Reports

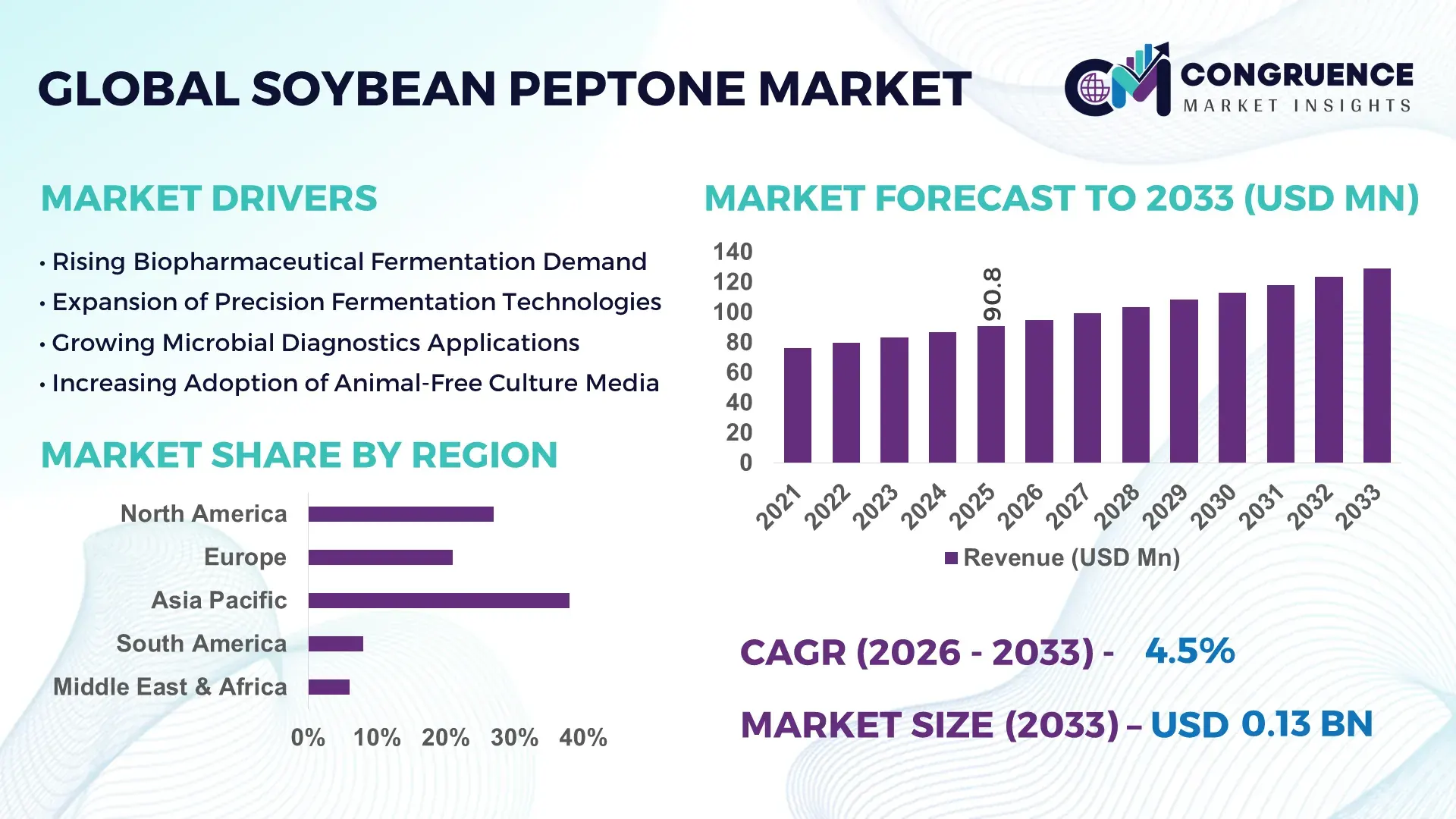

The Global Soybean Peptone Market was valued at USD 90.8 Million in 2025 and is anticipated to reach a value of USD 129.1 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033.

The market is accelerating due to rising biopharmaceutical fermentation demand, rapid replacement of animal-derived media components, and a 28% increase in plant-based nutrient substrate adoption across microbial culture manufacturing environments. Advanced downstream processing and enzyme-optimized hydrolysis technologies are improving protein recovery efficiency by nearly 18%, strengthening cost competitiveness against conventional peptones. Between 2024 and 2026, global biotechnology supply chains experienced strategic restructuring following protein raw material volatility and stricter contamination-control frameworks across pharmaceutical production networks. Regulatory preference for non-animal origin culture media in vaccine and recombinant protein manufacturing is reshaping procurement priorities, particularly across North America and Asia-Pacific.

China dominates the global Soybean Peptone Market with approximately 34% production share, supported by large-scale soybean processing capacity, expanding fermentation infrastructure, and strong biotechnology manufacturing investment. The country processes over 20 million metric tons of industrial soy derivatives annually, while biopharmaceutical production capacity expanded by nearly 21% during 2024–2025. Chinese manufacturers are increasingly integrating automated enzymatic hydrolysis systems that reduce batch inconsistency by 16% compared to conventional acid-based processing. In contrast, the United States leads in high-purity pharmaceutical-grade soybean peptone adoption, driven by advanced biologics and precision fermentation industries.

The market is shifting from commodity protein ingredients toward high-performance bio-manufacturing inputs, forcing companies to prioritize supply resilience, formulation precision, and strategic regional production expansion.

Market Size & Growth: USD 90.8 million in 2025 reaching USD 129.1 million by 2033, driven by 28% higher adoption of plant-based fermentation nutrients in biologics manufacturing.

Top Growth Drivers: Biopharmaceutical demand rose 31%, microbial fermentation usage increased 26%, and animal-free media conversion expanded 24% globally.

Short-Term Forecast: By 2028, enzymatic hydrolysis deployment is projected to reduce production waste by 19% and improve nutrient consistency by 17%.

Emerging Technologies: AI-assisted fermentation optimization, automated hydrolysis, and precision protein fractionation improved batch efficiency by nearly 22%.

Regional Leaders: Asia-Pacific exceeds USD 42 million demand led by fermentation scaling, North America surpasses USD 28 million via biologics adoption, Europe crosses USD 22 million through ESG-driven sourcing.

Consumer/End-User Trends: Over 46% of biotech manufacturers now prioritize non-animal culture media for contamination-risk reduction and compliance alignment.

Pilot/Case Example: In 2025, a precision fermentation project improved microbial yield by 18% after integrating high-purity soybean peptone formulations.

Competitive Landscape: Top five companies control nearly 48% market share, including Kerry Group, Thermo Fisher Scientific, Merck KGaA, Organotechnie, and HIMEDIA Laboratories.

Regulatory & ESG Impact: Sustainable plant-derived media adoption lowered carbon-intensive animal inputs by approximately 27% across advanced biotech facilities.

Investment & Funding: More than USD 180 million in fermentation and bioprocess expansion investments accelerated regional supply chain localization between 2024 and 2026.

Innovation & Future Outlook: High-solubility customized soybean peptones are reshaping next-generation cell culture efficiency and accelerating precision bio-manufacturing expansion.

Biopharmaceutical manufacturing accounts for nearly 41% of soybean peptone consumption, followed by industrial fermentation at approximately 33% and microbial diagnostics near 14%. Companies are introducing low-endotoxin and high-solubility soybean peptones optimized for precision fermentation workflows, improving nutrient absorption efficiency by 15%. Asia-Pacific continues leading volume demand, while Europe is accelerating adoption through sustainability-focused media sourcing requirements. Ongoing supply chain regionalization and stricter biologics quality frameworks are pushing manufacturers toward localized, high-purity production models that will increasingly define competitive positioning.

The Soybean Peptone Market is transforming into a strategically critical segment within global biotechnology and industrial fermentation ecosystems as pharmaceutical manufacturers, precision fermentation companies, and microbial culture producers aggressively shift toward non-animal nutrient systems. Rising contamination-control standards, accelerating biologics production, and tightening regulatory scrutiny are redefining supplier selection and forcing companies to optimize media consistency, traceability, and scalability simultaneously. This transition is accelerating investment competition across bio-manufacturing supply chains.

A major structural shift is emerging from post-pandemic supply diversification strategies and stricter biologics manufacturing compliance standards. Companies are increasingly localizing fermentation inputs to reduce procurement risk and shorten lead times by nearly 22%. Advanced enzymatic hydrolysis technology improves amino acid extraction efficiency by 24% while reducing production cost by 17% compared to conventional acid-hydrolysis systems. This technological transition is transforming soybean peptone from a commodity ingredient into a precision bio-processing solution.

Asia-Pacific leads in manufacturing volume due to large-scale soybean processing and lower production costs, while North America leads in innovation adoption with nearly 39% penetration of high-purity pharmaceutical-grade soybean peptones across biologics production facilities. Over the next two to three years, automated fermentation optimization systems are expected to improve batch productivity by approximately 20% while reducing nutrient variability by 14%.

ESG positioning is also becoming a competitive advantage. Plant-derived media inputs lower animal-origin dependency and support sustainability-linked procurement policies, improving market access for pharmaceutical exporters. In 2025, several bioprocessing facilities integrating optimized soybean peptone blends reported microbial yield improvements exceeding 18%, directly enhancing production throughput. Leading manufacturers are shifting capital allocation toward customized formulations, regional production hubs, and strategic biotechnology partnerships to secure long-term supply resilience. Companies that optimize purity, consistency, and integrated fermentation performance will define the next competitive frontier of the Soybean Peptone Market.

The Soybean Peptone Market is being reshaped by rapid expansion in biologics manufacturing, industrial fermentation optimization, and increasing adoption of animal-free culture media systems. Biotechnology manufacturers are prioritizing plant-derived nutrient substrates to improve contamination control, regulatory alignment, and production scalability. Demand concentration is strongest across pharmaceutical fermentation, microbial diagnostics, and enzyme production applications, where high-protein nutrient consistency directly influences process efficiency and product quality. More than 44% of advanced fermentation facilities are transitioning toward plant-based peptones to reduce operational variability and strengthen regulatory compliance. Simultaneously, supply chain restructuring across Asia-Pacific and North America is accelerating regional production investments and localized sourcing strategies. Precision fermentation growth, combined with increasing synthetic biology deployment, is redefining procurement priorities toward high-solubility and low-endotoxin soybean peptones. However, raw material price fluctuations and soybean supply concentration continue constraining production stability. Companies are responding through vertical integration, long-term agricultural sourcing agreements, and automated hydrolysis technologies that improve nutrient extraction efficiency by nearly 20%. Competitive dynamics are increasingly centered around formulation quality, scalability, and bioprocess performance optimization rather than purely price-based competition.

The strongest growth engine within the Soybean Peptone Market is the rapid expansion of biologics, vaccines, and precision fermentation manufacturing. Global biologics production capacity increased by approximately 27% between 2024 and 2026, directly increasing demand for high-purity, non-animal nutrient media. Pharmaceutical manufacturers are replacing conventional animal-derived peptones with soybean-based alternatives to strengthen contamination control and regulatory compliance. Nearly 46% of advanced microbial culture facilities now prioritize plant-origin fermentation substrates due to lower pathogen transmission risk and improved process reproducibility. A major global trigger has been the restructuring of pharmaceutical supply chains after international biologics shortages exposed dependency on limited animal-origin input suppliers. This shift is forcing fermentation companies to diversify sourcing strategies and accelerate regional manufacturing investments. As a result, soybean peptone producers are expanding enzymatic hydrolysis capacity, improving amino acid consistency by nearly 18%. The business impact is substantial. Higher fermentation efficiency improves microbial yield, reduces batch failure risk, and shortens production timelines. Companies are responding through strategic partnerships with biopharmaceutical firms, localized production facilities, and customized nutrient formulation development. This transition is redefining soybean peptone as a critical enabling component within advanced biotechnology manufacturing infrastructure.

The Soybean Peptone Market faces structural limitations due to soybean price volatility, agricultural dependency, and processing inconsistency across regional suppliers. Global soybean commodity fluctuations exceeded 19% during recent supply disruptions, directly impacting protein extraction costs and production stability. Approximately 61% of industrial soybean processing capacity remains concentrated across a limited group of exporting nations, increasing vulnerability to geopolitical trade shifts and weather-related agricultural disruptions. Infrastructure gaps within specialized hydrolysis and purification systems also constrain scalability. High-purity pharmaceutical-grade soybean peptones require advanced processing controls that increase operational expenditure by nearly 15% compared to standard industrial-grade variants. Regulatory pressure surrounding traceability and contamination management further intensifies production complexity for exporters targeting pharmaceutical applications. These constraints are creating direct business impacts through longer procurement cycles, higher input costs, and inconsistent product quality. Companies are mitigating risks by diversifying agricultural sourcing, signing multi-year supply agreements, and investing in automated process monitoring technologies. Some manufacturers are also developing hybrid protein extraction systems that improve nutrient stability and reduce dependency on single-origin soybean supply chains. The market remains fundamentally attractive, but scalability increasingly depends on operational resilience and supply diversification strategies.

Precision fermentation and synthetic biology are unlocking high-impact opportunities across the Soybean Peptone Market by expanding demand for customized nutrient formulations. More than 32% of emerging biotechnology companies are now developing tailored fermentation systems requiring application-specific protein substrates with higher solubility and amino acid precision. This shift is accelerating demand for next-generation soybean peptones optimized for recombinant protein production, microbial enzymes, and alternative protein manufacturing. One major innovation signal is the integration of AI-assisted fermentation optimization platforms that improve nutrient utilization efficiency by nearly 21% while reducing production waste by 14%. Companies deploying customized soybean peptone blends are achieving measurable improvements in microbial density and fermentation consistency, creating a strong operational advantage in high-throughput biologics manufacturing. Non-obvious upside is emerging from localized production ecosystems. Regionalized fermentation supply chains reduce lead times, lower transportation costs, and improve quality responsiveness for pharmaceutical manufacturers. Companies are positioning aggressively through R&D investment, biotechnology partnerships, and modular production expansion across Asia-Pacific and North America. This strategic transition is redefining soybean peptone from a standardized ingredient into a performance-optimized bioprocess solution with growing premium pricing potential and long-term competitive relevance.

Execution complexity remains one of the largest challenges constraining long-term stability within the Soybean Peptone Market. Maintaining nutrient consistency across high-volume production batches is increasingly difficult as fermentation applications become more specialized and quality-sensitive. Approximately 23% of biologics manufacturers report variability concerns linked to plant-based media performance consistency, particularly within high-density microbial culture environments. Another major pressure point involves infrastructure and processing scalability. Advanced enzymatic hydrolysis systems require significant capital investment, while energy-intensive purification stages increase operational costs by nearly 16%. Global logistics disruptions and container shortages during recent supply chain restructuring periods further exposed weaknesses in cross-border ingredient sourcing networks. These challenges directly impact long-term growth sustainability by increasing qualification timelines, reducing production predictability, and intensifying regulatory review requirements. Companies unable to guarantee batch reproducibility risk losing pharmaceutical-grade contracts. To remain competitive, manufacturers are investing in process automation, advanced quality analytics, and strategic raw material partnerships. Industry leaders are also pursuing vertical integration and regional production diversification to reduce exposure to logistics bottlenecks and agricultural volatility. Competitive success increasingly depends on operational precision rather than production scale alone.

18% Increase in Automated Hydrolysis Deployment Reshaping Production Efficiency: Manufacturers are rapidly integrating automated enzymatic hydrolysis systems to improve amino acid consistency and reduce processing waste. Batch variability declined by nearly 16%, while processing speed improved 14% across advanced facilities. Companies are restructuring production lines to support pharmaceutical-grade customization as stricter biologics compliance frameworks intensify globally.

27% Surge in Precision Fermentation Demand Accelerating Customized Formulations: Biotechnology companies are shifting toward application-specific soybean peptones optimized for recombinant protein and microbial enzyme production. Customized nutrient blends improved fermentation yield by approximately 19% in commercial deployments. Suppliers are expanding formulation portfolios and strengthening R&D partnerships to capture higher-value precision bio-manufacturing contracts.

22% Regional Supply Chain Localization Shift Redefining Procurement Strategies: Global fermentation companies are reducing dependence on cross-border raw material sourcing after recent logistics disruptions and agricultural volatility. Asia-Pacific producers expanded localized processing capacity by nearly 20%, while North American buyers increasingly prioritize domestic supply resilience. This restructuring is optimizing lead times and improving production continuity for pharmaceutical-grade fermentation inputs.

31% Growth in Sustainable Plant-Based Media Adoption Transforming Buyer Priorities: Biopharmaceutical manufacturers are aggressively replacing animal-derived peptones to align with ESG and contamination-control objectives. Plant-based media integration reduced high-risk biological input dependency by 24% across multiple fermentation applications. Companies are scaling low-endotoxin soybean peptone production and repositioning sustainability as a competitive procurement differentiator rather than a compliance requirement.

The Soybean Peptone Market is segmented across type, application, and end-user categories, with demand heavily concentrated in high-performance fermentation and biologics manufacturing environments. Pharmaceutical and biotechnology applications collectively account for more than 40% of total demand due to rising adoption of non-animal nutrient media in microbial culture systems. Industrial fermentation remains another critical demand center, particularly across enzyme production and precision bio-manufacturing processes. Demand distribution is increasingly shifting toward high-purity and customized soybean peptone formulations as manufacturers prioritize batch consistency, contamination control, and nutrient optimization. Approximately 36% of buyers now favor application-specific formulations over standard industrial-grade variants. End-user purchasing behavior is also evolving, with large biopharmaceutical companies accelerating long-term procurement agreements and localized sourcing strategies. Companies are strategically repositioning production capabilities toward specialized formulations, automated processing systems, and regional expansion initiatives to capture higher-margin demand segments and strengthen competitive positioning across advanced biotechnology ecosystems.

Enzymatic Hydrolysis Soybean Peptone dominates the Soybean Peptone Market with approximately 58% share due to superior amino acid retention, higher solubility, and better compatibility with pharmaceutical-grade fermentation processes. Its structural advantage lies in improved nutrient consistency and lower impurity levels, making it the preferred choice across biologics and microbial culture applications. Manufacturers continue expanding enzymatic processing capacity because automated hydrolysis systems improve nutrient recovery efficiency by nearly 18% while reducing batch inconsistency. Acid Hydrolysis Soybean Peptone is emerging as the fastest-expanding segment with adoption growth exceeding 15%, particularly across cost-sensitive industrial fermentation and enzyme manufacturing applications. Companies favor acid hydrolysis for faster processing cycles and lower production costs, despite comparatively lower nutrient precision. The market is increasingly witnessing a strategic comparison between enzymatic variants focused on high-value biotechnology applications and acid-hydrolyzed products targeting volume-based industrial deployment. Other specialized soybean peptone variants collectively account for nearly 21% market share, serving niche microbial diagnostics and customized fermentation systems. Companies are responding to shifting demand through formulation diversification, premium-grade product launches, and regional capacity expansion. Investment focus is increasingly shifting toward high-purity enzymatic solutions as biotechnology manufacturers prioritize performance optimization and regulatory alignment.

Biopharmaceutical Fermentation leads the Soybean Peptone Market with approximately 41% share because advanced biologics manufacturing requires highly consistent, non-animal nutrient media for microbial and recombinant protein production. Demand concentration is strongest among vaccine producers, monoclonal antibody manufacturers, and precision fermentation facilities prioritizing contamination control and regulatory compliance. High-purity soybean peptones improve microbial yield efficiency by nearly 18%, strengthening operational performance across pharmaceutical workflows. Industrial Fermentation is the fastest-growing application segment, expanding at nearly 16% adoption growth due to rising enzyme production, alternative protein manufacturing, and large-scale microbial processing activities. Compared with mature pharmaceutical applications focused on purity and validation, industrial fermentation prioritizes scalable nutrient performance and production cost optimization. This shift is accelerating deployment of customized soybean peptone formulations optimized for industrial throughput. Microbial diagnostics, research laboratories, and culture media preparation collectively contribute approximately 29% market share and continue gaining strategic importance through expanding biotechnology research activity. Companies are adapting by scaling specialized formulations, strengthening fermentation partnerships, and expanding localized supply capabilities. Demand is increasingly shifting toward application-specific nutrient systems that improve process reproducibility, operational scalability, and microbial performance efficiency.

Biopharmaceutical Companies dominate the Soybean Peptone Market with nearly 44% demand share due to their heavy dependency on contamination-controlled fermentation environments and high-performance microbial culture systems. Large-scale biologics manufacturing operations require highly standardized plant-derived nutrient media capable of supporting consistent recombinant protein production and regulatory compliance. Procurement preference increasingly favors low-endotoxin and high-solubility soybean peptone formulations that improve fermentation reliability by approximately 18%. Biotechnology Startups and Precision Fermentation Firms represent the fastest-growing end-user category, with adoption expansion exceeding 17% as synthetic biology and alternative protein development accelerate globally. Unlike established pharmaceutical firms focused on validated supply continuity, emerging biotechnology players prioritize customizable nutrient systems, rapid scalability, and optimized microbial productivity. This divergence is redefining supplier engagement models and product development priorities. Research institutes, industrial enzyme producers, and microbial diagnostics laboratories collectively account for around 31% market demand and continue increasing purchases for specialized culture media applications. Companies are targeting these users through flexible pricing models, customized formulation development, and strategic technical collaborations. Future demand concentration is shifting toward innovation-driven biotechnology ecosystems where fermentation optimization and localized production resilience are becoming key competitive differentiators.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific dominates due to large-scale soybean processing infrastructure, expanding fermentation capacity, and lower production costs, particularly across China, India, and South Korea. North America leads in high-purity biotechnology adoption, with approximately 39% of advanced biologics facilities utilizing premium plant-based fermentation media. Europe maintains strong influence through sustainability-driven procurement and stricter biologics manufacturing frameworks, accounting for nearly 21% market demand. South America is strengthening its position through soybean supply advantages, while the Middle East & Africa is accelerating biotechnology infrastructure investments. Global companies are increasingly prioritizing Asia-Pacific for production scale and North America for high-value innovation partnerships and premium formulation expansion.

North America holds approximately 27% of global Soybean Peptone Market demand, driven by strong biologics manufacturing, microbial diagnostics expansion, and accelerating precision fermentation deployment. The United States dominates regional consumption due to high adoption of non-animal culture media across pharmaceutical and recombinant protein production facilities. Regulatory focus on contamination control and traceability is forcing biotechnology manufacturers to transition toward high-purity plant-derived nutrient systems. Execution-level transformation is visible through automation integration and AI-assisted fermentation optimization, improving nutrient efficiency by nearly 18%. Several manufacturers expanded localized bioprocess ingredient capacity during 2025 to reduce supply chain dependency and shorten procurement timelines by approximately 15%. Enterprise buyers increasingly prioritize consistency, low endotoxin levels, and validated supply reliability over price-based sourcing. Companies continue investing aggressively in this region because North America combines high-margin pharmaceutical demand with rapid biotechnology innovation adoption.

Europe contributes nearly 21% of global Soybean Peptone Market demand, supported by strong biotechnology manufacturing activity across Germany, France, the United Kingdom, and Switzerland. The region’s market structure is heavily shaped by ESG-focused procurement standards and strict biologics production regulations emphasizing traceability and animal-free media adoption. More than 42% of advanced pharmaceutical fermentation facilities now prioritize sustainable plant-derived nutrient systems. Operational transformation is accelerating through low-emission processing technologies and automated quality-control systems that reduce production inconsistency by approximately 14%. European manufacturers are increasingly investing in high-purity customized soybean peptone formulations to align with advanced biologics compliance requirements. Enterprise buyers demonstrate strong quality-first purchasing behavior, even at premium pricing levels. This region is forcing companies to innovate faster because regulatory compliance, sustainability alignment, and formulation precision increasingly determine long-term competitive access across European biotechnology ecosystems.

Asia-Pacific leads the Soybean Peptone Market with approximately 38% demand share and the highest global production concentration. China, India, Japan, and South Korea dominate regional activity through large-scale soybean processing infrastructure and rapidly expanding fermentation manufacturing ecosystems. China alone accounts for nearly one-third of regional industrial soybean derivative output, creating a strong cost and supply advantage. Execution-level transformation is accelerating through localized hydrolysis processing expansion and integrated fermentation supply chains that improve production responsiveness by approximately 20%. Manufacturers across the region expanded industrial biotechnology processing capacity by nearly 18% between 2024 and 2025 to support rising pharmaceutical and precision fermentation demand. Buyers prioritize scale, supply continuity, and competitive pricing, particularly within industrial fermentation environments. Asia-Pacific remains strategically critical because it combines manufacturing speed, raw material availability, and high-volume biotechnology demand within a rapidly scaling production ecosystem.

South America accounts for nearly 8% of the Soybean Peptone Market, led primarily by Brazil and Argentina due to strong soybean cultivation capacity and expanding industrial fermentation activity. Regional demand is supported by growing biotechnology processing investments and increasing adoption of plant-derived fermentation inputs across enzyme and microbial production applications. However, infrastructure limitations and export logistics volatility continue constraining large-scale market acceleration. Transportation inefficiencies and port congestion increased cross-border shipment delays by approximately 12% during recent supply chain disruptions. Despite these limitations, localized processing investments are improving operational flexibility, while several manufacturers expanded soybean protein processing capacity by nearly 10% in 2025. Enterprise buyers across the region remain highly price-sensitive and increasingly favor regionally sourced fermentation inputs to reduce import dependency. South America presents strong strategic opportunity due to agricultural strength, but companies must balance expansion ambitions with infrastructure modernization and logistics risk management.

The Middle East & Africa region contributes approximately 6% of global Soybean Peptone Market demand, supported by expanding biotechnology investments and rising pharmaceutical manufacturing activity across the UAE, Saudi Arabia, and South Africa. Regional demand is increasingly linked to industrial diversification initiatives and healthcare manufacturing modernization strategies. A major transformation driver is the expansion of biotechnology infrastructure partnerships and localized pharmaceutical production programs. Advanced fermentation facility deployment increased by nearly 13% between 2024 and 2025, while several regional projects integrated automated microbial processing systems to improve operational productivity by approximately 15%. Enterprise procurement behavior strongly favors scalable, import-reliable plant-derived nutrient systems capable of supporting stable pharmaceutical production. The region remains strategically important because governments and industrial investors are prioritizing biotechnology self-sufficiency, localized manufacturing resilience, and advanced production infrastructure expansion to reduce dependency on imported biologics supply chains.

China – 34% market share: Dominates through massive soybean processing capacity, expanding fermentation infrastructure, and strong biotechnology manufacturing integration.

United States – 22% market share: Leads high-purity soybean peptone adoption due to advanced biologics manufacturing, precision fermentation deployment, and stringent pharmaceutical quality standards.

The Soybean Peptone Market is characterized by intense competition between global biotechnology ingredient leaders, specialized fermentation media suppliers, and cost-competitive regional manufacturers. Major players including Kerry Group, Thermo Fisher Scientific, Merck KGaA, HIMEDIA Laboratories, and Organotechnie compete aggressively across pharmaceutical-grade purity, customized formulations, and global supply reliability. The top five companies collectively control nearly 48% of the market, with competition increasingly shifting from volume-based pricing toward performance-driven differentiation.

Global leaders are competing through advanced hydrolysis technology, premium biologics-grade product portfolios, and vertically integrated sourcing strategies, while regional suppliers focus on lower-cost industrial fermentation applications. Customized formulation demand increased by approximately 26%, forcing companies to accelerate R&D investment and specialized production capabilities. Automation-driven hydrolysis systems improved nutrient consistency by nearly 18%, creating a major technological competitive advantage.

Competitive dynamics are also being reshaped by supply chain localization, strategic biotechnology partnerships, and regional production expansion initiatives. High entry barriers persist due to regulatory qualification requirements, process consistency expectations, and advanced purification infrastructure costs. Winning in this market increasingly requires precision manufacturing, formulation customization, strong biotechnology partnerships, and resilient regional supply ecosystems.

Thermo Fisher Scientific

Merck KGaA

HIMEDIA Laboratories

Organotechnie

Solabia Group

Titan Biotech Ltd.

BD Biosciences

Neogen Corporation

Bio Basic Inc.

MP Biomedicals

Apollo Scientific Ltd.

Rokomari Ingredients

Creative Peptides

Advanced enzymatic hydrolysis technology is becoming the dominant processing innovation within the Soybean Peptone Market due to its ability to improve amino acid retention, nutrient solubility, and batch consistency. Compared with conventional acid hydrolysis systems, enzymatic processing improves nutrient recovery efficiency by nearly 24% while reducing impurity levels by approximately 16%. More than 48% of newly commissioned biotechnology-grade soybean peptone facilities are integrating automated enzymatic control systems to optimize pharmaceutical fermentation compatibility.

AI-assisted fermentation optimization platforms are also reshaping operational precision. Biotechnology manufacturers are increasingly deploying predictive nutrient analytics and automated microbial monitoring systems that improve fermentation productivity by nearly 20%. These systems enable real-time nutrient adjustment, reducing process variability and shortening production cycles. Companies adopting AI-integrated nutrient management gain measurable advantages in biologics manufacturing throughput and contamination-risk reduction.

Another disruptive trend involves customized low-endotoxin soybean peptone formulations engineered specifically for recombinant protein production and precision fermentation. High-purity specialized formulations are rapidly replacing standardized industrial-grade variants in advanced biotechnology applications. Leading suppliers and pharmaceutical manufacturers benefit most from this transition because premium-grade formulations command stronger long-term supply agreements and higher operational dependence.

Between 2026 and 2028, integrated smart bioprocessing systems, automated purification infrastructure, and precision nutrient engineering are expected to redefine competitive positioning. Companies investing early in process automation, digital fermentation analytics, and customized formulation development will secure stronger market access and operational scalability across the evolving biotechnology ecosystem.

December 2025 – Thermo Fisher Scientific expanded its Bioprocess Design Center network across India, Singapore, and South Korea to strengthen regional biologics and fermentation support capabilities. The expansion added advanced localized bioprocess infrastructure and improved operational support efficiency for rapidly scaling biopharma manufacturers across Asia-Pacific. [Bioprocess Expansion] Source: www.thermofisher.com

January 2026 – Thermo Fisher Scientific announced a strategic collaboration with NVIDIA to integrate AI-driven laboratory automation and scientific instrumentation optimization. The initiative is designed to accelerate laboratory workflows, reduce manual intervention, and improve analytical processing speed and operational accuracy across advanced bioprocessing environments. [AI Lab Integration]

September 2025 – Kerry Group launched Smart Taste™ solutions integrating advanced food science and bio-fermentation expertise to address regulatory, sustainability, and supply-chain pressures. The platform supports cost optimization and formulation efficiency while strengthening fermentation-driven innovation capabilities for industrial biotechnology and nutrition applications. [Fermentation Innovation]

April 2026 – Thermo Fisher Scientific opened a new flagship U.S. Bioprocess Design Center featuring 4,000 square feet of laboratory and training infrastructure dedicated to biologics development and advanced therapy manufacturing. The facility strengthens scalable bioprocess collaboration capabilities and accelerates customer process-development timelines. [Facility Scale-Up]

The Soybean Peptone Market Report delivers comprehensive coverage across product types, applications, end-user industries, regional demand patterns, and emerging biotechnology processing technologies. The report evaluates segmentation across enzymatic and acid hydrolysis variants, industrial fermentation applications, biopharmaceutical production, microbial diagnostics, and precision biotechnology workflows. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with strategic assessment of manufacturing concentration, supply chain restructuring, and technology adoption dynamics.

The report includes detailed evaluation of more than 10 major industry participants and analyzes over 25 strategic market indicators, including adoption shifts, formulation demand trends, production concentration, and operational efficiency improvements. Approximately 46% of biotechnology manufacturers are transitioning toward non-animal fermentation media systems, while customized high-purity soybean peptone formulations now account for nearly 36% of advanced biologics demand. The study also assesses automation integration, AI-assisted fermentation optimization, and low-endotoxin formulation deployment trends shaping future competition.

From a strategic perspective, the report supports investment planning, regional expansion strategy, product positioning, and competitive benchmarking across evolving biotechnology ecosystems. It provides forward-looking directional analysis for 2026–2033, highlighting emerging precision fermentation opportunities, localized production expansion trends, and technology-driven operational shifts critical for long-term competitive advantage.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 90.8 Million |

| Market Revenue (2033) | USD 129.1 Million |

| CAGR (2026–2033) | 4.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Kerry Group; Thermo Fisher Scientific; Merck KGaA; HIMEDIA Laboratories; Organotechnie; Solabia Group; Titan Biotech Ltd.; BD Biosciences; Neogen Corporation; Bio Basic Inc.; MP Biomedicals; Apollo Scientific Ltd.; Rokomari Ingredients; Creative Peptides |

| Customization & Pricing | Available on Request (10% Customization Free) |