Reports

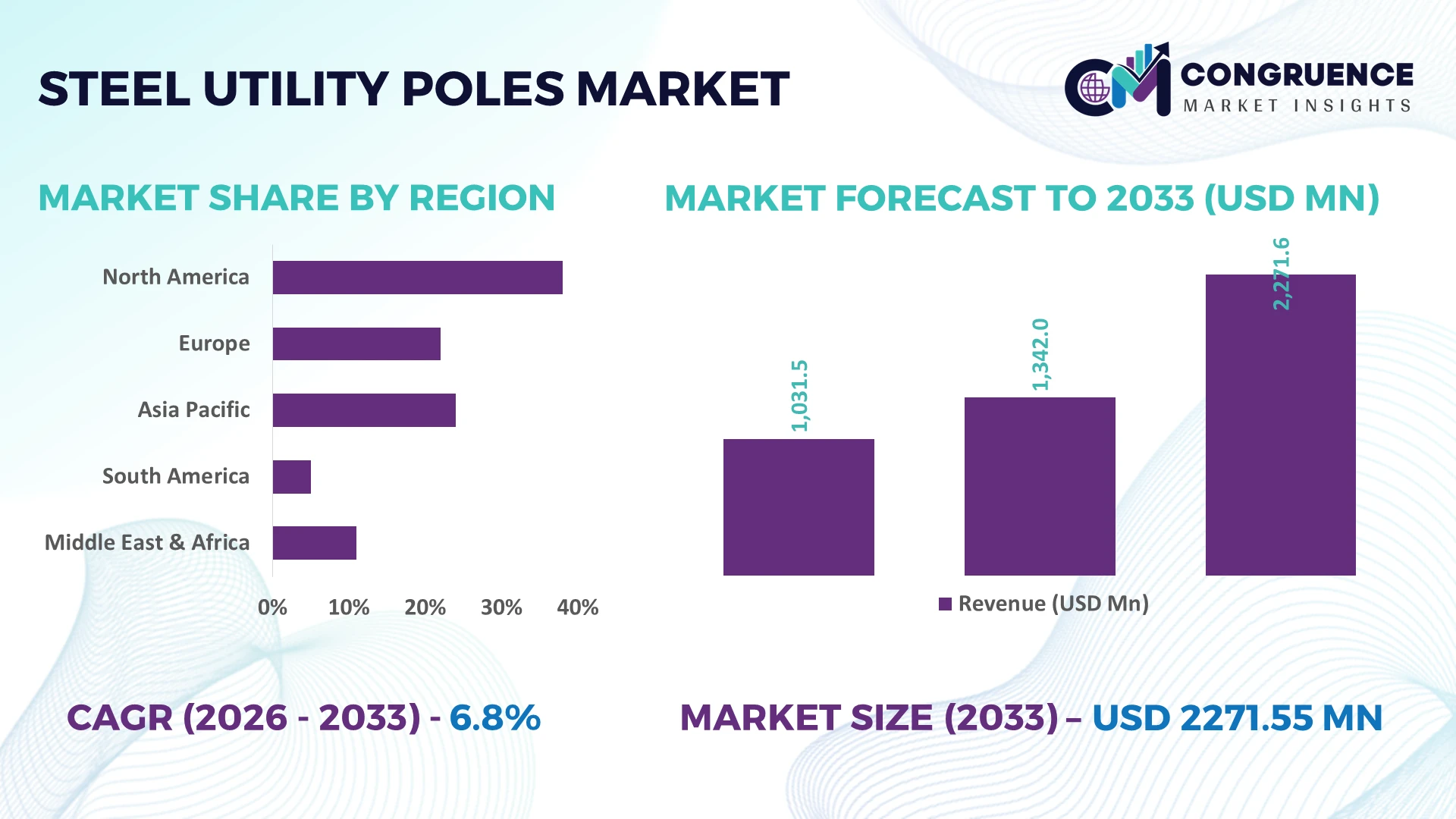

The Global Steel Utility Poles Market was valued at USD 1342 Million in 2025 and is anticipated to reach a value of USD 2271.55 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033. Grid modernization programs, renewable energy interconnections, and replacement of aging wooden transmission infrastructure are accelerating deployment of high-strength galvanized steel utility poles across transmission and distribution networks.

The United States leads the global steel utility poles market with approximately 31% of installed demand, supported by large-scale grid resilience investments, wildfire mitigation programs, and transmission expansion projects. More than 70% of new high-voltage line upgrades increasingly specify corrosion-resistant steel structures, while Canada continues expanding utility infrastructure at a comparatively faster pace through renewable power integration. Ongoing North American energy security initiatives and supply-chain diversification further reinforce regional manufacturing capacity and long-term procurement strategies.

Utilities and manufacturers should prioritize localized production, advanced corrosion-resistant designs, and resilient supply networks to secure long-term contracts in high-investment electricity infrastructure programs.

Market Size & Growth: USD 1342 million (2025) to USD 2271.55 million (2033) at 6.8% CAGR, driven by advanced grid modernization and transmission expansion.

Top Growth Drivers: Grid upgrades contribute 42%, renewable integration 33%, and pole replacement programs 25% of market momentum.

Short-Term Forecast: By 2028, installation efficiency improves 18% through digital engineering and standardized modular pole systems.

Emerging Technologies: AI-based asset inspection, drone monitoring, and advanced galvanized coatings extend service life by over 30%.

Regional Leaders: North America USD 760 million, Asia-Pacific USD 690 million, Europe USD 470 million, supported by resilient infrastructure investments.

Consumer/End-User Trends: Nearly 58% of utilities prioritize steel poles for longer lifecycle performance and reduced maintenance frequency.

Pilot/Case Example: 2026 transmission reinforcement project reduced maintenance requirements by 24% using high-strength steel pole systems.

Competitive Landscape: Top five companies control approximately 48% market share, led by Valmont, Sabre Industries, Arcosa, Nova Pole, and Nippon Steel.

Regulatory & ESG Impact: Asset resilience standards improve lifecycle emissions by approximately 22% through longer-lasting infrastructure materials.

Investment & Funding: More than USD 2.5 billion supports manufacturing expansion, utility partnerships, and transmission infrastructure upgrades amid regional supply-chain shifts.

Innovation & Future Outlook: Smart pole integration, digital monitoring, and higher-strength alloys strengthen next-generation utility infrastructure strategies.

Steel Utility Poles Market demand is expanding across transmission corridors, renewable energy connections, and urban distribution upgrades as utilities prioritize durable infrastructure with lower lifecycle maintenance. Advanced corrosion-resistant coatings and digitally engineered pole designs improve operational performance, while over 35% of new transmission projects increasingly specify steel structures. Grid resilience initiatives and localized manufacturing strategies continue shaping procurement priorities, setting the stage for deeper strategic market analysis.

Steel utility poles have become a strategic infrastructure asset as utilities prioritize grid resilience, transmission expansion, and climate adaptation over short-term replacement cycles. Infrastructure modernization, stricter reliability standards, and supply-chain restructuring following global steel sourcing disruptions are reshaping procurement strategies. Asset owners increasingly favor standardized steel structures because they reduce maintenance requirements, improve structural consistency, and support long-span transmission projects critical for renewable power integration and electrification.

Compared with conventional treated wooden poles, galvanized steel utility poles deliver service lives exceeding 60 years while reducing lifecycle maintenance costs by nearly 35% and installation interruptions by approximately 20% through modular engineering. The United States continues leading large-scale transmission replacement, whereas India is accelerating deployment through rural electrification and high-voltage corridor expansion, creating a stronger volume-driven market with increasing domestic manufacturing participation. Over the next two to three years, digital asset monitoring is expected to be incorporated into nearly 30% of newly installed transmission structures, improving inspection efficiency and maintenance planning.

Utilities are increasingly deploying high-strength steel poles across wildfire-prone transmission corridors where durability and rapid restoration are operational priorities. Manufacturers are expanding galvanizing capacity, forming long-term utility partnerships, and investing in digitally engineered pole systems to strengthen competitive positioning. Companies combining localized manufacturing, advanced corrosion protection, and integrated engineering capabilities will secure stronger contract pipelines and long-term operational advantage.

Replacement of aging utility infrastructure remains the strongest structural driver for steel utility poles as electricity demand and transmission capacity continue expanding. Approximately 45% of transmission assets in the United States are approaching planned replacement cycles, while steel poles reduce maintenance interventions by nearly 30% compared with traditional alternatives. Grid resilience policies and renewable energy interconnections are encouraging utilities to specify corrosion-resistant steel structures for higher reliability. Manufacturers are responding by expanding galvanizing facilities, increasing domestic fabrication capacity, and establishing engineering partnerships with transmission contractors. A notable operational shift is the growing use of standardized modular pole designs that shorten project installation schedules and improve procurement efficiency, strengthening long-term competitiveness across utility infrastructure programs.

Steel utility pole manufacturers continue facing pressure from fluctuating steel input prices, extended procurement timelines, and inconsistent project approvals. Raw material costs can account for nearly 60% of manufacturing expenses, while lead times for specialized structural steel have increased by approximately 20% during periods of supply imbalance. Infrastructure projects in countries including Germany and Australia also encounter strict certification and compliance requirements that extend procurement cycles. These conditions reduce pricing flexibility and complicate large utility contracts. Companies are mitigating operational risks through multi-year steel supply agreements, localized sourcing strategies, inventory optimization, and greater automation within fabrication facilities to stabilize production costs and improve delivery reliability.

Integration of digital monitoring technologies with steel utility poles is creating new value beyond structural performance. Embedded sensors, drone-compatible inspection systems, and digital asset management platforms can reduce inspection costs by nearly 25% while improving fault detection accuracy by over 30%. India is expanding high-voltage transmission corridors with greater emphasis on digitally managed infrastructure, creating opportunities for integrated engineering solutions. Manufacturers are investing in smart pole platforms, protective coating innovations, and collaborative technology partnerships that combine structural hardware with monitoring capabilities. An emerging opportunity lies in bundled infrastructure contracts where utilities procure engineering, installation, monitoring, and lifecycle maintenance through a single supplier, improving long-term operational efficiency.

Large-scale deployment increasingly depends on specialized engineering expertise, advanced fabrication capabilities, and coordinated utility project execution rather than manufacturing capacity alone. Skilled technical labor shortages exceeding 15% in several developed markets and project approval delays of up to 18% continue affecting installation schedules. Expansion of extra-high-voltage networks also requires more sophisticated structural analysis and digital design workflows, increasing execution complexity. Companies must strengthen workforce training, expand automated fabrication, and develop integrated project management capabilities to maintain delivery consistency. Strategic partnerships between utilities, engineering firms, and manufacturers are becoming essential to improve installation quality, accelerate commissioning, and sustain competitive advantage in increasingly complex transmission infrastructure projects.

Smart Asset Monitoring Expansion: Utilities are integrating sensor-enabled steel utility poles with drone inspection workflows, reducing manual inspection time by nearly 40% and improving fault detection accuracy by approximately 28%. Grid digitalization policies in the United States are accelerating deployment, while manufacturers are partnering with software providers to deliver integrated structural monitoring platforms that improve maintenance scheduling and reduce outage response times.

Localized Manufacturing Strategies: Supply-chain diversification is shifting fabrication closer to end markets, with domestic sourcing increasing by nearly 25% across several utility procurement programs and logistics costs declining by approximately 12%. Steel fabricators are expanding galvanizing capacity, restructuring supplier networks, and investing in automated production lines to improve delivery reliability while reducing exposure to international material disruptions.

Advanced Coating Technology Adoption: High-performance galvanizing and duplex coating systems are extending corrosion resistance by more than 30% in coastal and industrial environments while reducing lifecycle maintenance interventions by nearly 22%. Utilities are increasingly specifying enhanced protective finishes within procurement standards, encouraging manufacturers to expand metallurgical research, coating partnerships, and performance-certified product portfolios for demanding transmission applications.

Modular Engineering Standardization: Standardized modular steel pole designs are shortening field installation time by approximately 18% and lowering project engineering revisions by nearly 20% through digital design libraries and prefabricated components. Labor shortages across major transmission projects are encouraging utilities and engineering firms to adopt repeatable structural configurations, prompting suppliers to scale modular manufacturing capabilities and integrated engineering services.

Transmission Poles remain the dominant segment, accounting for approximately 39% of installations due to their ability to support high-voltage networks, long-span applications, and large-scale grid expansion projects. Utilities increasingly specify galvanized steel transmission poles because they offer superior structural reliability, lower lifecycle maintenance, and greater resilience under extreme weather conditions. Tubular Poles continue serving urban infrastructure projects where compact design and faster installation improve operational efficiency, while Lattice Poles retain strategic importance for extra-high-voltage corridors requiring maximum load-bearing performance. Companies are expanding fabrication capacity and strengthening engineering capabilities to support increasingly complex transmission specifications.

Tapered Poles represent the fastest-growing segment as utilities prioritize lighter structures, simplified transportation, and optimized installation workflows, with deployment increasing by nearly 24% across modern distribution upgrades. Distribution Poles continue representing a mature, high-volume category supporting urban electrification and replacement programs. Manufacturers are expanding modular product portfolios, improving corrosion-resistant coatings, and developing customized structural solutions to address diverse utility requirements while strengthening long-term procurement opportunities.

Power Transmission represents the largest application as governments and utilities expand high-voltage networks supporting renewable energy integration, cross-border interconnections, and grid resilience. Approximately 46% of new steel utility pole deployments are linked to transmission infrastructure where durability and higher load capacity remain essential. Power Distribution continues generating stable demand through replacement of aging poles and urban network reinforcement. Companies are increasing production flexibility, standardizing engineering designs, and expanding project support capabilities to meet utility procurement requirements.

Railway Electrification is emerging as the fastest-growing application, with deployment activity rising by nearly 21% as electrified rail corridors expand and carbon reduction policies accelerate infrastructure investment. Street Lighting increasingly adopts steel poles for longer operational life and lower maintenance requirements, while Telecommunications benefits from multi-purpose pole designs supporting communication equipment integration. Manufacturers are introducing application-specific designs and forming partnerships with transportation and infrastructure contractors to diversify deployment opportunities beyond conventional electricity networks.

Utilities remain the largest end-user group, representing approximately 62% of procurement activity because electricity transmission and distribution networks require continuous infrastructure modernization and asset replacement. Long-term maintenance savings, grid resilience objectives, and wildfire mitigation initiatives continue strengthening demand for steel utility poles. Industrial Facilities also contribute consistent demand through captive power infrastructure and private transmission systems. Manufacturers are prioritizing utility-focused engineering support, customized structural designs, and long-term framework agreements to strengthen customer retention.

Railways are the fastest-growing end-user segment, with electrification projects increasing procurement volumes by nearly 23% across expanding transportation corridors. Telecom Companies continue adopting steel poles supporting integrated communication infrastructure, while Municipalities increasingly specify corrosion-resistant poles for public infrastructure upgrades and smart city projects. Suppliers are responding through application-specific product development, integrated installation services, and strategic partnerships that improve lifecycle value while expanding opportunities across diversified infrastructure sectors.

North America accounted for the largest market share at 37.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 7.6% between 2026 and 2033.

Grid Resilience Drives Infrastructure Replacement

North America maintains the highest deployment concentration for steel utility poles through extensive transmission modernization, wildfire mitigation initiatives, and replacement of aging wooden infrastructure. The region contributes nearly 38% of global demand, supported by long-distance transmission expansion and utility resilience investments. More than 70% of new high-voltage utility projects increasingly specify galvanized steel structures for durability and lower lifecycle maintenance. Utilities are expanding procurement partnerships with domestic fabricators while manufacturers continue increasing galvanizing capacity and automated production to improve delivery reliability. Standardized engineering designs and digital asset management are further strengthening operational efficiency across major grid modernization programs.

United States Market Outlook: The United States remains the largest national market due to extensive transmission investments, advanced utility engineering standards, and large-scale infrastructure replacement programs. More than 45% of transmission assets are approaching modernization cycles, creating sustained demand for corrosion-resistant steel utility poles. Domestic manufacturers continue investing in fabrication automation, engineering services, and localized supply chains to improve production flexibility while supporting renewable energy integration and grid resilience objectives across multiple states.

Energy Transition Reshapes Utility Infrastructure

Europe continues strengthening steel utility pole deployment through electricity network modernization, renewable energy integration, and stricter infrastructure resilience requirements. The region represents approximately 24% of global demand, with utilities emphasizing long-service-life structures and standardized engineering specifications. Cross-border transmission investments and grid reinforcement programs continue supporting procurement activity, while advanced coating technologies improve structural durability in demanding environments. Manufacturers are collaborating with transmission operators and engineering firms to deliver customized high-voltage support systems that align with increasingly stringent technical and sustainability requirements.

Germany Market Outlook: Germany leads the European market through advanced transmission expansion, industrial manufacturing capabilities, and energy transition projects requiring resilient utility infrastructure. National grid operators continue upgrading high-voltage corridors connecting renewable generation assets, while engineering companies expand digital design and structural optimization capabilities. Approximately 35% of newly planned transmission reinforcement projects increasingly incorporate steel support structures to improve operational reliability and long-term maintenance performance.

Manufacturing Scale Accelerates Network Expansion

Asia-Pacific is emerging as the fastest-expanding market, supported by rapid electrification, industrialization, and large-scale transmission development. The region contributes approximately 31% of global installations and continues expanding manufacturing capacity for galvanized steel utility poles. National utilities are investing in extra-high-voltage transmission corridors, while local fabricators strengthen export competitiveness through automated production and standardized product portfolios. Large infrastructure programs and expanding renewable power integration continue driving demand for durable steel structures capable of supporting higher network loads with improved operational efficiency.

China Market Outlook: China remains the region's most influential market through unmatched manufacturing capacity, integrated steel production, and nationwide transmission expansion. Ultra-high-voltage electricity corridors and renewable energy projects continue generating significant procurement activity for advanced steel utility poles. More than 40% of newly installed long-distance transmission structures increasingly utilize high-strength steel configurations, encouraging manufacturers to expand automated fabrication, protective coating technologies, and engineering partnerships supporting domestic and international infrastructure projects.

Transmission Expansion Supports Utility Modernization

South America is strengthening demand through transmission expansion, rural electrification, and replacement of aging electricity infrastructure. The region accounts for nearly 5% of global market activity, with utilities prioritizing durable steel poles capable of operating in diverse climatic conditions. National infrastructure programs continue supporting high-voltage network upgrades, while electricity providers seek longer asset life and reduced maintenance requirements. Manufacturers are expanding regional distribution partnerships and localized fabrication capabilities to improve project responsiveness despite logistical and procurement challenges affecting certain infrastructure developments.

Brazil Market Outlook: Brazil represents the largest national market because of extensive electricity transmission requirements, expanding renewable energy projects, and continuous investment in grid modernization. Utility operators are strengthening long-distance transmission networks connecting hydropower, wind, and solar generation assets across multiple states. Steel utility pole suppliers continue enhancing domestic manufacturing and engineering support, while large infrastructure contractors increasingly specify corrosion-resistant structural solutions capable of improving long-term operational reliability.

Infrastructure Investment Strengthens Grid Reliability

The Middle East & Africa market continues advancing through electricity network expansion, industrial development, and national infrastructure modernization initiatives. The region contributes approximately 2% of global demand but is steadily increasing deployment across transmission and distribution networks. Governments are prioritizing resilient utility infrastructure supporting urban expansion, industrial zones, and renewable energy integration. Manufacturers are strengthening regional partnerships, expanding fabrication support, and improving localized engineering services to meet project specifications while reducing delivery timelines for strategic infrastructure developments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through large-scale electricity infrastructure investments aligned with industrial diversification and smart city development. National utilities continue expanding transmission capacity to support growing industrial zones and renewable energy projects, while engineering firms adopt advanced galvanized steel utility poles for improved durability in demanding environmental conditions. Utility infrastructure programs increasingly emphasize localized procurement and technology collaboration to strengthen long-term operational resilience and execution efficiency.

The market is led by global manufacturers including Valmont Industries, Sabre Industries, Arcosa, Nova Pole International, and Nippon Steel, competing against regional fabricators that emphasize lower production costs and faster delivery. Global leaders challenge regional suppliers through engineering capability, lifecycle performance, and integrated project support, while cost-focused manufacturers compete on localized fabrication and procurement flexibility. The top five companies collectively control approximately 48% of the market, reflecting moderate consolidation. Competition increasingly centers on corrosion-resistant technology, automated manufacturing, and supply-chain reliability, with advanced galvanizing reducing lifecycle maintenance by nearly 30% and automated fabrication improving production efficiency by approximately 20%. Companies are expanding galvanizing facilities, forming utility partnerships, integrating engineering with fabrication, and strengthening domestic steel sourcing through vertical integration. The competitive shift favors supply security, customized transmission solutions, and digital engineering over price-led bidding alone. High certification requirements and utility qualification processes remain the primary entry barriers. Winning requires engineering expertise, dependable delivery, localized manufacturing, and long-term utility relationships.

Valmont Industries

Sabre Industries

Arcosa Inc.

Nova Pole International Inc.

Nippon Steel Corporation

KEC International Ltd.

Pelco Structural LLC

RS Technologies Inc.

Skipper Limited

Tata Steel Limited

EZEFLOW Group

Elsewedy Electric

Jiangsu Hongtu High Technology Co., Ltd.

Digital engineering, advanced galvanizing, and high-strength steel alloys are redefining steel utility pole performance and manufacturing efficiency. Automated structural design platforms reduce engineering lead times by approximately 22%, while robotic welding improves fabrication consistency by nearly 18%. More than 45% of newly specified transmission projects now incorporate digitally engineered steel pole configurations, enabling faster customization and standardized production. Utilities benefit from improved project execution, while manufacturers strengthen competitiveness through shorter delivery cycles and higher production accuracy.

Emerging technologies include sensor-enabled structural monitoring, drone-assisted inspections, digital twins, and duplex corrosion-protection systems. Compared with conventional inspection methods, integrated monitoring solutions reduce maintenance costs by nearly 28% and improve fault identification efficiency by approximately 35%. Adoption continues expanding across critical transmission corridors where utilities prioritize predictive maintenance and network resilience. Companies offering combined engineering, monitoring, and lifecycle service capabilities gain stronger differentiation than suppliers focused solely on structural fabrication.

Between 2026 and 2028, modular prefabrication, AI-assisted structural optimization, and low-carbon steel processing will accelerate deployment across large transmission programs. Smart manufacturing platforms will improve production throughput by approximately 20%, while advanced material technologies extend operational service life beyond traditional galvanized designs. Companies investing early in integrated digital manufacturing, intelligent monitoring, and sustainable metallurgy will secure stronger utility partnerships, higher-value infrastructure contracts, and lasting competitive advantage.

March 2025 – Valmont Industries announced tariff mitigation measures, including supply-chain optimization, pricing actions, and logistics restructuring to protect infrastructure operations. The company expects these actions to remain cost neutral during the second half of 2025, strengthening delivery reliability for utility customers. Source: investors.valmont.com

April 2025 – Valmont Industries reported continued expansion of its infrastructure capacity investments as utility demand strengthened. Utility and telecommunications businesses supported operational momentum while new production capacity was scheduled to contribute during 2025, reinforcing manufacturing scalability and project execution. Operating cash flow reached USD 65.1 million.

June 2025 – Valmont Industries released its 2025 Sustainability Report, highlighting resilient infrastructure innovation and operational efficiency initiatives. The company emphasized performance improvements across global operations supported by its 11,000 employees, reinforcing long-term infrastructure resilience and ESG-focused customer engagement.

July 2025 – Valmont Industries raised its full-year earnings outlook following stronger infrastructure execution. Utility sales increased through higher volumes and pricing actions, while infrastructure operations maintained stable performance despite market pressures, demonstrating improved manufacturing discipline and portfolio optimization. Infrastructure sales totaled USD 765.5 million for the quarter.

The report delivers comprehensive analysis of the global Steel Utility Poles Market across Transmission Poles, Distribution Poles, Tubular Poles, Tapered Poles, and Lattice Poles. It evaluates demand across Power Transmission, Power Distribution, Street Lighting, Telecommunications, Railway Electrification, and major end-user groups including Utilities, Telecom Companies, Railways, Municipalities, and Industrial Facilities. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while tracking adoption patterns, deployment intensity, and competitive positioning across more than five major infrastructure ecosystems.

The study examines advanced galvanizing technologies, high-strength steel materials, digital engineering, smart asset monitoring, and automated fabrication shaping industry competitiveness between 2026 and 2033. It provides strategic benchmarking of leading manufacturers, identifies deployment trends exceeding 60% in transmission-focused utility projects, evaluates procurement priorities, manufacturing localization, and investment strategies, and supports expansion planning, product portfolio optimization, partnership development, competitive positioning, and long-term infrastructure decision-making across established and emerging markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1342 Million |

Market Revenue in 2033 | USD 2271.55 Million |

CAGR (2026 - 2033) | 6.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Valmont Industries, Sabre Industries, Arcosa Inc., Nova Pole International Inc., Nippon Steel Corporation, KEC International Ltd., Pelco Structural LLC, RS Technologies Inc., Skipper Limited, Tata Steel Limited, EZEFLOW Group, Elsewedy Electric, Jiangsu Hongtu High Technology Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |