Reports

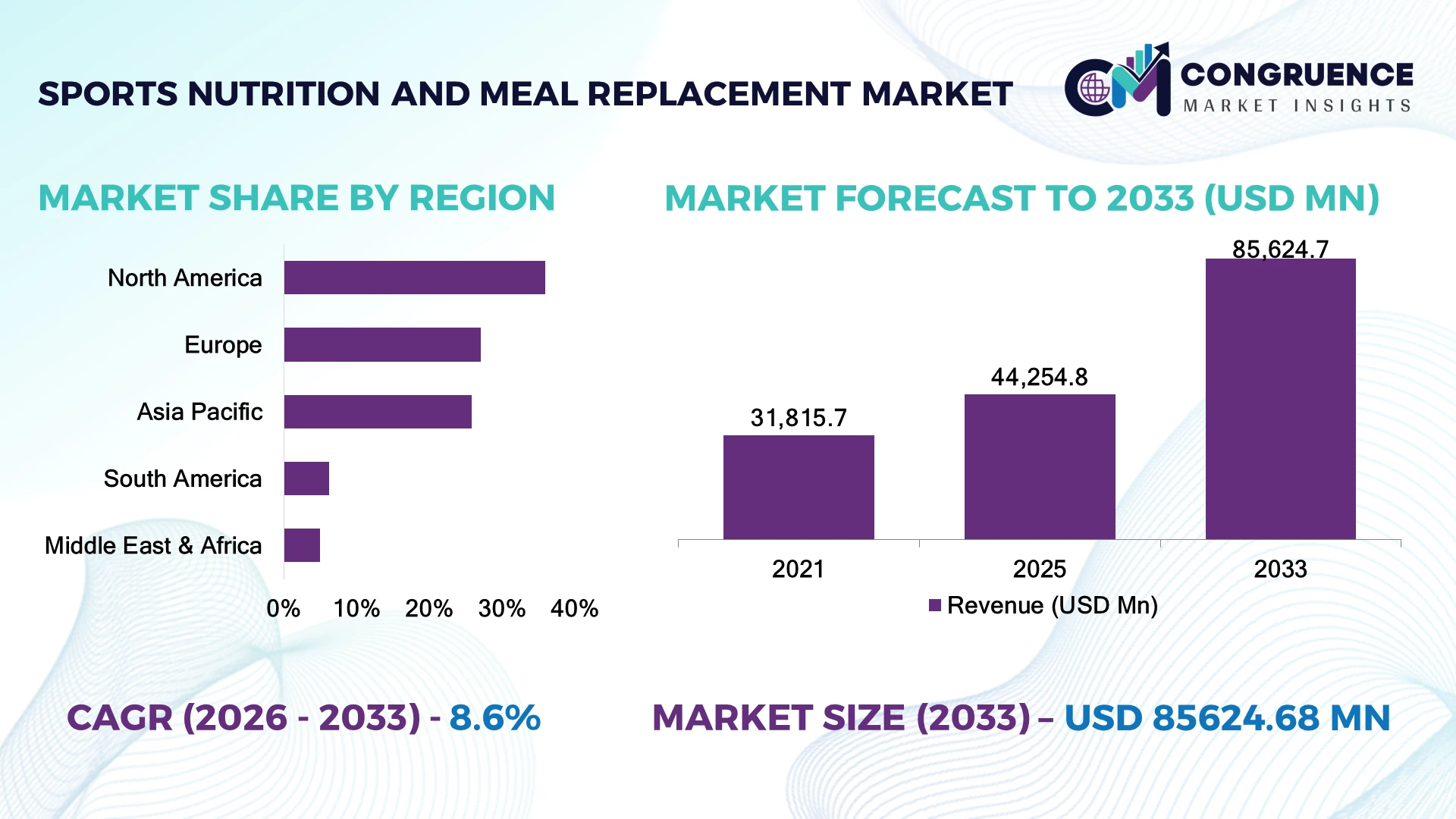

The Global Sports Nutrition and Meal Replacement Market was valued at USD 44,254.8 Million in 2025 and is anticipated to reach a value of USD 85,624.7 Million by 2033 expanding at a CAGR of 8.6% between 2026 and 2033. Rising demand for high-protein functional nutrition, personalized dietary solutions, and convenient on-the-go meal formats is accelerating product innovation across sports performance, weight management, and active lifestyle segments.

The United States leads the market with approximately 36% of global consumption, supported by advanced food manufacturing, widespread fitness participation, and strong investment in functional nutrition innovation. More than 71% of newly launched sports nutrition products incorporate clean-label or plant-based ingredients, compared with Japan's stronger emphasis on scientifically formulated performance nutrition. Global ingredient sourcing diversification following post-pandemic supply-chain restructuring continues influencing manufacturing and procurement strategies.

Companies investing in premium formulations, clinical validation, and resilient ingredient supply networks are strengthening long-term competitive positioning.

Market Size & Growth: USD 44,254.8 Million in 2025 reaches USD 85,624.7 Million by 2033 at a CAGR of 8.6%, driven by premium functional nutrition and protein innovation.

Top Growth Drivers: Plant-based nutrition (+29%), personalized nutrition (+24%), and active lifestyle participation (+22%) strengthen demand.

Short-Term Forecast: By 2028, manufacturing efficiency improves nearly 16%, while formulation costs decline approximately 10% through ingredient optimization.

Emerging Technologies: AI-powered nutrition personalization, precision fermentation, and microencapsulation improve product functionality and shelf stability.

Regional Leaders: North America exceeds USD 30 Billion, Europe approaches USD 21 Billion, and Asia-Pacific surpasses USD 24 Billion through premium nutrition adoption.

Consumer/End-User Trends: More than 66% of consumers prefer high-protein, clean-label meal replacement products with functional ingredients.

Pilot/Case Example: In 2026, AI-based personalized nutrition programs improved customer retention by approximately 27% across digital wellness platforms.

Competitive Landscape: Leading brands control nearly 43% of the market, led by Glanbia, Abbott, Herbalife, Nestlé Health Science, and Danone.

Regulatory & ESG Impact: Sustainable packaging initiatives reduce virgin plastic usage by nearly 18% while supporting evolving environmental compliance.

Investment & Funding: More than USD 2.8 Billion supports manufacturing expansion, ingredient innovation, and regional production diversification.

Innovation & Future Outlook: Precision nutrition, functional bioactive ingredients, and personalized meal planning are reshaping premium product development.

Sports Nutrition and Meal Replacement products are gaining traction across fitness enthusiasts, clinical nutrition users, busy professionals, and aging populations as brands expand functional formulations with protein blends, probiotics, adaptogens, and botanical ingredients. More than 58% of premium product launches now feature clean-label positioning, while evolving ingredient traceability standards and diversified protein sourcing continue reshaping manufacturing priorities, setting the stage for broader strategic transformation.

The Sports Nutrition and Meal Replacement Market has become strategically important as nutrition increasingly shifts from performance enhancement toward preventive health, metabolic wellness, and personalized dietary management. Consumer purchasing decisions are increasingly influenced by ingredient transparency, functional health claims, and digital nutrition guidance. At the same time, manufacturers are restructuring global ingredient sourcing and production networks to improve resilience against agricultural supply volatility and evolving food regulatory requirements.

Advanced formulation technologies using precision fermentation and microencapsulation improve nutrient stability by approximately 22% compared with conventional formulations while reducing ingredient degradation during processing by nearly 18%. North America continues leading premium product innovation and clinical nutrition development, whereas Asia-Pacific is experiencing faster expansion through urbanization, digital commerce, and growing health-conscious consumer populations. During the next two to three years, personalized nutrition platforms are expected to exceed 55% adoption among premium nutrition brands seeking differentiated consumer engagement.

A leading nutrition company integrating AI-powered dietary recommendations with subscription-based meal replacement products can improve customer retention while strengthening recurring sales. Companies are expanding investments in plant-based proteins, sustainable ingredient partnerships, and digital wellness ecosystems to diversify product portfolios. Businesses combining scientifically validated formulations, resilient supply chains, personalized nutrition technologies, and omnichannel distribution will secure stronger competitive positioning and long-term operational advantage in the evolving functional nutrition industry.

Demand is accelerating as sports nutrition products evolve from niche performance supplements into mainstream wellness and preventive nutrition solutions. More than 64% of new product launches now feature high-protein, clean-label, or functional ingredient claims, while plant-based protein formulations have expanded by approximately 29% across premium product portfolios. The United States continues strengthening domestic production of specialty nutrition products following supply-chain diversification initiatives that encourage localized ingredient sourcing. This structural transition improves product availability and strengthens consumer confidence. Leading manufacturers are responding through precision nutrition research, strategic ingredient partnerships, manufacturing expansion, and AI-assisted product development, enabling faster commercialization while broadening appeal beyond athletes to active lifestyle consumers and healthy aging populations.

Fluctuating prices for whey protein, specialty amino acids, and botanical ingredients continue pressuring production economics across the sports nutrition industry. Premium protein ingredients remain approximately 18–24% more expensive than conventional nutritional inputs, while regulatory validation and labeling compliance increase product development timelines by nearly 20%. European food labeling requirements and evolving health claim regulations require additional formulation validation before commercialization, increasing operational costs for manufacturers. These structural pressures reduce pricing flexibility and compress profit margins, particularly for premium brands. Companies are mitigating exposure through diversified ingredient sourcing, long-term supplier agreements, localized manufacturing, and expanded investment in alternative proteins such as pea, fava bean, and precision-fermented ingredients.

AI-driven dietary personalization, microbiome-based nutrition, and digital wellness platforms are creating new commercial opportunities beyond conventional sports supplements. Nearly 57% of premium nutrition brands are integrating personalized dietary recommendations into digital consumer engagement platforms, while AI-assisted formulation improves product matching accuracy by approximately 26%. South Korea continues expanding digital health infrastructure that supports personalized nutrition services integrated with wearable health technologies. Manufacturers are investing in clinical nutrition research, subscription-based nutrition programs, technology partnerships, and digital wellness ecosystems. A significant strategic opportunity lies in combining nutrition products with real-time health analytics, transforming one-time product purchases into long-term personalized wellness relationships.

Maintaining scientific credibility while accelerating product innovation remains a significant long-term challenge. Approximately 46% of consumers actively evaluate ingredient transparency before purchasing premium nutrition products, while inconsistent product claims continue affecting purchasing confidence across global markets. The United States has increased scrutiny of dietary supplement labeling and product quality expectations, placing greater emphasis on substantiated performance claims. These evolving expectations directly influence brand reputation, regulatory readiness, and international market access. Companies must strengthen clinical research, third-party ingredient verification, transparent labeling, and digital traceability systems while investing in academic collaborations and quality assurance infrastructure to maintain competitive differentiation and sustainable consumer trust.

Clean-Label Protein Expansion More than 61% of newly introduced sports nutrition products now feature clean-label positioning, while plant-based protein usage has increased by approximately 28% across premium formulations. Greater consumer scrutiny of ingredient transparency is reshaping product development, prompting manufacturers to strengthen traceable sourcing, simplify ingredient lists, and expand partnerships with sustainable protein suppliers to reinforce brand credibility.

Ready-to-Drink Formats Accelerate Ready-to-drink nutrition beverages continue gaining shelf space as convenience purchasing increases, with retail availability expanding by nearly 24% and impulse purchases improving approximately 19%. Improved aseptic processing and packaging technologies enhance shelf stability while reducing distribution complexity. Manufacturers are expanding regional production capacity and optimizing packaging operations to support faster omnichannel fulfillment and wider market penetration.

Digital Nutrition Personalization AI-enabled nutrition recommendations are becoming integral to premium consumer engagement strategies, improving personalized product matching by approximately 27% while increasing subscription retention by nearly 21%. Integration with wearable health devices enables continuous dietary optimization. Nutrition brands are investing in digital wellness platforms, technology partnerships, and data-driven consumer services to strengthen recurring engagement beyond traditional retail transactions.

Alternative Protein Diversification Precision-fermented proteins, blended plant proteins, and upcycled nutritional ingredients are reshaping formulation strategies as supply-chain resilience becomes a procurement priority. Alternative protein utilization has increased by approximately 23%, while diversified ingredient sourcing reduces dependency on conventional dairy proteins by nearly 17%. Companies are accelerating ingredient innovation, expanding regional supplier networks, and strengthening collaborative research to improve formulation flexibility and long-term manufacturing resilience.

Protein Supplements accounted for approximately 43% of the Sports Nutrition and Meal Replacement Market in 2025, maintaining leadership due to broad consumer acceptance, proven performance benefits, and extensive availability across powders, ready-to-drink beverages, and bars. Their versatility for muscle recovery, weight management, and daily nutritional support makes them the preferred category among athletes and lifestyle consumers alike. Meal Replacement Products continue strengthening their market presence as convenient nutrition solutions for busy professionals, while Sports Drinks remain essential for hydration and endurance activities. Energy Bars, Protein Bars, and Energy Gels retain strategic importance by addressing portable nutrition needs across fitness, outdoor recreation, and endurance sports. Manufacturers continue investing in clean-label formulations, advanced protein blends, and functional ingredient innovation to strengthen product differentiation.

Meal Replacement Products represent the fastest-growing type as consumers increasingly seek nutritionally balanced, convenient alternatives to traditional meals. Nearly 59% of premium meal replacement launches now feature high-protein, low-sugar, or plant-based formulations designed for personalized wellness goals. Sports Drinks continue evolving through electrolyte optimization and functional hydration technologies, while Protein Bars expand through premium ingredient innovation and improved taste profiles. Companies are strengthening product portfolios through precision nutrition research, strategic ingredient partnerships, regional manufacturing expansion, and digital consumer engagement, shifting investment toward multifunctional nutrition products that combine convenience, health benefits, and performance support.

According to findings published by the International Society of Sports Nutrition during 2025, high-protein nutritional products continued demonstrating strong adoption among physically active consumers, reinforcing sustained commercial demand for scientifically formulated sports nutrition solutions.

Muscle Building accounted for approximately 36% of total market demand in 2025, supported by increasing participation in resistance training, recreational fitness, and professional sports. Protein supplementation remains central to muscle recovery and lean mass development, driving sustained demand across gyms, health clubs, and digital fitness communities. Performance Enhancement continues serving competitive athletes through advanced nutritional formulations, while Energy & Endurance applications remain significant for runners, cyclists, and endurance sports participants. General Wellness and Clinical Nutrition applications continue expanding as sports nutrition products increasingly address preventive healthcare, healthy aging, and everyday nutritional support beyond athletic performance.

Weight Management represents the fastest-growing application as consumers increasingly integrate meal replacement products into structured wellness programs and calorie-controlled diets. More than 62% of premium nutrition brands have expanded product portfolios targeting weight control, metabolic health, and satiety management. Clinical Nutrition is also gaining momentum as healthcare providers recommend specialized nutritional products for recovery and nutritional supplementation. Companies are responding through personalized nutrition platforms, AI-assisted dietary recommendations, subscription-based wellness programs, and clinically validated formulations that broaden consumer adoption while strengthening long-term brand loyalty.

Industry findings released during 2026 by the American College of Sports Medicine highlighted continued expansion of nutrition-supported fitness programs, reinforcing growing utilization of protein supplementation and functional nutrition across both athletic and general wellness populations.

Adults accounted for approximately 68% of total market demand in 2025, supported by high participation in fitness activities, preventive healthcare awareness, and increasing adoption of protein-rich nutritional products. Working professionals, recreational athletes, and health-conscious consumers continue driving consistent purchases across protein supplements and meal replacement categories. Professional Athletes remain an influential premium segment due to performance-focused nutritional requirements, while Bodybuilders and Fitness Enthusiasts maintain strong demand for specialized formulations with enhanced protein, amino acids, and recovery ingredients. Manufacturers continue strengthening this segment through premium formulations, customized nutrition plans, and digital wellness partnerships.

Fitness Enthusiasts represent the fastest-growing end-user segment as gym participation, home fitness adoption, and wearable health technologies continue expanding globally. Nearly 57% of new sports nutrition consumers now originate from lifestyle fitness rather than competitive sports backgrounds, broadening the industry's addressable market. Teenagers and Senior Consumers are also emerging as important customer groups seeking healthy aging, mobility support, and balanced nutrition. Companies are targeting these segments through age-specific formulations, personalized nutrition subscriptions, omnichannel distribution strategies, and influencer-driven education programs to strengthen customer acquisition and long-term engagement.

According to the 2025 consumer participation findings published by the International Health, Racquet & Sportsclub Association (IHRSA), continued growth in fitness club participation has strengthened demand for performance nutrition, recovery products, and convenient meal replacement solutions across diverse consumer demographics.

North America accounted for the largest market share at 35.9% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2026 and 2033.

Premium nutrition innovation and omnichannel retail strengthen market leadership

North America accounted for approximately 35.9% of the global Sports Nutrition and Meal Replacement Market in 2025, supported by a mature fitness industry, advanced food manufacturing infrastructure, and strong consumer demand for functional nutrition. Premium protein supplements, ready-to-drink beverages, and personalized nutrition products continue gaining traction across retail, e-commerce, and specialty nutrition channels. Nearly 69% of new product launches feature clean-label, plant-based, or clinically supported ingredients, while manufacturers continue expanding automated production facilities to improve operational efficiency. Companies are strengthening digital nutrition platforms, retailer partnerships, and ingredient traceability programs, enabling faster product commercialization while responding to increasing consumer expectations for transparency and scientifically validated nutrition.

United States Market Outlook: The United States remains the region's largest market through its advanced functional food ecosystem, extensive contract manufacturing network, and strong consumer adoption of sports nutrition products. More than 72% of premium nutrition brands actively expand personalized nutrition offerings supported by digital wellness applications and subscription-based purchasing models. Manufacturers continue investing in precision nutrition research, domestic production capacity, and strategic ingredient partnerships to strengthen innovation and maintain leadership across both sports performance and lifestyle nutrition categories.

Clean-label regulation drives premium product differentiation

Europe represented approximately 27.1% of the global market in 2025, supported by growing demand for functional foods, transparent ingredient labeling, and sustainable nutrition products. Consumers increasingly prioritize high-protein, sugar-reduced, and plant-based meal replacement solutions that comply with stringent food quality standards. Nearly 57% of premium product launches emphasize clean-label positioning alongside scientifically supported nutritional claims. Manufacturers continue investing in sustainable packaging, localized ingredient sourcing, and advanced formulation technologies to strengthen product differentiation while maintaining regulatory compliance across diverse consumer markets.

Germany Market Outlook: Germany leads the European market due to its strong food processing industry, advanced nutritional science capabilities, and high consumer awareness of preventive health. Functional protein products and meal replacement beverages continue expanding through pharmacy, retail, and digital commerce channels. More than 60% of premium nutrition manufacturers are increasing investments in plant-based protein innovation and sustainable production technologies, strengthening the country's position as a key product development and manufacturing hub.

Manufacturing expansion and health awareness accelerate regional demand

Asia-Pacific accounted for approximately 25.8% of the global market in 2025 and continues experiencing the fastest expansion through rising disposable income, urban lifestyles, and growing participation in fitness activities. China, Japan, India, and South Korea continue strengthening regional demand for protein supplements, functional beverages, and convenient meal replacement products. Nearly 63% of premium nutrition manufacturers have expanded regional production or distribution capabilities to support increasing domestic consumption. Companies are investing in localized product development, digital commerce partnerships, and advanced manufacturing technologies to improve supply flexibility and shorten product delivery cycles.

China Market Outlook: China remains the region's largest market through its expanding health-conscious consumer base, large food manufacturing capacity, and rapidly growing e-commerce ecosystem. Functional nutrition products continue benefiting from increasing participation in fitness activities and preventive healthcare initiatives. More than 65% of premium sports nutrition brands now prioritize digital retail channels and localized formulations, encouraging manufacturers to strengthen domestic production, ingredient innovation, and omnichannel distribution strategies.

Fitness participation stimulates premium nutrition demand

South America accounted for approximately 6.2% of the global market in 2025, supported by expanding fitness participation, increasing health awareness, and growing penetration of organized retail channels. Sports nutrition brands continue strengthening their presence through protein supplements, meal replacement beverages, and convenient nutritional snacks targeting active consumers. Nearly 41% of premium product expansion focuses on urban metropolitan markets where digital commerce adoption continues rising. Although import dependency influences ingredient costs, manufacturers are strengthening regional production partnerships and localized distribution to improve supply continuity and operational efficiency.

Brazil Market Outlook: Brazil dominates the regional market owing to its large fitness industry, expanding sports culture, and well-established nutritional supplement manufacturing sector. Strong consumer demand for protein products and functional nutrition continues supporting investment in local production facilities and retail expansion. Companies are increasing partnerships with gyms, sports organizations, and digital commerce platforms while expanding locally sourced ingredient utilization to strengthen competitiveness and improve market responsiveness.

Health investment and retail modernization support market development

The Middle East & Africa accounted for approximately 5.0% of the global market in 2025, driven by increasing investment in wellness infrastructure, premium retail formats, and preventive healthcare initiatives. Urban consumers continue adopting sports nutrition products as part of broader healthy lifestyle trends, particularly through modern retail and online sales channels. Nearly 38% of premium nutrition product launches focus on high-protein and functional wellness formulations. Manufacturers continue expanding regional distribution partnerships, halal-certified product portfolios, and localized marketing strategies to improve accessibility while strengthening long-term market penetration.

Saudi Arabia Market Outlook: Saudi Arabia leads regional growth through expanding wellness investments, rising fitness participation, and continued modernization of retail infrastructure. Demand for premium protein supplements and meal replacement products is increasing across fitness centers, pharmacies, and digital commerce platforms. More than 52% of premium nutrition brands have strengthened regional distribution partnerships or localized product portfolios, positioning the country as the primary commercial hub for sports nutrition expansion across the Middle East.

Global nutrition leaders including Glanbia, Abbott, Herbalife, Nestlé Health Science, and Danone compete directly with performance-focused brands and regional functional nutrition manufacturers through formulation science, brand credibility, and distribution scale. The top five companies collectively account for approximately 43% of the global market, creating a moderately consolidated competitive landscape. Competition increasingly centers on protein quality, clean-label innovation, ingredient traceability, and omnichannel availability rather than price alone. Premium formulations improve consumer retention by nearly 24%, while localized manufacturing reduces supply lead times by approximately 16% and diversified ingredient sourcing lowers procurement risk by 18%. Companies strengthen market positions through manufacturing expansion, ingredient partnerships, digital nutrition platforms, athlete collaborations, and vertical integration across sourcing and production. The competitive shift favors personalized nutrition and scientifically validated formulations over conventional mass-market products, while regulatory compliance and premium ingredient access remain key entry barriers. Winning requires trusted formulations, resilient supply chains, clinical differentiation, and strong consumer engagement.

Glanbia plc

Abbott Laboratories

Herbalife Ltd.

Danone S.A.

Nestlé Health Science

The Simply Good Foods Company

USANA Health Sciences, Inc.

GNC Holdings, LLC

MusclePharm Corporation

Amway Corporation

NOW Foods

THG Nutrition (Myprotein)

Advanced protein processing, precision fermentation, and AI-enabled nutrition personalization are transforming product development across sports nutrition and meal replacement categories. Precision filtration technologies improve protein purity by approximately 18%, while microencapsulation enhances nutrient stability by nearly 22%. More than 62% of premium product launches now incorporate functional bioactive ingredients, probiotics, or plant-based protein blends to deliver targeted health benefits. These technologies strengthen product quality, extend shelf life, and improve formulation consistency, enabling brands to differentiate through scientifically supported nutrition rather than conventional protein content alone.

Emerging technologies including precision fermentation, digital nutrition platforms, wearable health integration, and AI-powered dietary recommendations are replacing traditional one-size-fits-all nutrition models. Compared with conventional formulation approaches, AI-assisted personalization improves product recommendation accuracy by approximately 30% while reducing new product development cycles by nearly 20%. Premium nutrition companies benefit most because digital ecosystems increase customer retention, support subscription-based purchasing, and generate valuable consumer health insights that strengthen long-term competitive positioning.

Between 2026 and 2028, personalized nutrition, smart ingredient traceability, and biotechnology-derived functional proteins will redefine premium product development. Digital nutrition engagement is expected to exceed 55% among leading nutrition brands as connected wellness ecosystems become mainstream. Companies investing early in precision nutrition, sustainable ingredient innovation, and AI-driven consumer analytics will secure stronger market differentiation, improve operational efficiency, and establish long-term leadership as sports nutrition evolves toward individualized health optimization.

April 2024 Glanbia announced the acquisition of Flavor Producers for approximately USD 300 million, expanding its flavor solutions portfolio and strengthening formulation capabilities for functional nutrition products. Business impact: enhances innovation capacity and ingredient integration across nutrition brands. Source: Glanbia

September 2025 Glanbia agreed to sell its SlimFast U.S. business as part of a portfolio optimization strategy, sharpening its focus on higher-growth performance nutrition categories. Business impact: strengthens investment priorities around premium protein and sports nutrition brands. Source: Glanbia

March 2026 Danone agreed to acquire Huel in a transaction valued at approximately €1 billion, significantly expanding its position in complete nutrition and plant-based meal replacement products. Business impact: accelerates scale in premium functional nutrition and direct-to-consumer channels. Source: Reuters

May 2026 Herbalife launched its global "Fuel Like Ronaldo" campaign, leveraging more than 20 years of elite sports nutrition expertise to expand consumer engagement beyond professional athletes. Business impact: strengthens brand positioning in mainstream performance nutrition. Source: Herbalife

The report provides comprehensive analysis of the Sports Nutrition and Meal Replacement Market across protein supplements, meal replacement products, sports drinks, protein bars, energy bars, and energy gels. It evaluates demand across muscle building, weight management, performance enhancement, endurance nutrition, general wellness, and clinical nutrition applications while assessing adoption among adults, professional athletes, fitness enthusiasts, bodybuilders, teenagers, and senior consumers. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with detailed operational and competitive intelligence.

The study examines formulation innovation, clean-label product development, plant-based protein adoption, personalized nutrition technologies, and digital wellness integration alongside manufacturing trends and distribution evolution. It profiles leading industry participants while evaluating consumer purchasing behavior, ingredient sourcing strategies, deployment patterns, and competitive positioning. Strategic insights support investment decisions, product portfolio optimization, regional expansion planning, partnership evaluation, and identification of emerging growth opportunities expected to influence the global sports nutrition and meal replacement industry between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 44,254.8 Million |

|

Market Revenue in 2033 |

USD 85,624.7 Million |

|

CAGR (2026 - 2033) |

8.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Glanbia plc, Abbott Laboratories, Herbalife Ltd., Danone S.A., Nestlé Health Science, The Simply Good Foods Company, USANA Health Sciences, Inc., GNC Holdings, LLC, MusclePharm Corporation, Amway Corporation, NOW Foods, THG Nutrition (Myprotein) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |