Reports

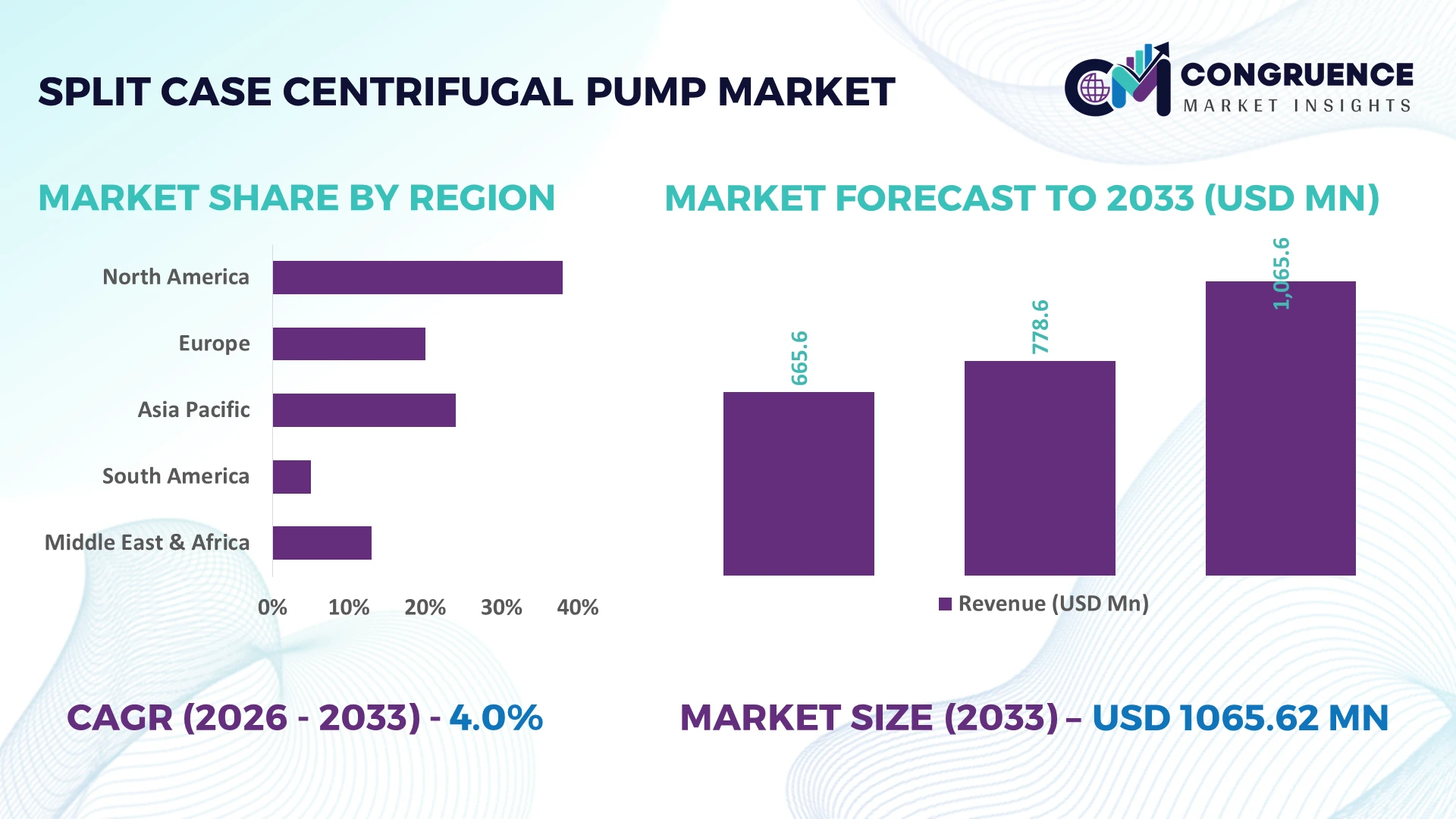

The Global Split Case Centrifugal Pump Market was valued at USD 778.64 Million in 2025 and is anticipated to reach a value of USD 1065.62 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. Growth is supported by expanding municipal water infrastructure, modernization of industrial pumping systems, and higher deployment of energy-efficient split case centrifugal pumps across power generation, irrigation, and wastewater treatment projects.

China leads the global Split Case Centrifugal Pump Market with approximately 31% manufacturing share, supported by large-scale water infrastructure, power generation, and industrial processing investments exceeding USD 20 billion annually. Compared with India, where municipal water projects are expanding rapidly, China maintains broader adoption of smart pump monitoring, with digital condition-monitoring integration exceeding 40% across major industrial installations despite evolving global supply-chain realignments.

The market favors manufacturers investing in energy-efficient designs, localized production, and digital asset monitoring to strengthen long-term competitiveness across infrastructure-driven procurement cycles.

Market Size & Growth: USD 778.64 Million (2025) to USD 1065.62 Million (2033) at 4% CAGR, driven by energy-efficient pumping upgrades across water and industrial infrastructure.

Top Growth Drivers: Municipal water projects (+28%), industrial modernization (+24%), and power sector upgrades (+19%) continue accelerating global installations.

Short-Term Forecast: By 2028, predictive maintenance platforms reduce unplanned downtime by 18% while improving operational efficiency by 14%.

Emerging Technologies: AI diagnostics, IoT-enabled condition monitoring, and advanced duplex stainless-steel components improve lifecycle performance and reliability.

Regional Leaders: Asia-Pacific USD 430 Million, North America USD 245 Million, Europe USD 205 Million, supported by infrastructure renewal and industrial automation adoption.

Consumer/End-User Trends: Over 52% of new municipal and utility procurements prioritize high-efficiency, digitally monitored centrifugal pumping systems.

Pilot/Case Example: A 2026 municipal water modernization project improved pumping efficiency by 17% while reducing maintenance interventions by 21%.

Competitive Landscape: Leading manufacturer holds approximately 15% market share alongside major global participants including Flowserve, KSB, Xylem, Sulzer, and Wilo.

Regulatory & ESG Impact: High-efficiency equipment standards lower electricity consumption by nearly 12% across upgraded pumping installations.

Investment & Funding: More than USD 1.6 billion supports manufacturing expansion, regional partnerships, and resilient supply-chain localization initiatives.

Innovation & Future Outlook: Smart digital twins, variable-speed integration, and predictive asset management strengthen next-generation infrastructure strategies.

Increasing investment in water transmission networks, district cooling, industrial utilities, and flood-control infrastructure continues expanding demand for advanced Split Case Centrifugal Pump Market solutions. Manufacturers are introducing intelligent monitoring platforms and higher-efficiency hydraulic designs that improve energy performance by nearly 15%. Growing localization of component manufacturing and stricter operational efficiency requirements are reinforcing resilient procurement strategies, setting the stage for the strategic discussion.

The Split Case Centrifugal Pump Market has become strategically important as governments and industrial operators prioritize resilient water infrastructure, energy optimization, and asset reliability. Infrastructure modernization and supply-chain restructuring are reshaping procurement strategies, with buyers increasingly favoring locally assembled, digitally monitored pumping systems over conventional equipment. This transition strengthens competitive positioning for manufacturers capable of delivering standardized products with shorter lead times and lifecycle support.

Modern split case centrifugal pumps integrated with variable frequency drives and IoT-based condition monitoring consume nearly 15% less electricity than legacy fixed-speed systems while reducing unplanned maintenance by approximately 20%. China continues scaling production through vertically integrated manufacturing, whereas Germany emphasizes high-efficiency engineering and predictive maintenance technologies for critical industrial applications. Over the next two to three years, digital monitoring adoption across newly commissioned municipal pumping stations is expected to exceed 45%, improving asset utilization and maintenance planning. Water treatment facilities replacing aging horizontal pumping equipment have already demonstrated measurable reductions in operating costs through intelligent performance optimization.

Manufacturers are expanding localized production, strengthening supplier partnerships, and increasing investment in digital service platforms to secure long-term contracts across utility and industrial sectors. ESG-focused infrastructure procurement is further encouraging high-efficiency pump deployment where lower energy consumption aligns with operating cost reduction targets. Companies combining advanced hydraulic engineering with predictive maintenance capabilities will secure stronger competitive differentiation, improve lifecycle value, and reinforce long-term market leadership.

Large-scale investment in municipal water systems, industrial utilities, and power infrastructure continues accelerating adoption of advanced split case centrifugal pumps. Nearly 58% of new utility tenders specify high-efficiency pumping equipment, while digital monitoring integration improves maintenance productivity by about 22% and reduces energy consumption by around 14%. India's nationwide water infrastructure expansion and continued industrial modernization in China are increasing procurement volumes for reliable pumping solutions. In response, manufacturers are expanding regional assembly facilities, strengthening engineering partnerships, and introducing standardized modular platforms that shorten delivery schedules. The structural shift toward lifecycle-based procurement is encouraging companies to compete through efficiency guarantees, predictive maintenance services, and long-term operational performance rather than equipment pricing alone.

Volatility in stainless steel, cast iron, and precision bearing prices continues pressuring manufacturing costs and procurement planning. Material expenses account for nearly 45% of production costs, while extended delivery times for specialized mechanical seals have increased project schedules by approximately 18% in selected industrial applications. Dependence on imported precision components remains a structural limitation for several developing manufacturing hubs. To reduce operational exposure, companies are localizing supplier networks, negotiating long-term procurement agreements, and qualifying alternative component vendors. Strategic inventory planning and diversified sourcing are becoming essential for maintaining delivery reliability, protecting project margins, and supporting consistent production during fluctuating global supply conditions.

The integration of intelligent diagnostics, cloud connectivity, and predictive analytics is creating new value beyond conventional equipment sales. Digital asset management platforms reduce maintenance interventions by approximately 25% while increasing equipment availability by nearly 16%. Japan and Singapore are advancing smart water infrastructure programs that encourage connected pumping assets capable of real-time operational optimization. Manufacturers are investing in embedded sensors, AI-enabled monitoring software, and service-based business models that generate recurring operational value. An emerging strategic opportunity lies in combining high-efficiency hydraulic designs with digital lifecycle services, allowing suppliers to differentiate through measurable operating performance instead of hardware specifications alone.

Deploying intelligent split case centrifugal pumping systems requires multidisciplinary expertise across mechanical engineering, automation, industrial networking, and cybersecurity. More than 35% of industrial operators report shortages of qualified maintenance personnel, while commissioning digitally integrated pumping systems typically extends implementation timelines by around 12% compared with conventional installations. Critical infrastructure operators also face increasing pressure to secure connected operational technology environments against cyber threats. Companies are responding through technical training programs, partnerships with automation specialists, and investments in standardized digital architectures that simplify integration. Organizations capable of combining workforce development with interoperable control platforms will achieve more consistent deployment quality and stronger long-term operational resilience.

Smart Predictive Maintenance Expansion Industrial operators are accelerating deployment of IoT-enabled monitoring, with connected pump installations increasing by nearly 32% and predictive diagnostics reducing unexpected failures by approximately 22%. Rising labor shortages and stricter uptime requirements are driving digital maintenance workflows. Manufacturers are expanding software partnerships and integrating remote asset management platforms to improve service responsiveness while strengthening recurring aftermarket business.

Localized Manufacturing Strategies Global supply-chain restructuring has encouraged manufacturers to regionalize production, reducing average equipment lead times by nearly 18% and lowering logistics costs by around 11%. India and Mexico continue attracting component manufacturing investments as procurement teams prioritize supply resilience. Companies are restructuring supplier networks, increasing local sourcing, and standardizing product platforms to improve delivery consistency without sacrificing engineering quality.

High-Efficiency Hydraulic Designs Demand for optimized hydraulic performance continues rising as redesigned impellers and advanced wear-resistant materials improve pump efficiency by approximately 14% while extending maintenance intervals by nearly 20%. Tightening industrial energy-performance standards are accelerating equipment replacement decisions. Manufacturers are increasing investment in computational fluid dynamics, advanced casting processes, and precision machining to differentiate through measurable lifecycle savings rather than acquisition cost.

Integrated Utility Automation Platforms Municipal utilities are increasingly connecting split case centrifugal pumps with SCADA and digital control environments, improving operational visibility by about 30% and reducing manual inspection workloads by approximately 25%. Water infrastructure modernization programs are reinforcing automation adoption. Equipment suppliers are strengthening automation partnerships, developing interoperable control architectures, and expanding lifecycle service portfolios to support long-term operational optimization.

Horizontal Split Case remains the leading segment, accounting for an estimated 46% of installed systems because of superior maintenance accessibility, high-flow capability, and dependable operation across municipal water supply and industrial utilities. Double Suction configurations continue strengthening this segment through balanced hydraulic loading, improved efficiency, and lower bearing wear during continuous-duty operations. Single-Stage pumps maintain strong adoption where moderate pressure and lower installation complexity are priorities, particularly across commercial infrastructure and standard utility applications.

Multi-Stage pumps represent the fastest-growing type as higher-pressure industrial processing, district water transmission, and energy facilities require greater discharge performance without excessive energy penalties. Adoption has increased by approximately 19% across new industrial installations, while Vertical Split Case systems continue gaining preference in facilities with constrained installation footprints. Manufacturers are expanding modular product families, improving hydraulic efficiency by nearly 15%, and investing in corrosion-resistant materials to address demanding operating environments. Product development increasingly focuses on digital monitoring compatibility and lifecycle optimization, shifting competitive investment toward high-performance engineered pumping solutions.

Water Supply remains the dominant application due to extensive deployment across municipal distribution networks, treatment facilities, and bulk water transfer infrastructure. Approximately 44% of installed split case centrifugal pumps operate within water supply systems, reflecting continuous investment in network modernization and operational reliability. Fire Protection maintains stable demand where dependable high-capacity pumping is mandatory, while Irrigation applications continue expanding alongside large-scale agricultural water management programs and reservoir distribution upgrades.

Industrial Processing is the fastest-growing application as manufacturing facilities require reliable, energy-efficient fluid movement for continuous production. Adoption of digitally monitored pumping systems has increased by approximately 23%, while automated process control improves operational efficiency by nearly 16%. Power Plants continue investing in high-capacity cooling water circulation systems with stricter efficiency targets and lower maintenance requirements. Manufacturers are responding through application-specific engineering, integrated monitoring solutions, and expanded service partnerships that improve equipment reliability across demanding industrial environments while strengthening long-term customer retention.

Water Utilities represent the largest end-user group because of continuous infrastructure renewal, network expansion, and growing emphasis on operational resilience. Roughly 41% of new procurement activity originates from utility operators seeking high-efficiency pumping systems capable of supporting uninterrupted water distribution. Municipalities remain a closely related demand center through wastewater modernization and flood-control infrastructure projects, while Agriculture continues investing in dependable high-volume irrigation systems that improve water delivery efficiency.

Energy is emerging as the fastest-growing end-user segment as thermal power stations, renewable energy facilities, and district cooling networks modernize pumping infrastructure. Deployment of intelligent monitoring solutions has increased by approximately 21%, while predictive maintenance programs reduce equipment downtime by nearly 18%. Industrial buyers continue emphasizing customized hydraulic configurations and lifecycle service agreements to optimize operational performance. Manufacturers are strengthening strategic partnerships, expanding localized engineering support, and introducing sector-specific product portfolios that improve competitiveness across mission-critical infrastructure and industrial applications.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Modern Infrastructure Renewal Drives Premium Pump Adoption

North America represents a mature market supported by water utility modernization, power infrastructure upgrades, and advanced industrial processing facilities. The region contributes approximately 24% of global demand, with utilities increasingly replacing aging pumping assets using digitally monitored, high-efficiency split case centrifugal pumps. More than 48% of new municipal procurement programs specify predictive maintenance capabilities and energy-efficient configurations. Industrial operators are expanding lifecycle service contracts while manufacturers strengthen engineering partnerships and localized assembly to improve project execution, shorten delivery cycles, and enhance long-term operational reliability across mission-critical infrastructure.

United States Market Outlook: The United States remains the regional leader due to extensive municipal water infrastructure, large industrial facilities, and continuous investment in resilient utility networks. More than 55% of large municipal upgrade projects incorporate intelligent pump monitoring and variable-speed operation to improve energy efficiency and asset performance. Domestic manufacturers continue expanding service networks, digital maintenance capabilities, and engineered product customization to support infrastructure rehabilitation and industrial modernization initiatives.

Efficiency Regulations Accelerate Equipment Modernization

Europe maintains a strong position through stringent energy-efficiency standards, industrial modernization, and water sustainability initiatives. The region accounts for approximately 22% of global deployment, with high adoption across municipal utilities, district heating systems, and manufacturing facilities. Modern hydraulic designs improve operational efficiency by nearly 15%, encouraging replacement of legacy pumping systems. Equipment suppliers increasingly integrate digital diagnostics and advanced materials while expanding strategic collaborations with engineering contractors to deliver optimized lifecycle performance and lower operating costs.

Germany Market Outlook: Germany leads the European market through advanced manufacturing capabilities, industrial automation, and strong engineering expertise. Approximately 46% of newly installed industrial pumping systems incorporate digital condition monitoring to optimize maintenance planning. Domestic enterprises continue investing in precision manufacturing, high-efficiency hydraulic technologies, and intelligent monitoring platforms that strengthen export competitiveness while supporting industrial decarbonization and infrastructure modernization objectives.

Manufacturing Scale and Infrastructure Expansion Strengthen Leadership

Asia-Pacific remains the largest regional market, supported by rapid industrialization, extensive municipal water investments, and expanding manufacturing capacity. The region contributes roughly 43% of global installations, with China and India driving large-scale deployment across utilities, irrigation, and industrial processing. More than 30% of newly commissioned water infrastructure projects integrate energy-efficient pumping technologies and automated monitoring systems. Manufacturers continue expanding localized production, supplier ecosystems, and engineering capacity to improve cost competitiveness while supporting infrastructure development and export demand.

China Market Outlook: China dominates regional production through integrated manufacturing clusters, extensive water infrastructure investment, and a mature industrial supply chain. Over 40% of large industrial pumping installations now incorporate intelligent monitoring platforms to improve asset utilization and maintenance efficiency. Domestic manufacturers are strengthening automation capabilities, expanding international distribution, and increasing investment in high-performance hydraulic technologies to reinforce global competitiveness across infrastructure and industrial markets.

Water Infrastructure Investment Supports Industrial Demand

South America continues expanding demand through municipal water upgrades, mining operations, agricultural irrigation, and industrial processing projects. The region contributes approximately 6% of global market activity, with infrastructure investment supporting higher deployment of reliable high-capacity pumping systems. Operational efficiency initiatives have improved pumping performance by nearly 13% across several modernization projects. Manufacturers are expanding distributor partnerships and regional service capabilities while balancing opportunities with infrastructure funding constraints and longer procurement timelines.

Brazil Market Outlook: Brazil represents the largest national market owing to extensive water utilities, mining activities, and agricultural irrigation requirements. More than 35% of recent infrastructure modernization projects prioritize energy-efficient pumping equipment capable of reducing operating costs and maintenance requirements. Companies continue strengthening local technical support, engineering partnerships, and application-specific product offerings to meet diverse industrial and municipal operating conditions.

Strategic Water Security Investments Accelerate Deployment

The Middle East & Africa market is advancing through desalination projects, urban infrastructure expansion, and industrial diversification strategies. The region represents approximately 5% of global installations while recording the strongest pace of new infrastructure deployment. Large water transmission and treatment projects have increased procurement of high-capacity split case centrifugal pumps by nearly 20% over recent implementation cycles. Manufacturers are expanding regional partnerships, technical service centers, and localized support capabilities to improve project execution and long-term equipment reliability under demanding operating environments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through large-scale desalination facilities, industrial cities, and strategic water infrastructure investment. Approximately 50% of newly commissioned water transmission projects specify high-efficiency pumping systems equipped with advanced monitoring capabilities. Equipment suppliers continue establishing local engineering partnerships, expanding maintenance services, and supporting localization initiatives that strengthen operational resilience while improving lifecycle performance across critical national infrastructure.

Global manufacturers including Flowserve, KSB, Sulzer, Xylem, and Wilo compete directly against regional engineering firms and cost-focused domestic producers, while OEMs increasingly challenge independent aftermarket suppliers through integrated lifecycle services. The top five players collectively control approximately 48% of the global market, leaving strong opportunities for specialized manufacturers in project-driven segments. Competition centers on hydraulic efficiency, delivery speed, lifecycle cost, and digital service capability rather than equipment pricing alone. High-efficiency pump designs reduce energy consumption by nearly 15%, predictive monitoring lowers maintenance interventions by around 20%, and localized manufacturing shortens delivery cycles by approximately 18%. Companies are expanding production facilities, forming engineering partnerships, investing in intelligent monitoring platforms, and strengthening vertical integration for critical components to improve supply resilience. Competitive pressure is shifting toward digitally enabled asset management and customized engineered solutions instead of standardized products. High engineering certification requirements, established service networks, and long-term procurement qualification remain major entry barriers. Winning requires superior lifecycle performance, responsive engineering support, localized supply capability, and measurable operational value.

Flowserve Corporation

KSB SE & Co. KGaA

Sulzer Ltd.

Xylem Inc.

Wilo SE

Ebara Corporation

Ruhrpumpen Group

Pentair plc

ITT Goulds Pumps

Kirloskar Brothers Limited

Shanghai Kaiquan Pump (Group) Co., Ltd.

Grundfos Holding A/S

C.R.I. Pumps Pvt. Ltd.

Torishima Pump Mfg. Co., Ltd.

Digital condition monitoring, intelligent sensors, and AI-assisted predictive maintenance have become standard technology priorities across advanced split case centrifugal pump deployments. Nearly 44% of newly specified utility pumping systems now include continuous performance monitoring, reducing unexpected failures by approximately 22%. Integrated IoT platforms provide real-time vibration, temperature, and hydraulic performance analysis, enabling operators to optimize maintenance schedules while improving equipment utilization and lowering service costs across critical infrastructure.

Advanced hydraulic engineering, computational fluid dynamics, precision casting, and variable frequency drive integration are replacing conventional fixed-speed pumping systems. Compared with legacy equipment, optimized hydraulic designs improve energy efficiency by approximately 15% while extending component life by nearly 18%. Global manufacturers with strong engineering capabilities benefit most because advanced digital integration creates higher switching costs and strengthens long-term service contracts. Intelligent digital twins are also supporting faster commissioning and performance optimization across complex industrial pumping applications.

Between 2026 and 2028, edge analytics, cloud-connected asset management, and cybersecurity-enhanced industrial control systems will reshape competitive differentiation. Adoption of digital lifecycle platforms is expected to exceed 50% among large infrastructure operators, improving maintenance planning and operational visibility. Companies investing early in interoperable automation, smart diagnostics, and modular high-efficiency designs will strengthen customer retention, reduce lifecycle operating costs, and secure a sustainable competitive advantage in infrastructure modernization programs.

January 2025 – Flowserve Corporation reported continued execution of its growth strategy, with aftermarket bookings increasing 10% to more than USD 680 million, strengthening lifecycle service capabilities for critical pump applications and reinforcing long-term infrastructure customer relationships.

April 2026 – KSB Limited expanded its Gamma and Omega horizontal split case pump portfolio by introducing new hydraulic and material variants, while advancing localization initiatives for water applications, strengthening domestic manufacturing capabilities and export competitiveness. Source: https://www.ksb.com

September 2025 – Flowserve partnered with Core Energy Systems to localize manufacturing of primary coolant pumps for India's nuclear sector following U.S. technology transfer approval, supporting domestic production and strengthening strategic energy infrastructure capabilities.

November 2025 – KSB highlighted accelerated innovation across its water and wastewater portfolio, including development of six additional KWP pump sizes during 2025, expanding application coverage for slurry, mining, and sewage operations while enhancing product competitiveness.

This report provides a comprehensive assessment of the Split Case Centrifugal Pump Market across Horizontal Split Case, Vertical Split Case, Single-Stage, Multi-Stage, and Double Suction configurations. It evaluates demand across water supply, irrigation, fire protection, power plants, and industrial processing while examining procurement patterns among water utilities, municipalities, industrial operators, agriculture, and energy sectors. Regional analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating deployment trends, technology adoption, and competitive positioning.

The study analyzes advanced technologies including predictive maintenance, IoT-enabled monitoring, variable frequency drives, and high-efficiency hydraulic systems, with digital monitoring adoption exceeding 40% across major infrastructure projects. It profiles leading manufacturers, competitive strategies, operational benchmarks, and investment priorities while identifying emerging opportunities in smart water infrastructure, localized manufacturing, and industrial modernization. The report supports expansion planning, product positioning, partnership evaluation, and strategic decision-making for the 2026–2033 market outlook through actionable business intelligence and segment-level analysis.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 778.64 Million |

Market Revenue in 2033 | USD 1065.62 Million |

CAGR (2026 - 2033) | 4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Flowserve Corporation, KSB SE & Co. KGaA, Sulzer Ltd., Xylem Inc., Wilo SE, Ebara Corporation, Ruhrpumpen Group, Pentair plc, ITT Goulds Pumps, Kirloskar Brothers Limited, Shanghai Kaiquan Pump (Group) Co., Ltd., Grundfos Holding A/S, C.R.I. Pumps Pvt. Ltd., Torishima Pump Mfg. Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |