Reports

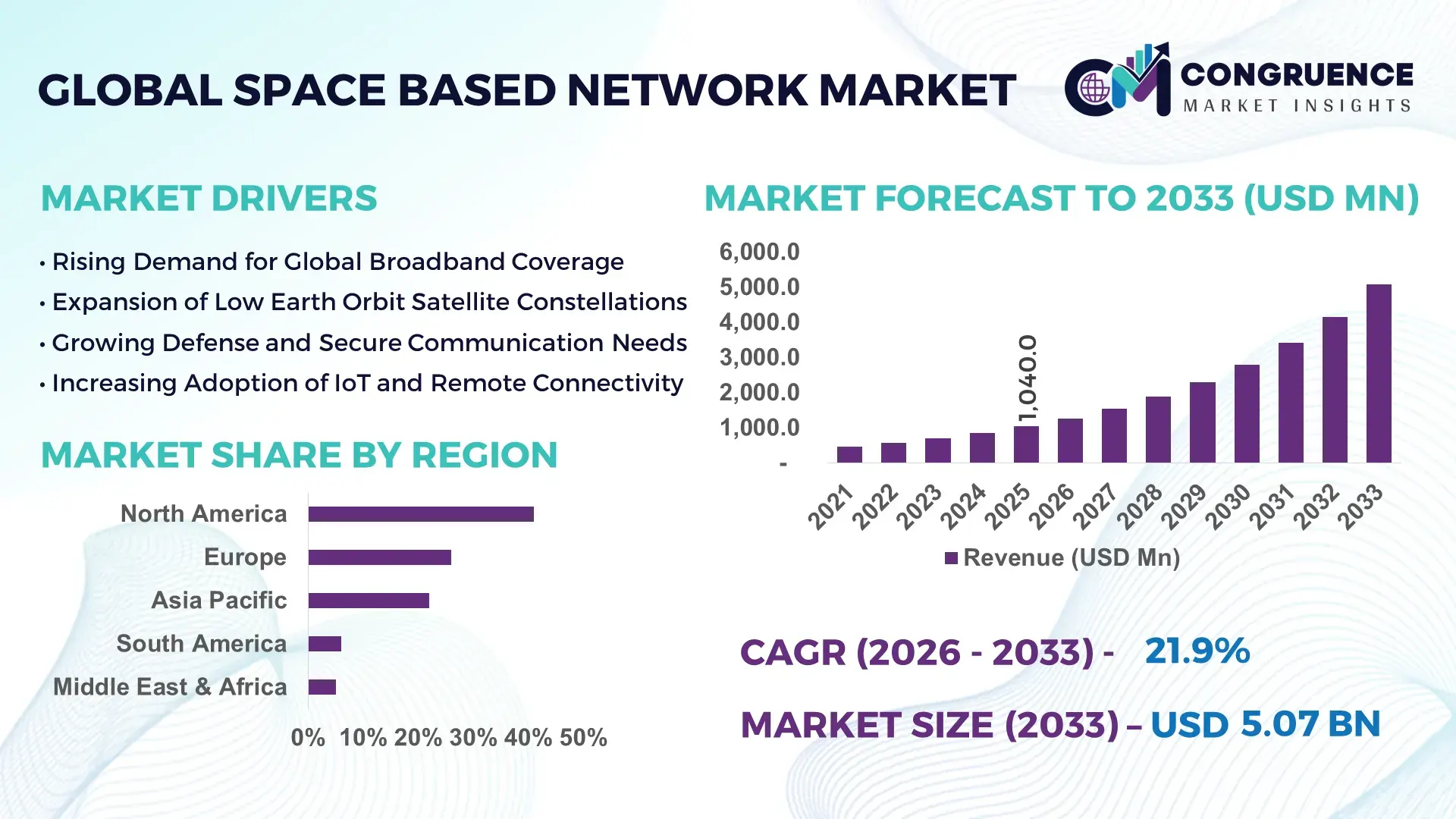

The Global Space Based Network Market was valued at USD 1,040 Million in 2025 and is anticipated to reach a value of USD 5,070.6 Million by 2033 expanding at a CAGR of 21.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by accelerating deployment of low-Earth orbit (LEO) satellite constellations and rising demand for resilient, low-latency global connectivity across commercial, defense, and industrial sectors.

The United States dominates the global Space Based Network Market in terms of ecosystem scale and technological depth. As of 2025, the country accounts for over 65% of active commercial LEO satellites, with more than 6,000 satellites launched or licensed for deployment. Annual public and private investment in space-based networking infrastructure exceeds USD 25 billion, supported by defense, broadband, and Earth observation applications. The U.S. also leads in advanced inter-satellite laser communication systems, with over 40% of operational satellites equipped with optical cross-links. Key applications include secure military communications, in-flight broadband, maritime connectivity, and IoT backhaul, with enterprise and government users representing more than 70% of total network utilization.

Market Size & Growth: Valued at USD 1,040 Million in 2025, projected to reach USD 5,070.6 Million by 2033, growing at a CAGR of 21.9%, driven by rapid satellite constellation expansion and demand for low-latency global connectivity.

Top Growth Drivers: LEO satellite adoption growth at 48%, latency reduction improvement of 62%, and global IoT backhaul integration increase of 39%.

Short-Term Forecast: By 2028, average network latency is expected to decline by 35% due to denser satellite mesh architectures.

Emerging Technologies: Optical inter-satellite links, AI-based network orchestration, and software-defined payloads.

Regional Leaders: North America projected at USD 1,980 Million by 2033 with defense adoption focus; Asia Pacific at USD 1,420 Million driven by rural broadband; Europe at USD 1,060 Million with strong aviation and maritime uptake.

Consumer/End-User Trends: Enterprise, defense, and mobility users account for over 68% of active network subscriptions.

Pilot or Case Example: In 2024, a U.S. LEO network pilot reduced maritime communication downtime by 41%.

Competitive Landscape: Market leader holds ~32% share, followed by major players including OneWeb, Amazon Kuiper, SES, and Telesat.

Regulatory & ESG Impact: Spectrum harmonization and space-debris mitigation standards influencing constellation design and deployment.

Investment & Funding Patterns: Over USD 18 billion invested globally since 2022, with rising venture funding for satellite-as-a-service models.

Innovation & Future Outlook: Integration of space-terrestrial networks and edge computing shaping next-generation connectivity architectures.

The Space Based Network Market spans defense communications (34%), commercial broadband (29%), aviation and maritime connectivity (21%), and industrial IoT backhaul (16%). Recent innovations include AI-driven traffic routing and laser-based cross-links improving throughput efficiency by over 50%. Regulatory emphasis on orbital sustainability and spectrum efficiency, combined with rising demand from remote regions in Asia Pacific and Africa, is shaping long-term adoption and future expansion pathways.

The Space Based Network Market has emerged as a strategic pillar of global digital infrastructure, enabling uninterrupted connectivity where terrestrial networks remain economically or technically unviable. Governments and enterprises increasingly view space-based networks as mission-critical assets for defense resilience, disaster recovery, aviation, maritime logistics, and remote industrial operations. From a strategic standpoint, low-Earth orbit architectures are redefining performance benchmarks; optical inter-satellite link technology delivers nearly 60% latency improvement compared to traditional radio-frequency relay systems, enabling real-time data transmission across continents.

Regionally, North America dominates in deployment volume, operating the highest number of active satellites, while Asia Pacific leads in adoption, with over 46% of new enterprise users integrating space-based connectivity for remote manufacturing, mining, and rural broadband use cases. In the near term, network virtualization and AI-driven traffic management are expected to reshape operational economics. By 2028, AI-enabled satellite network optimization is projected to reduce bandwidth congestion by 30%, improving service reliability for high-density users.

Compliance and ESG considerations are increasingly embedded in strategic planning. Operators are committing to orbital sustainability goals, including up to 40% reduction in end-of-life orbital debris risk by 2030 through controlled de-orbiting and reusable launch systems. A notable micro-scenario occurred in 2024, when a U.S.-based constellation operator achieved a 27% improvement in network uptime by deploying autonomous fault-detection algorithms across its satellite mesh. Looking forward, the Space Based Network Market is positioned as a foundation for resilient communications, regulatory compliance, and sustainable global connectivity growth.

The Space Based Network Market is shaped by rapid technological evolution, expanding satellite constellations, and growing demand for global, low-latency connectivity. Advances in launch cost efficiency, satellite miniaturization, and software-defined networking are accelerating deployment cycles and shortening time-to-service activation. Demand is increasingly driven by non-traditional users such as industrial IoT operators, mobility service providers, and emergency response agencies seeking coverage beyond terrestrial limits. At the same time, regulatory coordination for spectrum allocation and orbital management is influencing deployment strategies. Competitive intensity remains high as operators focus on differentiation through latency performance, network resilience, and integration with terrestrial 5G and edge computing ecosystems.

Rising demand for low-latency connectivity across aviation, maritime, defense, and remote enterprise operations is a primary driver of the Space Based Network Market. Modern LEO constellations deliver latency levels below 50 milliseconds, enabling real-time applications such as autonomous navigation, remote operations, and secure communications. Over 60% of global airlines and maritime fleets now evaluate satellite-based networks as core connectivity infrastructure rather than backup solutions. Industrial sectors increasingly rely on space-based networks to support continuous monitoring across geographically dispersed assets, improving operational continuity and decision-making speed.

Spectrum scarcity and orbital congestion present structural restraints for the Space Based Network Market. As of 2025, more than 8,000 active satellites operate in LEO, increasing collision-avoidance complexity and regulatory oversight requirements. Delays in cross-border spectrum coordination can postpone network activation by 12–18 months in certain regions. Additionally, compliance costs associated with debris mitigation, tracking systems, and licensing have increased operational expenditure by nearly 20% for new entrants, limiting rapid expansion for smaller operators.

Integration with terrestrial 5G and edge computing presents significant opportunities for the Space Based Network Market. Hybrid space-terrestrial architectures enable seamless connectivity across urban and remote environments, supporting applications such as smart logistics, connected vehicles, and remote healthcare. Over 45% of telecom operators are actively piloting non-terrestrial network integration to extend coverage footprints. Edge processing at ground stations reduces backhaul load by up to 33%, enhancing service quality and enabling new enterprise-grade service models.

High upfront deployment costs and complex lifecycle management remain key challenges. Although launch costs have declined by over 50% in the past decade, constellation deployment still requires multi-billion-dollar capital commitments. Satellite replacement cycles averaging 5–7 years necessitate continuous reinvestment. Additionally, managing thousands of satellites requires advanced monitoring, cybersecurity, and collision-avoidance systems, increasing technical complexity and operational risk for network operators.

Rapid Expansion of LEO Satellite Constellations: Operators increased active LEO satellites by over 70% between 2022 and 2025, enabling global coverage density improvements of nearly 45%. This expansion has reduced average signal handover time by 28%, significantly improving service continuity for mobility users.

Adoption of Optical Inter-Satellite Communication: More than 40% of newly launched satellites in 2024 were equipped with laser-based cross-links, improving data throughput by up to 60% and reducing reliance on ground relay stations by 35%, particularly for transoceanic data routing.

AI-Driven Network Management: AI-enabled traffic optimization systems are now deployed across approximately 38% of operational constellations, cutting network congestion incidents by 31% and improving fault detection response times by 44%.

Growing Enterprise and Government Utilization: Enterprise and government users account for nearly 68% of total network demand, with defense, disaster response, and industrial monitoring applications driving a 52% increase in high-priority data traffic requirements.

The Space Based Network Market is segmented by type, application, and end-user, reflecting the diverse operational models and demand profiles shaping adoption globally. From a type perspective, network architecture and orbital configuration determine latency, coverage density, and scalability, making segmentation critical for performance-driven decision-making. Application-wise, demand spans mission-critical communications, broadband access, mobility services, and emerging IoT backhaul use cases, each with distinct reliability and throughput requirements. End-user segmentation highlights varied adoption maturity, with defense and government agencies prioritizing resilience and security, while commercial enterprises focus on coverage expansion and service continuity. Together, these segmentation layers illustrate how technological capability, operational use case, and institutional priorities interact to define investment and deployment strategies across the Space Based Network Market.

The Space Based Network Market by type is primarily categorized into Low Earth Orbit (LEO) networks, Medium Earth Orbit (MEO) networks, Geostationary Orbit (GEO) networks, and hybrid/multi-orbit architectures. LEO-based networks currently lead the segment, accounting for approximately 58% of total deployments, driven by their ability to deliver sub-50 millisecond latency and higher bandwidth density. In comparison, GEO networks represent around 24%, valued for wide-area broadcast and legacy applications, while MEO systems hold nearly 10%, largely supporting navigation and regional connectivity. The remaining 8% comprises hybrid architectures that combine multiple orbital layers for resilience.

Among these, hybrid multi-orbit networks are the fastest-growing type, expanding at an estimated 24% CAGR, supported by demand for seamless handover between LEO and GEO systems, redundancy, and optimized cost-performance balance. Growth is driven by enterprise and government users seeking uninterrupted connectivity across varied geographies and mission profiles. LEO systems continue to evolve through inter-satellite laser links, while GEO platforms maintain niche relevance for high-throughput broadcasting and fixed infrastructure backhaul.

In 2025, a national space agency validated a multi-orbit satellite communication testbed that demonstrated a 32% improvement in network resilience during simulated outage scenarios.

By application, the Space Based Network Market spans defense and secure communications, commercial broadband and backhaul, aviation and maritime connectivity, Earth observation data relay, and IoT/M2M connectivity. Defense and secure communications dominate with approximately 34% application share, reflecting sustained demand for encrypted, resilient networks supporting surveillance, command, and emergency response operations. Commercial broadband and backhaul follow at around 29%, driven by rural connectivity initiatives and enterprise-grade global coverage requirements. Aviation and maritime connectivity account for nearly 21%, while Earth observation and IoT together contribute the remaining 16%.

The IoT/M2M connectivity application is expanding fastest, with an estimated 26% CAGR, fueled by asset tracking, environmental monitoring, and remote industrial automation. Adoption trends support this rise, as over 38% of global enterprises reported piloting satellite-enabled IoT platforms in 2025 to extend monitoring beyond terrestrial network reach. Additionally, more than 55% of maritime operators now rely on space-based connectivity as a primary communication channel, underscoring shifting usage patterns.

In 2024, a global aviation consortium reported that satellite-enabled in-flight connectivity systems improved real-time aircraft monitoring efficiency by 29% across long-haul fleets.

End-user segmentation in the Space Based Network Market includes government and defense agencies, commercial enterprises, telecom operators, transportation and logistics providers, and research and environmental institutions. Government and defense users lead with approximately 36% adoption, driven by requirements for secure, sovereign-controlled communication infrastructure. Commercial enterprises account for about 28%, increasingly integrating space-based networks into global operations, while telecom operators represent roughly 18%, leveraging satellites to extend coverage and support non-terrestrial networks. The remaining 18% includes transportation, logistics, and research entities.

The commercial enterprise segment is the fastest-growing end-user, expanding at an estimated 23% CAGR, supported by digital transformation, remote asset management, and global workforce connectivity needs. Adoption depth is notable, with over 41% of large enterprises deploying or testing satellite connectivity for redundancy and remote operations in 2025. Meanwhile, transportation and logistics users show strong penetration, with satellite-based tracking used by nearly 47% of international shipping operators.

In 2025, a multinational logistics provider deployed satellite-based network integration across its fleet, achieving a 35% reduction in communication outages during transoceanic operations.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24.6% between 2026 and 2033.

The regional landscape of the Space Based Network Market reflects varying levels of technological maturity, infrastructure readiness, and institutional demand. North America benefits from dense satellite deployments, strong defense spending, and early adoption of non-terrestrial networks, while Europe demonstrates steady expansion supported by regulatory coordination and sustainability mandates. Asia-Pacific is emerging as the most dynamic region due to rapid digitalization, large underserved populations, and state-backed space programs. South America and the Middle East & Africa collectively represent a smaller share but show rising demand for satellite-enabled connectivity in remote, maritime, and energy-intensive environments. Regional differentiation is also evident in application mix, enterprise adoption rates, and public-sector involvement.

North America represents approximately 41% of the global Space Based Network Market, supported by extensive satellite constellations and advanced ground infrastructure. Key demand originates from defense, aerospace, aviation, maritime logistics, and enterprise broadband applications. Government initiatives supporting non-terrestrial networks and space resilience programs continue to accelerate adoption, with over 70% of newly deployed satellites in the region equipped with inter-satellite communication capabilities. Digital transformation trends emphasize integration with 5G and edge computing, enabling hybrid connectivity models. A leading regional operator has focused on expanding laser-based satellite links, improving data throughput efficiency by nearly 55%. From a consumer and enterprise behavior standpoint, North America shows higher adoption among healthcare, finance, and defense enterprises, where secure, low-latency connectivity is a critical operational requirement.

Europe accounts for nearly 26% of the Space Based Network Market, with strong activity across Germany, the UK, and France. Regional growth is shaped by coordinated spectrum management, space sustainability initiatives, and cross-border connectivity programs. European regulatory bodies emphasize orbital debris mitigation and secure digital infrastructure, influencing constellation design and deployment practices. Adoption of emerging technologies such as software-defined satellites and encrypted communication payloads is increasing, with over 45% of newly launched regional satellites supporting flexible reconfiguration. A prominent regional satellite operator is advancing multi-orbit interoperability to support aviation and maritime corridors. Consumer and enterprise behavior in Europe reflects higher sensitivity to regulatory compliance and data transparency, driving demand for secure, explainable, and standards-aligned space-based networks.

Asia-Pacific ranks as the fastest-expanding region by volume, contributing around 22% of global deployments in 2025. China, India, and Japan are the top consuming countries, driven by national space programs, rural connectivity initiatives, and industrial digitization. Manufacturing and launch infrastructure in the region has expanded rapidly, with satellite production capacity increasing by over 40% in the past three years. Innovation hubs focusing on low-cost satellite platforms and AI-enabled network management are accelerating deployment timelines. A regional space enterprise has recently demonstrated constellation-scale automation, reducing operational intervention needs by 30%. Consumer behavior shows that growth is strongly driven by e-commerce platforms, mobile services, and digital public infrastructure, particularly in underserved and remote areas.

South America holds approximately 6% of the Space Based Network Market, with Brazil and Argentina as the primary contributors. Demand is closely tied to infrastructure development, energy operations, and remote connectivity needs across vast geographies. Satellite networks support oil & gas monitoring, agriculture analytics, and broadcast services, especially in regions lacking terrestrial coverage. Governments are encouraging satellite adoption through digital inclusion policies and cross-border connectivity agreements. A regional satellite service provider has expanded coverage to remote inland areas, increasing broadband accessibility for over 20% of previously unconnected communities. Consumer behavior in South America highlights demand linked to media distribution, language localization, and rural connectivity access.

The Middle East & Africa region represents about 5% of the global market, with demand driven by oil & gas operations, construction megaprojects, defense, and humanitarian connectivity. The UAE and South Africa are key growth countries, investing heavily in space infrastructure and satellite-enabled smart services. Technological modernization includes adoption of secure communication payloads and real-time monitoring systems. Regional regulations increasingly support public-private partnerships and cross-border satellite services. A Middle Eastern operator has enhanced offshore energy communications, reducing operational downtime by 28%. Consumer behavior varies widely, with strong reliance on satellite networks for remote industrial sites, mobility services, and emergency connectivity.

United States – 34% Market Share: Strong satellite deployment capacity, advanced defense demand, and deep private-sector investment in space-based connectivity.

China – 18% Market Share: High-volume satellite manufacturing, state-backed space programs, and expanding enterprise and public-sector adoption of non-terrestrial networks.

The Space Based Network Market exhibits a moderately consolidated competitive environment with 15+ active global competitors vying across orbital layers, connectivity applications, and technology platforms. Major players such as SpaceX’s Starlink, OneWeb (Eutelsat), Amazon’s Project Kuiper, SES, and AST SpaceMobile collectively represent an estimated ~55–60% combined operational influence due to constellation scale, subscriber base, and enterprise/government contracts. Starlink alone operates over 6,000 satellites and serves more than 6 million customers worldwide as of mid-2025, underscoring the intensity of competition.

Strategic initiatives shaping market dynamics include large mergers and acquisitions, such as SES’s acquisition of Intelsat consolidating GEO/MEO assets with broader multi-orbit capabilities, plus joint ventures like OneWeb with Airbus to co-develop next-generation satellites, enhancing manufacturing throughput and service delivery.

Innovation trends are central to competitive positioning, with firms prioritizing inter-satellite optical links, laser communication payloads, hybrid orbital architectures, and 5G non-terrestrial network (NTN) interoperability. Partnerships with terrestrial network providers — exemplified by Verizon’s collaboration with AST SpaceMobile to integrate space-based cellular services — reflect a broader push toward converged connectivity offerings.

Regional and application segmentation further influences competition: North America remains a stronghold due to defense, enterprise, and broadband demand, while Asia-Pacific and Europe see heightened activity driven by regional initiatives and sovereign connectivity programs. The increasing number of players and alliances indicates a dynamic competitive landscape where technology differentiation, constellation scale, and strategic collaborations are key determinants of market leadership.

SES S.A.

AST SpaceMobile

Intelsat

Iridium Communications

Viasat Inc.

Hughes Network Systems

Telesat

Inmarsat Global Limited

Airbus Defence and Space

Boeing

Globalstar

SKYLOOM

Mynaric

ICEYE Oy

The Space Based Network Market is undergoing rapid technological transformation driven by advancements in satellite platforms, networking capabilities, and integration with terrestrial systems. Low Earth Orbit (LEO) networks remain foundational, offering reduced latency and improved coverage, while Medium Earth Orbit (MEO) and Geostationary Orbit (GEO) systems provide complementary capabilities for high-throughput and wide-area connectivity. Inter-satellite communication is increasingly implemented via optical/laser links, enabling high-bandwidth data transfer and reduced dependency on ground stations. Mesh networking protocols and advanced phased-array antennas are standard features in new satellite designs, increasing throughput and resilience for mission-critical applications.

Emerging technologies include non-terrestrial network (NTN) 5G integration, which allows satellites to interoperate with terrestrial 5G infrastructure, enabling seamless connectivity for mobile devices without legacy ground constraints. Advanced beam-hopping and dynamic allocation algorithms improve spectrum efficiency and service quality, particularly in high-demand corridors. Hybrid network orchestration software, often leveraging AI, is used to optimize traffic between space and ground segments, reducing congestion and enhancing user experience. Ground segment innovations — including automated tracking, cloud-native payload processing, and secure edge data centers — are equally pivotal for scaling services to global consumers and enterprises.

Additionally, quality-of-service enhancements such as encryption, secure key management, and resilient link protocols are critical for defense, financial services, and industrial IoT use cases. CubeSat and small satellite platforms contribute to cost-effective deployment strategies, supporting rapid constellation expansion and niche service offerings. As satellite networking evolves toward higher speeds and lower latencies, integration with terrestrial fiber and radio systems will define the next era of global connectivity.

• In February 2025, Eutelsat completed the world’s first 5G non-terrestrial network (NTN) trial using OneWeb LEO satellites, advancing satellite-to-5G interoperability and expanding broadband access potential to remote areas. Source: www.reuters.com

• In October 2025, Verizon announced a strategic partnership with AST SpaceMobile to deliver space-based cellular services starting in 2026, integrating satellite and terrestrial networks to extend low-band coverage in underserved regions. Source: www.apnews.com

• In October 2025, AST SpaceMobile announced a successful space-based direct-to-cell connectivity test in partnership with Bell Canada, triggering a share price surge of nearly 12 % and demonstrating tangible progress toward commercial cellular broadband from orbit. Source: markets.financialcontent.com

• In mid-2025, SpaceX accelerated its Starlink V2 mini satellite rollout, launching 28 satellites equipped with advanced phased arrays and high data throughput to enhance global broadband connectivity, particularly in underserved markets.

The Space Based Network Market Report provides a comprehensive examination of the industry’s structure, segmentation, technologies, regional dynamics, and competitive landscape. It encompasses detailed categorizations by orbital type — including LEO, MEO, and GEO platforms — and evaluates how different architectures address specific connectivity needs such as broadband access, mobile backhaul, IoT support, and secure communications. The report covers technological themes like inter-satellite optical links, phased-array antennas, NTN/5G convergence, mesh networking, and ground segment automation, offering insights into how these innovations shape deployment strategies and service differentiation.

Geographically, the report analyzes regional markets including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in infrastructure maturity, regulatory environments, consumer adoption behavior, and institutional demand. Each region’s market volume, key applications, and strategic initiatives are outlined to support investment and operational decision-making. End-user segments such as defense and government, commercial enterprises, telecom operators, transportation, and industrial sectors are examined to reveal demand drivers and usage patterns.

In addition to current market structure and competitive positioning, the report identifies emerging and niche segments such as satellite-based cellular broadband, IoT mesh networks, hybrid orbit systems, and space-edge computing services. It also assesses industry challenges related to spectrum coordination, orbital congestion, interoperability, and service quality. By offering quantitative data and qualitative analysis, the report serves as a decision-support tool for stakeholders evaluating investment opportunities, technology partnerships, and strategic growth in the evolving space-based connectivity ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,040 Million |

| Market Revenue (2033) | USD 5,070.6 Million |

| CAGR (2026–2033) | 21.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | SpaceX (Starlink), OneWeb (Eutelsat), Amazon Leo, SES S.A., AST SpaceMobile, Intelsat, Iridium Communications, Viasat Inc., Hughes Network Systems, Telesat, Inmarsat Global Limited, Airbus Defence and Space, Boeing, Globalstar, SKYLOOM, Mynaric, ICEYE Oy |

| Customization & Pricing | Available on Request (10% Customization Free) |