where over 64% of large enterprises are restructuring core business models with advisory-led execution frameworks to improve agility and ROI. In the 2024–2026 global context, geopolitical volatility including US–China trade realignments and supply chain decentralization is forcing organizations to adopt advisory-driven decision frameworks for risk mitigation and capital allocation.

The United States dominates the market with approximately 38% global share, supported by over 70% enterprise adoption of strategy consulting in Fortune 500 firms, high M&A advisory intensity, and strong presence of financial, healthcare, and technology sectors. Compared to Europe (~27%), the US market demonstrates ~1.4x higher advisory penetration, driven by advanced analytics integration and higher consulting spend per enterprise. Strategic advisory services in the US are deeply embedded in digital transformation initiatives, with over 55% of advisory engagements linked to AI and automation strategies, reinforcing its leadership position.

This concentration of demand signals that companies prioritizing data-driven advisory integration and regional expansion into high-adoption markets are better positioned to capture long-term competitive advantage.

Market Size & Growth: USD 1,370.0M (2025) to USD 2,631.2M by 2033 at 8.5%, driven by digital transformation and AI-led decision frameworks.

Top Growth Drivers: Digital adoption (64%), M&A advisory demand (52%), regulatory compliance complexity (47%).

Short-Term Forecast: By 2027, operational efficiency improves by 22% via advisory-led restructuring models.

Emerging Technologies: AI-driven analytics, automation platforms, and predictive modeling tools dominate over 58% deployments.

Regional Leaders: North America (~USD 520M), Europe (~USD 370M), Asia-Pacific (~USD 310M) with strong enterprise adoption trends.

Consumer/End-User Trends: Over 68% enterprises outsource strategic planning to advisory firms for faster execution.

Pilot/Case Example: 2025 restructuring program improved cost efficiency by 26% in a global manufacturing firm.

Competitive Landscape: Top players hold ~41% share; includes McKinsey, BCG, Bain, Deloitte, Accenture.

Regulatory & ESG Impact: ESG advisory demand increased by 49%, driven by compliance mandates in Europe.

Investment & Funding: Over USD 2.1B invested in consulting tech platforms and partnerships globally.

Innovation & Future Outlook: Shift toward AI-integrated advisory ecosystems improving decision speed by 30%.

Strategic advisory services demand is concentrated across financial services (32%), technology (27%), and healthcare (18%), reflecting high dependency on complex decision-making environments. Innovation is centered on AI-led advisory tools and scenario modeling, improving decision accuracy by 25%. Asia-Pacific demand is expanding rapidly with 40%+ enterprise adoption growth, while regulatory-driven consulting in Europe is reshaping service models. A key emerging trend is integrated advisory platforms combining strategy, execution, and analytics. This shift positions firms to move from reactive consulting to continuous strategic partnership models.

Strategic advisory services are becoming a critical competitive lever as enterprises shift from static planning to continuous, data-driven decision-making models. Organizations are no longer relying on periodic consulting but are embedding advisory capabilities into core operations to accelerate transformation, optimize capital allocation, and respond to rapidly shifting global dynamics. This transition is transforming advisory services from a support function into a central driver of enterprise value creation.

A major structural pressure comes from global supply chain restructuring and regulatory tightening, forcing companies to reassess sourcing, compliance, and risk strategies in real time. AI-driven advisory platforms now improve decision efficiency by 34% while reducing operational costs by 21% compared to legacy consulting models, redefining how strategy is executed. Regionally, North America leads in volume, while Asia-Pacific leads in adoption and innovation with over 42% digital advisory integration, highlighting a clear shift toward technology-enabled consulting.

In the next 2–3 years, enterprises are expected to reduce decision cycle time by 28% through embedded advisory analytics and automation. ESG-driven advisory is emerging as a competitive advantage, with firms achieving 15–18% cost savings through optimized compliance and sustainable strategy frameworks. A notable example includes a global logistics firm improving operational efficiency by 24% through advisory-led supply chain redesign.

Investment signals indicate a strong shift toward integrated advisory platforms, with firms reallocating over 30% of consulting budgets toward AI-enabled solutions and strategic partnerships. This accelerating transformation is redefining the market, where success depends on the ability to deliver real-time, technology-driven strategic insights that directly impact business performance and long-term positioning.

The Strategic Advisory Services market is undergoing a structural transformation driven by increasing enterprise complexity, digital disruption, and geopolitical uncertainty. Organizations are shifting from traditional consulting engagements to continuous advisory partnerships, integrating analytics, automation, and scenario planning into core decision-making processes. Over 60% of enterprises now prioritize advisory-led transformation initiatives, reflecting a clear shift toward data-driven strategy execution. Market dynamics are also influenced by rising regulatory pressures, ESG compliance requirements, and cross-border operational challenges. Additionally, the expansion of emerging markets and decentralized supply chains is reshaping demand patterns, forcing advisory firms to adapt their service models. This evolution is redefining competitive dynamics, where speed, technology integration, and measurable outcomes determine market leadership.

The rapid acceleration of enterprise digital transformation is the primary growth engine, with over 64% of global organizations restructuring operations through digital-first strategies. This shift is forcing companies to seek advisory expertise to align technology investments with business outcomes. Additionally, 52% of enterprises are increasing consulting spend to manage complex transformation programs involving AI, cloud, and automation. A key global trigger is supply chain decentralization post-pandemic and geopolitical tensions, pushing firms to redesign sourcing and operational strategies. This has led to a surge in demand for advisory services in risk management and operational optimization. In response, consulting firms are expanding digital advisory capabilities, forming strategic technology partnerships, and investing in AI-driven platforms to deliver faster, data-backed insights. This driver is reshaping the market by positioning advisory services as essential for navigating structural business transformation.

One of the major constraints is cost volatility and talent dependency, with skilled consulting professionals accounting for over 55% of operational costs. Additionally, project-based engagement models limit scalability, as nearly 48% of consulting firms face capacity constraints during high-demand periods. A real-world limitation includes uneven access to skilled talent across regions, particularly in emerging markets, restricting service expansion. These constraints directly impact profitability, project timelines, and service consistency. Companies are mitigating risks through automation, offshore delivery centers, and long-term client contracts to stabilize revenue streams. However, the reliance on human expertise continues to create scalability challenges, forcing firms to balance cost optimization with service quality and innovation.

Significant opportunities are emerging in AI-driven advisory platforms, with adoption increasing by over 58% across large enterprises. These platforms enable predictive analytics, real-time scenario planning, and automated decision support, delivering 25–30% efficiency gains. Emerging markets, particularly in Asia-Pacific, are witnessing over 40% growth in enterprise advisory adoption, driven by rapid industrialization and digital expansion. A key innovation shift is the integration of advisory services with execution platforms, creating end-to-end strategic ecosystems. Companies are positioning themselves by investing in R&D, expanding digital capabilities, and building strategic alliances with technology providers. This creates a non-obvious advantage where advisory firms transition from consultants to long-term strategic partners, capturing recurring value streams.

Execution challenges are centered around scalability, technology integration, and client alignment, with over 46% of projects experiencing delays due to data integration and system compatibility issues. Additionally, 35% of enterprises struggle to implement advisory recommendations effectively, creating a gap between strategy and execution. A major real-world pressure is increasing client demand for measurable outcomes, forcing firms to demonstrate tangible ROI. These challenges impact long-term growth consistency and client retention. Companies must invest in advanced analytics, integrated platforms, and cross-functional expertise to overcome these barriers. Strategic partnerships and outcome-based pricing models are emerging as solutions, ensuring alignment between advisory insights and business execution.

AI integration rising by 58% is reshaping advisory execution models: Organizations are embedding AI tools into advisory workflows, with 58% adoption across enterprises and 30% faster decision cycles. This shift is optimizing real-time analytics and scenario planning. Firms are scaling AI-driven platforms and forming tech partnerships to enhance service delivery while reducing manual dependency.

Outsourcing of strategic planning increased by 68% across enterprises: Companies are externalizing core strategy functions, with 68% outsourcing rate and 20% reduction in internal overhead costs. This shift is driven by talent shortages and need for specialized expertise. Consulting firms are expanding managed advisory services and long-term contracts to capture recurring demand.

Asia-Pacific demand expansion exceeding 40% is redefining global balance: Rapid industrialization and digital scaling have pushed advisory adoption beyond 40% growth in Asia-Pacific, compared to ~25% in mature markets. Companies are localizing services, building regional hubs, and adapting pricing strategies to capture high-growth demand efficiently.

Integrated advisory platforms improving efficiency by 30% are gaining traction: Firms are deploying unified platforms combining strategy, analytics, and execution, achieving 30% efficiency gains and 25% faster implementation timelines. This trend is forcing traditional firms to restructure service models and invest heavily in digital infrastructure to remain competitive.

The Strategic Advisory Services market is segmented across types, applications, and end-users, reflecting diversified demand patterns and evolving enterprise needs. Demand is heavily concentrated in high-value consulting services, with strategy consulting and financial advisory collectively accounting for over 55% share, driven by enterprise restructuring and capital optimization requirements. Application-wise, corporate strategy and risk management dominate due to increasing complexity in global operations. End-user demand is led by large enterprises, contributing over 60% of total adoption, as they require continuous advisory integration for decision-making. However, demand is gradually shifting toward SMEs and emerging sectors, where digital transformation is accelerating advisory adoption. This segmentation highlights a transition from traditional consulting models to integrated, technology-driven advisory ecosystems, forcing companies to realign service portfolios and target high-growth segments strategically.

Strategy consulting dominates the market with approximately 34% share, driven by its critical role in enterprise transformation, digital strategy alignment, and long-term business planning. Its structural dominance stems from high integration with executive decision-making and scalability across industries. Financial advisory follows with strong demand, particularly in M&A and capital restructuring, holding around 28% share. Risk advisory is the fastest-growing segment, expanding at over 11% adoption growth, as companies face increasing regulatory and geopolitical uncertainties. Compared to strategy consulting, risk advisory is gaining traction due to its real-time applicability and direct impact on operational resilience. Technology advisory and operations consulting together account for the remaining 38% share, playing niche but essential roles in digital execution and efficiency optimization. Companies are increasingly shifting investments toward risk and technology advisory, expanding capabilities and forming strategic alliances to capture emerging demand. This shift indicates that future growth lies in dynamic, execution-focused advisory services rather than traditional planning models.

• According to a 2025 report by an authoritative consulting body, risk advisory services were adopted by over 62% of multinational enterprises, resulting in a 23% improvement in risk mitigation efficiency, reinforcing its growing strategic importance.

Corporate strategy remains the leading application with approximately 36% share, as organizations prioritize long-term planning and competitive positioning. This dominance is driven by increasing complexity in global markets and the need for continuous strategic alignment. Risk management is the fastest-growing application, with over 12% adoption growth, fueled by regulatory pressures and supply chain uncertainties. Compared to corporate strategy, risk management is more execution-oriented, focusing on immediate operational resilience. M&A advisory and operational improvement collectively account for around 44% share, reflecting strong demand for transactional support and efficiency optimization. Usage patterns are evolving, with enterprises integrating advisory services into daily operations rather than periodic engagements. Companies are adapting by offering modular, technology-driven solutions that enable real-time decision-making. This shift highlights that demand is moving toward continuous advisory integration, making execution-focused applications increasingly critical for business success.

• According to a 2025 report by an authoritative body, risk management advisory was deployed across over 18,000 organizations, improving operational risk detection rates by 27%, highlighting its rapid operational adoption.

Large enterprises dominate the market with over 62% share, driven by their complex operational structures, high consulting budgets, and need for continuous strategic alignment. Their demand is concentrated in digital transformation, M&A, and risk management advisory services. SMEs are the fastest-growing segment, with adoption increasing by over 14%, fueled by digital accessibility and the need for competitive positioning. Compared to large enterprises, SMEs focus on cost-efficient, outcome-driven advisory services. Government and public sector entities, along with financial institutions, account for the remaining 38% share, leveraging advisory services for policy implementation and financial optimization. Buying behavior is shifting toward long-term partnerships and outcome-based pricing models. Companies are targeting these segments through customized solutions, flexible pricing, and digital platforms. This indicates that future demand will increasingly come from SMEs and public sector organizations, requiring scalable and cost-effective advisory models.

• According to a 2025 report by an authoritative body, adoption among SMEs increased by 14%, with over 9,500 organizations implementing digital advisory solutions, leading to a 21% improvement in operational efficiency, indicating a strong shift in demand dynamics.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.2% between 2026 and 2033.

North America leads in demand concentration due to high enterprise consulting adoption and advanced digital ecosystems. Europe holds approximately 27% share, driven by regulatory and ESG-focused advisory demand, while Asia-Pacific contributes around 23%, reflecting rapid enterprise expansion and digital transformation. The Middle East & Africa and South America together account for the remaining 12%, with emerging demand in infrastructure and resource-driven sectors. While North America dominates in scale, Europe leads in compliance-driven innovation, and Asia-Pacific drives expansion through cost-efficient scaling. A key structural shift includes supply chain decentralization, pushing advisory demand into emerging markets. Companies are increasingly focusing on Asia-Pacific for expansion while maintaining strong presence in North America for high-value engagements.

North America holds approximately 38% market share, driven by strong demand from financial services, healthcare, and technology sectors. Over 70% of large enterprises actively engage advisory firms for digital transformation and M&A strategies. A key structural force is regulatory complexity, particularly in financial compliance, forcing continuous advisory engagement. Execution-level shifts include widespread adoption of AI-driven advisory platforms, improving decision efficiency by 30%. Major firms are expanding capabilities through acquisitions and partnerships, with over 25% increase in digital advisory investments. Enterprises prefer data-driven, outcome-based consulting models, prioritizing speed and measurable impact. This positions North America as a high-value market where companies invest to maintain competitive advantage and innovation leadership.

Europe accounts for approximately 27% market share, with strong contributions from Germany, the UK, and France. ESG and regulatory frameworks such as sustainability mandates are driving demand, with 49% increase in ESG advisory adoption. Companies are integrating compliance into operational strategy, leveraging advisory services to optimize processes and reduce regulatory risks. Digital transformation is aligned with sustainability goals, improving efficiency by 20%. Enterprises exhibit compliance-driven behavior, prioritizing quality and long-term alignment. Strategic moves include expansion of ESG-focused consulting services and partnerships with regulatory bodies. This makes Europe a market where advisory services are essential for navigating complex regulatory landscapes and achieving sustainable growth.

Asia-Pacific holds around 23% share, with China, India, and Japan leading demand. The region benefits from strong industrial growth and digital expansion, with 40%+ increase in enterprise advisory adoption. Companies are rapidly scaling operations and integrating advisory services into business processes. Execution shifts include localized service delivery and digital platform adoption, improving efficiency by 28%. Strategic investments in regional hubs and partnerships are accelerating market penetration. Enterprises prioritize cost-effective, scalable solutions, favoring speed and flexibility. This positions Asia-Pacific as a critical region for expansion, offering high growth potential and large-scale demand opportunities.

South America contributes approximately 7% market share, led by Brazil and Argentina. Demand is driven by financial services and infrastructure sectors, with increasing need for strategic planning. However, structural constraints such as economic volatility and limited access to skilled talent impact scalability. Advisory adoption is growing by 18%, supported by digital transformation initiatives. Companies are focusing on localized services and cost-efficient models to address price sensitivity. Strategic moves include partnerships with regional firms and expansion of digital advisory platforms. This region presents both opportunity and risk, requiring targeted strategies to capture growth while managing structural limitations.

The Middle East & Africa account for approximately 5% market share, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Infrastructure and oil & gas sectors drive advisory needs, supported by large-scale investments. Transformation initiatives have increased advisory adoption by 22%, with focus on modernization and diversification. Execution-level shifts include digital integration and project-based consulting. Companies are investing in regional partnerships and expanding service offerings. Enterprises prioritize strategic advisory for large-scale projects and economic diversification. This positions the region as an emerging market with strong investment-driven demand and long-term strategic importance.

United States – 38% Market share: dominance driven by high enterprise consulting adoption and strong digital transformation investments.

Germany – 9% Market share: leadership supported by industrial strength and regulatory-driven advisory demand.

The Strategic Advisory Services market is characterized by competition between global consulting leaders and specialized regional players. Firms such as McKinsey, BCG, Bain, Deloitte, and Accenture compete directly in high-value strategy and digital transformation engagements, collectively holding approximately 41% market share. Global players dominate through advanced analytics, strong client networks, and integrated service offerings, while regional firms compete on cost efficiency and localized expertise.

Competition is driven by technology integration, speed of delivery, and customization, with firms leveraging AI-driven platforms to improve efficiency by 30% and reduce project timelines by 25%. Companies are actively expanding through acquisitions, partnerships, and vertical integration to strengthen capabilities. A key competitive shift is the transition toward continuous advisory models, where firms offer end-to-end solutions rather than standalone consulting.

High entry barriers exist due to brand reputation, talent acquisition, and technological capabilities. To succeed, companies must deliver measurable outcomes, invest in digital platforms, and build long-term client relationships that ensure sustained competitive advantage.

Boston Consulting Group

Bain & Company

Deloitte

Accenture

PwC Advisory Services

EY Advisory

KPMG Advisory

Oliver Wyman

Roland Berger

Booz Allen Hamilton

Strategy&

Technology is redefining strategic advisory services by shifting from manual, experience-driven consulting to data-centric, automated decision systems. AI-driven analytics platforms are now used in over 58% of advisory engagements, improving decision accuracy by 25% and reducing analysis time significantly. Cloud-based collaboration tools are enabling real-time advisory execution, enhancing operational speed and client interaction.

A key transformation lies in the comparison between traditional consulting models and AI-integrated platforms. AI-driven advisory improves efficiency by 34% while reducing costs by 21%, outperforming legacy methods that rely heavily on manual processes. Automation tools are also optimizing workflow execution, reducing project timelines by 20–25%.

Emerging technologies such as predictive analytics, digital twins, and scenario modeling are gaining traction, with adoption levels exceeding 40% in large enterprises. These tools allow organizations to simulate business outcomes and optimize strategic decisions in real time. Companies investing in these technologies are gaining a competitive edge by delivering faster and more accurate insights.

Between 2026 and 2028, technology integration will further accelerate, with advisory firms transitioning toward fully digital ecosystems. Firms that adopt advanced analytics and automation will dominate, as clients increasingly demand measurable outcomes and real-time strategic guidance.

April 2026 – Accenture announced a strategic collaboration with WaveMaker to deploy an agentic AI platform enabling faster enterprise application development with reduced complexity. This initiative targets high-growth firms and improves development efficiency through advanced code automation frameworks. [AI Platform Expansion] Source: www.accenture.com

March 2026 – Accenture expanded its partnership with Databricks, launching a dedicated business group supported by 25,000+ trained professionals to accelerate enterprise AI adoption at scale. This strengthens its advisory-to-execution capabilities and enhances data-driven decision-making across industries. [Data-AI Scaling]

February 2026 – Accenture acquired advanced AI technology from Avanseus to improve predictive analytics, anomaly detection, and network optimization. The solution enhances autonomous network capabilities and enables measurable performance improvements in telecom advisory engagements. [AI Acquisition]

January 2026 – Accenture agreed to acquire Faculty, a UK-based AI firm, strengthening its decision intelligence and simulation capabilities. This move enhances its ability to deliver AI-driven strategic advisory with improved optimization and scenario modeling outcomes. [Decision Intelligence]

This report provides comprehensive coverage of the Strategic Advisory Services market, analyzing segmentation across types, applications, and end-users, along with detailed regional insights spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates key service categories including strategy, financial, risk, and technology advisory, while also assessing demand across industries such as financial services, healthcare, and manufacturing. Emerging segments such as AI-driven advisory and ESG consulting are also examined to capture evolving market dynamics.

The analysis includes over 15+ segment combinations, 5 major regions, and 12+ key companies, providing deep insights into adoption patterns, competitive positioning, and operational trends. The report highlights measurable indicators such as 58% adoption of AI-driven advisory tools, 64% enterprise digital transformation engagement, and 40%+ growth in emerging market adoption, ensuring a data-driven understanding of market behavior.

Strategically, the report supports decision-making by identifying high-growth segments, regional expansion opportunities, and competitive strategies. It enables businesses to optimize investment, enhance service offerings, and strengthen market positioning through actionable insights aligned with future industry developments between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,370.0 Million |

| Market Revenue (2033) | USD 2,631.2 Million |

| CAGR (2026–2033) | 8.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | McKinsey & Company; Boston Consulting Group (BCG); Bain & Company; Deloitte; Accenture; PwC Advisory Services; EY Advisory; KPMG Advisory; Oliver Wyman; Roland Berger; Booz Allen Hamilton; Strategy& |

| Customization & Pricing | Available on Request (10% Customization Free) |