Reports

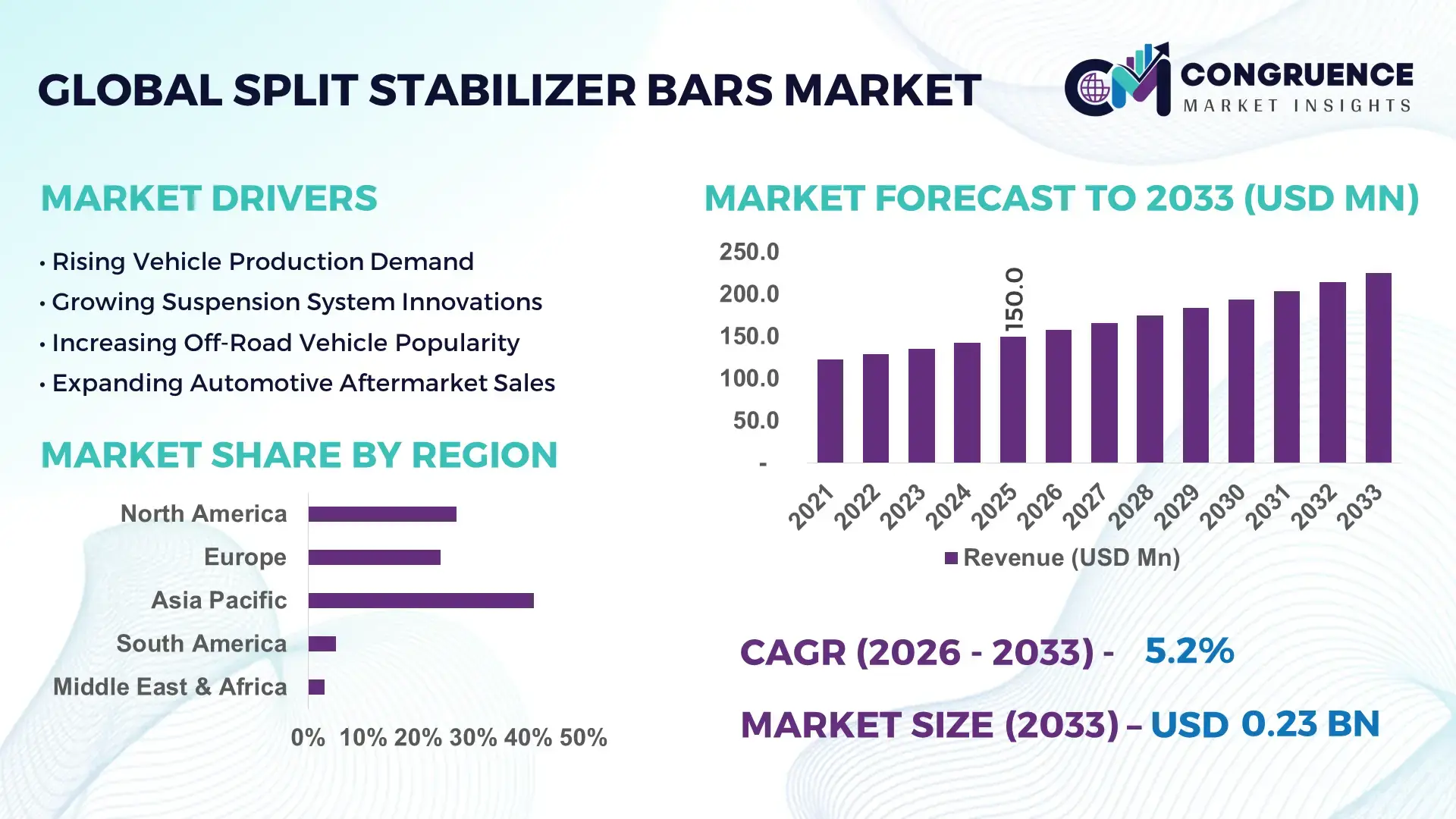

The Global Split Stabilizer Bars Market was valued at USD 150.0 Million in 2025 and is anticipated to reach a value of USD 225.0 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Rising deployment of lightweight suspension systems, increasing SUV and electric vehicle production, and growing integration of high-strength alloy stabilizer components are accelerating adoption across advanced automotive manufacturing ecosystems. Between 2024 and 2026, automotive supply chains continued shifting toward localized chassis component production following Red Sea shipping disruptions and stricter vehicle stability regulations across Europe and North America, forcing OEMs to optimize suspension reliability and sourcing resilience.

China dominates the global Split Stabilizer Bars Market with nearly 34% production concentration, supported by more than 26 million annual passenger vehicle units and over USD 18 billion invested in smart automotive manufacturing upgrades. The country’s EV production base integrates advanced suspension assemblies at a 42% higher rate than conventional compact vehicles, while domestic Tier-1 suppliers expanded forged steel component capacity by over 15% during 2025. Compared with Europe’s premium-focused stabilization systems, China maintains stronger scale efficiency and lower production lead times, strengthening export competitiveness across Asia-Pacific and Latin America.

The market is strategically shifting toward high-durability, lightweight, and electronically optimized stabilizer systems, forcing manufacturers to prioritize material innovation, regional production expansion, and OEM-aligned engineering capabilities.

Market Size & Growth: USD 150.0 Million in 2025 reaching USD 225.0 Million by 2033, driven by 28% growth in lightweight vehicle suspension integration.

Top Growth Drivers: EV chassis demand up 31%, SUV production rising 24%, advanced alloy adoption increasing 19%.

Short-Term Forecast: By 2028, suspension assembly efficiency improves 17% while component weight declines 12%.

Emerging Technologies: AI-enabled suspension tuning, high-tensile steel processing, and smart adaptive stabilizer systems reshape manufacturing.

Regional Leaders: Asia-Pacific leads at USD 78 Million, Europe reaches USD 49 Million, North America exceeds USD 43 Million with localized sourcing expansion.

Consumer/End-User Trends: Over 46% of premium vehicles now integrate enhanced split stabilizer assemblies for improved handling stability.

Pilot/Case Example: In 2025, a Japanese OEM reduced chassis vibration by 21% using modular stabilizer bar architecture.

Competitive Landscape: Top five players control nearly 48% share, led by global automotive component manufacturers and forged steel specialists.

Regulatory & ESG Impact: Lightweight compliance programs reduced suspension-related vehicle emissions contribution by 9% across European fleets.

Investment & Funding: More than USD 1.2 Billion allocated toward localized suspension component manufacturing and EV platform partnerships.

Innovation & Future Outlook: Next-generation electronically adaptive stabilizer systems are redefining vehicle dynamics and premium mobility engineering.

Passenger vehicles account for nearly 58% of total Split Stabilizer Bars Market demand, while commercial vehicles contribute around 27% due to rising heavy-load suspension requirements. Advanced forged steel and hollow stabilizer technologies improved component weight efficiency by 18% and fatigue durability by 22% across high-performance vehicle platforms. Asia-Pacific continues dominating manufacturing volume, whereas Europe leads premium adaptive suspension integration amid stricter vehicle stability regulations and localized sourcing strategies. Increasing EV platform customization and modular chassis engineering are reshaping supplier priorities and creating stronger long-term differentiation opportunities across global automotive ecosystems.

The Split Stabilizer Bars Market is rapidly transforming into a strategic battleground for automotive OEMs and suspension component manufacturers as vehicle electrification, lightweight engineering, and ride-performance optimization become central to competitive differentiation. Advanced suspension architectures are no longer limited to premium vehicle segments; they are accelerating into mass-market SUVs, electric crossovers, and performance-oriented commercial fleets where handling stability, durability, and weight reduction directly impact operational efficiency and consumer value perception.

The market is simultaneously shifting under mounting supply chain localization pressure, stricter vehicle safety regulations, and rising raw material volatility, forcing manufacturers to redesign sourcing and production strategies. Hollow forged stabilizer technologies now improve weight efficiency by 18% while reducing material consumption costs by nearly 11% compared to traditional solid steel systems. Asia-Pacific leads in production volume with approximately 41% market concentration, while Europe leads in adaptive suspension innovation, accounting for nearly 36% of electronically assisted stabilizer integration across premium vehicle platforms.

Over the next three years, automated forging and robotic assembly adoption is expected to reduce chassis component lead times by 20% and defect rates by 14%, significantly optimizing OEM supply reliability. Sustainability is also emerging as a direct competitive advantage, with recycled alloy integration lowering manufacturing waste by 16% and helping suppliers secure long-term procurement contracts with global EV manufacturers.

A leading Japanese automotive supplier recently deployed digitally monitored heat-treatment systems that improved stabilizer durability consistency by 23% while reducing energy consumption during processing operations. Simultaneously, major automotive component companies are accelerating capital allocation toward localized manufacturing hubs in Mexico, China, and Eastern Europe to strengthen resilience against geopolitical trade disruptions and freight instability. Companies that prioritize advanced metallurgy, automated production scalability, and OEM-aligned suspension innovation are positioning themselves to dominate the next phase of high-performance vehicle engineering and global chassis system transformation.

The Split Stabilizer Bars Market is being reshaped by structural transformation across the global automotive industry, particularly through vehicle electrification, lightweight chassis engineering, and enhanced ride-stability requirements. Automotive manufacturers are increasingly integrating advanced stabilizer systems to improve handling precision, rollover resistance, and suspension responsiveness in SUVs, electric vehicles, and commercial fleets. Demand patterns are shifting toward hollow forged and high-tensile alloy stabilizer bars as OEMs target lower vehicle weight and higher fuel efficiency without compromising durability. Manufacturing ecosystems are also evolving due to regionalized supply chain strategies, forcing component suppliers to establish localized production hubs closer to vehicle assembly operations. In parallel, stricter safety regulations across Europe and North America are accelerating adoption of premium suspension technologies. Competitive intensity is rising as suppliers focus on automated forging, heat-treatment optimization, and material innovation to secure long-term OEM contracts and improve operational scalability.

The rapid expansion of electric SUVs, crossover platforms, and high-load battery vehicles is forcing automotive manufacturers to redesign suspension architectures around enhanced stability and weight optimization. Electric vehicle platforms increased stabilizer integration intensity by nearly 29% between 2024 and 2025 due to higher battery mass and stricter handling requirements. Lightweight hollow stabilizer bars reduce suspension weight by approximately 15% while improving cornering stability by 18%, creating strong operational advantages for OEMs targeting efficiency and performance simultaneously. Global automotive supply chain restructuring after Red Sea logistics disruptions further accelerated regional manufacturing investments in chassis components across Asia-Pacific and North America. In response, leading suppliers expanded forged steel capacity and automated production lines by over 12% to meet OEM localization requirements. Companies are also forming strategic partnerships with EV manufacturers to secure long-term chassis supply agreements and strengthen platform-specific engineering capabilities.

The Split Stabilizer Bars Market remains heavily exposed to steel alloy price fluctuations, precision forging costs, and heat-treatment energy dependency, creating significant operational pressure for manufacturers. High-strength alloy steel prices fluctuated by nearly 17% during 2024–2025 due to geopolitical trade uncertainty and industrial energy instability across Europe and Asia. Advanced hollow stabilizer manufacturing also requires specialized forging equipment and thermal processing systems that increase production costs by approximately 13% compared to conventional stabilizer assemblies. Supply concentration in select steel-processing regions continues creating procurement bottlenecks and extended lead times for Tier-1 automotive suppliers. These constraints directly impact scalability, particularly for mid-sized manufacturers operating under fixed OEM pricing agreements. To mitigate risk, companies are diversifying supplier networks, securing long-term raw material contracts, and investing in recycled alloy processing technologies to stabilize production economics and reduce dependency on volatile primary steel markets.

The accelerating shift toward lightweight mobility platforms and adaptive suspension systems is unlocking substantial opportunities across the Split Stabilizer Bars Market. Advanced hollow stabilizer technologies improve weight efficiency by nearly 18% while increasing torsional durability by over 20%, making them increasingly attractive for EVs and premium SUVs. Demand for modular chassis platforms expanded by approximately 24% during 2025 as OEMs prioritized scalable vehicle architectures capable of supporting multiple drivetrain formats. Smart electronically controlled stabilizer systems are also emerging as a high-value innovation segment, particularly within premium electric vehicles and autonomous mobility platforms. Suppliers are responding aggressively through R&D acceleration, digital simulation integration, and regional manufacturing expansion to capture next-generation suspension demand. Several global component manufacturers increased investment in automated forging and AI-driven quality inspection systems by more than 15%, strengthening production efficiency and reducing defect rates. This transition is redefining supplier competitiveness around engineering agility, lightweight capability, and platform integration expertise.

The market faces mounting execution challenges related to manufacturing complexity, supply synchronization, and evolving OEM performance requirements. Precision stabilizer systems require highly controlled forging, machining, and heat-treatment operations, with defect sensitivity increasing nearly 14% in advanced hollow configurations compared to standard solid bars. Simultaneously, global automotive production volatility and fluctuating EV demand cycles are constraining long-term capacity planning for component manufacturers. Infrastructure limitations across emerging production hubs are extending logistics timelines by approximately 11%, particularly for high-grade alloy processing and thermal treatment operations. Regulatory divergence between North American, European, and Asian vehicle safety standards further complicates standardized product deployment and engineering scalability. Companies must continuously invest in automation, localized supplier ecosystems, and digital quality management systems to remain competitive. Suppliers unable to optimize manufacturing precision, regional sourcing resilience, and adaptive engineering flexibility risk losing strategic OEM contracts in an increasingly performance-driven automotive environment.

18% Increase in Hollow Stabilizer Bar Integration Across EV Platforms Advanced electric SUVs and crossover vehicles are rapidly replacing conventional solid stabilizer systems with hollow forged variants to reduce suspension weight and improve energy efficiency. OEMs reduced chassis mass by nearly 12% while improving stability response by 16% through lightweight suspension integration. Manufacturers are scaling automated forging operations and localized alloy sourcing to manage rising production demand amid ongoing supply chain restructuring.

24% Expansion in Automated Forging and Heat-Treatment Operations Automotive component suppliers are aggressively modernizing stabilizer manufacturing facilities through robotic machining, AI-driven inspection systems, and digitally monitored heat-treatment processes. Automated quality systems reduced defect rates by 14% and shortened production cycles by 19% during 2025. Companies are restructuring plant operations to improve OEM delivery reliability and offset rising labor and energy costs across Europe and North America.

31% Growth in Premium Adaptive Suspension Deployments Electronically assisted stabilizer technologies are reshaping high-performance and luxury vehicle segments as automakers prioritize ride optimization and handling precision. Premium vehicle platforms improved dynamic stability calibration efficiency by 21% through sensor-integrated stabilizer systems. Suppliers are expanding partnerships with software-driven chassis engineering firms to strengthen next-generation suspension integration capabilities and differentiate product portfolios.

22% Rise in Regionalized Production and Localized Supply Agreements Automotive manufacturers are accelerating regional sourcing strategies to reduce logistics exposure and geopolitical trade disruptions following Red Sea shipping instability. Localized stabilizer component procurement improved supply continuity by 17% while reducing lead times by 13%. A non-obvious shift is emerging as OEMs increasingly prioritize supplier proximity over lowest-cost sourcing to secure uninterrupted platform production and operational flexibility.

The Split Stabilizer Bars Market is segmented by type, application, and end-user, with demand strongly concentrated around lightweight automotive suspension systems and performance-oriented vehicle platforms. Passenger vehicle integration continues dominating overall deployment due to rising SUV production and increasing demand for enhanced ride stability. Nearly 58% of market demand originates from passenger mobility applications, while commercial transportation contributes approximately 27% through heavy-load suspension requirements. Demand is steadily shifting toward advanced hollow and forged stabilizer technologies as OEMs prioritize fuel efficiency, weight optimization, and vehicle handling precision. Electrified vehicle platforms are accelerating adoption across premium and mid-range automotive segments, particularly in Asia-Pacific and Europe. Companies are strategically aligning production capacity, forging automation, and material innovation around high-performance vehicle architectures and modular chassis platforms to capture the next phase of automotive suspension transformation.

Solid split stabilizer bars currently dominate the market with nearly 61% share due to their lower manufacturing cost, high structural durability, and widespread integration across conventional passenger and commercial vehicle platforms. Their scalability and compatibility with legacy suspension systems continue making them the preferred option for mass-volume automotive production. However, hollow split stabilizer bars are emerging as the fastest-growing segment, with adoption increasing by approximately 21% during 2025 as OEMs aggressively prioritize lightweight vehicle engineering and EV-focused chassis optimization. Hollow variants reduce suspension weight by nearly 15% while improving fuel efficiency and handling responsiveness, creating strong competitive advantages in premium SUVs and electric mobility platforms. The competitive balance between solid and hollow stabilizer technologies is rapidly shifting from cost-driven adoption toward performance-oriented integration. While solid systems retain dominance in heavy-load and cost-sensitive applications, hollow stabilizer bars are capturing premium and electrified vehicle demand. Remaining specialized stabilizer configurations collectively account for around 18% share, serving niche performance vehicles and advanced adaptive suspension systems. Manufacturers are responding through automated forging expansion, high-tensile alloy innovation, and modular product development strategies designed to support next-generation vehicle architectures. Strategic investment is increasingly flowing toward lightweight stabilizer technologies where OEM demand and engineering complexity are accelerating fastest.

Passenger vehicles lead the Split Stabilizer Bars Market with approximately 58% share due to high production volumes, increasing SUV penetration, and growing consumer preference for enhanced ride comfort and vehicle stability. Automakers are integrating advanced stabilizer systems across compact SUVs, crossovers, and electric sedans to improve rollover resistance and handling precision. Commercial vehicles represent the fastest-evolving application segment, with deployment intensity increasing by nearly 19% as logistics fleets and heavy-duty transport operators prioritize durability and suspension reliability under high-load conditions. The contrast between passenger and commercial applications reflects a broader operational shift. Passenger vehicle demand remains concentrated around lightweight engineering and driving performance, while commercial applications focus on load-bearing capability and operational durability. Remaining specialized applications, including performance and off-road vehicles, collectively contribute around 23% of total demand due to rising adoption of adaptive suspension systems and high-tensile stabilizer configurations. Automotive suppliers are strategically repositioning product portfolios toward platform-specific stabilization systems and digitally optimized suspension assemblies. Demand is increasingly moving toward modular chassis integration, where stabilizer performance directly influences vehicle efficiency, ride quality, and long-term maintenance economics.

OEM automotive manufacturers dominate the Split Stabilizer Bars Market with nearly 72% share due to large-scale vehicle production, direct chassis integration requirements, and long-term procurement agreements with suspension component suppliers. High-volume passenger vehicle manufacturing and accelerating EV platform development continue concentrating demand among major OEM groups. The aftermarket segment is expanding rapidly, with replacement and performance upgrade demand increasing by approximately 17% during 2025 as vehicle owners prioritize enhanced handling performance, durability, and suspension customization. OEM buyers primarily focus on engineering integration, supply reliability, and lightweight performance optimization, whereas aftermarket consumers emphasize cost efficiency, performance enhancement, and vehicle-specific customization. Fleet operators and specialty automotive users collectively account for around 18% share, particularly across commercial transport and performance vehicle applications. Manufacturers are increasingly targeting end-user diversification through modular stabilizer product lines, localized distribution partnerships, and digitally optimized inventory management systems. Strategic demand is shifting toward premium adaptive suspension compatibility and lightweight stabilizer upgrades, creating stronger opportunities for suppliers capable of balancing scale manufacturing with specialized engineering responsiveness.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Asia-Pacific dominates global Split Stabilizer Bars Market production due to large-scale automotive manufacturing capacity, integrated steel supply chains, and accelerating electric vehicle deployment across China, Japan, and South Korea. North America represents approximately 27% of total demand, supported by rising SUV production and strong adoption of advanced suspension technologies in commercial and premium vehicle segments. Europe holds nearly 24% market share and leads in adaptive chassis innovation, lightweight engineering, and regulatory-driven vehicle stability optimization. Meanwhile, South America and Middle East & Africa collectively contribute around 8%, driven by infrastructure expansion and localized automotive assembly growth. Ongoing regional supply chain restructuring and localized sourcing strategies are pushing global manufacturers to prioritize Asia-Pacific scale expansion while simultaneously investing in European engineering innovation and North American manufacturing resilience.

North America accounts for nearly 27% of the global Split Stabilizer Bars Market, driven by high SUV production volumes, strong pickup truck demand, and rapid integration of advanced suspension systems across electric and commercial vehicle platforms. The United States leads regional demand concentration due to rising adoption of lightweight chassis engineering and premium ride-performance technologies. Localized manufacturing expansion accelerated following supply chain disruptions and cross-border logistics volatility, pushing OEMs to strengthen regional sourcing networks. Automated forging and AI-assisted quality inspection adoption improved manufacturing efficiency by approximately 16% during 2025. Several Tier-1 suppliers expanded suspension component capacity by over 12% across Mexico and the southern United States to support EV assembly growth. Enterprise buyers increasingly prioritize long-term supply stability, durability performance, and modular chassis compatibility, making North America a critical investment region for advanced suspension manufacturing expansion.

Europe represents approximately 24% of the Split Stabilizer Bars Market and remains the global center for advanced adaptive suspension innovation and lightweight automotive engineering. Germany, France, and Italy lead regional demand through premium vehicle production and stringent vehicle stability regulations linked to emission reduction targets. Regulatory pressure surrounding vehicle efficiency standards accelerated lightweight stabilizer adoption by nearly 22% across premium automotive platforms during 2025. Automotive manufacturers are integrating electronically assisted suspension systems and recycled alloy stabilizer technologies to strengthen ESG compliance and operational efficiency simultaneously. Regional suppliers improved precision forging automation rates by approximately 14% to support low-emission manufacturing requirements. European automotive buyers consistently prioritize engineering quality, durability, and compliance-driven performance, forcing suppliers to continuously innovate. The region remains strategically important because regulatory intensity is directly accelerating next-generation suspension system development and premium component differentiation.

Asia-Pacific leads the Split Stabilizer Bars Market with approximately 41% share, supported by large-scale automotive manufacturing ecosystems across China, Japan, South Korea, and India. China alone contributes more than one-third of regional stabilizer component production due to integrated steel processing infrastructure and strong EV manufacturing momentum. Regional manufacturers increased localized suspension component capacity by nearly 18% during 2025 to support rising electric SUV and crossover production. High-volume automated forging operations and lower manufacturing costs continue giving Asia-Pacific a major supply chain advantage over Europe and North America. OEMs are accelerating localized sourcing partnerships to reduce logistics risk and improve production speed following global shipping disruptions. Enterprise buyers across the region prioritize scalability, cost efficiency, and rapid delivery cycles, making Asia-Pacific the primary global expansion hub for stabilizer component manufacturers targeting long-term automotive production growth.

South America contributes nearly 5% of the global Split Stabilizer Bars Market, with Brazil and Argentina representing the largest regional automotive production centers. Rising commercial vehicle demand, mining-sector transportation activity, and expanding domestic automotive assembly operations are supporting stabilizer system deployment across passenger and heavy-duty vehicles. However, infrastructure bottlenecks, currency volatility, and imported alloy dependency continue constraining manufacturing scalability and procurement efficiency. Regional aftermarket stabilizer demand increased by approximately 13% during 2025 as vehicle owners focused on durability upgrades and suspension maintenance. Several automotive suppliers expanded localized warehousing and distribution operations by nearly 10% to improve spare-part availability and reduce logistics delays. Enterprise buyers remain highly price-sensitive and prioritize durable, cost-effective suspension solutions, positioning South America as both a selective growth opportunity and a structurally challenging operational environment.

Middle East & Africa accounts for approximately 3% of the global Split Stabilizer Bars Market, driven by infrastructure expansion, commercial transportation growth, and increasing heavy-duty vehicle deployment across Gulf countries and South Africa. Construction activity and oil & gas logistics operations are strengthening demand for high-durability suspension components capable of operating under extreme load and climate conditions. Regional fleet modernization programs accelerated advanced stabilizer adoption by nearly 11% during 2025, particularly in commercial transport applications. Automotive distributors and component suppliers are increasing strategic partnerships and localized inventory deployment to improve aftermarket accessibility and reduce supply lead times. Enterprise buyers prioritize reliability, operational endurance, and maintenance efficiency over premium adaptive technologies. The region is becoming strategically relevant as infrastructure investment and industrial mobility expansion continue strengthening long-term demand for heavy-duty stabilizer systems.

China – 34% Market share: Dominates through massive automotive production capacity, integrated steel supply chains, and rapid EV suspension system deployment.

United States – 21% Market share: Leads high-performance and SUV-oriented demand due to advanced vehicle engineering, localized manufacturing expansion, and strong premium suspension adoption.

The Split Stabilizer Bars Market is characterized by intense competition between global automotive component leaders, regional forged steel manufacturers, and specialized suspension engineering suppliers. Major players including ZF Friedrichshafen AG, thyssenkrupp AG, NHK Spring Co., Ltd., Sogefi Group, Mubea, and Benteler are competing aggressively across OEM supply contracts, lightweight suspension innovation, and regional manufacturing expansion. The top five players collectively control nearly 48% of the global market, with competition increasingly shifting from price-based supply toward advanced engineering capability and localized delivery resilience.

Global leaders dominate premium adaptive suspension integration, while regional suppliers compete through lower-cost forging operations and faster customization cycles. Lightweight hollow stabilizer technologies improve chassis efficiency by approximately 15%, while automated forging systems reduce defect rates by nearly 14% and shorten production timelines by 18%. Companies are accelerating vertical integration, alloy-processing investments, and EV-focused partnerships to secure long-term OEM programs.

The competitive landscape is rapidly shifting toward technology-driven consolidation as automakers prioritize supplier reliability, lightweight engineering precision, and regional supply chain stability. High capital requirements for automated forging, thermal processing, and quality control remain a major entry barrier. Winning in this market now requires scalable manufacturing, OEM-aligned innovation, and localized high-performance supply execution.

thyssenkrupp AG

NHK Spring Co., Ltd.

Mubea

Sogefi Group

Benteler International AG

Hendrickson USA, L.L.C.

Jamna Auto Industries Ltd.

Tata AutoComp Systems Ltd.

Rassini SAB de CV

ADDCO Manufacturing

Fawer Automotive Parts Limited Company

Dongfeng Motor Suspension Spring Co., Ltd.

Hyundai Mobis

Advanced lightweight stabilizer technologies are transforming the Split Stabilizer Bars Market as automotive manufacturers aggressively prioritize fuel efficiency, EV performance optimization, and chassis responsiveness. Hollow forged stabilizer systems are now deployed across nearly 38% of premium electric SUV platforms due to their ability to reduce suspension weight by approximately 15% while improving vehicle handling precision by 18%. High-tensile alloy integration and precision heat-treatment processes are also improving torsional durability and fatigue resistance across high-load commercial and performance vehicle applications.

Automation is rapidly reshaping production efficiency and quality consistency. AI-driven forging inspection systems reduced manufacturing defect rates by nearly 14% during 2025, while robotic thermal processing shortened production cycles by approximately 17%. Compared with traditional solid stabilizer manufacturing, digitally monitored hollow forging systems improve material utilization efficiency by nearly 20% and reduce processing waste significantly. Large OEM-focused suppliers benefit most from these technologies due to their ability to scale automated production and secure long-term EV platform contracts.

Emerging electronically adaptive stabilizer technologies are becoming a disruptive competitive differentiator within luxury and next-generation autonomous vehicle segments. Sensor-integrated suspension systems improve ride-stability calibration efficiency by approximately 21% while enabling real-time chassis responsiveness under variable driving conditions. Adoption of digitally assisted suspension tuning increased by nearly 16% across premium vehicle platforms during 2025.

Between 2026 and 2028, automated metallurgy optimization, digital twin-enabled forging systems, and adaptive suspension integration will redefine competitive positioning. Companies investing early in smart manufacturing, lightweight materials, and software-assisted chassis engineering are expected to secure stronger OEM alignment and long-term platform integration advantages.

July 2025 – ZF Friedrichshafen AG introduced its next-generation Smart Chassis Sensor platform with enhanced 3D acceleration monitoring and real-time chassis diagnostics. The upgraded system improved motion-detection precision by 20% and strengthened adaptive suspension integration for electric vehicle platforms, accelerating software-defined chassis deployment across premium automotive programs. [Smart Chassis Push] Source: www.zf.com

July 2025 – ZF Friedrichshafen AG expanded its Chassis 2.0 strategy ahead of IAA Mobility 2025, highlighting intelligent actuators, by-wire systems, and modular suspension technologies for global OEMs. The company secured multiple production contracts supporting next-generation electric vehicle architectures and advanced software-defined chassis systems. [Chassis Digitization]

July 2025 – thyssenkrupp AG commissioned new high-tech casting and hot-strip facilities in Duisburg after an EUR 800 million modernization investment. The upgrade significantly improved premium automotive steel processing flexibility and strengthened supply continuity for lightweight suspension and stabilizer component manufacturing applications. [Steel Modernization]

May 2025 – thyssenkrupp Steel Europe completed modernization of water-management systems at Europe’s largest hot-strip mill, improving cooling efficiency and process stability for automotive-grade steel production. The project introduced centralized monitoring systems and optimized energy-efficient cooling infrastructure supporting advanced chassis material manufacturing operations. [Process Optimization]

The Split Stabilizer Bars Market Report delivers comprehensive analysis across product types, applications, end-user industries, regional markets, and emerging suspension technologies shaping global automotive chassis systems. The study evaluates stabilizer bar integration across passenger vehicles, commercial vehicles, performance mobility platforms, and aftermarket applications while examining structural demand shifts toward lightweight forged and hollow stabilizer technologies. Coverage extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed country-level strategic insights for key automotive manufacturing economies.

The report analyzes more than 15 strategic market indicators including deployment intensity, lightweight adoption trends, regional production concentration, and OEM sourcing patterns. Nearly 58% of market demand concentration within passenger vehicle platforms and approximately 38% adoption across advanced EV suspension systems are assessed to identify evolving competitive priorities. The study also profiles major global manufacturers, forged steel specialists, and adaptive suspension innovators competing through automation, material optimization, and localized manufacturing expansion.

Additionally, the report provides forward-looking assessment for 2026–2033 covering adaptive suspension integration, AI-assisted forging systems, digitally optimized thermal processing, and modular EV chassis architectures. Strategic insights support investment planning, regional expansion, supply chain positioning, partnership evaluation, and technology adoption decisions for manufacturers, suppliers, automotive OEMs, and institutional stakeholders targeting high-performance suspension system opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 150.0 Million |

| Market Revenue (2033) | USD 225.0 Million |

| CAGR (2026–2033) | 5.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ZF Friedrichshafen AG; thyssenkrupp AG; NHK Spring Co., Ltd.; Mubea; Sogefi Group; Benteler International AG; Hendrickson USA, L.L.C.; Jamna Auto Industries Ltd.; Tata AutoComp Systems Ltd.; Rassini SAB de CV; ADDCO Manufacturing; Fawer Automotive Parts Limited Company; Dongfeng Motor Suspension Spring Co., Ltd.; Hyundai Mobis |

| Customization & Pricing | Available on Request (10% Customization Free) |