Reports

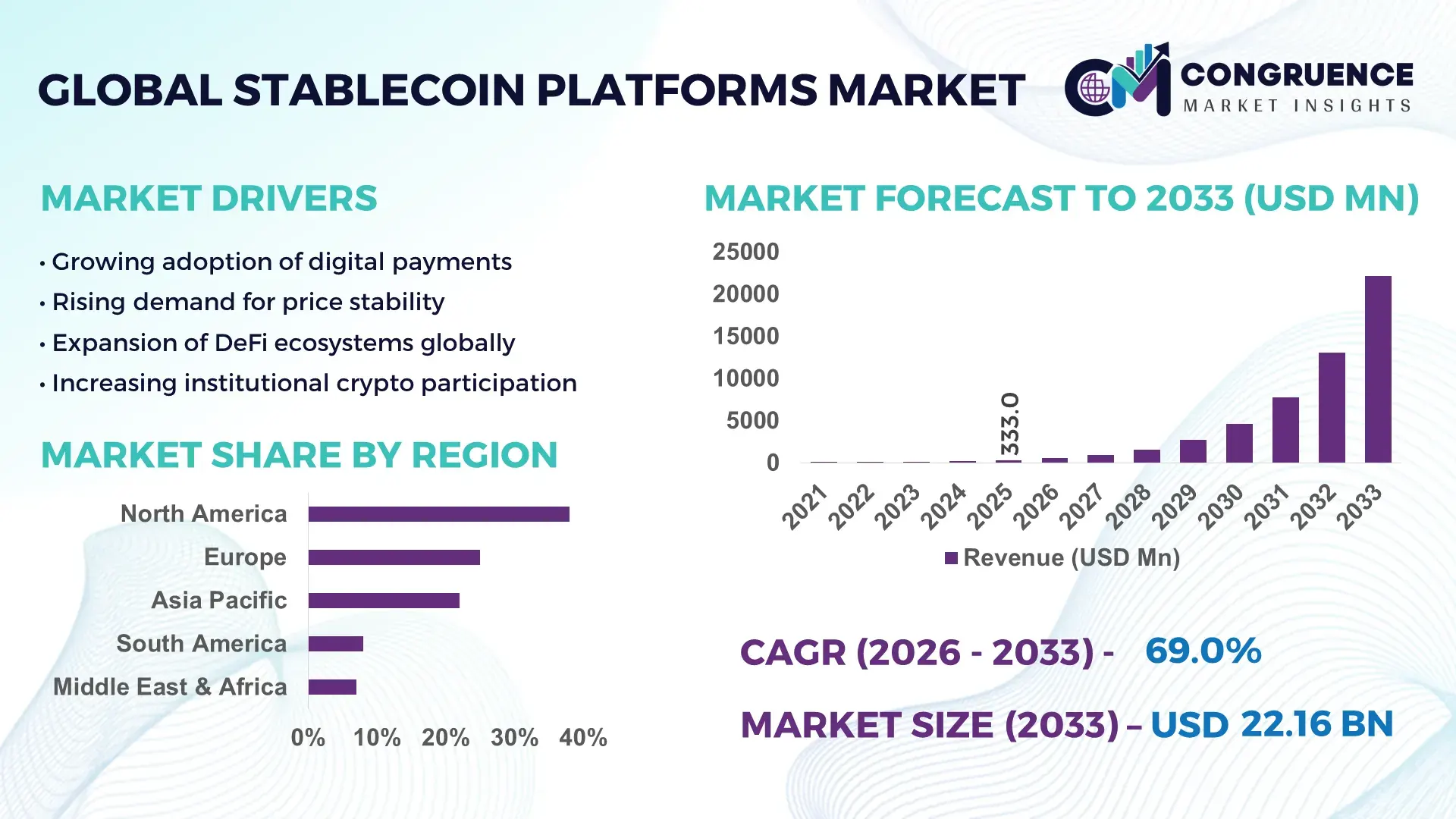

The Global Stablecoin Platforms Market was valued at USD 333.0 Million in 2025 and is anticipated to reach a value of USD 22,158.4 Million by 2033 expanding at a CAGR of 69.0% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing demand for low-volatility digital assets in cross-border payments and decentralized finance ecosystems.

