Reports

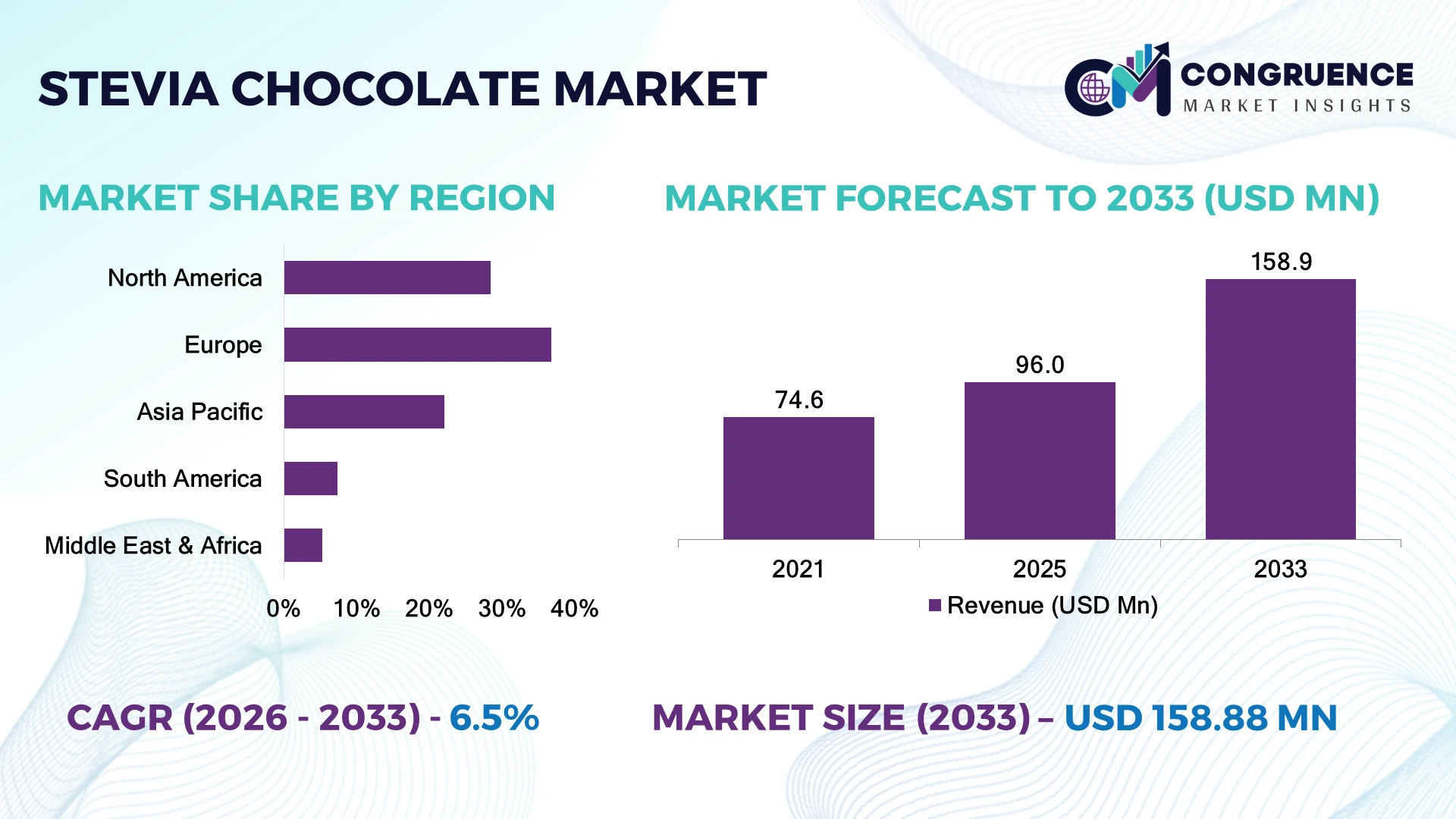

The Global Stevia Chocolate Market was valued at USD 96 Million in 2025 and is anticipated to reach a value of USD 158.9 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. Rising reformulation of premium chocolate with natural stevia sweeteners, expanding sugar-reduction regulations, and clean-label product innovation across confectionery portfolios are accelerating market expansion.

