Reports

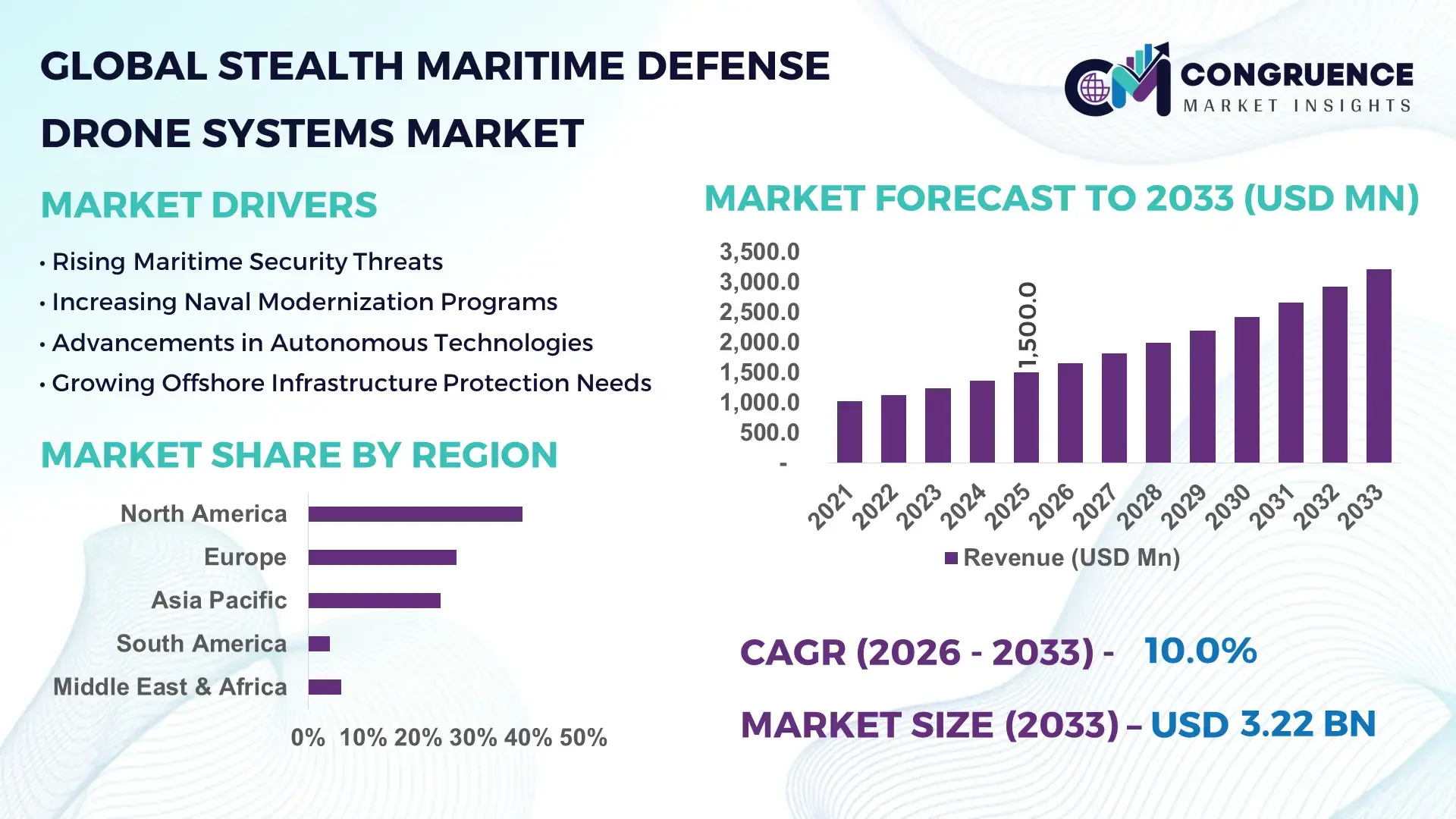

The Global Stealth Maritime Defense Drone Systems Market was valued at USD 1,500.0 Million in 2025 and is anticipated to reach a value of USD 3,215.4 Million by 2033 expanding at a CAGR of 10% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising naval modernization programs, increasing maritime border surveillance requirements, and expanding investments in autonomous stealth-enabled defense platforms.

The United States dominates the Stealth Maritime Defense Drone Systems Market with strong production capacity and sustained defense investment. In 2025, the U.S. defense budget exceeded USD 850 billion, with over USD 40 billion allocated to naval modernization and unmanned systems development. The U.S. Navy operates more than 150 active unmanned maritime platforms, including stealth-capable unmanned surface and underwater vehicles for ISR and mine countermeasure missions. Domestic manufacturers have expanded autonomous maritime drone production lines by nearly 30% since 2022. Additionally, over 65% of next-generation naval R&D programs in the country integrate AI-driven navigation, low-observable materials, and advanced sonar-avoidance technologies, reinforcing technological leadership in stealth maritime defense systems.

Market Size & Growth: Valued at USD 1,500.0 Million in 2025, projected to reach USD 3,215.4 Million by 2033 at 10% CAGR, driven by rising naval automation and stealth surveillance needs.

Top Growth Drivers: 48% increase in naval drone procurement, 35% improvement in mission endurance, 27% reduction in operational risk through autonomy.

Short-Term Forecast: By 2028, AI-enabled maritime drones are expected to reduce patrol operation costs by 22% and improve detection accuracy by 30%.

Emerging Technologies: AI-based autonomous navigation, low-observable composite hull materials, quantum-resistant encrypted communication systems.

Regional Leaders: North America projected at USD 1,120 Million by 2033 with advanced naval integration; Asia-Pacific at USD 980 Million with rapid fleet expansion; Europe at USD 760 Million emphasizing cross-border maritime surveillance.

Consumer/End-User Trends: Over 58% of naval forces globally are piloting autonomous stealth drones for ISR and mine countermeasure operations.

Pilot Case Example: In 2024, a naval deployment reduced maritime surveillance downtime by 26% through AI-powered stealth unmanned surface vehicles.

Competitive Landscape: Market leader holds approximately 24% share, followed by major competitors including BAE Systems, Northrop Grumman, General Dynamics, and Thales Group.

Regulatory & ESG Impact: Over 40% of new naval drone tenders mandate low-emission propulsion and recyclable composite materials.

Investment & Funding Patterns: More than USD 3.5 Billion invested globally in autonomous maritime defense programs between 2023–2025.

Innovation & Future Outlook: Integration of swarm intelligence and hybrid-electric propulsion systems is reshaping next-generation stealth maritime capabilities.

Naval defense accounts for nearly 62% of demand, followed by coast guard surveillance at 21% and border security at 12%. Autonomous underwater vehicles represent 38% of deployments, while unmanned surface vehicles contribute 44%. Regulatory mandates promoting reduced acoustic signatures and hybrid propulsion are influencing procurement. Asia-Pacific defense expansion programs are accelerating consumption, while AI-driven predictive maintenance and swarm-enabled operations are expected to redefine long-term operational efficiency.

The Stealth Maritime Defense Drone Systems Market plays a strategic role in strengthening maritime domain awareness, naval deterrence, and autonomous warfare readiness. Modern stealth maritime drones equipped with AI-enabled navigation deliver 35% higher detection precision compared to traditional manned patrol vessels while reducing crew deployment risks by nearly 40%. Swarm-enabled unmanned surface vehicles outperform conventional single-unit patrol crafts by enabling coordinated coverage expansion of up to 50% per mission cycle.

North America dominates in volume deployment, while Asia-Pacific leads in adoption acceleration with over 60% of newly commissioned naval assets integrating unmanned or semi-autonomous modules. By 2028, AI-powered predictive maintenance in maritime drones is expected to cut unplanned downtime by 28%, enhancing fleet readiness rates significantly.

From a compliance and ESG perspective, defense contractors are committing to 30% reductions in carbon emissions from naval auxiliary systems by 2030 through hybrid-electric propulsion and recyclable stealth composites. In 2024, the United States achieved a 25% improvement in autonomous maritime patrol efficiency through AI-enabled swarm deployment trials.

Strategically, the Stealth Maritime Defense Drone Systems Market is positioned as a pillar of resilience, compliance, and sustainable naval modernization, supporting future-ready maritime security frameworks across advanced and emerging economies.

The Stealth Maritime Defense Drone Systems Market is shaped by increasing geopolitical tensions, maritime territorial disputes, and the need for persistent ocean surveillance. More than 70% of global trade passes through maritime routes, prompting governments to invest in stealth-capable unmanned systems to secure chokepoints and exclusive economic zones. Technological convergence between AI, advanced composites, and encrypted satellite communications is accelerating deployment cycles. Additionally, naval modernization programs across 25+ countries include dedicated budgets for autonomous maritime systems. Operational efficiency improvements of up to 30% compared to conventional patrol units further drive procurement decisions. However, high development costs and integration complexity remain structural considerations influencing procurement strategies.

Increasing piracy incidents, maritime border conflicts, and underwater surveillance needs are accelerating adoption of stealth maritime drones. Over 50 countries reported strengthening naval unmanned capabilities between 2022 and 2025. Autonomous drones reduce manpower requirements by nearly 45% during long-duration patrol missions and extend operational endurance by 30% compared to crewed vessels. These systems provide real-time ISR coverage across high-risk maritime corridors, improving response times by 25%. Growing underwater infrastructure such as subsea cables and offshore energy platforms further necessitates stealth surveillance capabilities, reinforcing demand for advanced maritime defense drones.

Advanced stealth composites, AI navigation systems, and secure communication modules significantly increase production costs. Prototype development cycles can extend beyond 36 months, delaying commercialization. Integration with legacy naval command systems requires additional infrastructure investments of up to 20% of total deployment budgets. Maintenance of stealth coatings and acoustic suppression systems also raises lifecycle costs by nearly 18% compared to standard unmanned vessels. Export restrictions and cross-border regulatory approvals further limit rapid international adoption.

Swarm-enabled maritime drones can expand surveillance coverage by up to 60% without proportional cost increases. AI-driven coordination enhances threat detection probability by 32% compared to single-unit operations. Emerging hybrid-electric propulsion extends underwater endurance by nearly 40%. More than 45% of next-generation naval R&D programs are integrating swarm intelligence frameworks. These advancements create new opportunities in anti-submarine warfare, mine countermeasures, and environmental monitoring applications.

Over 65% of naval systems rely on satellite-based communication networks, increasing exposure to cyber threats. Encryption upgrades raise operational budgets by nearly 12%. Secure data relay latency issues can impact real-time mission coordination by up to 15%. Additionally, the complexity of safeguarding AI-driven autonomous decision systems requires advanced threat-detection infrastructure, increasing integration timelines and compliance obligations for defense contractors.

Expansion of AI-Driven Autonomous Navigation: Over 68% of newly deployed stealth maritime drones in 2025 feature AI-based route optimization, improving mission accuracy by 30% and reducing fuel consumption by 18%.

Hybrid-Electric Propulsion Adoption: Nearly 42% of new unmanned surface vehicle programs incorporate hybrid-electric systems, extending endurance by 35% and reducing acoustic signatures by 22%.

Swarm Intelligence Integration: More than 33% of naval R&D projects are testing coordinated drone swarms capable of expanding coverage radius by 50% per mission cycle.

Advanced Composite Stealth Materials: Around 55% of new production models utilize radar-absorbing composites that decrease radar cross-section by up to 40%, improving survivability in contested maritime zones.

The Stealth Maritime Defense Drone Systems Market is segmented by type, application, and end-user, reflecting diverse operational and strategic defense requirements. Unmanned Surface Vehicles (USVs) and Autonomous Underwater Vehicles (AUVs) dominate system deployments due to their flexibility in ISR, mine countermeasure, and anti-submarine missions. Applications span naval defense, coastal surveillance, infrastructure protection, and maritime intelligence. End-users primarily include naval forces, coast guards, and defense contractors, with growing adoption among homeland security agencies. Technology-driven procurement strategies emphasize AI integration, stealth optimization, and long-endurance capabilities across all segments.

Unmanned Surface Vehicles (USVs) account for approximately 44% of system deployments due to their versatility in ISR and patrol missions, while Autonomous Underwater Vehicles (AUVs) hold around 38% owing to strong demand in anti-submarine and mine countermeasure operations. However, hybrid surface-underwater stealth drones are rising fastest, expected to grow at a CAGR of 12% through 2033 due to multi-mission adaptability. Remaining segments, including remotely operated stealth vessels and semi-autonomous patrol crafts, collectively contribute nearly 18% of the market. AUV adoption is expanding rapidly as underwater threat detection needs grow, with endurance improvements of 40% achieved through lithium-ion battery advancements. USVs remain the preferred option for long-duration maritime border patrol missions exceeding 72 hours. Hybrid drones combining surface and subsurface capability enhance tactical flexibility by nearly 35% compared to single-mode platforms.

Intelligence, Surveillance, and Reconnaissance (ISR) leads with nearly 46% share, followed by mine countermeasure operations at 22%. Anti-submarine warfare applications are growing fastest, projected at 13% CAGR due to increasing underwater threat detection requirements. Infrastructure monitoring and maritime border security collectively account for about 32% of demand. In 2025, more than 52% of naval modernization programs globally prioritized ISR drone deployment. Approximately 38% of maritime security agencies reported piloting stealth drone systems for offshore asset protection. Increased geopolitical tensions are accelerating anti-submarine drone procurement cycles by nearly 20% compared to pre-2022 levels.

Naval defense forces represent around 62% of total deployments, while coast guards account for 21% and homeland security agencies contribute 11%. Private defense contractors and research institutions collectively hold 6%. However, coast guard adoption is growing fastest at 11% CAGR due to expanding coastal surveillance mandates. Over 58% of naval fleets worldwide are integrating autonomous maritime modules into new shipbuilding programs. In 2025, nearly 41% of coast guard agencies globally reported testing stealth-enabled unmanned patrol systems for illegal trafficking monitoring. Growing offshore energy installations further encourage adoption among maritime security authorities.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of11.8% between 2026 and 2033.

North America deployed more than 180 active stealth-capable unmanned maritime platforms across naval and coast guard operations in 2025, supported by defense budgets exceeding USD 850 billion. Europe held approximately 27% market share, driven by multinational naval modernization programs across Germany, the UK, and France, collectively operating over 90 unmanned maritime assets. Asia-Pacific represented 24% share, with China, India, Japan, and South Korea increasing combined naval unmanned procurement volumes by over 35% since 2022. The Middle East & Africa contributed 6%, primarily through offshore infrastructure protection programs, while South America accounted for 4%, led by Brazil’s coastal surveillance expansion initiatives covering more than 7,400 km of shoreline.

North America represents approximately 39% of global deployment volume, with strong demand from naval defense, homeland security, and offshore infrastructure monitoring sectors. The United States operates over 150 unmanned maritime vehicles, with nearly 60% incorporating stealth composites and AI navigation systems. Regulatory frameworks under the U.S. Department of Defense emphasize cybersecurity compliance, encrypted communications, and autonomous operational safety standards. Canada is investing in Arctic maritime surveillance, expanding unmanned patrol coverage by 25% since 2023. Technological advancements include hybrid-electric propulsion systems improving endurance by 35% and AI-enabled predictive maintenance reducing operational downtime by 28%. A notable player, Huntington Ingalls Industries, expanded production of large unmanned surface vessels in 2024, increasing autonomous vessel endurance beyond 90 days per mission cycle. Enterprise-level adoption in defense-related industries is significantly higher compared to other regions, reflecting strong government procurement behavior and long-term modernization budgets.

Europe holds nearly 27% of global market share, driven by coordinated defense programs among Germany, the United Kingdom, France, and Italy. The region operates more than 90 stealth-enabled maritime drones, with investments increasing by over 20% since 2022 under joint naval defense initiatives. The European Defence Agency promotes interoperability standards for autonomous maritime systems, while sustainability mandates require low-emission propulsion integration in nearly 40% of new defense tenders. Advanced sonar-avoidance materials and AI-based navigation systems are being integrated across next-generation unmanned underwater vehicles. Thales Group expanded autonomous mine countermeasure drone testing in 2025, improving detection efficiency by 30% in joint maritime drills. Regional procurement behavior reflects strong regulatory oversight, emphasizing explainable AI decision systems and cross-border interoperability for NATO-aligned operations.

Asia-Pacific ranks third in overall volume but is the fastest-growing regional market. It accounts for approximately 24% of global deployments, with China, India, Japan, and South Korea leading procurement activities. China has expanded unmanned maritime production capacity by nearly 30% since 2022, while India increased naval unmanned trials by over 40% between 2023 and 2025. Japan integrates stealth underwater drones for deep-sea monitoring exceeding 1,000 meters operational depth. Regional manufacturing hubs emphasize cost-efficient composite materials, reducing production costs by nearly 18% compared to Western counterparts. Mitsubishi Heavy Industries has advanced autonomous underwater vehicle development with endurance exceeding 72 hours continuous submerged operations. Consumer adoption patterns in the region reflect government-driven procurement rather than private defense participation, with rapid technology localization trends across key naval economies.

South America accounts for roughly 4% of global market share, led by Brazil and Argentina. Brazil operates unmanned maritime systems across more than 7,400 km of coastline, supporting offshore oil & gas asset protection. Regional energy infrastructure investments have grown by over 15% annually, increasing surveillance needs for subsea pipelines and offshore rigs. Government-backed modernization programs focus on maritime border control and anti-smuggling operations. Brazil’s naval research institutions have expanded autonomous patrol testing zones by 20% since 2023. Trade policies encouraging domestic defense manufacturing provide import substitution benefits. Regional procurement behavior ties closely to energy sector protection, reflecting a targeted rather than large-scale fleet expansion approach.

The Middle East & Africa region contributes approximately 6% of global deployment volume, driven by offshore oil & gas security and maritime chokepoint surveillance. The UAE and Saudi Arabia are investing in smart naval bases integrating autonomous patrol drones, while South Africa is enhancing coastal monitoring coverage by 18% since 2022. Hybrid-electric propulsion systems are gaining traction, reducing fuel usage by nearly 20% in long-endurance patrol missions. Regional modernization programs emphasize AI-driven surveillance and encrypted satellite communications. The UAE has launched autonomous maritime testing corridors covering over 1,000 square kilometers of coastal waters. Procurement behavior centers on infrastructure protection and strategic maritime corridor monitoring.

United States – 34% Market Share: Strong naval production capacity, over 150 active unmanned maritime systems, and sustained defense modernization programs drive leadership.

China – 18% Market Share: Rapid indigenous manufacturing expansion, 30% increase in unmanned maritime production since 2022, and strong naval fleet growth support dominance.

The Stealth Maritime Defense Drone Systems Market demonstrates a moderately consolidated competitive structure, with the top five companies accounting for approximately 58% of total global deployments. More than 25 active defense contractors and maritime technology firms compete across unmanned surface vehicles (USVs), autonomous underwater vehicles (AUVs), and hybrid stealth systems.

Strategic initiatives include partnerships between naval agencies and technology firms to accelerate AI-enabled navigation, sonar-avoidance composites, and swarm intelligence integration. Between 2023 and 2025, over 18 new stealth maritime drone models were introduced globally. Approximately 40% of competitive differentiation is based on endurance performance exceeding 72 hours, while 30% focuses on acoustic signature reduction technologies.

Mergers and joint ventures are increasing, particularly in Europe and Asia-Pacific, to enhance cross-border interoperability. Companies are allocating nearly 15–20% of defense R&D budgets toward autonomous maritime platforms. Competitive positioning is increasingly defined by hybrid propulsion efficiency, cybersecurity compliance capabilities, and integration readiness with legacy naval command systems.

BAE Systems

Thales Group

General Dynamics

Huntington Ingalls Industries

L3Harris Technologies

Saab AB

Elbit Systems

Kongsberg Gruppen

Mitsubishi Heavy Industries

Israel Aerospace Industries

Leonardo S.p.A.

Textron Systems

Damen Shipyards Group

Technological evolution in the Stealth Maritime Defense Drone Systems Market centers on AI-driven autonomy, advanced composite stealth materials, secure communications, and hybrid propulsion systems. Over 68% of newly developed platforms incorporate machine-learning-based navigation algorithms capable of processing more than 1 terabyte of sensor data per mission cycle. Autonomous underwater vehicles now achieve submerged endurance exceeding 96 hours, supported by lithium-ion and solid-state battery innovations that improve energy density by nearly 25%.

Low-observable composite hull materials reduce radar cross-section by up to 40%, while acoustic dampening technologies decrease underwater detection probability by approximately 30%. Satellite-linked encrypted communication systems using quantum-resistant encryption standards are being integrated in nearly 50% of next-generation prototypes.

Swarm intelligence platforms enable coordinated mission deployment of up to 20 unmanned units simultaneously, expanding surveillance coverage by 50–60% per operation. Predictive maintenance powered by AI analytics reduces unexpected component failures by 28%, enhancing fleet availability. Additionally, hybrid-electric propulsion systems decrease fuel dependency by nearly 20%, aligning with defense sustainability goals and long-endurance mission requirements.

• In November 2025, Thales announced delivery of an autonomous surface drone system fitted with advanced towed and multi-view sonar, AI-enabled mission software, and cyber-resilient communication suites designed to significantly improve sea mine detection rates above 99% while reducing personnel exposure to hazardous minefields during operations. This delivery marks a milestone in unmanned maritime capability for mine countermeasure missions. Source: www.thalesgroup.com

• In December 2024, Thales delivers first autonomous drone system for mine countermeasures to the French Navy — the company completed serial production and delivery of its autonomous mine countermeasure surface drones under the Franco-British MMCM programme, featuring AI data analysis, enhanced sensor integration, and mission planning tools for naval operations.

• In October 2025, Lockheed Martin announced a strategic USD 50 million investment in Saildrone to integrate combat-capable systems onto unmanned surface vehicles for the U.S. Navy — this press release details plans to fit Saildrone platforms with Lockheed Martin’s JAGM Quad Launcher and advanced systems for fleet defense, reconnaissance, and undersea surveillance, with live-fire demonstrations expected in 2026.

• In February 2026, BAE Systems announced a memorandum of understanding with Frankenburg Technologies to jointly explore next-generation counter-drone capabilities and integrated systems that enhance maritime and land forces’ resilience against unmanned threats, reflecting industry movement toward integrated defensive tools.

The Stealth Maritime Defense Drone Systems Market Report provides a comprehensive evaluation of unmanned surface vehicles (USVs), autonomous underwater vehicles (AUVs), and hybrid stealth maritime systems deployed across naval defense, coast guard, and homeland security operations. The scope covers more than 25 active producing countries, with detailed segmentation across type, application, and end-user categories.

Geographically, the report analyzes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting over 500 active unmanned maritime deployments worldwide. Application-level analysis includes ISR operations accounting for approximately 46% of deployments, mine countermeasures at 22%, anti-submarine warfare, offshore infrastructure protection, and border security.

Technology coverage spans AI-enabled navigation systems, radar-absorbing composite materials, encrypted satellite communications, swarm intelligence integration, and hybrid-electric propulsion solutions. The report also examines regulatory frameworks, ESG integration initiatives targeting 30% emission reductions, and cybersecurity compliance mandates impacting procurement strategies.

Additionally, the report evaluates competitive positioning across more than 25 global defense contractors, product innovation pipelines, naval modernization programs, and emerging opportunities in swarm-based maritime surveillance. It provides strategic insights for defense agencies, policymakers, and technology investors seeking to align procurement decisions with evolving autonomous maritime defense requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,500.0 Million |

| Market Revenue (2033) | USD 3,215.4 Million |

| CAGR (2026–2033) | 10% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Northrop Grumman; BAE Systems; Thales Group; General Dynamics; Huntington Ingalls Industries; L3Harris Technologies; Saab AB; Elbit Systems; Kongsberg Gruppen; Mitsubishi Heavy Industries; Israel Aerospace Industries; Leonardo S.p.A.; Textron Systems; Damen Shipyards Group |

| Customization & Pricing | Available on Request (10% Customization Free) |