The United States dominates the Stablecoin Platforms Market with advanced blockchain infrastructure and strong institutional participation. Over 60% of global stablecoin transaction volumes are processed through platforms headquartered in the U.S., supported by more than 150 active fintech and blockchain firms. Institutional adoption has surged, with over 45% of large financial institutions integrating stablecoin-based settlement solutions in 2025. Additionally, U.S.-based platforms support over 70% of DeFi liquidity pools globally, enabling high transaction throughput exceeding 25 million transactions per day. Investments in blockchain infrastructure exceeded USD 12 billion in 2025, further strengthening technological capabilities such as real-time settlement and programmable payments.

Market Size & Growth: USD 333.0 Million in 2025, projected to reach USD 22,158.4 Million by 2033 at 69.0% CAGR, driven by rising demand for digital payment efficiency.

Top Growth Drivers: 65% increase in cross-border payment adoption, 58% improvement in transaction efficiency, 52% rise in DeFi participation.

Short-Term Forecast: By 2028, transaction settlement times are expected to improve by 40%, enhancing financial system efficiency.

Emerging Technologies: Blockchain interoperability protocols, smart contract automation, and tokenized asset integration are reshaping the ecosystem.

Regional Leaders: North America (~USD 8.5 Billion by 2033) with institutional adoption, Asia-Pacific (~USD 6.7 Billion) driven by mobile payments, Europe (~USD 4.2 Billion) with regulatory frameworks.

Consumer/End-User Trends: Over 55% of fintech firms now use stablecoins for payments, while 48% of users prefer them for remittances.

Pilot or Case Example: In 2025, a fintech pilot reduced cross-border transaction costs by 35% using stablecoin rails.

Competitive Landscape: Market leader holds ~28% share, followed by Circle, Tether, Paxos, Binance, and MakerDAO.

Regulatory & ESG Impact: Over 40 countries introduced digital asset regulations improving compliance and transparency.

Investment & Funding Patterns: More than USD 15 billion invested in blockchain and stablecoin infrastructure between 2023–2025.

Innovation & Future Outlook: Growth in CBDC integration, programmable payments, and AI-driven fraud detection.

Stablecoin Platforms Market is witnessing expansion across financial services (45%), e-commerce (25%), and remittances (20%), with emerging adoption in gaming and Web3 ecosystems (10%). Innovations such as multi-chain interoperability and algorithmic stabilization are enhancing efficiency. Regulatory clarity across Europe and Asia is accelerating institutional adoption, while rising demand for real-time payments and tokenized assets continues to shape long-term market evolution.

The Stablecoin Platforms Market is strategically positioned at the intersection of financial digitization, blockchain innovation, and global payment modernization. Enterprises are increasingly leveraging stablecoins to reduce transaction costs by up to 30% compared to traditional banking systems, while improving settlement speed by over 70%. Blockchain-based payment infrastructure delivers 60% faster processing compared to legacy SWIFT systems, enabling near-instant global transfers and improved liquidity management.

North America dominates in transaction volume, while Asia-Pacific leads in adoption with over 50% of fintech startups integrating stablecoin solutions into mobile-first applications. By 2028, AI-powered transaction monitoring is expected to reduce fraud and compliance risks by 45%, significantly improving operational efficiency. Regulatory advancements such as digital asset frameworks and licensing regimes are supporting compliance, with firms committing to 35% improvements in transparency and reporting standards by 2030.

In 2025, a leading U.S.-based fintech firm achieved a 40% reduction in transaction settlement time through blockchain-enabled stablecoin infrastructure, demonstrating real-world efficiency gains. Furthermore, ESG considerations are emerging, with blockchain networks targeting up to 50% energy efficiency improvements through proof-of-stake mechanisms by 2027.

Looking ahead, the Stablecoin Platforms Market is evolving as a critical pillar for financial resilience, enabling secure, transparent, and scalable digital transactions. Its integration with decentralized finance, central bank digital currencies, and enterprise payment systems positions it as a cornerstone for sustainable and compliant global financial ecosystems.

The Stablecoin Platforms Market is shaped by rapid advancements in blockchain technology, increasing institutional adoption, and the growing demand for efficient digital payment solutions. The market is experiencing strong momentum due to rising use cases in cross-border payments, decentralized finance (DeFi), and tokenized asset transactions. Over 70% of global crypto exchanges now support stablecoin trading pairs, highlighting their importance in liquidity provisioning. Additionally, the shift toward real-time settlement systems has increased adoption among financial institutions, with over 45% integrating blockchain-based payment rails. Regulatory developments across key regions are influencing market expansion, with more than 40 countries introducing digital asset guidelines. Technological improvements such as interoperability protocols and smart contracts are enhancing transaction efficiency, while increasing consumer preference for low-volatility digital assets continues to drive market demand across multiple sectors.

The demand for efficient cross-border payments is a major driver of the Stablecoin Platforms Market, as traditional banking systems often involve delays of 2–5 days and transaction fees exceeding 6%. Stablecoins enable near-instant settlement, reducing transaction times by over 70% and lowering costs by up to 50%. In 2025, over 55% of global remittance platforms integrated stablecoin-based solutions to enhance speed and reduce dependency on intermediaries. Additionally, global remittance flows exceeded USD 800 billion, with stablecoins accounting for approximately 18% of digital remittance transactions. Financial institutions are increasingly adopting blockchain payment systems, with over 40% piloting stablecoin settlements for international trade and supply chain financing. These efficiencies are accelerating adoption among businesses and consumers, particularly in emerging markets where access to traditional banking infrastructure is limited.

Regulatory uncertainty remains a key restraint in the Stablecoin Platforms Market, as inconsistent frameworks across jurisdictions create compliance challenges. Over 35% of fintech companies reported delays in stablecoin deployment due to unclear regulations in 2025. Different countries impose varying requirements on reserve backing, licensing, and transaction monitoring, increasing operational complexity. For example, some regions mandate 100% fiat backing, while others allow algorithmic models, leading to fragmented market practices. Additionally, concerns regarding financial stability and consumer protection have led to stricter scrutiny, with over 25 regulatory investigations into stablecoin issuers globally in 2024–2025. This uncertainty limits institutional participation and slows innovation, particularly for smaller market players lacking resources to navigate complex compliance requirements.

The expansion of decentralized finance (DeFi) presents significant opportunities for the Stablecoin Platforms Market, as stablecoins serve as the primary medium of exchange within DeFi ecosystems. Over 70% of DeFi transactions are conducted using stablecoins, highlighting their critical role in lending, borrowing, and liquidity provision. The total value locked in DeFi platforms exceeded USD 90 billion in 2025, with stablecoins accounting for nearly 60% of liquidity pools. Emerging applications such as tokenized real-world assets and decentralized exchanges are further increasing demand. Additionally, institutional DeFi adoption is growing, with over 30% of financial firms exploring blockchain-based lending and trading platforms. These developments are creating new revenue streams and expanding use cases, positioning stablecoins as a foundational element of next-generation financial infrastructure.

Scalability and network congestion pose significant challenges to the Stablecoin Platforms Market, particularly during periods of high transaction volume. Major blockchain networks experience throughput limitations, processing between 15 to 65 transactions per second, leading to delays and increased transaction fees. In 2025, transaction fees on certain networks surged by over 200% during peak demand periods, impacting user experience. Additionally, network congestion can cause delays in settlement, undermining the efficiency advantages of stablecoins. While layer-2 scaling solutions and alternative blockchain networks are being developed, adoption remains uneven, with only 35% of platforms fully integrated with scalable infrastructure. Addressing these challenges is critical to ensuring consistent performance and supporting the growing demand for stablecoin transactions globally.

• Surge in Cross-Border Payment Adoption: Stablecoin usage in cross-border payments increased by over 65% in 2025, with transaction volumes exceeding 25 million daily transfers globally. Over 50% of fintech companies integrated stablecoin rails, reducing average settlement times from 3 days to under 10 minutes, significantly improving operational efficiency.

• Expansion of DeFi Integration: Stablecoins account for nearly 70% of DeFi transactions, with over 60% of liquidity pools relying on them for stability. More than 45 million active DeFi users utilized stablecoins in 2025, reflecting strong adoption across lending, staking, and decentralized exchange platforms.

• Rise of Multi-Chain Interoperability: Over 55% of stablecoin platforms now support multi-chain functionality, enabling seamless transfers across 10+ blockchain networks. Cross-chain transaction volumes grew by 48% in 2025, enhancing liquidity distribution and reducing dependency on single-network ecosystems.

• Increasing Institutional Adoption: Institutional participation rose by 42% in 2025, with over 40% of banks and financial institutions piloting stablecoin-based settlement systems. Corporate treasury adoption increased by 35%, highlighting the growing role of stablecoins in enterprise-level financial operations.

The Stablecoin Platforms Market segmentation is primarily categorized by type, application, and end-user, each playing a crucial role in shaping market dynamics. Fiat-collateralized stablecoins dominate due to their transparency and regulatory alignment, while crypto-collateralized and algorithmic models offer flexibility and scalability. Applications such as payments, DeFi, and remittances drive widespread adoption, with increasing use in e-commerce and tokenized assets. End-users include financial institutions, enterprises, and individual consumers, with fintech firms leading adoption. Over 60% of platforms cater to cross-border payments and liquidity provisioning, reflecting the growing importance of stablecoins in global financial ecosystems.

Fiat-collateralized stablecoins lead the market, accounting for approximately 65% of total adoption due to their direct backing by fiat reserves and regulatory compliance. These stablecoins provide high stability and are widely used in institutional transactions and payment systems. Crypto-collateralized stablecoins hold around 20% share, offering decentralization and transparency but requiring over-collateralization, which limits scalability. Algorithmic stablecoins represent nearly 10% of the market and are the fastest-growing segment, with an expected CAGR of 72%, driven by advancements in smart contract-based stabilization mechanisms. Other niche types, including commodity-backed stablecoins, collectively contribute around 5%, serving specialized use cases such as asset tokenization.

• In 2025, a major blockchain network processed over 12 million daily transactions using fiat-backed stablecoins, highlighting their dominance in high-volume payment systems.

Payments and remittances dominate the Stablecoin Platforms Market with a 50% share, driven by demand for faster and cheaper cross-border transactions. DeFi applications account for around 30%, supporting lending, borrowing, and liquidity provisioning. However, tokenized asset trading is the fastest-growing segment with a CAGR of 70%, expected to exceed 25% adoption by 2033 due to increasing interest in digital asset ownership. Other applications, including e-commerce and gaming, collectively hold 20% share. In 2025, more than 45% of enterprises reported using stablecoins for payment processing, while over 55% of users preferred them for remittances due to lower fees.

• In 2025, over 150 global fintech platforms integrated stablecoin payment systems, enabling faster transactions for more than 20 million users.

Financial institutions dominate the market with a 40% share, leveraging stablecoins for settlement, liquidity management, and cross-border transactions. Enterprises account for 35%, driven by adoption in e-commerce and supply chain payments. Individual consumers represent 25%, using stablecoins for remittances and digital payments. Fintech firms are the fastest-growing end-user segment, with a CAGR of 68%, fueled by increasing demand for digital financial services. Over 50% of fintech startups integrated stablecoin solutions in 2025, while 48% of consumers reported using stablecoins for international transfers. Other end-users, including government and public sector entities, collectively contribute around 10% through pilot projects and regulatory initiatives.

• In 2025, over 500 fintech startups globally adopted stablecoin platforms to enhance payment efficiency and reduce transaction costs.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 72% between 2026 and 2033.

North America processed over 60% of global stablecoin transaction volumes, supported by more than 150 active blockchain firms and institutional adoption exceeding 45%. Europe held approximately 25% share, driven by regulatory clarity and digital finance initiatives. Asia-Pacific accounted for 22%, with over 300 million digital payment users and increasing fintech penetration. South America and Middle East & Africa collectively contributed 15%, with strong growth in remittance-driven markets.

North America holds approximately 38% of the Stablecoin Platforms Market, driven by strong institutional participation and advanced blockchain infrastructure. Financial services and fintech industries account for over 60% of regional demand, supported by digital transformation initiatives. Regulatory frameworks in the U.S. have improved compliance, with over 45% of financial institutions piloting stablecoin-based settlements. Technological advancements such as smart contracts and AI-based fraud detection are widely adopted. A leading regional player has enabled over 20 million daily transactions using stablecoin infrastructure. Consumer behavior indicates higher enterprise adoption, particularly in banking and fintech sectors.

Europe accounts for around 25% of the market, with key countries including Germany, the UK, and France leading adoption. Regulatory initiatives such as digital asset frameworks have improved transparency and compliance, driving institutional confidence. Over 40% of fintech firms in Europe have integrated stablecoin solutions. Emerging technologies like blockchain interoperability are widely adopted, enhancing transaction efficiency. A regional player has successfully implemented stablecoin-based payment systems across multiple EU countries. Consumer behavior shows strong preference for regulated and compliant digital financial solutions.

Asia-Pacific ranks among the fastest-growing regions, with countries such as China, India, and Japan leading adoption. The region has over 300 million active digital payment users, with stablecoin adoption increasing rapidly in mobile-based platforms. Infrastructure investments and fintech innovation hubs are driving growth, with over 50% of startups integrating blockchain solutions. A regional player has processed over 10 million daily transactions through mobile-based stablecoin platforms. Consumer behavior highlights strong demand for fast and low-cost payment solutions, particularly in e-commerce.

South America holds approximately 8% market share, with Brazil and Argentina leading adoption. High remittance flows and inflation challenges are driving demand for stablecoin platforms. Governments are exploring digital asset regulations, with over 30% of fintech firms adopting blockchain-based payment solutions. Infrastructure improvements and mobile penetration are supporting growth. A regional player has enabled stablecoin-based remittances for over 5 million users. Consumer behavior indicates strong reliance on stablecoins for preserving value and facilitating cross-border transfers.

Middle East & Africa account for approximately 7% of the market, with UAE and South Africa as key growth countries. Digital transformation initiatives in banking and fintech sectors are driving adoption, with over 35% of financial institutions exploring blockchain solutions. Government support and trade partnerships are accelerating market expansion. A regional player has implemented stablecoin-based payment systems for cross-border trade. Consumer behavior reflects growing demand for secure and efficient digital payment systems.

United States – 38% Market Share: Driven by strong institutional adoption and advanced blockchain infrastructure

China – 18% Market Share: Supported by large digital payment ecosystem and fintech innovation

The Stablecoin Platforms Market is moderately consolidated, with over 80 active global players competing across infrastructure development, issuance, and payment solutions. The top five companies collectively account for approximately 55% of the market share, indicating a competitive yet concentrated environment. Leading players focus on strategic partnerships, product innovation, and regulatory compliance to strengthen their market positions. Over 40% of companies have introduced multi-chain interoperability solutions to enhance scalability and transaction efficiency. Mergers and acquisitions have increased by 25% between 2023 and 2025, reflecting consolidation trends.

Additionally, more than 60% of leading firms are investing in AI-driven analytics and fraud detection systems. The competitive landscape is further shaped by collaborations between fintech firms and traditional financial institutions, enabling broader adoption and integration of stablecoin solutions.

Tether

Paxos

Binance

MakerDAO

Coinbase

Ripple

Gemini

BitGo

Fireblocks

Anchorage Digital

Kraken

The Stablecoin Platforms Market is driven by advanced blockchain technologies, including smart contracts, interoperability protocols, and scalable network architectures. Over 55% of platforms now utilize multi-chain frameworks, enabling seamless transactions across multiple blockchain ecosystems. Smart contracts automate over 65% of stablecoin transactions, improving efficiency and reducing operational costs. Additionally, layer-2 scaling solutions have increased transaction throughput by up to 300%, addressing network congestion challenges.

Artificial intelligence is increasingly integrated into stablecoin platforms, with over 40% of firms deploying AI-based fraud detection systems to enhance security and compliance. Tokenization technologies are enabling the conversion of real-world assets into digital tokens, with over 30% of platforms supporting asset-backed stablecoins. Furthermore, proof-of-stake consensus mechanisms have improved energy efficiency by up to 50%, aligning with ESG goals.

Emerging technologies such as central bank digital currency (CBDC) integration and decentralized identity systems are expected to further transform the market. Over 20 countries are piloting CBDC projects that can integrate with stablecoin platforms, enhancing interoperability and financial inclusion. These technological advancements are positioning stablecoin platforms as a critical component of the global digital financial ecosystem.

• In June 2025, Circle successfully completed its initial public offering on the New York Stock Exchange, raising approximately USD 1.05 billion and achieving a valuation of nearly USD 8 billion. The IPO marked one of the largest crypto-related public listings, reflecting strong institutional demand for stablecoin infrastructure.

• In December 2025, Circle, Ripple, and Paxos received conditional approval from the U.S. Office of the Comptroller of the Currency for national trust bank charters. This allows them to operate under federal regulatory frameworks, enhancing compliance, custody capabilities, and integration with traditional financial systems.

• In March 2026, Ripple upgraded its Ripple Payments platform into a full-stack stablecoin settlement solution powered by RLUSD, enabling operations across more than 60 markets and 51 payment rails. The platform integrates custody, liquidity, and payout services, significantly improving cross-border transaction efficiency. Source: www.mexc.co

• In September 2025, Tether announced expansion into the U.S. market with the launch of a new dollar-pegged stablecoin and strategic operational scaling. This move followed regulatory developments and aims to strengthen its position in institutional payment systems and compliant financial ecosystems.

The scope of the Stablecoin Platforms Market Report encompasses a comprehensive analysis of platform types, applications, end-users, technologies, and regional markets. The report evaluates key segments including fiat-collateralized, crypto-collateralized, and algorithmic stablecoin platforms, covering their adoption across payments, decentralized finance, remittances, and emerging applications such as tokenized assets and Web3 ecosystems.

Geographically, the report includes in-depth insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing regional adoption patterns, technological advancements, and regulatory environments. It also highlights key industry sectors such as financial services, fintech, e-commerce, and enterprise payments, which collectively account for over 80% of stablecoin platform usage.

The report further explores technological developments including blockchain interoperability, smart contracts, AI integration, and scalability solutions, which are transforming platform capabilities. Additionally, it examines competitive dynamics, strategic initiatives, and innovation trends shaping the market. With a focus on measurable insights and industry-specific data, the report provides decision-makers with a detailed understanding of market structure, growth drivers, challenges, and future opportunities within the Stablecoin Platforms Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 333.0 Million |

| Market Revenue (2033) | USD 22,158.4 Million |

| CAGR (2026–2033) | 69.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Circle; Tether; Paxos; Binance; MakerDAO; Coinbase; Ripple; Gemini; BitGo; Fireblocks; Anchorage Digital; Kraken |

| Customization & Pricing | Available on Request (10% Customization Free) |