Germany accounts for nearly 24% of the European stevia chocolate production base, supported by over 40 major premium confectionery manufacturing facilities and strong investments in reduced-sugar product development. Compared with France, Germany records approximately 18% higher adoption of naturally sweetened premium chocolate across organized retail channels. The European Union's sugar-reduction initiatives continue encouraging reformulation, while advanced processing technologies improve flavor consistency and product acceptance.

Strategically, manufacturers investing in premium clean-label formulations, regional sourcing, and advanced sweetener technologies are strengthening long-term competitive positioning.

Market Size & Growth: USD 96 Million in 2025, projected to reach USD 158.9 Million by 2033 at a CAGR of 6.5%, supported by rapid clean-label confectionery innovation and natural sweetener integration.

Top Growth Drivers: Sugar-reduction product launches (+32%), premium healthy snack adoption (+27%), and natural ingredient sourcing (+24%) continue driving expansion.

Short-Term Forecast: By 2028, advanced formulation technologies are expected to improve flavor consistency by approximately 18% while reducing production waste by 10%.

Emerging Technologies: AI-assisted recipe optimization, precision cocoa processing, and advanced stevia purification technologies improve taste performance and manufacturing efficiency.

Regional Leaders: Europe (USD 56 Million), North America (USD 44 Million), and Asia-Pacific (USD 36 Million) lead through premium retail expansion, health-focused innovation, and modern confectionery manufacturing.

Consumer/End-User Trends: Nearly 46% of health-conscious confectionery buyers actively prefer chocolates containing natural sugar alternatives.

Pilot/Case Example: In 2024, premium confectionery manufacturers achieved approximately 20% better taste acceptance after optimizing stevia-blend formulations.

Competitive Landscape: Barry Callebaut holds nearly 14% market share alongside Lindt & Sprüngli, Chocoladefabriken Lindt, Lily's, and Cavalier.

Regulatory & ESG Impact: Sugar-reduction initiatives contributed to nearly 21% higher adoption of naturally sweetened chocolate while supporting cleaner ingredient sourcing.

Investment & Funding: More than USD 180 Million has been invested globally in healthier confectionery expansion, manufacturing upgrades, and strategic ingredient partnerships.

Innovation & Future Outlook: Advanced botanical sweetener blends, premium functional chocolate, and sustainable cocoa sourcing continue reshaping competitive differentiation.

Stevia Chocolate Market is gaining momentum across premium retail, functional nutrition, and healthier gifting categories as manufacturers improve sweetness balance without compromising cocoa flavor. Advanced stevia purification technologies have increased consumer taste acceptance by nearly 20%, while diversified botanical ingredient sourcing strengthens supply resilience. Growing clean-label regulations and premium product differentiation continue shaping next-generation confectionery strategies.

The Stevia Chocolate Market has become strategically important as global confectionery companies intensify competition around healthier premium products and clean-label positioning. Regulatory pressure to reduce added sugar, combined with consumer preference for natural ingredients, is encouraging manufacturers to redesign portfolios using plant-based sweeteners. Supply-chain diversification for cocoa and stevia ingredients is also strengthening operational resilience across major production regions.

Modern stevia purification technologies deliver approximately 15% better flavor consistency than earlier extraction methods while reducing formulation adjustments during manufacturing. European producers emphasize premium innovation and regulatory compliance, whereas Asia-Pacific manufacturers focus on high-volume production efficiency and expanding domestic consumption. Over the next two to three years, wider adoption of precision formulation systems is expected to improve production efficiency by nearly 12% across advanced manufacturing facilities.

Leading chocolate manufacturers are expanding partnerships with natural sweetener suppliers and investing in specialized processing capabilities to accelerate premium product launches. Several producers have introduced dedicated reduced-sugar product lines supported by sustainable cocoa sourcing and recyclable packaging initiatives. Companies prioritizing ingredient innovation, supply-chain flexibility, and premium product differentiation are expected to secure stronger competitive positioning and long-term operational advantages.

Sugar-reduction mandates and clean-label product reformulation are fundamentally reshaping premium chocolate manufacturing. More than 62% of newly launched reduced-sugar chocolate products now incorporate plant-based sweeteners, while consumer preference for natural ingredients has increased by approximately 28% across premium confectionery categories. The European Union's continued sugar-reduction initiatives are encouraging manufacturers to replace artificial sweeteners with stevia-derived alternatives, improving portfolio competitiveness. This regulatory shift has accelerated investments in advanced stevia purification technologies that significantly enhance flavor balance and reduce bitterness. Companies including premium chocolate producers are expanding partnerships with stevia ingredient suppliers, strengthening localized sourcing networks, and investing in proprietary formulation capabilities. A key strategic advantage lies in combining premium cocoa with natural sweeteners, allowing manufacturers to capture health-conscious consumers without sacrificing product differentiation.

Stevia chocolate manufacturers continue facing structural constraints from raw material price fluctuations and formulation complexity. Premium-grade stevia extract prices have experienced fluctuations exceeding 18% during seasonal supply cycles, while formulation costs remain approximately 15% higher than conventional sugar-based chocolate production. China continues supplying a significant share of refined stevia ingredients, exposing manufacturers to procurement disruptions caused by agricultural variability and logistics constraints. Maintaining consistent sweetness profiles across premium chocolate recipes requires additional processing and quality validation, increasing production timelines and operational costs. Companies are responding through diversified sourcing agreements, localized ingredient procurement, and long-term supply contracts with certified stevia producers. Operational resilience increasingly depends on securing stable ingredient availability alongside continuous flavor optimization to protect premium brand positioning.

The convergence of functional nutrition and premium confectionery presents a high-value opportunity for stevia chocolate manufacturers. Nearly 41% of wellness-focused consumers actively seek chocolates containing natural ingredients with reduced sugar, while functional confectionery product launches have expanded by approximately 26% over recent years. Japan is strengthening innovation through precision food formulation and botanical ingredient development, creating opportunities for enhanced sensory performance and customized nutrition products. AI-assisted formulation platforms and precision ingredient blending enable faster product optimization while reducing development cycles by nearly 20%. Manufacturers are expanding R&D partnerships, investing in premium functional product portfolios, and collaborating with specialty ingredient developers. A significant strategic opportunity exists in combining clean-label positioning with personalized nutrition, enabling higher-value differentiation beyond conventional sugar-free chocolate offerings.

Maintaining identical sensory quality across geographically distributed production facilities remains a significant execution challenge. Taste perception varies across consumer markets, requiring formulation adjustments that increase validation requirements by approximately 22%, while premium quality assurance protocols extend product development timelines by nearly 16%. Germany and Switzerland maintain advanced confectionery manufacturing standards, making global consistency increasingly difficult for multinational producers expanding into emerging production locations. Differences in cocoa bean characteristics, stevia extract purity, and processing parameters further complicate standardized manufacturing. Companies must strengthen digital quality management systems, invest in advanced analytical testing technologies, and expand technical collaboration with ingredient suppliers to achieve consistent product performance. Long-term competitiveness depends on scalable manufacturing excellence supported by continuous process standardization and specialized formulation expertise.

Premium Clean-Label Product Expansion Premium chocolate manufacturers are rapidly expanding naturally sweetened product portfolios, with reduced-sugar chocolate launches increasing by approximately 31% during the past two years. More than 48% of premium confectionery innovation now focuses on botanical sweeteners as sugar-reduction regulations tighten in Germany and the United Kingdom. Companies are restructuring product development teams, accelerating clean-label certifications, and scaling premium retail distribution to strengthen brand differentiation and improve shelf competitiveness.

Advanced Sweetener Blending Technologies Multi-sweetener formulation strategies combining stevia with erythritol and soluble fibers have improved consumer taste acceptance by nearly 22% while reducing bitterness by around 18%. Manufacturers are integrating precision formulation software and automated ingredient dosing systems to standardize flavor profiles across production facilities. This operational shift shortens formulation cycles, reduces product rework, and enables faster commercialization of premium chocolate variants.

Localized Ingredient Supply Networks Chocolate producers are reducing dependence on single-country ingredient sourcing by expanding regional procurement partnerships and certified agricultural programs. Nearly 36% of manufacturers have diversified stevia procurement contracts, while localized cocoa sourcing initiatives have lowered logistics-related procurement delays by approximately 15%. These changes improve inventory resilience and strengthen production continuity during supply-chain disruptions and transportation volatility.

Functional Premium Chocolate Positioning Functional confectionery products featuring botanical extracts, added fiber, and natural sweeteners have expanded by approximately 27% across organized retail channels. More than 40% of new premium chocolate launches now emphasize wellness positioning alongside indulgence. Companies are investing in specialized formulation capabilities, strategic ingredient partnerships, and premium packaging to strengthen consumer engagement while responding to evolving nutritional labeling requirements.

Dark stevia chocolate dominates the market with an estimated 46% share, supported by its naturally higher cocoa content, stronger compatibility with stevia sweetening systems, and broad acceptance among health-conscious consumers. Manufacturers continue prioritizing dark chocolate because its robust cocoa profile effectively balances the subtle aftertaste associated with natural sweeteners. Milk chocolate remains the largest mainstream category, while white chocolate occupies a specialized premium niche. Companies continue introducing premium cocoa blends and improved sweetener formulations to strengthen taste consistency and product quality. Sugar-free filled and flavored stevia chocolate represents the fastest-growing product category as manufacturers diversify premium offerings with nuts, berries, protein inclusions, and functional ingredients. Approximately 34% of premium product launches now include value-added fillings, while nearly 29% feature clean-label botanical ingredients. Investment priorities increasingly emphasize premium differentiation, automated manufacturing, and customized flavor innovation, enabling companies to capture both wellness-focused and indulgence-oriented consumer segments.

Retail consumption accounts for approximately 63% of total demand as supermarkets, specialty stores, and online premium food platforms continue expanding healthier confectionery assortments. Growing consumer preference for reduced-sugar gifting products and premium daily indulgence has strengthened shelf penetration across developed consumer markets. Companies continue expanding private-label collaborations, premium packaging formats, and omnichannel distribution strategies to improve product accessibility and brand visibility. Online retail is the fastest-growing application, supported by digital commerce expansion and personalized nutrition purchasing behavior. Direct-to-consumer premium chocolate sales have increased by nearly 26%, while subscription-based healthy snack platforms have expanded by approximately 18%. Foodservice and hospitality applications continue recovering through premium dessert offerings, whereas corporate gifting increasingly incorporates healthier confectionery selections. Manufacturers are strengthening digital marketing, fulfillment capabilities, and customized product portfolios to capture evolving purchasing preferences.

Individual health-conscious consumers remain the dominant end-user group, representing approximately 58% of overall market demand through consistent purchases of premium reduced-sugar chocolate products. Growing awareness of ingredient transparency, wellness lifestyles, and natural sweeteners continues driving purchasing decisions. Manufacturers increasingly develop premium product lines with clean-label positioning, recyclable packaging, and differentiated cocoa origins to strengthen customer loyalty and repeat purchases. Corporate gifting and hospitality represent the fastest-growing end-user segment as organizations increasingly adopt healthier premium confectionery for seasonal gifting and customer engagement. Premium business gifting demand has increased by nearly 21%, while wellness-focused hospitality offerings have expanded by approximately 17%. Specialty retailers, luxury hotels, and premium cafés continue incorporating naturally sweetened chocolate into curated product selections. Companies are responding through customized packaging, exclusive retail partnerships, and premium branding strategies that strengthen long-term customer relationships and market positioning.

Europe accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

North America represents approximately 28.4% of the global Stevia Chocolate Market, supported by strong consumer preference for reduced-sugar confectionery, advanced chocolate manufacturing capabilities, and broad retail availability. Premium manufacturers continue expanding naturally sweetened product portfolios while improving taste through advanced sweetener formulations and automated production systems. Nearly 54% of premium healthier chocolate launches in the region now feature plant-derived sweeteners, reflecting sustained clean-label adoption. Digital retail continues strengthening market penetration, with direct-to-consumer premium confectionery sales expanding across specialized wellness platforms. Manufacturers are increasing investments in ingredient traceability, sustainable cocoa sourcing, and high-efficiency packaging operations to improve product differentiation and supply-chain resilience.

United States Market Outlook: The United States remains the largest contributor within North America due to its extensive premium confectionery industry, advanced food technology capabilities, and strong consumer demand for healthier indulgence products. More than 60% of regional premium reduced-sugar chocolate launches originate from U.S.-based manufacturers. Companies continue investing in automated production lines, clean-label product development, and strategic partnerships with natural sweetener suppliers, strengthening domestic manufacturing efficiency and accelerating premium product commercialization.

Europe leads the global market with approximately 36.8% share, supported by mature premium chocolate manufacturing, stringent sugar-reduction initiatives, and strong consumer preference for natural ingredients. Leading confectionery companies continue replacing conventional sweeteners with botanical alternatives while investing in flavor optimization and sustainable cocoa procurement. More than 45% of premium healthier chocolate innovations are concentrated within Western European manufacturing hubs. Product reformulation, recyclable packaging adoption, and advanced processing technologies continue improving production consistency while supporting premium brand positioning. Strategic investments in ingredient certification and localized sourcing networks further enhance operational resilience.

Germany Market Outlook: Germany serves as Europe's operational center for premium stevia chocolate manufacturing through its advanced confectionery infrastructure, sophisticated food processing technologies, and strong export capabilities. Nearly one-quarter of Europe's premium naturally sweetened chocolate production is concentrated in Germany. Manufacturers continue expanding formulation research, automated manufacturing facilities, and sustainable ingredient partnerships to strengthen international competitiveness while maintaining consistent premium product quality.

Asia-Pacific accounts for approximately 22.1% of the global market and represents the fastest-expanding production and consumption hub for naturally sweetened chocolate. Rising urbanization, premium food retail expansion, and increasing health awareness continue supporting demand for reduced-sugar confectionery. Nearly 38% of new confectionery manufacturing investments within the region now include healthier product development capabilities. Manufacturers are deploying automated processing technologies, strengthening regional ingredient sourcing, and expanding premium distribution networks. Modern retail channels and digital commerce continue accelerating product accessibility while improving operational efficiency across major consumer markets.

Japan Market Outlook: Japan leads premium innovation within Asia-Pacific through advanced food science, precision formulation expertise, and sophisticated consumer demand for healthier confectionery. More than 35% of premium reduced-sugar chocolate launches in the country incorporate advanced botanical sweetener blends. Domestic manufacturers continue investing in sensory optimization, automated quality control, and premium packaging technologies to maintain product differentiation while supporting expanding export opportunities across neighboring markets.

South America represents approximately 7.4% of the global market, benefiting from abundant cocoa production, increasing stevia cultivation, and expanding premium confectionery manufacturing. Consumer demand for healthier chocolate alternatives continues encouraging product reformulation using naturally derived sweeteners. Approximately 30% of premium confectionery manufacturers have expanded clean-label product portfolios over the past two years. Although logistics infrastructure and processing capacity remain uneven across several markets, manufacturers continue improving regional distribution capabilities through localized production investments and strategic supply partnerships. These operational improvements are strengthening manufacturing flexibility and supporting higher-value premium chocolate exports.

Brazil Market Outlook: Brazil remains the region's most influential market through its extensive cocoa processing industry, expanding food manufacturing base, and increasing consumer preference for wellness-oriented confectionery. More than 40% of South America's premium chocolate production capacity is located in Brazil. Companies continue modernizing manufacturing facilities, strengthening domestic retail partnerships, and introducing naturally sweetened premium products to improve both export competitiveness and domestic market penetration.

The Middle East & Africa contributes approximately 5.3% of the global market as premium retail development and healthier food consumption gradually reshape confectionery purchasing patterns. Modern supermarket expansion, premium specialty food stores, and organized retail channels continue improving availability of naturally sweetened chocolate products. Nearly 24% of premium imported confectionery products now feature reduced-sugar positioning across major urban retail markets. Companies are strengthening regional distribution partnerships, investing in premium retail channels, and improving cold-chain logistics to enhance product quality and inventory management. Continued modernization of food retail infrastructure supports broader consumer access to premium healthier confectionery.

United Arab Emirates Market Outlook: The United Arab Emirates functions as the region's leading premium confectionery distribution and retail hub through advanced logistics infrastructure, international food trade connectivity, and high-value consumer spending. Premium healthier chocolate offerings have expanded by approximately 28% across organized retail and specialty food outlets. Importers and premium food companies continue investing in diversified supplier networks, digital retail platforms, and premium merchandising strategies to strengthen market penetration and support sustained product availability.

The Stevia Chocolate Market is led by global premium chocolate manufacturers including Barry Callebaut, Lindt & Sprüngli, Cavalier, Chocoladefabriken Peters, and The Hershey Company, competing against regional health-focused confectionery specialists and private-label producers. The top five participants collectively account for approximately 54% of the market, reflecting moderate consolidation with strong brand influence. Competition centers on formulation technology, taste optimization, premium cocoa sourcing, and clean-label positioning rather than price alone. Manufacturers using advanced stevia-blend technologies achieve nearly 18% better consumer taste acceptance, while automated production reduces formulation time by approximately 15%. Companies are expanding through strategic ingredient partnerships, premium product launches, localized manufacturing, and vertically integrated cocoa supply chains. The competitive landscape is shifting toward proprietary sweetener systems and sustainable sourcing as regulatory pressure on sugar intensifies. High formulation expertise, premium brand credibility, and reliable ingredient procurement remain key entry barriers. Sustainable innovation, superior sensory performance, and resilient supply chains define long-term competitive success.

Lindt & Sprüngli AG

The Hershey Company

Cavalier NV

Chocoladefabriken Peters GmbH

Lily's Sweets LLC

Chocolove

Russell Stover Chocolates

Cavalier Chocolate

Valor Chocolates

Torras S.A.

Diablo Sugar Free

Asher's Chocolate Co.

Advanced stevia purification, precision sweetener blending, and AI-assisted formulation platforms are transforming premium chocolate development. More than 46% of premium manufacturers now integrate digital formulation tools to improve sweetness consistency, while advanced steviol glycoside refinement reduces bitter aftertaste by nearly 20%. Automated ingredient dosing and real-time quality monitoring strengthen batch consistency and reduce manufacturing variability, creating stronger product differentiation in premium confectionery.

Modern multi-sweetener systems combining stevia with dietary fibers and polyols outperform earlier single-sweetener formulations by improving flavor acceptance approximately 18% while reducing formulation adjustments by nearly 15%. Digital process control enables faster product validation and lower ingredient waste. Premium manufacturers with integrated formulation laboratories and automated processing capabilities gain competitive advantages through shorter commercialization cycles, improved quality control, and more flexible product customization.

Between 2026 and 2028, predictive formulation software, digital sensory analytics, and precision ingredient optimization are expected to become mainstream across premium confectionery manufacturing. Nearly 55% of larger chocolate producers are projected to expand intelligent production management for healthier product portfolios. Companies investing early in formulation automation, advanced ingredient science, and integrated quality systems will strengthen operational efficiency, accelerate innovation, and maintain superior positioning as clean-label confectionery standards continue advancing.

January 2025 – Barry Callebaut AG reported the commercial rollout of its "Second Generation Chocolate" platform, delivering chocolate with up to 50% less sugar while maintaining cocoa intensity through proprietary processing innovation. The launch strengthens industrial customers' ability to develop premium reduced-sugar chocolate portfolios. Source: www.barry-callebaut.com

March 2024 Barry Callebaut expanded its sugar-reduction solutions portfolio for industrial food manufacturers, promoting clean-label chocolate formulations using natural sweeteners. New formulation technologies improved sugar reduction capability by up to 50%, strengthening healthier confectionery innovation and accelerating customer product reformulation. Source: www.barry-callebaut.com

November 2025 – Barry Callebaut AG announced continued investment in value-added chocolate innovation despite challenging cocoa markets, reaffirming its focus on premium specialty chocolate, customer innovation, and differentiated product solutions. The strategy supports long-term development of healthier chocolate formulations and industrial partnerships. Source: www.barry-callebaut.com

2024–2025 – The Hershey Company, Lily's Sweets, Cavalier, Chocolove, and Russell Stover did not publish verified official press releases specifically announcing new stevia chocolate launches or major stevia-focused manufacturing expansions during this period. Their published updates primarily covered broader confectionery portfolios, sustainability initiatives, seasonal launches, and corporate developments rather than dedicated stevia chocolate products.

This report provides comprehensive analysis of the global Stevia Chocolate Market across major product categories, applications, end-user groups, and regional markets. It evaluates competitive positioning, manufacturing developments, formulation technologies, clean-label innovation, sustainable ingredient sourcing, and evolving premium confectionery trends. The assessment covers established chocolate varieties alongside emerging functional and naturally sweetened product segments, with regional evaluation spanning North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study examines deployment patterns, consumer adoption trends, product innovation strategies, and competitive activities across leading manufacturers and specialty confectionery companies. More than 50% of market activity is concentrated among premium health-oriented chocolate portfolios, while growing investment in advanced sweetener technologies and automated manufacturing continues reshaping product development. The report supports strategic expansion planning, investment evaluation, competitive benchmarking, product portfolio optimization, partnership assessment, and long-term business decision-making across the 2026–2033 planning horizon.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 96 Million |

| Market Revenue (2033) | USD 158.9 Million |

| CAGR (2026–2033) | 6.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Barry Callebaut AG; Lindt & Sprüngli AG; The Hershey Company; Cavalier NV; Chocoladefabriken Peters GmbH; Lily's Sweets LLC; Chocolove; Russell Stover Chocolates; Valor Chocolates; Torras S.A.; Diablo Sugar Free; Asher's Chocolate Co. |

| Customization & Pricing | Available on Request (10% Customization Free) |