Reports

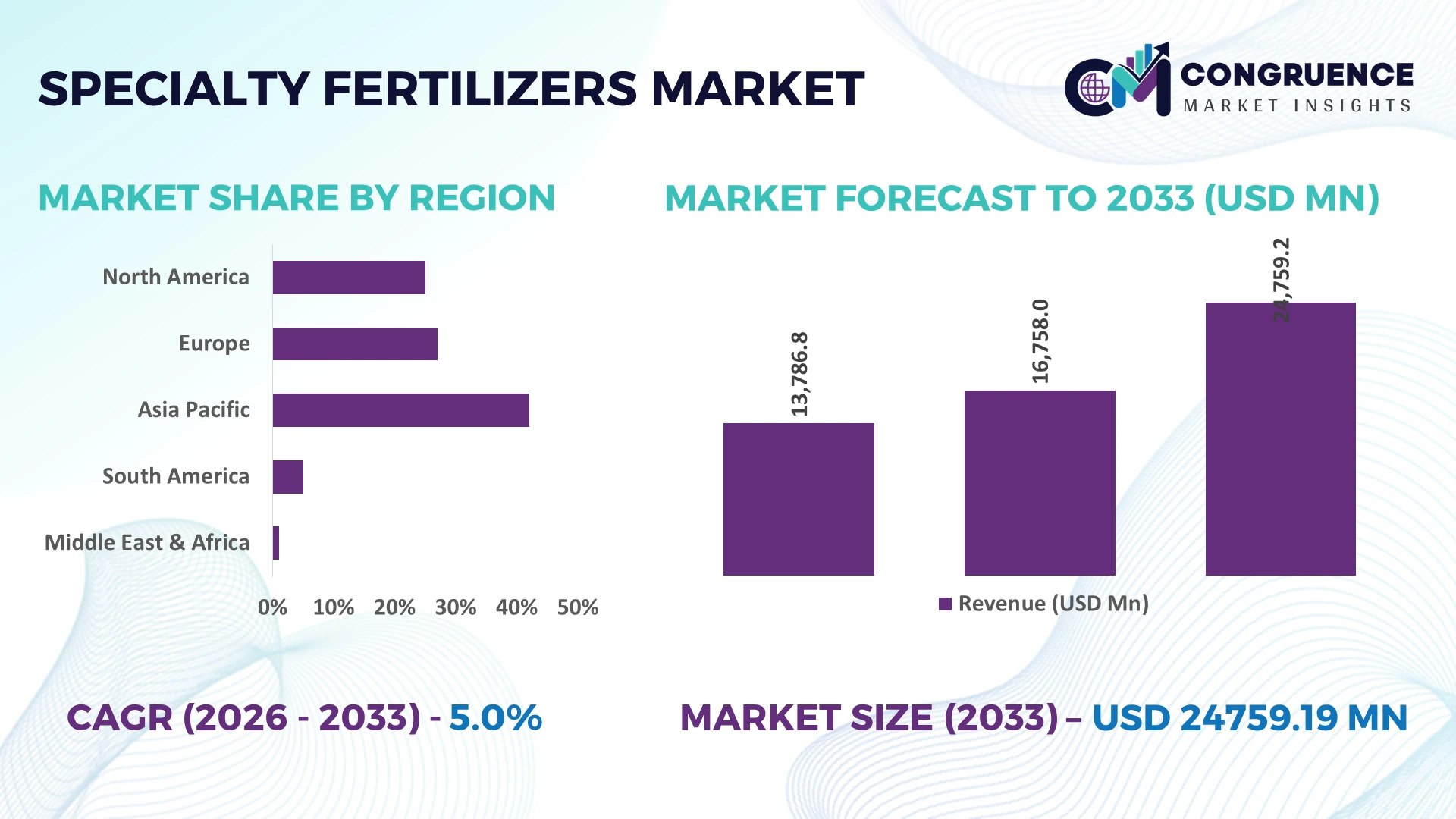

The Global Specialty Fertilizers Market was valued at USD 16758 Million in 2025 and is anticipated to reach a value of USD 24759.19 Million by 2033 expanding at a CAGR of 5% between 2026 and 2033.

Growth is driven by precision agriculture adoption, controlled-release nutrient technologies, expanding fertigation systems, and stricter nutrient-use efficiency regulations improving crop productivity while reducing fertilizer losses.

China leads the global specialty fertilizers market with approximately 29% production capacity, supported by large-scale horticulture, protected cultivation, and continuous investments in advanced nutrient manufacturing. More than 42% of high-value fruit and vegetable cultivation increasingly utilizes specialty nutrition solutions, outpacing India's adoption despite its larger agricultural workforce. Ongoing global supply-chain diversification following Red Sea shipping disruptions has accelerated regional production investments and procurement strategies across Asia.

Strategic investment in localized production, precision nutrient technologies, and resilient supply networks will define long-term competitive positioning across the global specialty fertilizers market.

Market Size & Growth: USD 16,758 million (2025) to USD 24,759.19 million (2033) at 5% CAGR, supported by precision farming and advanced nutrient management.

Top Growth Drivers: Precision agriculture adoption (+18%), fertigation expansion (+22%), controlled-release fertilizer usage (+16%) accelerate market growth.

Short-Term Forecast: By 2028, nutrient-use efficiency improves 14%, while fertilizer application costs decline nearly 10% through optimized formulations.

Emerging Technologies: AI-driven nutrient analytics, coated fertilizers, and digital farm monitoring increase application accuracy by over 20%.

Regional Leaders: Asia-Pacific exceeds USD 10 billion, Europe approaches USD 5 billion, North America surpasses USD 4 billion with precision farming expansion.

Consumer/End-User Trends: Nearly 48% of commercial horticulture growers increasingly adopt specialty fertilizers to improve crop quality and export consistency.

Pilot/Case Example: 2025 field programs achieved 17% higher nutrient efficiency and 12% lower fertilizer consumption through controlled-release technologies.

Competitive Landscape: Top suppliers collectively control nearly 45% market share, supported by product innovation and strategic manufacturing expansion.

Regulatory & ESG Impact: Nutrient-loss reduction programs improve nitrogen-use efficiency by approximately 15% while supporting sustainable agricultural practices.

Investment & Funding: More than USD 2 billion supports capacity expansion, technology partnerships, and regional manufacturing amid global supply-chain realignment.

Innovation & Future Outlook: Biostimulant integration, customized micronutrient blends, and smart fertilizer formulations strengthen high-growth precision agriculture strategies.

Specialty Fertilizers Market demand continues expanding across horticulture, greenhouse cultivation, high-value field crops, and precision farming systems where nutrient efficiency directly influences profitability. Advanced controlled-release coatings, water-soluble formulations, and micronutrient blends improve application efficiency by nearly 20%. Tightening environmental regulations and regional supply-chain optimization continue reshaping product development priorities, establishing a strong foundation for the strategic market discussion.

The specialty fertilizers market has become strategically important as agricultural producers prioritize higher nutrient-use efficiency, resilient food production, and precision input management amid tightening environmental standards. Supply-chain restructuring since recent logistics disruptions has encouraged localized manufacturing and diversified raw-material sourcing, reducing procurement risks while strengthening long-term competitiveness. These shifts are accelerating investments in advanced formulations, digital agronomy platforms, and integrated crop nutrition solutions that improve operational performance across commercial farming systems.

Modern controlled-release fertilizers improve nutrient-use efficiency by approximately 18% while reducing nutrient losses by nearly 25% compared with conventional granular fertilizers, lowering application frequency and improving farm economics. China leads large-scale manufacturing and protected cultivation deployment, whereas Brazil is rapidly expanding specialty fertilizer adoption across soybean and sugarcane production through precision agriculture investments. Over the next two to three years, digital nutrient management adoption is expected to exceed 40% among large commercial farming operations, supporting more consistent fertilizer optimization.

Commercial greenhouse operators increasingly integrate water-soluble fertilizers with automated fertigation systems, improving nutrient delivery precision while reducing labor requirements. In response, manufacturers are expanding regional blending facilities, investing in customized formulations, and strengthening technology partnerships with precision agriculture providers. Companies capable of combining localized production, digital agronomy capabilities, and differentiated specialty products will secure stronger competitive positioning and long-term operational advantage.

Precision farming and intensive cultivation continue transforming fertilizer application strategies as growers seek higher productivity with lower nutrient losses. More than 45% of commercial greenhouse operations now utilize specialty fertilizer programs, while controlled-release formulations improve nutrient-use efficiency by nearly 20% and reduce application frequency by approximately 15%. India's expansion of micro-irrigation and China's protected cultivation investments are reinforcing demand for advanced crop nutrition products. In response, manufacturers are expanding water-soluble fertilizer capacity, investing in customized micronutrient formulations, and partnering with digital agronomy providers. The strongest competitive advantage increasingly comes from integrated nutrient management solutions rather than standalone fertilizer products, improving customer retention and operational differentiation.

Price fluctuations in specialty nutrients, coating materials, and imported micronutrients continue challenging production economics across the value chain. Raw-material procurement costs have experienced swings exceeding 18%, while logistics expenses remain roughly 12% above pre-disruption levels in several importing markets. Countries dependent on imported potassium and specialty mineral inputs remain particularly exposed to shipping disruptions and currency volatility, affecting production planning and customer pricing. Companies are responding through localized blending facilities, long-term procurement agreements, diversified supplier networks, and greater use of regionally sourced inputs. Operational resilience increasingly depends on procurement flexibility rather than production scale alone, strengthening supply-chain competitiveness.

Digital crop intelligence and customized nutrition programs are opening new revenue opportunities beyond conventional fertilizer supply. AI-enabled nutrient recommendation platforms improve fertilizer utilization by approximately 16%, while variable-rate application technologies reduce unnecessary input use by nearly 14%. Brazil and India are expanding precision agriculture initiatives alongside government-supported irrigation modernization, creating favorable conditions for advanced specialty fertilizer deployment. Manufacturers are increasing R&D investment in bio-based formulations, smart nutrient coatings, and data-driven advisory partnerships that combine agronomic services with product sales. Companies building integrated ecosystems around digital farming capabilities are creating stronger customer relationships and premium product differentiation.

Maintaining consistent product quality across expanding production networks remains a significant execution challenge for specialty fertilizer manufacturers. Advanced coated formulations require highly controlled manufacturing conditions, while quality deviations above 5% can reduce field performance and customer confidence. Skilled technical workforce shortages approaching 20% in specialized fertilizer processing and stricter environmental compliance requirements increase operational complexity, particularly in emerging manufacturing hubs. Companies must strengthen automation, expand technical workforce development, and modernize quality assurance systems while investing in advanced production infrastructure. Long-term competitiveness will depend on reliable manufacturing consistency and scalable innovation rather than rapid capacity expansion alone.

Precision Nutrition Integration: Commercial farms are integrating specialty fertilizers with digital nutrient mapping and variable-rate application systems, improving nutrient placement accuracy by nearly 21% while reducing input waste by approximately 16%. Regulatory pressure on nutrient runoff and rising fertilizer optimization requirements are accelerating deployment. Companies are expanding agronomic software partnerships and integrating fertilizer recommendations with precision farming platforms to improve field-level decision-making and strengthen long-term customer engagement.

Localized Manufacturing Expansion: Manufacturers are restructuring production networks through regional blending facilities and localized micronutrient sourcing to reduce logistics risks. Average delivery times have declined by 18%, while inventory availability has improved by almost 15% across key agricultural markets. Supply-chain disruptions and trade uncertainties continue driving this shift. Companies are expanding domestic manufacturing capacity, strengthening supplier diversification, and redesigning procurement strategies to improve operational continuity and reduce dependency on imported specialty inputs.

Advanced Coating Technology Adoption: Polymer-coated and controlled-release formulations are replacing conventional nutrient delivery systems across high-value crops, improving nutrient-use efficiency by nearly 20% while lowering fertilizer application frequency by approximately 17%. Commercial greenhouse operators in the Netherlands and China are accelerating deployment through automated fertigation infrastructure. Manufacturers are investing in next-generation coating technologies, production automation, and collaborative product development to differentiate premium specialty fertilizer portfolios.

Crop-Specific Product Customization: Fertilizer manufacturers are expanding crop-specific nutrient formulations for fruits, vegetables, plantation crops, and protected cultivation, increasing product portfolio customization by nearly 24% while reducing nutrient imbalance by around 13%. Rising export-quality standards and intensive farming practices are driving this transition. Companies are strengthening agronomic advisory services, expanding formulation research, and establishing strategic partnerships with agricultural cooperatives to improve customer retention and operational efficiency.

Water-Soluble fertilizers remain the leading segment as they integrate efficiently with fertigation systems, precision irrigation, and protected cultivation, making them the preferred choice for high-value crop production. Nearly 48% of greenhouse fertilizer applications utilize water-soluble formulations because of their rapid nutrient availability and application flexibility. Controlled-Release fertilizers represent the fastest-growing segment, improving nutrient-use efficiency by approximately 20% while reducing application frequency by nearly 17%. Manufacturers are expanding customized nutrient blends and investing in advanced coating technologies to improve product differentiation. Liquid fertilizers continue gaining traction in mechanized farming, while Micronutrient fertilizers address increasing soil deficiency concerns. Slow-Release fertilizers maintain strategic importance for turf management and perennial crop cultivation where consistent nutrient release improves operational efficiency.

Investment priorities are shifting toward premium formulations that combine precision application with sustainability objectives. Companies are expanding production capacity, strengthening formulation research, and partnering with irrigation technology providers to develop integrated crop nutrition solutions. The market is steadily moving from standardized fertilizer offerings toward crop-specific, performance-oriented products that improve productivity while lowering operational complexity.

Fruits & Vegetables account for the largest application segment due to intensive nutrient requirements, greenhouse expansion, and growing demand for premium-quality produce. More than 44% of specialty fertilizer consumption is associated with high-value horticultural crops where nutrient precision directly influences yield and product quality. Plantation Crops represent the fastest-growing application as commercial cultivation of coffee, cocoa, tea, and oil palm increasingly adopts controlled nutrient management. Cereals & Grains remain a stable volume market, while Oilseeds & Pulses are benefiting from balanced micronutrient programs that improve soil fertility. Turf & Ornamentals continue expanding through urban landscaping and professional sports infrastructure requiring consistent nutrient performance.

Manufacturers are introducing crop-specific formulations, expanding agronomic advisory services, and integrating specialty fertilizers with precision irrigation systems to improve nutrient delivery efficiency. Investment strategies increasingly prioritize specialty solutions designed for export-oriented agriculture and commercial cultivation, where product consistency and operational efficiency deliver measurable competitive advantages.

Commercial Growers represent the dominant end-user segment because of large cultivation areas, advanced irrigation infrastructure, and continuous investment in precision nutrient management. Nearly 52% of premium specialty fertilizer purchases originate from commercial farming enterprises focused on maximizing yield consistency and input efficiency. Greenhouses are the fastest-growing end-user segment, with automated fertigation systems improving fertilizer-use efficiency by approximately 22% while reducing nutrient losses by nearly 18%. Farmers continue increasing adoption through government-supported precision agriculture initiatives, while Horticulture operations prioritize customized nutrient programs for premium crop quality. Agricultural Cooperatives are strengthening purchasing power by consolidating procurement and expanding technical advisory services for member farms.

Manufacturers are developing tailored product portfolios, expanding distributor partnerships, and introducing flexible pricing strategies for different cultivation systems. Companies are increasingly building integrated service ecosystems combining agronomic consulting, digital nutrient recommendations, and specialty fertilizer products to strengthen customer loyalty and long-term market positioning.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

Precision Agriculture Strengthens Premium Nutrient Adoption

North America represents a mature specialty fertilizers market driven by precision agriculture, advanced irrigation infrastructure, and commercial-scale farming operations. The region accounts for nearly 24% of global demand, supported by extensive adoption of controlled-release and water-soluble fertilizers across corn, soybean, and specialty crop production. More than 58% of large commercial farms now integrate precision nutrient management with GPS-enabled application technologies, improving fertilizer-use efficiency and operational planning. Companies continue investing in digital agronomy platforms, automated blending facilities, and crop-specific formulations while strengthening partnerships with precision agriculture technology providers to improve productivity and reduce nutrient losses.

United States Market Outlook: The United States leads regional demand through highly mechanized farming, extensive precision agriculture deployment, and continuous investment in specialty crop production. Nearly 65% of commercial precision farming operations utilize advanced nutrient management systems integrated with specialty fertilizers. Manufacturers are expanding domestic production capacity, developing customized fertilizer blends, and strengthening collaborations with agri-tech companies to improve application accuracy, supply resilience, and long-term operational efficiency.

Sustainability Policies Accelerate Product Innovation

Europe maintains a strong position through advanced environmental regulations, high-value horticulture, and widespread adoption of nutrient-efficient farming practices. The region contributes approximately 21% of global specialty fertilizer consumption, supported by increasing deployment of controlled-release technologies and precision fertigation systems. Nutrient management initiatives have improved fertilizer-use efficiency by nearly 18% across commercial cultivation. Manufacturers are investing in low-emission formulations, bio-based nutrient technologies, and localized production while modernizing manufacturing facilities to align with sustainability targets and evolving agricultural compliance requirements.

Germany Market Outlook: Germany remains the regional technology leader through advanced agricultural research, precision farming infrastructure, and strong manufacturing capabilities. Commercial growers continue expanding digital nutrient management programs, with automated fertilizer application adopted across approximately 48% of large-scale farming operations. Domestic producers are increasing investment in environmentally efficient formulations, coating technologies, and collaborative innovation programs supporting sustainable agricultural productivity.

Manufacturing Scale Drives Market Leadership

Asia-Pacific dominates the specialty fertilizers market through extensive agricultural production, large manufacturing capacity, and rapidly expanding precision farming initiatives. The region accounts for approximately 42% of global market activity, supported by intensive cultivation of fruits, vegetables, rice, and plantation crops. More than 50% of newly commissioned specialty fertilizer production investments are concentrated within the region, strengthening supply security and export competitiveness. Companies continue expanding localized manufacturing, advanced micronutrient production, and digital agronomy services to support commercial farming modernization and improve nutrient-use efficiency.

China Market Outlook: China represents the largest national market due to integrated fertilizer manufacturing, protected cultivation, and large-scale commercial agriculture. Nearly 60% of greenhouse cultivation utilizes specialty nutrient programs supported by automated fertigation technologies. Domestic manufacturers continue expanding advanced coating technologies, customized micronutrient production, and precision agriculture partnerships while strengthening export capabilities across Asian agricultural markets.

Commercial Agriculture Expands Premium Nutrient Demand

South America is experiencing rapid specialty fertilizer adoption as commercial agriculture intensifies across soybean, sugarcane, coffee, and fruit production. The region contributes roughly 9% of global demand while recording one of the fastest operational adoption rates for precision nutrient management. Controlled fertilizer programs have improved nutrient-use efficiency by approximately 19% across large commercial farming operations. Companies are strengthening regional distribution networks, expanding blending facilities, and partnering with agronomic service providers despite logistics challenges affecting fertilizer distribution into interior farming regions.

Brazil Market Outlook: Brazil dominates regional demand through its large-scale export-oriented agricultural sector and expanding precision farming infrastructure. Nearly 55% of commercial soybean operations increasingly utilize specialty fertilizers to improve nutrient efficiency and crop performance. Manufacturers are investing in localized production, strengthening dealer networks, and developing crop-specific nutrient programs that support productivity while reducing operational input losses across major farming states.

Modern Irrigation Supports Market Transformation

The Middle East & Africa market is steadily expanding through irrigation modernization, greenhouse agriculture, and government-supported food security initiatives. The region contributes nearly 4% of global specialty fertilizer demand, with increasing deployment of water-soluble fertilizers in water-constrained agricultural systems. Precision irrigation projects have improved fertilizer application efficiency by approximately 17% in commercial farming operations. Companies are expanding regional distribution infrastructure, investing in localized blending operations, and collaborating with irrigation technology providers to improve nutrient management under challenging climatic conditions.

Saudi Arabia Market Outlook: Saudi Arabia leads regional modernization through large-scale greenhouse investments, advanced irrigation infrastructure, and national food security programs. More than 45% of commercial protected cultivation projects incorporate specialty fertilizer programs integrated with automated fertigation systems. Businesses continue investing in controlled-environment agriculture, localized fertilizer distribution, and precision nutrient technologies to improve water-use efficiency and strengthen domestic agricultural production.

Global leaders including Yara International, ICL Group, K+S, Haifa Group, and Nutrien compete directly against regional formulation specialists and low-cost domestic manufacturers, while technology-focused innovators challenge commodity suppliers through precision nutrition solutions. The top five companies collectively control approximately 43% of the market, creating moderate concentration with strong differentiation. Competition increasingly depends on formulation performance, customized crop nutrition, and supply-chain resilience rather than pricing alone. Premium specialty products improve nutrient-use efficiency by nearly 20%, while localized production reduces delivery times by approximately 18% and customized formulations increase customer retention by around 15%. Leading companies are expanding regional blending facilities, pursuing distribution partnerships, integrating digital agronomy platforms, and strengthening vertical control over specialty raw materials. Competition is shifting toward technology-enabled crop-specific portfolios as regulatory standards tighten and growers demand measurable field performance. High R&D requirements, formulation expertise, and distribution infrastructure remain major entry barriers. Winning requires integrated agronomic services, localized manufacturing, innovation speed, and consistent product performance.

Yara International ASA

Nutrien Ltd.

ICL Group Ltd.

Haifa Group

K+S AG

EuroChem Group

SQM S.A.

OCI Global

Coromandel International Limited

Deepak Fertilisers and Petrochemicals Corporation Limited

The Mosaic Company

COMPO EXPERT GmbH

Koch Agronomic Services LLC

Grupa Azoty S.A.

Advanced coating technologies, water-soluble formulations, and precision fertigation systems currently define the specialty fertilizers market. Polymer-coated nutrients improve nutrient-use efficiency by nearly 20% while reducing application frequency by approximately 17% compared with conventional fertilizers. More than 45% of commercial greenhouse operations now integrate automated fertigation with specialty fertilizers, improving nutrient consistency and reducing labor intensity. Manufacturers investing in integrated formulation and application technologies achieve stronger product differentiation and higher customer retention through measurable agronomic performance.

Emerging technologies combine AI-driven nutrient recommendation platforms, remote sensing, soil analytics, and variable-rate application equipment to optimize fertilizer deployment. Digital nutrient management improves application accuracy by nearly 18%, while precision recommendations reduce unnecessary fertilizer consumption by around 15%. Compared with traditional uniform application methods, intelligent nutrient management delivers approximately 22% higher efficiency under intensive cultivation. Commercial growers and precision agriculture technology providers benefit most as integrated digital ecosystems strengthen operational planning and improve input utilization.

Disruptive innovation between 2026 and 2028 will center on biodegradable coating materials, bio-based specialty formulations, nanotechnology-enabled nutrient delivery, and predictive agronomic analytics. Manufacturers are integrating digital advisory services with customized fertilizer portfolios to strengthen competitive positioning and recurring customer relationships. Early adopters investing in smart nutrient technologies, automated manufacturing, and crop-specific formulation platforms will achieve faster product commercialization, stronger supply resilience, and sustained operational advantage in increasingly performance-driven agricultural markets.

March 2024: EuroChem Group inaugurated a state-of-the-art phosphate fertilizer complex in Brazil, strengthening regional specialty fertilizer production and supply capabilities. The new facility significantly expands domestic processing capacity, improving product availability for commercial agriculture and reducing import dependence.

August 2024: ICL Group signed a five-year distribution agreement with AMP Holdings in China valued at approximately USD 170 million for specialty water-soluble fertilizers, expanding fertigation product reach across high-value crops and reinforcing its strategic position in the world's largest fertigation market.

February 2025: Haifa Group introduced the Haifa Soluble DUO water-soluble fertilizer range for fertigation, enabling higher calcium application without additional nitrogen while offering two specialized formulations for intensive cultivation. The launch strengthens precision crop nutrition and sustainable production strategies.

April 2025: Yara International reported continued portfolio optimization alongside stronger crop nutrition deliveries, achieving a 47% increase in EBITDA excluding special items year over year. The operational improvements reinforce investment in premium specialty fertilizer solutions and global supply optimization.

The report provides comprehensive analysis across Controlled-Release, Water-Soluble, Liquid, Micronutrient, and Slow-Release fertilizers while evaluating demand across Cereals & Grains, Fruits & Vegetables, Oilseeds & Pulses, Turf & Ornamentals, and Plantation Crops. It also examines purchasing behavior among Farmers, Commercial Growers, Greenhouses, Horticulture, and Agricultural Cooperatives. The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating technology adoption, deployment patterns, manufacturing capabilities, and competitive benchmarking across more than 10 major market participants.

The study evaluates precision fertigation, controlled nutrient-release technologies, digital agronomy integration, customized formulations, and sustainable crop nutrition strategies shaping market evolution between 2026 and 2033. It highlights operational trends, regional investment priorities, product innovation, supply-chain developments, and adoption shifts supported by measurable deployment indicators. The report enables stakeholders to assess expansion opportunities, competitive positioning, portfolio optimization, strategic partnerships, and long-term investment priorities across established and emerging specialty fertilizer applications.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 16758 Million |

|

Market Revenue in 2033 |

USD 24759.19 Million |

|

CAGR (2026 - 2033) |

5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Yara International ASA, Nutrien Ltd., ICL Group Ltd., Haifa Group, K+S AG, EuroChem Group, SQM S.A., OCI Global, Coromandel International Limited, Deepak Fertilisers and Petrochemicals Corporation Limited, The Mosaic Company, COMPO EXPERT GmbH, Koch Agronomic Services LLC, Grupa Azoty S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |