Reports

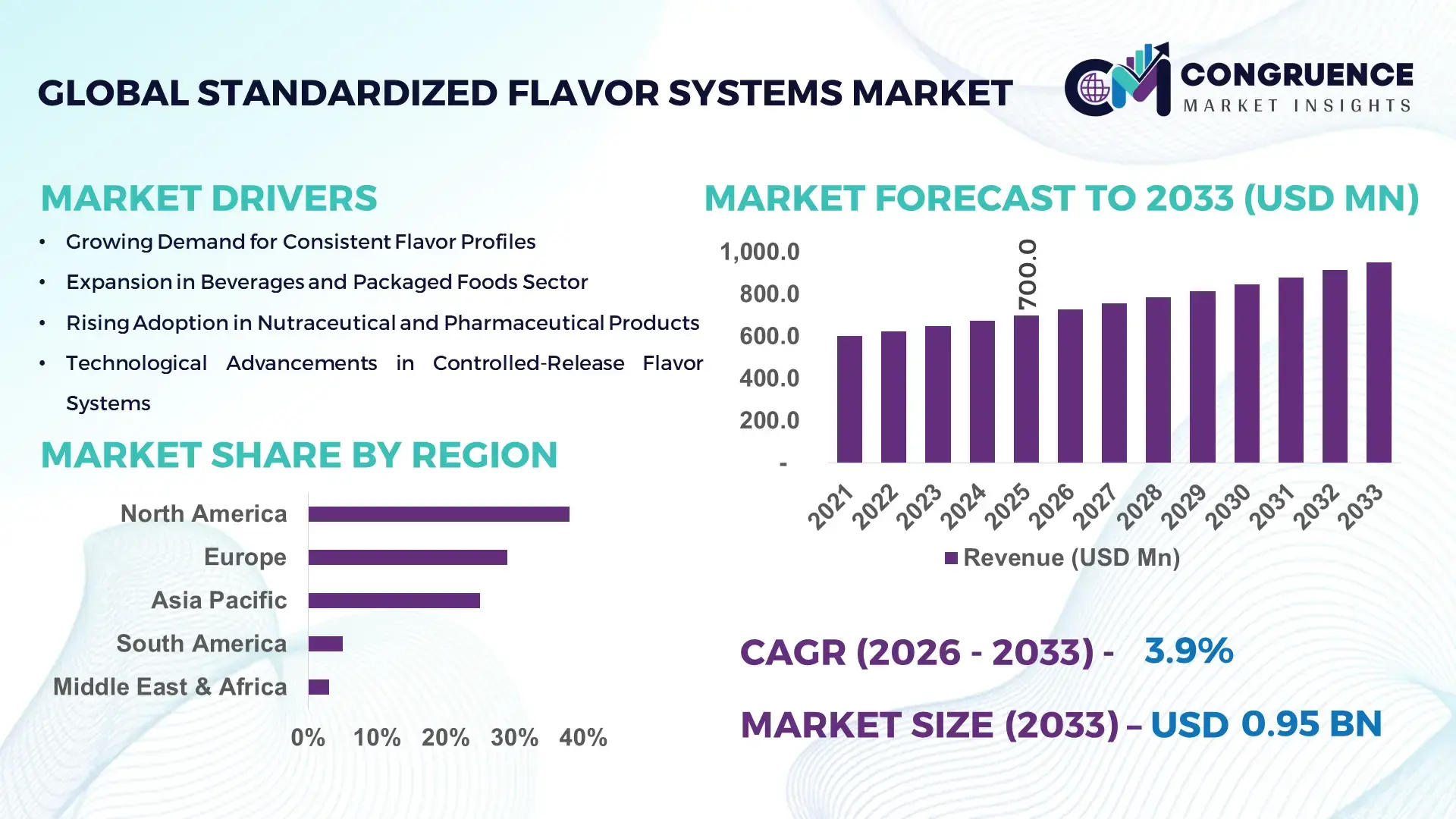

The Global Standardized Flavor Systems Market was valued at USD 700.0 Million in 2025 and is anticipated to reach a value of USD 950.7 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the rising demand for consistent taste profiles across packaged foods, beverages, and pharmaceutical formulations.

The United States dominates the Standardized Flavor Systems Market through its large-scale production infrastructure and sustained industrial investment. In 2025, the U.S. hosted more than 1,200 industrial flavor manufacturing facilities, with an estimated annual production capacity exceeding 2.5 million metric tons of liquid and dry flavor formulations. Private and corporate investments in food ingredient R&D surpassed USD 4.8 billion, supporting advanced encapsulation, spray-drying, and controlled-release technologies. Standardized flavor systems are extensively deployed across beverages (32%), dairy and bakery (28%), and pharmaceuticals and nutraceuticals (19%). Automation penetration in U.S. flavor blending lines exceeds 65%, while digital batch control systems are used in over 58% of large-scale facilities, improving batch consistency and regulatory traceability.

Market Size & Growth: USD 700.0 Million in 2025, projected to reach USD 950.7 Million by 2033, growing at 3.9% CAGR due to rising packaged food standardization.

Top Growth Drivers: Processed food adoption +42%, beverage product launches +36%, pharmaceutical excipient usage +29%.

Short-Term Forecast: By 2028, batch consistency errors are expected to decline by 18% through automated dosing systems.

Emerging Technologies: Microencapsulation systems, AI-based flavor profiling, continuous inline blending platforms.

Regional Leaders: North America USD 310 Million, Europe USD 265 Million, Asia Pacific USD 290 Million by 2033 with rapid clean-label adoption in Asia.

Consumer/End-User Trends: 61% of food manufacturers prefer standardized over customized flavor systems for scalability.

Pilot or Case Example: In 2024, a German beverage plant improved formulation accuracy by 21% using inline digital dosing.

Competitive Landscape: Market leader holds ~18% share, followed by 4 global players each between 7–11%.

Regulatory & ESG Impact: Over 47% of producers now comply with low-solvent and allergen-free formulation mandates.

Investment & Funding Patterns: More than USD 2.1 Billion invested globally in flavor production automation since 2022.

Innovation & Future Outlook: Integration of AI sensory modeling and digital twins will shape next-generation flavor standardization.

The Standardized Flavor Systems Market serves food and beverage (52%), pharmaceuticals (21%), nutraceuticals (14%), and personal care (9%). Recent innovations include solvent-free spray-drying, controlled-release encapsulation, and allergen-free carrier systems. Regulatory pressure on labeling, environmental solvent reduction, and regional taste harmonization is shaping adoption. Asia Pacific shows the fastest consumption growth, while Europe leads in regulatory-driven reformulation trends.

The Standardized Flavor Systems Market plays a strategic role in ensuring formulation consistency, regulatory compliance, and scalable production across food, beverage, and pharmaceutical industries. Standardized systems reduce formulation variability by 22–30% compared to manual blending methods, enabling manufacturers to maintain uniform sensory profiles across multi-plant operations. Advanced microencapsulation technology delivers 25% improvement in flavor stability compared to conventional spray drying standards.

North America dominates in production volume, while Asia Pacific leads in adoption with 48% of new beverage manufacturers deploying standardized flavor platforms. By 2028, AI-driven flavor modeling is expected to cut product development cycles by 19%, improving time-to-market for functional beverages and nutraceuticals. Firms are committing to ESG improvements such as 30% solvent reduction by 2030 and increased use of biodegradable carriers.

In 2024, a Japanese food processor achieved 17% batch rejection reduction through digital dosing and inline quality monitoring. Looking forward, the Standardized Flavor Systems Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable formulation growth across global ingredient supply chains.

The Standardized Flavor Systems Market is shaped by rising industrial food processing, expanding pharmaceutical excipient usage, and stricter regulatory requirements for formulation consistency. Large-scale manufacturers increasingly rely on pre-defined flavor matrices to reduce formulation errors, improve audit traceability, and shorten development cycles. Automation, digital batch control, and modular blending platforms are restructuring production economics. Regional harmonization of taste profiles for global brands further accelerates demand, while sustainability mandates drive solvent-free and allergen-free system adoption across major production hubs.

The expansion of processed food manufacturing directly increases demand for standardized flavor systems. In 2025, packaged food consumption accounted for over 58% of urban dietary intake in developed economies. More than 63% of multinational food producers now require identical taste profiles across at least five production regions. Automated dosing systems reduce batch deviation rates by 24%, lowering rework and compliance risk. Beverage manufacturers report 31% reduction in sensory variation after shifting from custom blending to standardized platforms, making industrial scalability a primary growth driver.

Regulatory fragmentation limits cross-border deployment of standardized formulations. More than 120 country-specific food additive and excipient regulations govern flavor system composition. Reformulation costs increase by 15–22% when entering new regulatory markets. Allergen labeling mandates affect over 38% of existing flavor formulations, requiring costly reformulation and retesting. Smaller manufacturers face compliance delays averaging 9–14 months, slowing standardized system adoption despite operational advantages.

Pharmaceutical and nutraceutical usage of standardized flavor systems is expanding rapidly. In 2025, flavored oral formulations represented 41% of pediatric and geriatric medicines. Encapsulated flavor carriers improve taste masking efficiency by 27% and shelf stability by 19%. Nutraceutical beverage launches increased 34% year-over-year, creating demand for low-calorie and clean-label standardized systems. Regulatory-grade flavor excipients now account for over 20% of new system development pipelines, opening long-term institutional supply opportunities.

Raw material price volatility impacts production planning and contract stability. Natural flavor compound prices fluctuated by 18–25% between 2023 and 2025. Citrus oil shortages reduced supply availability by 14%, disrupting standardized formulations. Long-term contracts now require average buffer inventory increases of 22%, raising working capital pressure. Transportation disruptions further increase lead times by 11–16%, challenging just-in-time flavor system deployment.

Expansion of Modular Flavor Manufacturing Lines: Over 49% of new flavor production plants now deploy modular blending and dosing units, reducing plant commissioning time by 32% and lowering labor dependency by 27% across Europe and North America.

Adoption of AI-Based Sensory Modeling: AI-assisted flavor profiling platforms are used by 36% of Tier-1 manufacturers, improving sensory prediction accuracy by 21% and reducing trial batches by 18%.

Growth of Clean-Label Standardized Systems: Clean-label flavor systems now represent 44% of new product launches, with solvent-free carriers reducing residual chemical content by 35% and improving regulatory acceptance.

Digital Traceability and Inline Quality Control: Inline NIR and mass-flow monitoring systems are deployed in 58% of large facilities, cutting batch rejection rates by 23% and improving audit traceability by 29%.

The Standardized Flavor Systems Market is segmented by type, application, and end-user, reflecting diverse formulation requirements across food, beverage, pharmaceutical, and personal care industries. By type, liquid, powder, and encapsulated systems dominate industrial usage due to their scalability, stability, and dosing precision. Application-wise, beverages and packaged foods account for the highest utilization, driven by high-volume production and strict batch-to-batch consistency requirements. Pharmaceutical and nutraceutical applications are expanding steadily as taste masking and controlled release become critical formulation parameters. End-user segmentation highlights multinational food processors, beverage bottlers, and pharmaceutical manufacturers as the primary adopters, supported by increasing automation penetration and regulatory compliance needs. Across all segments, adoption is shaped by traceability mandates, allergen management, and clean-label reformulation trends, making segmentation a core determinant of technology deployment and investment priorities.

Liquid standardized flavor systems currently account for 46% of total adoption, supported by their high solubility, rapid dispersion, and suitability for beverages and syrups. Powder-based systems represent 31%, widely used in bakery, snacks, and dry mixes due to extended shelf life and ease of transport. Encapsulated and controlled-release systems hold 14%, but adoption in this segment is rising fastest, expected to surpass 22% by 2033, driven by demand for taste masking and functional ingredient protection in pharmaceuticals and nutraceuticals. Encapsulation is the fastest-growing type, supported by increasing use of microencapsulation and spray-chilling technologies, with growth exceeding 6.1% annually due to regulatory-grade formulation needs.

Other niche formats, including paste and gel-based systems, contribute a combined 9%, serving specialized confectionery and dairy applications where texture integration is critical.

• In 2025, a national food safety authority validated controlled-release flavor capsules for pediatric syrups, enabling stable taste masking across more than 12 million annual medicine doses.

Beverages remain the leading application segment, accounting for 34% of total adoption, as carbonated drinks, flavored waters, and functional beverages require tight sensory standardization across global bottling networks. Packaged and processed foods follow with 29%, including bakery, snacks, and ready meals. However, pharmaceutical formulations are the fastest-growing application, with adoption rising at 5.8% annually, expected to exceed 20% of total usage by 2033, driven by pediatric, geriatric, and nutraceutical dosage forms.

Other applications such as personal care, oral hygiene, and dietary supplements collectively contribute 17%, reflecting growing sensory differentiation in non-food products.

In 2025, more than 41% of pharmaceutical manufacturers reported deploying standardized flavor systems for oral liquids and chewables. Over 57% of beverage brands now use pre-validated flavor matrices to ensure cross-plant consistency.

• In 2024, a public health research institute reported standardized flavor platforms deployed in over 180 hospitals to improve patient compliance in liquid medicines.

Multinational food and beverage manufacturers lead the end-user landscape with 48% of total adoption, supported by multi-plant operations and stringent consistency requirements. Pharmaceutical companies represent 27%, driven by regulatory-grade taste masking and formulation stability. Contract manufacturers and private-label producers account for 15%, while personal care and nutraceutical specialists contribute the remaining 10%.

Pharmaceutical end-users are the fastest-growing segment, expanding at 5.6% annually, as flavored oral dosage forms increase in pediatric and chronic therapies. Food processors continue to prioritize automation, with 62% of Tier-1 manufacturers using digital dosing and batch control systems in 2025.

In 2025, more than 39% of global food enterprises reported migrating from custom blending to standardized platforms. In the US, 44% of pharmaceutical plants now use encapsulated flavor excipients for controlled-release formulations.

• In 2025, a national medicines regulatory agency documented standardized flavor systems deployed across 520 licensed drug manufacturing facilities to improve dosage uniformity and patient adherence.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

North America’s leadership is supported by over 1,200 industrial flavor manufacturing units, high automation penetration above 65%, and strong pharmaceutical usage. Europe follows with 29% share, driven by regulatory-led reformulation and clean-label mandates across more than 450 certified ingredient facilities. Asia-Pacific contributes 25% of global demand, supported by more than 3,500 food and beverage processing plants across China, India, and Japan. South America and the Middle East & Africa together account for the remaining 8%, with localized growth driven by beverage expansion, urbanization, and rising pharmaceutical production. Cross-region deployment of standardized flavor matrices now exceeds 54% of multinational production networks, indicating increasing regional integration.

The region holds approximately 38% of global adoption, supported by high-volume beverage bottling, packaged food processing, and pharmaceutical formulation activity. Key demand comes from beverages (34%), processed foods (31%), and pharmaceuticals (24%). Regulatory oversight from food safety authorities has led to more than 72% of large plants implementing validated batch-control systems. Digital transformation is evident, with 68% of facilities using automated dosing and inline quality monitoring. Local players have expanded encapsulation capacity by over 19% since 2023 to serve pediatric medicines. Consumer behavior shows higher enterprise adoption in healthcare and functional beverages, with 59% of product launches using pre-standardized flavor matrices.

Europe accounts for around 29% of total market adoption, with Germany, the UK, and France representing more than 62% of regional demand. Clean-label and allergen-free regulations have resulted in over 47% of flavor systems being reformulated since 2022. More than 410 certified ingredient plants operate under advanced traceability rules. Emerging technologies such as solvent-free spray drying are now deployed in 44% of new installations. A leading regional producer invested in biodegradable carriers, increasing clean-label capacity by 21%. Regulatory pressure drives demand for explainable formulations, with 53% of manufacturers prioritizing audit-ready standardized systems.

Asia-Pacific ranks second by volume, contributing 25% of global usage, with China, India, and Japan accounting for 71% of regional consumption. The region hosts more than 3,500 high-capacity food and beverage plants and over 900 pharmaceutical formulation facilities. Manufacturing automation adoption reached 52% in 2025, supporting high-volume standardized production. Innovation hubs in Shanghai, Osaka, and Bengaluru lead microencapsulation deployment, with 18% of new systems using controlled-release carriers. A major regional producer expanded liquid flavor capacity by 240,000 tons annually. Consumer behavior shows growth driven by packaged foods and e-commerce channels, with 61% of urban consumers preferring standardized branded products.

South America represents about 5% of global adoption, led by Brazil and Argentina with a combined 67% regional share. Beverage processing accounts for 41% of demand, followed by bakery and confectionery at 29%. Infrastructure investment has increased automated blending penetration to 38% of industrial plants. Government incentives supporting food processing modernization cover more than 120 certified facilities. A Brazilian producer added 14 new blending lines in 2024 to serve export markets. Consumer behavior shows demand tied to flavored dairy and juice products, with 46% of new launches using standardized systems.

The region contributes nearly 3% of global usage, with UAE, Saudi Arabia, and South Africa accounting for 74% of regional demand. Beverage and dairy processing represent 48% of total applications, while pharmaceuticals contribute 21%. Technological modernization includes digital dosing adoption in 33% of new plants. Trade partnerships with Europe and Asia now supply over 60% of flavor inputs. A regional producer in the Gulf expanded spray-drying capacity by 16% in 2024. Consumer behavior reflects growing preference for flavored dairy and functional drinks, with 39% of urban consumers favoring standardized branded products.

United States – 32% Market Share: Dominates due to high production capacity, advanced automation, and strong pharmaceutical formulation demand.

China – 18% Market Share: Leads through large-scale food processing infrastructure and rapid expansion of standardized beverage manufacturing.

The competitive environment in the Standardized Flavor Systems Market is moderately consolidated yet intensely innovative, with over 60 active global competitors spanning multinational ingredient houses, specialty flavor innovators, and regional suppliers. Major players such as Givaudan SA, International Flavors & Fragrances Inc. (IFF), Symrise AG, Sensient Technologies Corporation, and Kerry Group plc lead the market with extensive flavor libraries, digital formulation platforms, and broad application support across beverages, packaged foods, and pharmaceutical taste systems. Collectively, the top 5 companies hold approximately 48–54% of the overall standardized flavor systems market, demonstrating leadership yet leaving room for agile mid-tier and regional firms to grow.

Competition is shaped by strategic partnerships, technology investments, and product launches aimed at improving sensory consistency, clean-label credentials, and formulation traceability. For example, leading innovators are deploying AI-assisted aroma prediction tools, handheld co-creation devices, and advanced encapsulation formats to shorten development cycles and bolster customer retention.

Innovation trends influencing competition include digital sensory analytics, biotech-derived and fermentation-based flavor components, and mobile co-creation tools that accelerate customer feedback loops. Mid-sized competitors are differentiating through specialty natural systems, regional flavor portfolios, and tailor-made solutions for plant-based or functional food sectors. Overall, market positioning hinges on R&D depth, digital transformation strategies, and responsiveness to evolving regulatory and consumer demands, underlining the importance of strategic agility and sustained investment for competitive advantage.

Sensient Technologies Corporation

Kerry Group plc

Robertet SA

Mane SA

McCormick & Company

Takasago International Corporation

Cargill, Incorporated

ADM (Archer Daniels Midland Company)

T. Hasegawa Co., Ltd.

Bell Flavors & Fragrances

Flavorchem Corporation

Current and emerging technologies are reshaping the Standardized Flavor Systems Market by enhancing formulation precision, accelerating innovation cycles, and improving quality control across production environments. Advanced digital formulation platforms and sensory analytics are enabling developers to simulate taste profiles, optimize ingredient ratios, and predict consumer preferences with greater accuracy. Devices like handheld aroma co-creation tools allow real-time engagement between flavor specialists and end-users, streamlining product refinement.

AI and machine learning integration in flavor design is driving computational flavor prediction, enabling rapid prototyping and reducing dependency on labor-intensive trial-and-error methods. These tools analyze extensive sensory databases and demographic preferences to anticipate successful flavor combinations, significantly cutting R&D cycle times. Biotech approaches, including precision fermentation and microbial synthesis, are producing flavor molecules that mimic natural profiles while lowering reliance on volatile agricultural inputs, contributing to sustainable formulation pipelines.

Encapsulation technology has also advanced, with micro- and nano-encapsulation systems that protect sensitive flavor compounds from processing stresses such as heat, pH shifts, and oxidation. These systems ensure controlled release and improve shelf stability, especially in complex matrices like dairy, beverages, and nutritional formulations. Digital inline quality monitoring solutions, such as near-infrared (NIR) and mass flow sensors, are increasingly deployed to ensure consistent batch performance, reducing rejection rates and enhancing traceability for compliance audits.

Emerging tech trends include predictive consumer preference engines, cloud-connected flavor libraries, and mobile-integrated sensory tools that collect real-time feedback. Together, these innovations are enabling flavor houses and manufacturers to respond quickly to consumer trends, regulatory demands, and operational constraints, making technology a core competitive lever in the standardized flavor systems domain.

• In June 2025, Givaudan unveiled its latest digital innovation showcase at VivaTech 2025, highlighting new digital tools and consumer-insight platforms designed to accelerate flavor and fragrance formulation and enhance sensory engagement through technology. Source: www.givaudan.com

• In May 2025, Givaudan announced the launch of Myromi™, a patent-pending handheld aroma delivery device controlled via smartphone, enabling real-time flavor co-creation and reducing development uncertainty. Source: www.givaudan.com

• In October 2025, Symrise showcased its Symvision AI™ tool at Gulfood Manufacturing 2025, an award-winning flavor and ingredient prediction platform that aligns product concepts with evolving consumer preferences for faster market entries. Source: www.symrise.com

• In December 2025, Givaudan completed the acquisition of Belle Aire Creations, enhancing regional reach and creative capabilities in the U.S. fragrance and flavor space, reinforcing its strategic expansion. Source: www.givaudan.com

The Standardized Flavor Systems Market Report encompasses a broad and detailed examination of industry segments, technological innovations, geographic markets, application domains, and end-user landscapes. The report systematically analyzes product types including liquid, powder, encapsulated, and emulsified systems, providing insights into usage contexts such as beverages, confectionery, dairy alternatives, snacks, and pharmaceuticals. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering regional behavior patterns, industrial infrastructure assessments, and adoption tendencies across mature and emerging markets. The report also evaluates functional performance categories like taste enhancement, aroma delivery, heat stability, and controlled release systems that influence formulation standards.

Within application analysis, the report examines diverse environments where standardized flavor systems are critical, such as high-volume beverage bottling lines, automated bakery processing, pharmaceutical taste-masking formulations, and nutraceutical product design. End-user insights section profiles leading adopters including multinational food and beverage producers, pharmaceutical manufacturers, contract manufacturers, and specialty ingredient formulators, detailing consumption patterns and technical requirements.

The scope includes technology impact assessments, exploring digital sensory platforms, AI-enhanced formulation tools, biotechnology-derived flavor compounds, and advanced encapsulation technologies. Competitive mapping features major global players, innovation trends, and strategic initiatives such as partnerships, acquisitions, and product launches that shape market dynamics. Additionally, niche segments like clean-label systems, region-specific flavor portfolios, and consumer preference forecasting tools are evaluated, offering decision-makers a comprehensive view of opportunities and challenges in this evolving market landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 700.0 Million |

| Market Revenue (2033) | USD 950.7 Million |

| CAGR (2026–2033) | 3.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Givaudan SA, International Flavors & Fragrances (IFF), Symrise AG, Sensient Technologies Corporation, Kerry Group plc, Robertet SA, Mane SA, McCormick & Company, Takasago International Corporation, Cargill, ADM, T. Hasegawa Co., Bell Flavors & Fragrances, Flavorchem Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |