Reports

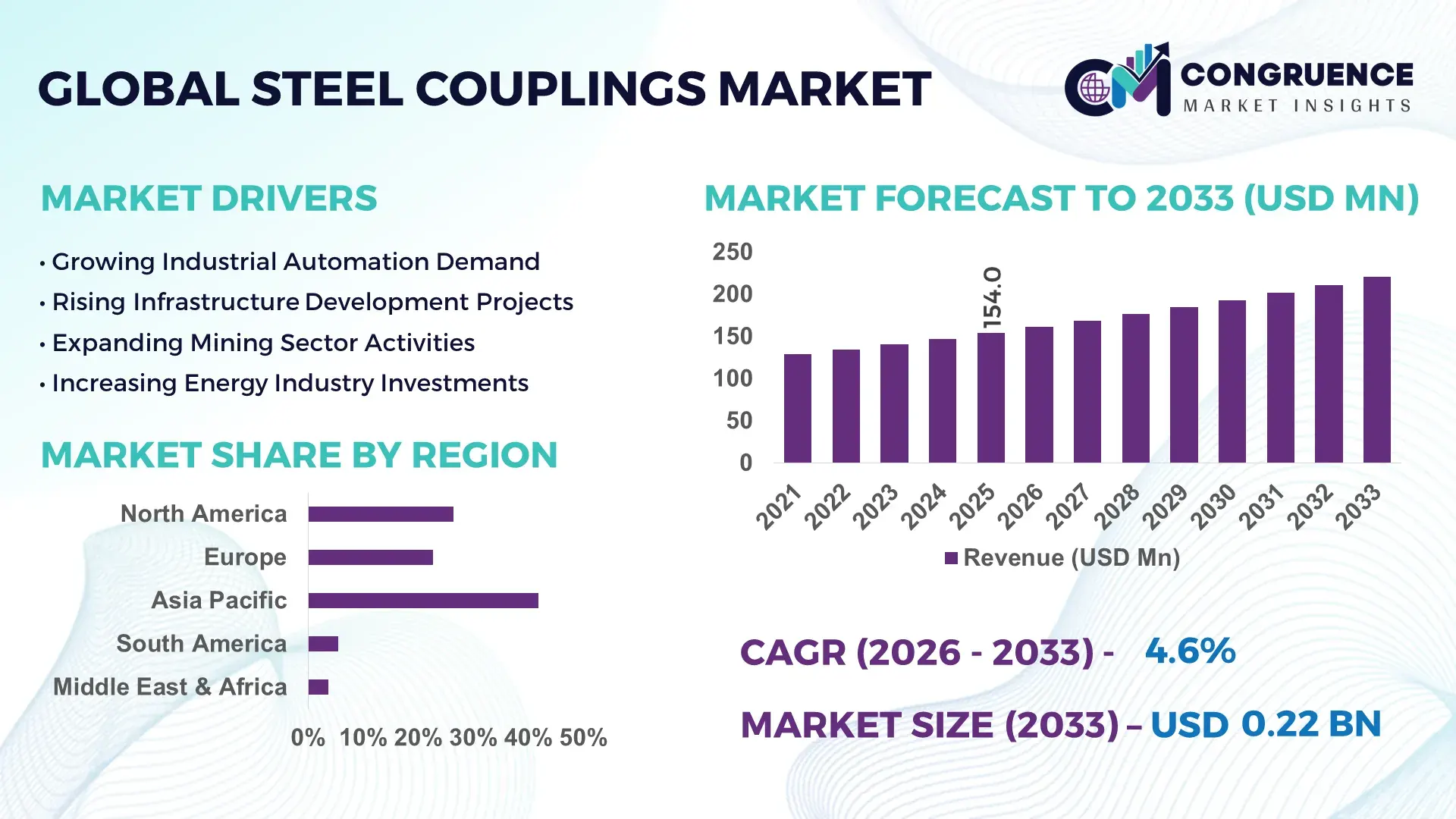

The Global Steel Couplings Market was valued at USD 154.0 Million in 2025 and is anticipated to reach a value of USD 220.7 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Growth is being propelled by accelerating pipeline modernization projects, rising deployment of high-torque industrial transmission systems, and increasing replacement of aging mechanical coupling infrastructure across energy, mining, and water networks.

China remains the dominant country in the global steel couplings market, accounting for nearly 32% of global industrial machinery output and over 30% of installed pipeline infrastructure additions linked to manufacturing, energy, and water treatment sectors. The country’s steel processing capacity exceeds 1 billion tons annually, significantly outpacing Germany’s industrial metal component production footprint. Supported by large-scale industrial automation investments and infrastructure upgrades, coupling adoption in heavy-duty transmission systems has increased by approximately 12% over the past three years. Ongoing industrial expansion and supply-chain localization initiatives continue strengthening its leadership position.

Strategic implication: Manufacturers prioritizing industrial automation compatibility, localized production, and high-performance coupling solutions are best positioned to capture long-term infrastructure and process-industry opportunities.

Market Size & Growth: USD 154.0 Million in 2025, reaching USD 220.7 Million by 2033 at 4.6% CAGR, supported by pipeline modernization, industrial automation, and transmission efficiency upgrades.

Top Growth Drivers: Water infrastructure investments (+14%), industrial automation deployment (+18%), and energy pipeline refurbishment activities (+11%) are accelerating demand.

Short-Term Forecast: By 2028, predictive maintenance integration is expected to reduce unplanned downtime by nearly 20% across industrial transmission systems.

Emerging Technologies: Smart monitoring sensors, AI-enabled maintenance analytics, and advanced corrosion-resistant alloys are improving operational reliability by over 15%.

Regional Leaders: Asia Pacific (~USD 82 Million), North America (~USD 48 Million), and Europe (~USD 41 Million) lead through manufacturing expansion, energy upgrades, and automation adoption.

Consumer/End-User Trends: More than 42% of large industrial facilities now prioritize high-performance flexible couplings for vibration reduction and equipment longevity.

Pilot/Case Example: In 2024, a mining transmission upgrade project achieved a 17% reduction in maintenance interventions through advanced steel coupling deployment.

Competitive Landscape: Top manufacturers collectively control approximately 38% market share, with key participants including Rexnord, Regal Rexnord, SKF, Timken, and Voith.

Regulatory & ESG Impact: Energy-efficiency standards have driven equipment optimization initiatives delivering up to 10% lower power transmission losses.

Investment & Funding: More than USD 900 Million in industrial drivetrain and infrastructure modernization investments are supporting advanced coupling installations globally.

Innovation & Future Outlook: Digital condition monitoring, lightweight high-strength metallurgy, and supply-chain regionalization are reshaping competitive positioning across high-growth industrial sectors.

Steel couplings play a critical role in power transmission systems across mining, oil & gas, manufacturing, and water treatment facilities where reliability and torque management remain operational priorities. Recent innovations focus on smart condition-monitoring integration, corrosion-resistant alloy development, and vibration-control technologies. Approximately 35% of large industrial operators are expanding predictive maintenance programs, while ongoing supply-chain localization efforts are accelerating procurement of high-performance coupling assemblies, creating a favorable environment for strategic industrial investments and technology-led differentiation.

Steel couplings are becoming strategically important as industrial operators focus on equipment reliability, energy efficiency, and asset lifecycle optimization. Infrastructure modernization programs, manufacturing expansion, and transmission-system upgrades are increasing the importance of durable mechanical power-transfer components. Simultaneously, supply-chain restructuring following global manufacturing realignments is encouraging localized sourcing strategies, prompting suppliers to strengthen regional production footprints and aftermarket service networks.

Technology advancement is reshaping competitive dynamics. Smart monitoring-enabled coupling systems can reduce unexpected equipment failures by nearly 20% compared with conventional maintenance approaches, while advanced alloy-based couplings extend service life by approximately 15% in high-load environments. China continues to lead in large-scale deployment due to extensive industrial capacity, whereas Germany and Japan emphasize precision-engineered, high-efficiency solutions for advanced manufacturing applications. Over the next two to three years, industrial digitalization initiatives are expected to increase condition-monitoring adoption rates by more than 25% across critical machinery assets.

A practical example is the deployment of sensor-integrated couplings in mining and process industries, enabling real-time vibration monitoring and maintenance planning. Manufacturers are expanding partnerships with automation providers, investing in smart component portfolios, and strengthening localized production capabilities. Companies that combine engineering performance, digital diagnostics, and supply-chain resilience will secure stronger competitive positioning and long-term industrial relevance.

Expansion of industrial infrastructure and modernization of power transmission systems remains the strongest demand catalyst for steel couplings. More than 60% of newly commissioned process-industry facilities now incorporate upgraded mechanical drive systems designed for higher operational efficiency. Industrial automation deployment has increased by approximately 18% across major manufacturing hubs, while water infrastructure investments have expanded by nearly 14% in key economies. Rising pipeline rehabilitation activity following energy-security initiatives has further strengthened replacement demand. As transmission systems become more sophisticated, equipment operators require couplings capable of handling greater torque loads and vibration control. In response, manufacturers are expanding production capacity, developing application-specific coupling designs, and forming partnerships with industrial OEMs. A notable strategic outcome is the growing shift toward lifecycle-performance contracts that integrate component reliability with maintenance services.

Steel couplings manufacturers continue to face pressure from fluctuating steel prices, supply disruptions, and procurement uncertainty. Industrial steel input costs have experienced periodic swings exceeding 15% in several manufacturing markets, while logistics expenses remain elevated compared with pre-disruption benchmarks. Dependence on specialized alloy grades creates additional sourcing challenges, particularly for precision-engineered coupling products. These factors directly impact margins, pricing consistency, and production planning efficiency. Manufacturers serving oil & gas, mining, and heavy industry customers often encounter extended procurement cycles as buyers delay capital expenditures during periods of cost instability. To mitigate risks, companies are diversifying supplier networks, increasing localized sourcing, and negotiating long-term procurement agreements. A critical operational insight is that firms with vertically integrated supply capabilities are maintaining stronger delivery performance and customer retention rates.

The emergence of connected industrial ecosystems is creating significant opportunities for intelligent steel coupling solutions. Predictive maintenance deployments have expanded by approximately 30% across digitally advanced industrial facilities, while connected asset monitoring programs now cover more than 40% of critical rotating equipment in several manufacturing sectors. Smart couplings equipped with vibration, torque, and alignment monitoring capabilities enable earlier fault detection and improved maintenance scheduling. Germany, Japan, and South Korea are accelerating adoption through advanced manufacturing initiatives emphasizing operational efficiency and machine uptime. Manufacturers are investing in sensor-enabled product development, industrial IoT integration, and strategic partnerships with automation providers. A less obvious opportunity lies in aftermarket analytics services, where coupling performance data can support maintenance optimization and generate recurring service revenues beyond traditional component sales.

Long-term market expansion depends on overcoming integration complexity across diverse industrial environments. Nearly 28% of industrial operators report challenges related to equipment compatibility and system standardization during transmission upgrades. At the same time, shortages of experienced maintenance personnel continue affecting installation quality and operational consistency across heavy industries. The growing incorporation of digital monitoring technologies introduces additional requirements for data interpretation, system calibration, and workforce training. In countries with aging industrial infrastructure, modernization projects often face implementation delays due to technical integration challenges. Companies are responding through training programs, digital support platforms, and closer collaboration with OEMs and maintenance providers. A key strategic requirement is developing standardized coupling ecosystems that simplify deployment while supporting advanced monitoring capabilities and long-term operational reliability.

Smart Monitoring Integration Accelerates Industrial operators are embedding sensors into coupling assemblies to improve asset visibility and maintenance planning. Adoption of condition-monitoring technologies has increased by nearly 28%, while predictive maintenance deployment across rotating equipment has expanded by over 30%. Facilities using real-time torque and vibration diagnostics report maintenance response times improving by approximately 18%. Companies are partnering with industrial automation providers and integrating coupling data into plant-wide monitoring platforms to strengthen operational reliability and reduce unplanned shutdowns.

Localization Reshapes Supply Networks Ongoing supply-chain disruptions and geopolitical manufacturing realignments are accelerating regional sourcing strategies. More than 40% of industrial equipment manufacturers have increased local procurement initiatives, while lead times for critical mechanical components have improved by nearly 15% through supplier diversification programs. China and India continue expanding domestic production capabilities to reduce dependency on imported industrial components. Manufacturers are restructuring supplier ecosystems, expanding local inventories, and establishing regional assembly operations to improve responsiveness and supply security.

Advanced Metallurgy Gains Traction Demand for high-strength, corrosion-resistant coupling materials continues rising in mining, energy, and marine applications. Deployment of advanced alloy-based couplings has increased by approximately 22%, while lifecycle replacement intervals have improved by nearly 16% in high-load operating environments. A less obvious shift involves operators prioritizing lifecycle efficiency rather than upfront equipment costs. Companies are expanding metallurgical R&D programs and launching application-specific product lines designed for harsh industrial conditions and extended operational performance.

Modular Design Adoption Expands Industrial facilities are increasingly selecting modular coupling systems to simplify maintenance workflows and accelerate equipment upgrades. Installation times have declined by roughly 20%, while maintenance labor requirements have fallen by nearly 12% through modular component standardization. Labor shortages across industrial maintenance functions are reinforcing this trend, particularly in Germany and Japan. Manufacturers are introducing configurable coupling platforms, expanding aftermarket service programs, and strengthening OEM partnerships to support faster deployment and improved asset utilization.

Flexible couplings represent the leading segment within the steel couplings market, accounting for approximately 48% of total installations due to their superior vibration damping, misalignment compensation, and equipment protection capabilities. Heavy industries including mining, water treatment, and manufacturing increasingly prioritize flexible designs to improve machinery lifespan and reduce maintenance frequency. Their scalability across multiple operating environments and compatibility with automated industrial systems continue supporting widespread adoption. Manufacturers are expanding flexible coupling portfolios with advanced elastomer and metallic designs capable of handling higher torque requirements and demanding operational conditions. Rigid couplings are emerging as the fastest-growing segment, supported by increasing deployment in precision-driven industrial applications where alignment accuracy and torque transmission efficiency remain critical. Adoption has increased by nearly 14% among advanced manufacturing facilities seeking improved drivetrain stability. Sleeve, flange, and clamp-style couplings continue serving established applications requiring cost-effective mechanical connectivity and simplified installation. Investment priorities are gradually shifting toward performance-optimized coupling solutions that combine durability, operational efficiency, and digital monitoring compatibility, creating new differentiation opportunities for equipment suppliers.

Industrial machinery remains the dominant application segment, representing approximately 42% of steel coupling utilization due to extensive deployment across manufacturing, processing, and material-handling operations. Rising automation intensity and increasing equipment utilization rates continue reinforcing demand. Facilities integrating advanced production systems have reported operational efficiency improvements exceeding 15% when deploying upgraded mechanical transmission components. Manufacturers are responding by expanding industrial-grade coupling offerings optimized for high-load and continuous-duty environments. Oil & gas is emerging as the fastest-growing application segment as pipeline modernization programs, refinery upgrades, and energy infrastructure investments accelerate deployment of high-performance coupling solutions. Demand from water and wastewater treatment facilities is also increasing, supported by infrastructure rehabilitation initiatives and stricter reliability requirements. Mining applications continue emphasizing heavy-duty couplings capable of operating under extreme loads and abrasive conditions. Companies are scaling production capacity, strengthening aftermarket support networks, and developing application-specific engineering solutions to address increasingly specialized operational requirements across these sectors.

The Energy & Utilities sector remains the largest end-user segment, accounting for nearly 38% of total demand due to extensive dependence on pumps, compressors, turbines, and pipeline infrastructure. Continuous asset operation requirements and reliability-focused maintenance strategies are sustaining procurement activity. More than 45% of utility operators have accelerated equipment modernization initiatives to improve operational efficiency and reduce lifecycle maintenance costs. Suppliers are increasingly offering customized coupling solutions tailored to critical infrastructure environments where equipment downtime carries significant operational consequences. The Manufacturing Industry represents the fastest-growing end-user segment, driven by factory automation investments, production line upgrades, and expanding deployment of connected industrial systems. Adoption of advanced drivetrain technologies has increased by approximately 17% among large-scale manufacturers over recent years. Mining, Construction, and Water Infrastructure organizations continue expanding usage of heavy-duty coupling systems designed for harsh operating conditions and long service intervals. To strengthen competitive positioning, manufacturers are pursuing OEM partnerships, sector-focused product development strategies, and service-based support models that address evolving customer performance requirements.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

North America accounted for approximately 26.4% of global steel coupling demand in 2025, supported by extensive deployment across energy infrastructure, industrial manufacturing, mining operations, and water treatment facilities. The region continues to prioritize asset reliability and predictive maintenance integration, accelerating demand for high-performance coupling systems. More than 45% of large industrial facilities have incorporated condition-monitoring technologies into rotating equipment maintenance programs. Ongoing investments in pipeline upgrades and industrial automation are strengthening replacement demand for advanced couplings. Equipment operators increasingly favor engineered solutions capable of reducing vibration-related failures and improving transmission efficiency across critical infrastructure assets.

United States Market Outlook: The United States remains the dominant market within North America due to its extensive industrial base, large-scale energy infrastructure, and advanced manufacturing ecosystem. The country operates thousands of miles of transmission pipelines and maintains one of the world's largest installed bases of industrial rotating equipment. Nearly 50% of major manufacturing facilities have expanded automation-focused modernization initiatives, increasing demand for precision-engineered couplings. Domestic suppliers are investing in smart monitoring capabilities, localized production, and aftermarket service networks to improve equipment uptime and lifecycle performance.

Europe represented nearly 22.7% of global market activity in 2025, supported by advanced manufacturing operations, process industries, and infrastructure modernization projects. Regulatory emphasis on energy efficiency and operational reliability continues influencing equipment replacement strategies across industrial sectors. Adoption of predictive maintenance technologies has increased by approximately 24% among major industrial operators. Industrial facilities are increasingly deploying advanced coupling systems to optimize power transmission efficiency and reduce maintenance requirements. Strategic collaborations between component manufacturers and automation providers are accelerating deployment of digitally enabled drivetrain solutions across key industrial hubs.

Germany Market Outlook: Germany serves as the strategic center of the European steel couplings market due to its strong engineering expertise, industrial machinery leadership, and highly automated manufacturing environment. The country accounts for a significant share of European industrial equipment production and continues expanding Industry 4.0 implementation programs. More than 30% of large manufacturing facilities have accelerated digital maintenance initiatives to improve asset reliability. German enterprises are increasingly adopting high-precision couplings designed for automated production systems, robotics, and advanced process-control environments.

Asia-Pacific remains the largest regional market, contributing approximately 41.8% of global demand in 2025. Strong manufacturing activity, expanding industrial infrastructure, and large-scale construction of energy and water networks continue supporting market expansion. The region accounts for more than 50% of global industrial machinery production capacity, creating substantial demand for mechanical power transmission components. Industrial automation deployment has increased by nearly 18% across major manufacturing economies, while infrastructure investment programs continue strengthening replacement and new-installation opportunities. Manufacturers are expanding local production capabilities and enhancing supply-chain integration to support rising demand.

China Market Outlook: China maintains the strongest market position in Asia-Pacific through its extensive manufacturing ecosystem, steel processing capacity, and industrial infrastructure investments. The country contributes over 30% of global manufacturing output and continues expanding automation-driven production facilities. Industrial equipment modernization initiatives have increased adoption of advanced drivetrain technologies by approximately 12% in recent years. Domestic manufacturers are strengthening technological capabilities through product innovation, smart manufacturing integration, and export-oriented production strategies, reinforcing China's leadership across industrial coupling applications.

South America accounted for approximately 5.4% of global market demand in 2025, driven primarily by mining operations, energy projects, and industrial infrastructure development. Demand remains concentrated in sectors requiring heavy-duty power transmission systems capable of operating under challenging environmental conditions. Mining investment activity has increased across several countries, creating opportunities for high-torque coupling solutions. However, infrastructure limitations and capital expenditure fluctuations continue influencing project timelines. Manufacturers are addressing these challenges through regional partnerships, localized distribution strategies, and expanded aftermarket support services that improve equipment availability and operational continuity.

Brazil Market Outlook: Brazil represents the largest market in South America due to its substantial mining sector, industrial manufacturing capacity, and expanding energy infrastructure. The country accounts for a significant portion of regional industrial output and continues investing in transportation, energy, and resource extraction projects. More than 40% of regional mining-related coupling demand originates from Brazilian operations. Suppliers are strengthening local service networks and inventory management capabilities to support critical industrial assets operating in remote and high-utilization environments.

The Middle East & Africa region contributed approximately 3.7% of global demand in 2025, supported by energy infrastructure modernization, water management projects, and industrial diversification initiatives. Large-scale investments in petrochemical facilities, pipeline networks, and utility infrastructure continue generating demand for high-performance steel couplings. Several countries are expanding industrial development programs aimed at reducing dependence on traditional hydrocarbon revenues. Coupling suppliers are increasingly participating in engineering partnerships and localized support programs to meet project-specific performance requirements. Reliability and operational continuity remain key purchasing priorities across critical infrastructure sectors.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically important market within the region due to its extensive energy infrastructure, industrial diversification agenda, and large-scale capital investment programs. Ongoing industrial development projects are increasing deployment of pumps, compressors, and rotating equipment requiring advanced coupling systems. More than 35% of regional energy-related coupling installations are associated with projects located in the Kingdom. Companies are expanding technical service capabilities, project partnerships, and localized supply operations to support long-term infrastructure modernization and industrial expansion objectives.

The Steel Couplings Market is characterized by competition between global power transmission leaders such as Regal Rexnord Corporation, SKF, Voith, The Timken Company, and Altra Industrial Motion against regional manufacturers competing primarily on cost, lead time, and localized engineering support. The top five players collectively account for approximately 38–42% of market activity, creating a moderately consolidated structure. Competition centers on technology performance, customization capability, supply-chain responsiveness, and lifecycle reliability. Advanced coupling systems can reduce maintenance interventions by nearly 15%, while localized production models improve delivery times by 20–25%. OEM-focused suppliers increasingly differentiate through application-specific engineering and predictive maintenance integration. Leading companies are expanding manufacturing footprints, strengthening distributor partnerships, and investing in smart monitoring capabilities. The competitive shift is moving from component supply toward integrated drivetrain solutions and aftermarket services. High engineering requirements, certification standards, and customer qualification cycles remain significant entry barriers. Winning requires superior reliability, digital integration, localized support, and rapid application-specific customization.

SKF

Voith

The Timken Company

Altra Industrial Motion

Lovejoy LLC

R+W Coupling Technology

KTR Systems GmbH

Tsubakimoto Chain Co.

VULKAN Group

John Crane

Renold plc

Rathi Transpower Pvt. Ltd.

Industrial coupling technology is rapidly evolving from purely mechanical power-transmission components toward intelligent, performance-optimized systems. Current adoption is led by advanced flexible couplings, high-strength alloy designs, and precision-machined torque transmission systems. Nearly 45% of large industrial operators now prioritize vibration-control and alignment-compensation features to improve equipment longevity. Advanced metallurgy is delivering up to 15% longer operational life in harsh mining, energy, and processing environments while reducing replacement frequency.

Emerging technologies center on sensor-enabled condition monitoring, Industrial IoT integration, and predictive maintenance platforms. Smart coupling deployments have increased by approximately 30% across digitally advanced facilities. Compared with conventional inspection-based maintenance, connected coupling systems reduce unplanned downtime by nearly 20% and improve maintenance scheduling accuracy by approximately 25%. Global manufacturers and industrial automation providers benefit most because they can combine hardware, software, and service offerings into integrated drivetrain solutions that strengthen customer retention and aftermarket revenues.

Between 2026 and 2028, intelligent monitoring capabilities, digital twins, and AI-supported diagnostics are expected to become increasingly embedded within critical rotating equipment ecosystems. Adoption levels are projected to exceed 35% among large industrial enterprises. Companies acting now gain stronger asset visibility, faster fault detection, lower maintenance costs, and improved operational continuity, creating measurable competitive advantages in reliability-focused industries.

July 2024 – Voith secured selection of its E-Coupler design as the basis for interface standardization of digital automatic couplers across European rail freight systems. The solution supports interoperability at impact speeds up to 12 km/h, strengthening Voith’s position in next-generation coupling technology deployment. Source: www.voith.com

July 2024 – Voith showcased its CargoFlex Hybrid coupling platform at InnoTrans 2024, enabling gradual fleet conversion toward digital automatic coupling systems. The exhibition targeted more than 130,000 mobility-sector visitors from over 56 countries, reinforcing market visibility and strategic adoption momentum.

May 2025 – SKF announced a partnership with Carnegie Clean Energy to design and manufacture three Power Take-Off units for CETO wave-energy deployment. The collaboration expands SKF’s role from component supplier to integrated system provider, strengthening participation in renewable-energy drivetrain applications.

September 2025 – SKF entered a strategic partnership with Sieb & Meyer to develop integrated high-efficiency drive solutions. The plug-and-play architecture reduces engineering effort while enhancing system efficiency for compressors, turbo-blowers, and HVAC applications, supporting broader industrial drivetrain integration opportunities.

The Steel Couplings Market Report provides comprehensive analysis across major coupling types, applications, end-user industries, and regional markets. The study evaluates flexible, rigid, sleeve, flange, and specialized coupling categories used across industrial machinery, oil & gas, mining, water treatment, and infrastructure environments. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing more than 95% of global industrial deployment activity. The report also assesses evolving demand patterns, technology adoption trends, procurement strategies, and competitive positioning across key industrial sectors.

The analysis incorporates operational benchmarks, deployment trends, digital monitoring adoption, manufacturing capacity developments, and industrial modernization initiatives influencing market direction between 2026 and 2033. Coverage extends to smart coupling technologies, predictive maintenance integration, advanced metallurgy, and localized supply-chain strategies. With evaluation of leading manufacturers, enterprise adoption patterns, and sector-specific investment priorities, the report supports expansion planning, product development, partnership strategies, competitive intelligence, and long-term decision-making for stakeholders operating across the global industrial power transmission ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 154.0 Million |

| Market Revenue (2033) | USD 220.7 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Regal Rexnord Corporation; SKF; Voith; The Timken Company; Altra Industrial Motion; Lovejoy LLC; R+W Coupling Technology; KTR Systems GmbH; Tsubakimoto Chain Co.; VULKAN Group; John Crane; Renold plc; Rathi Transpower Pvt. Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |