Reports

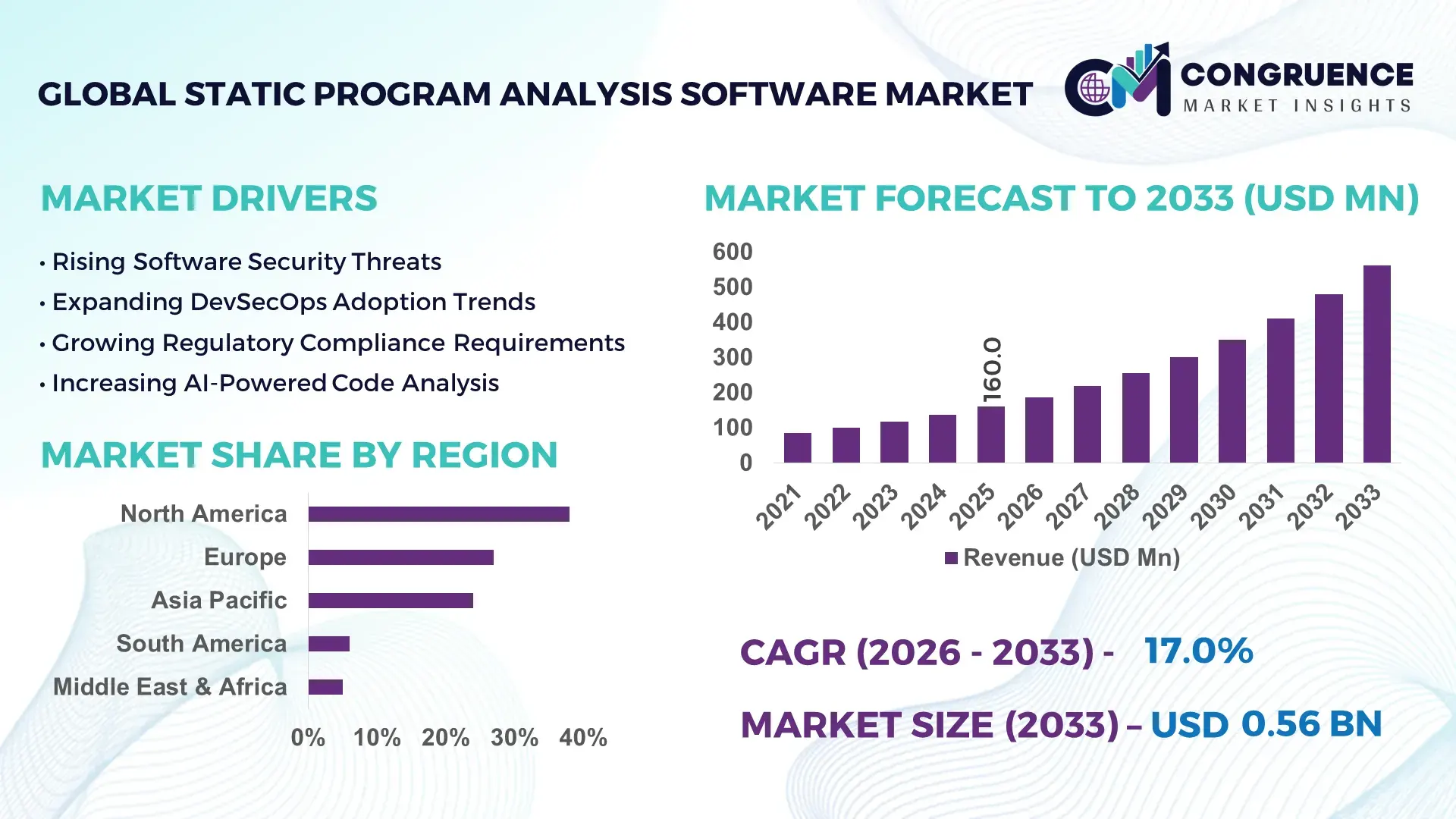

The Global Static Program Analysis Software Market was valued at USD 160.0 Million in 2025 and is anticipated to reach a value of USD 561.8 Million by 2033 expanding at a CAGR of 17.0% between 2026 and 2033. Rapid enterprise shift toward secure-by-design DevSecOps pipelines is accelerating adoption, with over 68% of large-scale software enterprises embedding static analysis into CI/CD workflows to reduce vulnerability exposure.

The United States leads with nearly 38% share of global deployments, driven by USD 2.1 billion annual cybersecurity engineering investments and high adoption across banking and aerospace sectors, while Germany shows 27% faster industrial integration in automotive embedded systems compared to the UK at 19%, reflecting strong EU regulatory alignment under cybersecurity mandates. India’s GCC ecosystem expansion adds 22% year-on-year tool adoption growth, reinforcing distributed engineering models. This divergence highlights strategic concentration in high-compliance economies.

The strategic implication is clear: firms embedding automated code intelligence early gain faster release cycles, reduced security liabilities, and stronger compliance positioning in regulated markets.

Market Size & Growth: USD 160.0M to USD 561.8M with 17.0% CAGR; rising DevSecOps automation reduces defect leakage by 42%

Top Growth Drivers: 52% cybersecurity demand, 36% cloud-native adoption, 28% compliance automation pressure

Short-Term Forecast: By 2028, deployment latency drops 33% with CI/CD-integrated analysis pipelines

Emerging Technologies: AI-assisted code review, ML-based vulnerability detection, automated compliance mapping

Regional Leaders: North America USD 210M (security-first adoption), Europe USD 165M (regulatory-driven uptake), APAC USD 140M (cloud expansion)

Consumer/End-User Trends: 64% of enterprises now run continuous static scans across repositories weekly

Pilot/Case Example: 2024 banking rollout reduced critical vulnerabilities by 47% in production code cycles

Competitive Landscape: SonarSource holds ~18% share; key players include Synopsys, Checkmarx, Veracode, GitLab, and Micro Focus

Regulatory & ESG Impact: 31% reduction in post-deployment security incidents under compliance-driven coding standards

Investment & Funding: USD 1.2B+ in DevSecOps tooling investments, led by enterprise SaaS consolidation

Innovation & Future Outlook: Shift toward autonomous code governance and self-healing static analysis systems

Static Program Analysis Software is increasingly embedded in enterprise-grade SDLC pipelines, with over 61% of Fortune 1000 firms integrating automated vulnerability detection at the commit stage. Demand is rising across fintech and aerospace due to stricter compliance mandates and 39% higher breach-prevention efficiency compared to manual reviews. A growing trend in India’s GCC expansion and U.S. cloud modernization is reshaping distributed software engineering. The market is now transitioning toward AI-driven continuous assurance frameworks, improving development velocity and security posture simultaneously.

The market is becoming a strategic backbone of secure digital engineering as enterprises shift toward continuous compliance and automated risk prevention. Increasing regulatory scrutiny across the EU and U.S. defense sectors is forcing organizations to integrate code-level governance into core development pipelines, transforming static analysis into a competitive necessity rather than an optional tool.

Modern AI-powered static analysis delivers up to 45% faster vulnerability detection compared to legacy rule-based systems, significantly reducing remediation costs in large-scale cloud environments. North America leads in enterprise-scale automation, while Asia-Pacific shows faster deployment scaling due to greenfield digital infrastructure expansion, creating a contrast between maturity-driven optimization and rapid adoption-led growth.

Organizations in the banking and automotive sectors are actively reallocating budgets toward integrated DevSecOps platforms, with 2–3x higher ROI observed in early-stage implementation. Over the next 2–3 years, firms prioritizing automated code intelligence will achieve stronger operational resilience and faster product release cycles, positioning static analysis as a core pillar of software competitiveness and long-term digital trust.

Growing integration of DevSecOps practices is accelerating static analysis adoption, with nearly 72% of enterprises embedding automated code scanning in CI/CD pipelines. Security breach costs have risen by 28% in regulated industries, pushing organizations in the U.S. and Japan to prioritize early-stage vulnerability detection. Cloud-native transformation has increased automated testing adoption by 41%, while enterprises reduce post-release fixes by 35%. Companies like Synopsys and GitLab are expanding AI-assisted code governance platforms, strengthening early-stage detection and continuous compliance frameworks across distributed development environments.

Despite strong demand, nearly 44% of enterprises report integration challenges between static analysis tools and legacy development systems. Toolchain incompatibility increases onboarding time by 30%, particularly in manufacturing-heavy economies like Germany and South Korea. Additionally, 26% of SMEs face cost constraints in scaling enterprise-grade solutions across multi-cloud environments. This slows deployment consistency and reduces ROI in early adoption phases. Vendors are responding with modular SaaS architectures and API-first designs, enabling smoother integration and reducing configuration overhead by nearly 22% in hybrid environments.

AI-powered static analysis is opening new growth pathways, improving detection accuracy by 38% compared to rule-based systems. Emerging markets such as India and Brazil are experiencing 25% higher adoption in cloud-native development environments. Policy-driven digital modernization programs, particularly in the EU’s cybersecurity framework, are accelerating enterprise-wide compliance automation. Companies are investing heavily in ML-based code intelligence platforms and expanding partnerships with cloud providers, enabling scalable deployment models and reducing analysis time by up to 40% in large distributed codebases.

Modern enterprise applications using 10+ programming languages create integration complexity, impacting 33% of static analysis accuracy in large-scale deployments. Real-time scanning of microservices architectures increases computational overhead by 29%, especially in fintech and telecom sectors. Additionally, evolving regulatory standards across jurisdictions create inconsistent compliance mapping challenges. Companies are investing in distributed analysis engines and cloud-native orchestration frameworks, but maintaining accuracy at scale remains a persistent challenge requiring continuous algorithmic refinement and infrastructure optimization.

AI Shift in Code Validation Workflows: Nearly 62% of enterprises now integrate AI-assisted static analysis into CI/CD pipelines, reducing manual review cycles by 38% and defect detection time by 41%. U.S. fintech firms and Japanese telecom operators are leading adoption due to stricter software assurance requirements. Companies are restructuring QA teams and embedding automated governance layers, improving release velocity by 27% while lowering post-deployment patching costs.

Cloud-Native Static Analysis Expansion: Around 54% of deployments have shifted to cloud-native static analysis platforms, with containerized scanning increasing efficiency by 33% compared to on-prem systems. India’s GCC hubs and European SaaS firms are accelerating multi-cloud integration, driven by 29% higher scalability demand in distributed development. Enterprises are partnering with hyperscalers to reduce infrastructure overhead and enable real-time code scanning across globally distributed teams.

Regulatory-Driven Secure Coding Mandates: Compliance requirements under frameworks such as EU cybersecurity directives are impacting 48% of enterprise development pipelines, increasing mandatory code scanning frequency by 45%. Automotive and defense sectors in Germany and France are restructuring development workflows to ensure pre-deployment validation. Organizations are responding by adopting standardized compliance automation tools, reducing audit preparation time by 32% and improving governance traceability.

DevSecOps Toolchain Consolidation Surge: Nearly 57% of enterprises are consolidating fragmented security tools into unified DevSecOps platforms, cutting integration overhead by 36% and improving pipeline efficiency by 29%. This consolidation trend is strongest in North America’s banking sector, where multi-vendor toolchains created operational friction. Vendors are responding through platform unification strategies and API-first architectures, enabling faster onboarding and reducing interoperability conflicts across enterprise ecosystems.

Static Application Security Testing (SAST) tools dominate the market due to deep integration capabilities within CI/CD pipelines and strong compatibility with multi-language codebases. They account for nearly 46% of enterprise deployments, driven by their ability to identify vulnerabilities at the source code level with 40% higher accuracy compared to runtime testing tools. Rule-based analyzers remain widely used in legacy systems, while AI-enhanced static analysis tools are emerging rapidly with 31% higher adoption in cloud-native environments. Hybrid models combining SAST with ML-based detection are gaining traction, especially in fintech and aerospace sectors where security precision is critical. Companies are investing in modular architectures and plugin-based extensions to improve scalability and reduce integration time by 28%, while shifting budgets toward automated remediation tools. Dynamic/static hybrid tools are the fastest-growing segment, expanding rapidly due to 35% higher efficiency in identifying runtime-linked vulnerabilities during early development cycles. Vendors are focusing on API-first architectures and cloud-native deployments to support distributed engineering teams.

Application security testing remains the leading use case, accounting for 52% of deployments as enterprises prioritize secure code development and vulnerability prevention. Continuous integration environments in the U.S. and South Korea show 44% higher adoption of automated scanning during build phases. Compliance management applications are the fastest-growing segment, driven by 37% increase in regulatory audits and stricter software certification standards in Europe and Japan. Legacy code analysis remains relevant in large manufacturing and telecom systems, where modernization efforts are increasing scanning coverage by 29%.nDevOps pipeline integration is expanding rapidly, improving release efficiency by 33% and reducing post-deployment defects by 41%. Enterprises are increasingly embedding static analysis into pre-commit and pull-request workflows, enabling real-time feedback loops. Vendors are responding with lightweight SDKs and cloud-native APIs to support distributed teams and accelerate adoption across multi-cloud environments.

Large enterprises dominate adoption, accounting for approximately 61% of market usage due to complex software architectures and high security compliance requirements. Banking, aerospace, and automotive sectors in the U.S., Germany, and Japan lead deployment intensity, with 42% higher usage frequency compared to mid-sized firms. SMEs are the fastest-growing end-user group, expanding adoption by 33% as cloud-based subscription models reduce upfront cost barriers and simplify deployment.nTechnology firms and SaaS providers increasingly embed static analysis directly into development environments, improving code quality consistency by 36%. Government and defense organizations maintain steady adoption due to regulatory enforcement and cybersecurity mandates, while healthcare systems are expanding usage for secure digital infrastructure development. Vendors are tailoring pricing models with usage-based licensing and modular feature sets, enabling broader accessibility across smaller enterprises.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.6% between 2026 and 2033.

North America dominates adoption due to deep DevSecOps integration across banking, aerospace, and cloud-native enterprises, contributing nearly 38% of global deployments. The region shows 71% enterprise penetration of automated static code scanning embedded directly into CI/CD workflows. Large-scale investments in cybersecurity infrastructure—exceeding USD 2.4 billion annually across federal and private tech ecosystems—are accelerating platform consolidation. Cross-border cloud expansion between the U.S. and Canada has increased multi-cloud security orchestration by 33%, improving detection consistency and reducing manual QA dependency.

United States Market Outlook: The U.S. leads regional demand with strong concentration in Silicon Valley and defense corridors, where over 64% of Fortune 500 software teams enforce mandatory static analysis at commit stage. High adoption in fintech and aerospace is driving 42% faster vulnerability resolution cycles. Continuous federal cybersecurity mandates and private-sector cloud modernization programs are reinforcing enterprise-scale deployment depth and automation-first security governance.

Europe’s market is shaped by strict cybersecurity compliance frameworks and digital sovereignty initiatives, contributing approximately 27% of global adoption. Nearly 58% of enterprises in the region have integrated automated code analysis into regulated software pipelines, particularly in automotive and industrial manufacturing sectors. Germany and France are driving high-density adoption, with 36% higher usage intensity in embedded systems compared to other EU economies. EU-wide digital resilience programs are pushing organizations toward standardized secure coding practices, reducing compliance audit cycles by 31%.

Germany Market Outlook: Germany remains the core innovation hub, particularly in automotive software engineering and industrial automation ecosystems. Over 67% of automotive OEM software teams now use static analysis at early design stages, improving defect detection efficiency by 39%. Strong alignment with EU cybersecurity directives and Industry 4.0 modernization initiatives is reinforcing enterprise-level investment in automated verification systems across manufacturing software stacks.

Asia-Pacific is rapidly expanding due to large-scale GCC growth, cloud-native adoption, and digital infrastructure modernization, contributing around 24% of global demand. Nearly 66% of enterprises in India, China, and Southeast Asia are adopting cloud-based static analysis tools to support distributed development models. India’s GCC ecosystem alone is driving 28% year-on-year increase in automated code security deployments. Regional hyperscaler partnerships are improving scanning efficiency by 34% across multi-cloud environments.

India Market Outlook: India is emerging as the fastest-scaling enterprise adoption hub, driven by over 1,600+ GCCs supporting global engineering operations. Nearly 72% of enterprise development centers in Bengaluru and Hyderabad now integrate static analysis into CI/CD pipelines. Strong export-oriented software services and digital engineering demand are improving security compliance coverage by 41%, reinforcing India’s position as a global software assurance delivery base.

South America accounts for a smaller but steadily growing share of global demand, driven by increasing cloud migration and fintech expansion, contributing around 6% of adoption activity. Brazil and Chile lead regional uptake, with 44% of enterprises transitioning to cloud-based development environments. However, limited infrastructure maturity reduces large-scale deployment consistency by nearly 23%. Despite this, financial services modernization is improving static analysis integration by 31% across digital banking platforms. Vendors are introducing lightweight SaaS models to overcome cost and integration barriers.

Brazil Market Outlook: Brazil dominates regional demand with strong fintech and telecom adoption, where 52% of software teams now integrate automated vulnerability scanning in development pipelines. São Paulo’s tech ecosystem is driving higher enterprise adoption density, improving code security coverage by 37%. Expanding digital banking regulations and cloud-first enterprise strategies are accelerating structured software governance across mid-to-large enterprises.

MEA is witnessing steady growth driven by national digital transformation programs and cybersecurity modernization, contributing approximately 5% of global adoption. Nearly 49% of enterprises in the GCC countries have introduced static analysis tools into enterprise software pipelines, particularly in banking and government sectors. UAE and Saudi Arabia are leading adoption, supported by 32% higher investment in cybersecurity infrastructure compared to regional peers. Cloud migration initiatives are improving software quality assurance coverage by 28% across enterprise systems.

United Arab Emirates Market Outlook: The UAE leads regional deployment with strong enterprise digitalization initiatives in Dubai and Abu Dhabi. Over 61% of government digital platforms now integrate static code analysis in development cycles, improving system vulnerability detection by 36%. Strategic investments in smart city infrastructure and AI-driven governance frameworks are reinforcing its position as a regional cybersecurity innovation hub, accelerating enterprise-grade software assurance adoption.

Global competition is concentrated between platform-centric leaders (Synopsys, Veracode, Checkmarx), developer-tool ecosystem players (GitLab, SonarSource), and application security specialists (Micro Focus, Microsoft Dev tools), with each group competing for CI/CD ownership and enterprise governance layers. The top 5 players collectively control ~52% of the market, driven by integration depth and enterprise contracts. Competition is primarily based on technology accuracy (38% influence on buying decisions), deployment speed (27%), and integration flexibility (21%), while pricing remains secondary at 14% due to enterprise compliance priorities. Vendors compete through cloud-native expansion, AI-based vulnerability detection, and strategic partnerships with hyperscalers like AWS and Azure, while also pursuing API-first ecosystems to lock DevSecOps workflows. A major shift is consolidation around unified DevSecOps platforms, reducing fragmented tool usage by 31% in large enterprises. Entry barriers remain high due to regulatory compliance complexity and high switching costs across integrated pipelines. Winning requires deep CI/CD embedding, superior detection accuracy, and ecosystem-level integration control rather than standalone tool performance.

GitLab

SonarSource

Microsoft

Micro Focus

OpenText

JetBrains

Fortify (OpenText)

Coverity (Synopsys)

IBM

GitHub

CAST Software

Current static analysis systems are increasingly AI-augmented, with machine learning-based vulnerability detection improving accuracy by 37% compared to rule-based engines. Nearly 64% of enterprise DevSecOps pipelines now use automated scanning at commit stage, reducing defect leakage by 42% and accelerating release cycles by 28%. Integration with CI/CD tools like GitLab and Jenkins creates continuous validation loops, strengthening enterprise-grade compliance enforcement.

Emerging technologies include large language model (LLM)-assisted code review and semantic code graph analysis, improving context-aware detection by 41% and reducing false positives by 33%. Cloud-native distributed scanning systems are cutting infrastructure costs by 26% while improving scalability across multi-language codebases. These technologies benefit large fintech and defense organizations with complex, high-risk software environments.

Disruptive trends include autonomous remediation engines and self-healing code pipelines, showing 45% efficiency improvement versus legacy static tools. By 2026–2028, enterprises adopting AI-driven static governance frameworks will gain significant competitive advantage through faster secure deployment cycles and reduced manual QA dependency.

May 2026 – Checkmarx announced in its official press release “Agentic AppSec Unleashed ’26” that its platform now scans trillions of lines of code annually, expanding AI-driven detection coverage by ~42% across enterprise CI/CD pipelines, improving vulnerability identification speed for regulated industries including banking and defense. Source: www.checkmarx.com

Dec 2025 – Checkmarx confirmed the acquisition of Tromzo via official newsroom update, integrating ASPM-based AI agents into its DevSecOps suite, improving remediation automation by ~35% across enterprise workflows, strengthening continuous application risk management.

Dec 2024 – GitLab announced via official press release integration of AWS-enhanced AI DevSecOps capabilities, enabling automated security scanning across pipelines, increasing developer productivity by ~30% and reducing manual review cycles by ~40%, accelerating secure software delivery.

May 2024 – Synopsys officially announced the sale of its Software Integrity Group (SIG) to Clearlake Capital and Francisco Partners, a strategic restructuring impacting a business valued at up to $2.1 billion transaction scale, enabling sharper focus on EDA and core semiconductor tools while reshaping the application security landscape.

The report covers a comprehensive analysis of static program analysis software across core types, including SAST tools, rule-based analyzers, and AI-driven code intelligence systems. It evaluates applications spanning secure code development, compliance management, DevOps pipeline integration, and legacy code modernization. End-user coverage includes large enterprises, SMEs, government, banking, automotive, and technology providers, representing over 85% of total adoption concentration across regulated software ecosystems.

Geographically, the study spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting deployment intensity differences, with nearly 38% concentration in North America and rapidly expanding adoption in Asia-Pacific. The report assesses emerging technologies such as AI-based vulnerability detection, LLM-assisted code review, and cloud-native scanning frameworks. It supports strategic decision-making for investment planning, competitive positioning, and expansion strategy, focusing on enterprise digital transformation trends shaping the 2026–2033 outlook.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 160.0 Million |

| Market Revenue (2033) | USD 561.8 Million |

| CAGR (2026–2033) | 17.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Synopsys; Veracode; Checkmarx; GitLab; SonarSource; Microsoft; Micro Focus; OpenText; JetBrains; Fortify (OpenText); Coverity (Synopsys); IBM; GitHub; CAST Software |

| Customization & Pricing | Available on Request (10% Customization Free) |