Reports

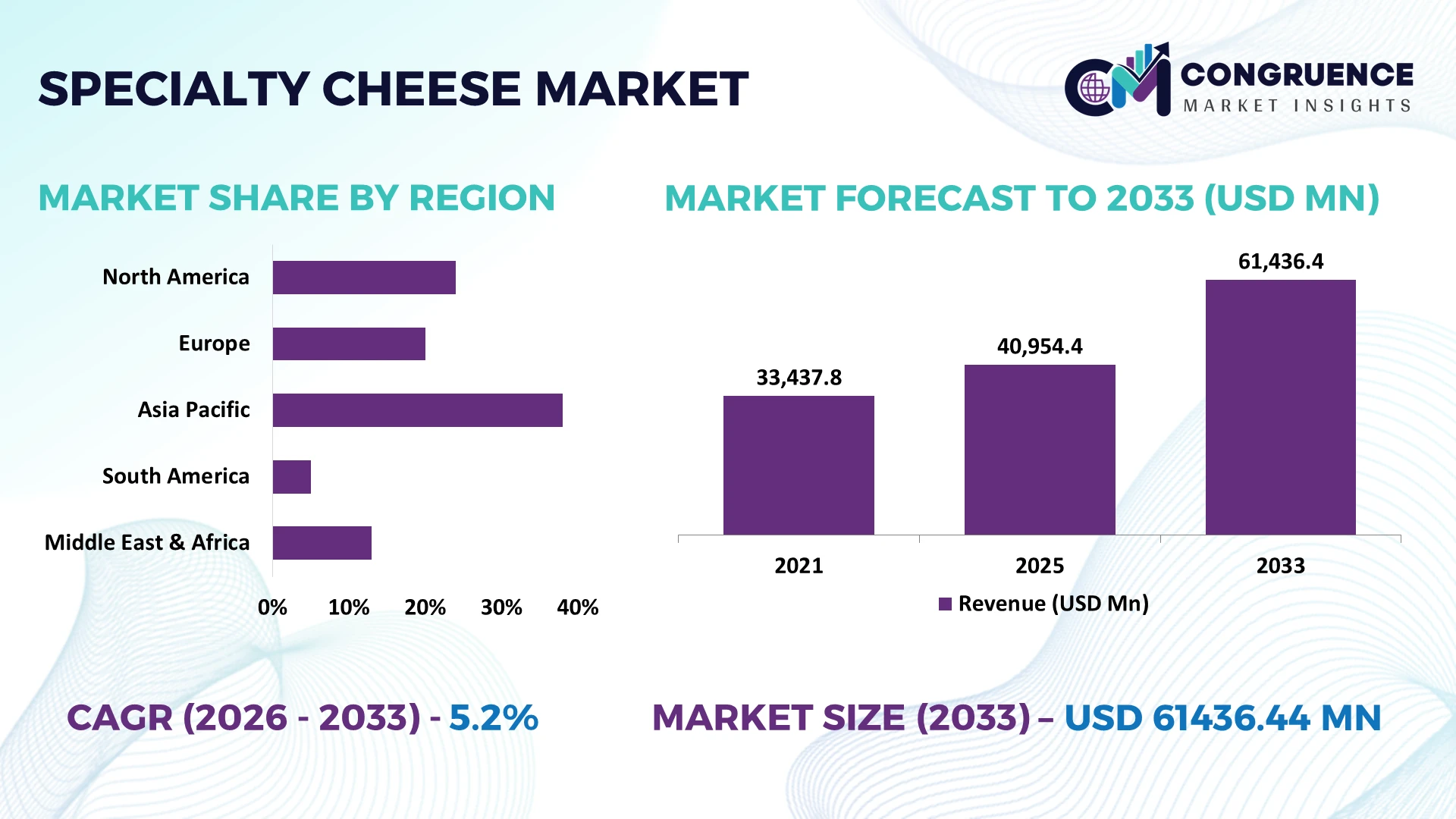

The Global Specialty Cheese Market was valued at USD 40954.36 Million in 2025 and is anticipated to reach a value of USD 61436.44 Million by 2033 expanding at a CAGR of 5.2% between 2026 and 2033. Growth is supported by premium dairy product innovation, protected-origin cheese production, expanding cold-chain logistics, and advanced fermentation technologies that improve quality consistency while extending product shelf life.

France remains the dominant specialty cheese producer, accounting for approximately 18% of global specialty cheese production, supported by more than 1,200 recognized cheese varieties, sustained dairy modernization investments, and advanced ripening technologies. Italy follows with nearly 13% production share, while the EU's protected geographical indication framework and evolving post-Brexit trade adjustments continue influencing premium cheese exports and cross-border supply strategies.

Strategic implication: Companies prioritizing premium regional portfolios, automated maturation facilities, and resilient export networks are positioned to strengthen market competitiveness across high-value international distribution channels.

Market Size & Growth: USD 40,954.36 Million (2025) to USD 61,436.44 Million (2033) at 5.2% CAGR, driven by premium cheese innovation and advanced cold-chain distribution.

Top Growth Drivers: Premium product demand (+24%), artisanal cheese consumption (+18%), and automated dairy processing adoption (+21%) continue accelerating global expansion.

Short-Term Forecast: By 2028, automated ripening systems improve production efficiency by 15% while reducing quality variation across premium cheese facilities.

Emerging Technologies: AI quality inspection, automated aging chambers, and precision fermentation improve consistency, traceability, and premium product development across advanced dairy operations.

Regional Leaders: Europe exceeds USD 26 Billion, North America approaches USD 16 Billion, and Asia-Pacific surpasses USD 11 Billion, supported by premium retail expansion and modern cold-chain infrastructure.

Consumer/End-User Trends: More than 42% of urban premium dairy consumers actively purchase specialty cheese through organized retail and digital grocery platforms.

Pilot/Case Example: In 2026, smart dairy processing deployment reduced product losses by 12% while improving production traceability across integrated manufacturing operations.

Competitive Landscape: The leading producer holds approximately 8% market share, while Lactalis, Saputo, Arla Foods, Bel Group, and Emmi strengthen competition through premium portfolio expansion.

Regulatory & ESG Impact: Sustainable dairy initiatives reduce processing emissions by nearly 14%, while stricter origin labeling strengthens premium product positioning across export markets.

Investment & Funding: More than USD 2 Billion supports dairy modernization, strategic partnerships, automated processing, and premium production capacity amid evolving global supply chain diversification.

Innovation & Future Outlook: Advanced cultures, precision fermentation, premium clean-label formulations, and digital traceability continue reshaping high-growth specialty cheese manufacturing strategies.

Specialty Cheese Market demand continues expanding across premium retail, foodservice, gourmet hospitality, and e-commerce channels as manufacturers introduce clean-label formulations, plant-assisted fermentation, and digital quality monitoring. More than 30% of premium product launches emphasize regional authenticity and sustainability, while evolving cold-chain optimization and stricter origin-label compliance strengthen international distribution efficiency, setting the foundation for broader strategic market evaluation.

The Specialty Cheese Market has become strategically important as premium dairy products evolve into high-value food categories supported by product differentiation, protected-origin branding, and advanced processing capabilities. Competitive advantage increasingly depends on resilient milk procurement, modern aging facilities, and digitally managed cold-chain logistics rather than production scale alone. Supply-chain restructuring across Europe and North America, combined with stricter geographical indication and food traceability regulations, is encouraging manufacturers to invest in localized processing and export-ready infrastructure.

AI-enabled quality inspection and automated ripening systems now reduce product quality deviations by nearly 18% while lowering manual inspection requirements by approximately 22% compared with conventional production methods. France and Italy continue leading premium cheese innovation through established protected-origin ecosystems, whereas South Korea and Japan are accelerating specialty cheese adoption through modern retail expansion and premium foodservice channels. Over the next two to three years, digital batch traceability adoption is expected to exceed 60% among large dairy processors, improving compliance and inventory optimization.

A practical example includes dairy producers integrating sensor-based maturation monitoring with predictive inventory planning to reduce product waste while maintaining flavor consistency. Companies are expanding partnerships with specialty milk suppliers, investing in sustainable processing technologies, and strengthening premium export portfolios to secure long-term differentiation. Organizations that combine operational efficiency, regional authenticity, and digital traceability will establish stronger competitive positioning across global specialty cheese value chains.

Premium consumer preferences and modernization of dairy processing continue strengthening specialty cheese production across established dairy economies. More than 35% of premium dairy product launches now emphasize artisanal recipes, clean-label ingredients, and protected-origin certification, while automated maturation technologies improve production consistency by nearly 20%. France continues investing in geographically protected cheese manufacturing, and advanced cold-chain infrastructure has reduced premium product losses by approximately 15% across major distribution networks. These structural improvements enable producers to supply premium retail and foodservice channels more efficiently. In response, leading manufacturers are expanding aging facilities, forming partnerships with regional milk cooperatives, and investing in digital quality monitoring to strengthen product differentiation and operational resilience.

Volatile raw milk prices and increasingly stringent food labeling requirements remain significant structural constraints for specialty cheese manufacturers. Feed and energy expenses account for nearly 40% of production costs in many European dairy operations, while compliance expenditures have increased by approximately 12% following tighter traceability and origin-label regulations. Export-oriented producers also face certification complexity across multiple international markets, extending commercialization timelines. These factors compress operating margins and complicate premium pricing strategies. Companies are mitigating risk through long-term milk procurement agreements, diversified sourcing across neighboring dairy regions, and localized packaging operations that reduce logistics exposure while improving regulatory responsiveness.

Precision fermentation, advanced microbial cultures, and digital supply-chain platforms are creating new opportunities for premium specialty cheese production. Automated process analytics improve manufacturing efficiency by approximately 17%, while predictive demand forecasting reduces inventory waste by nearly 14%. Switzerland and Denmark continue expanding research into functional cheese cultures that improve flavor consistency and production flexibility. Manufacturers are combining R&D investments with technology partnerships to develop premium formulations featuring cleaner ingredient profiles and enhanced traceability. An emerging strategic opportunity lies in digitally verified origin authentication, enabling premium exporters to strengthen consumer confidence and access high-value international retail channels with differentiated product positioning.

Maintaining artisanal quality standards during production expansion remains a major execution challenge for specialty cheese manufacturers. Skilled cheese-making professionals represent more than 25% of specialized production labor, while product maturation cycles often extend beyond 90 days, limiting manufacturing flexibility. Climate-related fluctuations affecting milk composition further complicate consistent flavor and texture development across production batches. These operational pressures increase quality management complexity and reduce scalability for premium producers. Companies must expand workforce training, deploy intelligent production monitoring, invest in climate-resilient dairy supply networks, and strengthen collaborations with research institutions to preserve product authenticity while achieving larger-scale commercial operations.

Digital Ripening Control Expansion Automated aging chambers integrated with AI-based environmental monitoring have increased by nearly 24% across large dairy processors, reducing maturation variability by approximately 18%. Rising labor shortages in France and stricter traceability requirements are accelerating deployment. Companies are expanding smart production facilities and integrating predictive quality analytics to improve batch consistency while lowering manual intervention across premium cheese manufacturing.

Premium Origin Labeling Focus Protected-origin certifications and digital product authentication have strengthened premium positioning, with authenticated specialty cheese portfolios expanding by nearly 20% and export-oriented producers reporting approximately 15% higher premium pricing realization. Regulatory tightening surrounding food origin transparency is driving investment in blockchain-enabled traceability. Manufacturers are restructuring supplier networks and strengthening regional partnerships to preserve authenticity while improving cross-border compliance.

Cold-Chain Network Optimization Modern refrigerated logistics systems have reduced distribution losses by around 14% while improving delivery reliability by nearly 17% for premium dairy products. Higher export volumes and evolving global supply-chain diversification are encouraging processors to redesign fulfillment networks. Companies are investing in automated warehouses, temperature-monitoring technologies, and integrated logistics partnerships to improve operational resilience and product freshness.

Sustainable Dairy Processing Integration Energy-efficient production equipment has lowered processing energy consumption by approximately 16%, while water recycling technologies reduce freshwater usage by nearly 12% across advanced cheese facilities. Increasing environmental compliance requirements and retailer sustainability standards are influencing procurement decisions. Companies are modernizing production assets, expanding renewable energy adoption, and collaborating with dairy cooperatives to strengthen long-term operational efficiency and premium brand competitiveness.

Parmesan remains the leading specialty cheese segment, representing approximately 29% of total market demand due to standardized production methods, extended shelf life, premium retail positioning, and widespread application across foodservice and packaged foods. Its scalable manufacturing processes and strong export acceptance support consistent commercial performance. Blue Cheese and Brie continue serving premium hospitality and gourmet retail channels, while Feta maintains stable demand through Mediterranean cuisine and convenience food applications. Manufacturers continue expanding protected-origin production and automated aging capacity to improve quality consistency.

Goat Cheese is the fastest-growing segment as health-conscious consumers increasingly seek distinctive flavor profiles and digestibility advantages. Adoption has increased by nearly 19% across premium retail assortments, while clean-label product launches have expanded by approximately 16%. Companies are introducing flavored variants, expanding artisanal production partnerships, and strengthening specialty distribution networks. The strategic shift toward premium differentiation is redirecting investment toward value-added cheese portfolios while maintaining established production capacity for mature categories.

Retail Consumption accounts for approximately 46% of specialty cheese demand, supported by supermarket expansion, premium private-label portfolios, and wider refrigerated distribution. Organized retail continues increasing premium shelf allocation, while digital grocery platforms have expanded specialty cheese availability by nearly 21%. Foodservice remains a mature application supported by premium restaurants and hospitality operators seeking differentiated menu offerings. Bakery Products maintain stable utilization through premium fillings and toppings.

Ready-to-Eat Meals represent the fastest-growing application as premium convenience foods integrate specialty cheese into value-added meal solutions. Product adoption has increased by approximately 18%, while automated food manufacturing has improved production efficiency by nearly 15%. Gourmet Cooking continues benefiting from rising home culinary experimentation and premium ingredient purchasing. Manufacturers are expanding retail-ready packaging, partnering with meal producers, and optimizing portion-controlled formats to strengthen operational efficiency and respond to evolving consumer purchasing behavior.

Households remain the dominant end-user segment, accounting for approximately 49% of specialty cheese purchases as premium grocery shopping, home entertaining, and healthier snacking continue expanding. Modern retail availability and wider refrigerated logistics support consistent household demand. Restaurants remain an important commercial buyer, while Hotels and Cafés increasingly incorporate specialty cheese into premium dining experiences to strengthen menu differentiation. Companies continue introducing smaller pack sizes and premium assortment strategies to improve consumer accessibility.

Food Manufacturers represent the fastest-growing end-user category as premium packaged foods and convenience meals integrate higher-value dairy ingredients. Procurement volumes have increased by nearly 20%, while customized ingredient solutions have expanded by approximately 17% across industrial food production. Manufacturers are strengthening long-term supply agreements, co-developing customized formulations, and expanding production partnerships to improve reliability and support premium product innovation. Competitive positioning increasingly depends on tailored ingredient solutions aligned with evolving industrial processing requirements.

Europe accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

Premium Manufacturing and Cold-Chain Optimization

North America represents approximately 28% of the global Specialty Cheese Market, supported by advanced dairy processing, premium retail penetration, and integrated refrigerated logistics. Manufacturers continue modernizing production through automated aging systems and digital quality monitoring to improve consistency across premium cheese portfolios. Foodservice recovery and expanding gourmet retail channels are increasing demand for differentiated cheese varieties. More than 65% of premium specialty cheese distribution is handled through temperature-controlled supply networks, while new investments in automated packaging have reduced processing downtime by nearly 14%. Companies are strengthening relationships with regional dairy cooperatives, expanding value-added product portfolios, and investing in traceability technologies to reinforce premium positioning and operational resilience.

United States Market Outlook: The United States leads regional specialty cheese production through a highly integrated dairy supply chain, advanced processing facilities, and broad premium retail distribution. Wisconsin and California remain major production hubs, supported by continuous investment in specialty cheese innovation and automation. More than 40% of domestic specialty cheese launches now emphasize clean-label formulations and premium flavor differentiation, while processors continue expanding direct partnerships with foodservice operators and national retailers to strengthen market competitiveness.

Protected-Origin Leadership and Premium Dairy Modernization

Europe remains the global production center for specialty cheese, contributing approximately 41% of market demand through established dairy infrastructure, protected geographical indications, and centuries of artisanal expertise. Investments in automated maturation facilities, digital traceability, and energy-efficient processing continue modernizing premium cheese manufacturing without compromising product authenticity. Nearly 30% of premium cheese exports originate from protected-origin categories, strengthening international competitiveness. Dairy enterprises are expanding export-focused production, modernizing cold-chain logistics, and integrating sustainability initiatives that improve operational efficiency while maintaining strict quality standards across premium product portfolios.

France Market Outlook: France remains the region's strategic leader through its extensive protected-origin ecosystem, diversified specialty cheese portfolio, and advanced dairy processing capabilities. The country produces more than 1,200 recognized cheese varieties while continuing investments in smart maturation technologies and export-oriented processing facilities. French producers increasingly combine traditional production methods with digital batch monitoring, enabling premium quality preservation while improving manufacturing efficiency across domestic and international distribution networks.

Premium Consumption and Processing Capacity Expansion

Asia-Pacific is emerging as the fastest-expanding specialty cheese marketplace as urbanization, premium food consumption, and organized retail networks reshape dairy purchasing behavior. The region accounts for approximately 19% of global demand, with rapid expansion across premium supermarkets, digital grocery platforms, and hospitality channels. Modern refrigerated logistics have improved premium dairy distribution efficiency by nearly 18%, supporting broader product availability. Manufacturers are establishing regional processing partnerships, expanding localized production, and introducing country-specific specialty cheese portfolios to reduce import dependence while improving supply responsiveness.

Japan Market Outlook: Japan remains the region's most strategically developed specialty cheese market through sophisticated cold-chain infrastructure, premium consumer preferences, and high food quality standards. Premium cheese utilization across hospitality and convenience food manufacturing continues increasing, supported by advanced packaging technologies and strong retail penetration. Automated food processing investments have improved production efficiency by approximately 15%, encouraging domestic manufacturers and international brands to strengthen premium product offerings.

Premium Dairy Diversification Across Domestic Markets

South America continues strengthening its specialty cheese industry through expanding dairy modernization, improving processing standards, and growing premium consumer demand. The region represents approximately 7% of global market activity, supported by established milk production and increasing investments in specialty dairy manufacturing. Modern refrigeration infrastructure has improved premium product distribution by nearly 13%, although logistics disparities remain across several rural production areas. Dairy companies are expanding processing partnerships, upgrading manufacturing facilities, and developing premium regional cheese portfolios to enhance value creation while improving export readiness.

Brazil Market Outlook: Brazil serves as the region's largest specialty cheese market due to its extensive dairy production capacity, expanding modern retail sector, and rising premium food consumption. Domestic processors continue investing in automated packaging, quality certification, and premium product innovation. Organized retail distribution now represents more than half of specialty cheese sales in major metropolitan markets, encouraging manufacturers to strengthen localized production and differentiated product development.

Retail Modernization and Premium Food Investment

The Middle East & Africa market is evolving through expanding premium retail infrastructure, hospitality investments, and improved refrigerated distribution systems. The region contributes approximately 5% of global specialty cheese demand, with premium imports supporting much of the current product mix. Modern cold-chain investments have increased premium product availability by nearly 16%, while hospitality expansion continues stimulating demand for imported and locally processed specialty cheeses. Companies are strengthening regional distribution partnerships, investing in packaging facilities, and exploring localized production opportunities to improve supply reliability and operational flexibility.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional specialty cheese consumption through premium retail expansion, international hospitality growth, and sophisticated food import infrastructure. Dubai continues serving as a regional distribution hub, supported by advanced cold-chain logistics and efficient trade connectivity. Premium specialty cheese availability has expanded significantly across supermarkets and luxury foodservice channels, encouraging international dairy companies to establish strategic partnerships and strengthen regional distribution capabilities.

The Specialty Cheese Market is led by Lactalis, Saputo, Arla Foods, Bel Group, and Emmi, competing directly against regional artisanal producers and protected-origin cheese manufacturers. The top five players collectively control approximately 38% of global market share, while regional specialists compete through authenticity and localized product portfolios. Competition centers on premium product differentiation, processing technology, and supply-chain reliability rather than price alone. Automated maturation systems improve production consistency by nearly 18%, digital traceability enhances compliance efficiency by approximately 20%, and optimized cold-chain logistics reduce distribution losses by around 14%. Global leaders continue expanding production capacity, securing long-term milk supply agreements, acquiring premium regional brands, and strengthening vertically integrated dairy operations. Regional producers respond through geographical indication certifications, specialty formulations, and partnerships with premium retailers. The competitive landscape is shifting toward supply control, digital quality assurance, and portfolio consolidation. High capital investment, strict food safety compliance, and specialized aging infrastructure remain major entry barriers. Sustainable sourcing, operational efficiency, premium innovation, and resilient distribution networks define lasting competitive advantage.

Lactalis

Saputo Inc.

Arla Foods

Bel Group

Emmi AG

FrieslandCampina

Savencia Fromage & Dairy

Fonterra Co-operative Group

Murray Goulburn Co-operative

Glanbia plc

Hochland SE

Groupe Sodiaal

Président

Castello

Digital transformation is redefining specialty cheese manufacturing through AI-enabled quality inspection, automated ripening chambers, and Industrial IoT monitoring. Nearly 48% of large dairy processors have deployed intelligent production monitoring, while automated environmental control improves aging consistency by approximately 18%. Compared with conventional manual maturation, sensor-driven systems reduce quality deviations by almost 20% and shorten inspection cycles by nearly 25%. Premium manufacturers benefit most through improved batch uniformity and reduced product waste.

Emerging technologies include blockchain-enabled traceability, predictive maintenance, and precision fermentation for advanced culture development. Digital traceability adoption exceeds 40% among export-focused producers, improving inventory accuracy and compliance efficiency by roughly 16%. Precision fermentation enables greater control of flavor development than conventional culture management while reducing process variability. Companies are integrating cloud-based production platforms with automated cold-chain monitoring to strengthen operational visibility and premium product authentication across international distribution channels.

Between 2026 and 2028, intelligent manufacturing platforms, robotic packaging, and digital twin process optimization will become major competitive differentiators. Early adopters are expected to achieve approximately 15% lower operating costs and 12% higher production efficiency than facilities relying on legacy production workflows. Manufacturers investing in integrated automation, predictive analytics, and sustainable processing technologies will strengthen operational resilience, accelerate premium product commercialization, and secure stronger positioning in increasingly quality-driven global specialty cheese markets.

August 2025 Lactalis signed an agreement to acquire Fonterra's consumer and associated businesses across Oceania, Southeast Asia, and the Middle East, covering operations in 8 countries. The acquisition strengthens premium specialty cheese manufacturing and regional distribution capabilities. Business impact: Expands production footprint and reinforces international market presence.

March 2026 Bel Group announced a USD 200 million expansion of its Brookings, South Dakota facility, doubling Mini Babybel production capacity from 10,000 to 20,000 tonnes annually. Business impact: Increases specialty cheese manufacturing capacity and strengthens North American supply resilience.

April 2026 Lactalis Canada commissioned a new milk receiving installation at its Winchester cheese facility, increasing milk intake capacity by 25%. Business impact: Improves production flexibility, supports higher specialty cheese output, and enhances operational efficiency.

January 2026 Emmi introduced its nutrition+ strategic platform while reporting 4.3% organic growth across its premium dairy portfolio. Business impact: Accelerates specialty cheese innovation and strengthens premium product competitiveness in international markets.

The Specialty Cheese Market report delivers comprehensive analysis across product types, applications, end-users, competitive positioning, technology trends, and regional performance. It evaluates Blue Cheese, Brie, Goat Cheese, Feta, and Parmesan while assessing demand across Retail Consumption, Foodservice, Bakery Products, Ready-to-Eat Meals, and Gourmet Cooking. The study also examines purchasing behavior among Households, Restaurants, Hotels, Cafés, and Food Manufacturers, covering more than 20 major producing and consuming countries with detailed operational and strategic insights.

The report provides in-depth assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting production modernization, digital traceability, automated maturation systems, cold-chain optimization, and sustainable dairy processing. It benchmarks leading companies, evaluates deployment trends, supply-chain developments, investment priorities, and innovation strategies to support market entry, capacity expansion, portfolio optimization, competitive positioning, and long-term business planning between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 40954.36 Million |

Market Revenue in 2033 | USD 61436.44 Million |

CAGR (2026 - 2033) | 5.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Lactalis, Saputo Inc., Arla Foods, Bel Group, Emmi AG, FrieslandCampina, Savencia Fromage & Dairy, Fonterra Co-operative Group, Murray Goulburn Co-operative, Glanbia plc, Hochland SE, Groupe Sodiaal, Président, Castello |

Customization & Pricing | Available on Request (10% Customization is Free) |