Reports

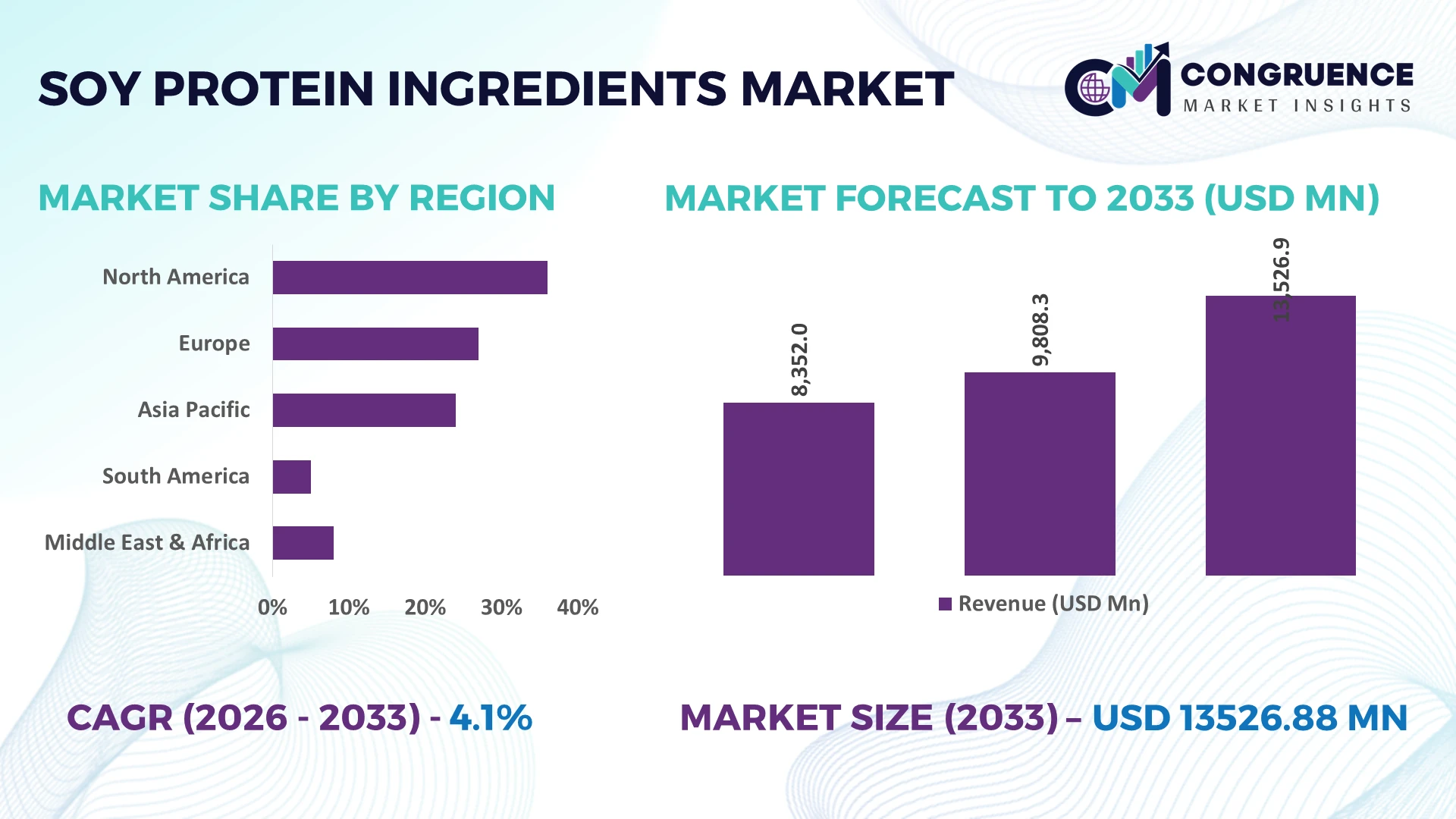

The Global Soy Protein Ingredients Market was valued at USD 9808.25 Million in 2025 and is anticipated to reach a value of USD 13526.88 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Expansion is driven by higher utilization of soy protein isolates and concentrates in functional foods, meat alternatives, sports nutrition, and industrial food processing, supported by advanced extraction technologies and protein-fortification strategies.

The United States leads the global soy protein ingredients market with approximately 31% of global processing capacity, supported by large-scale soybean cultivation, advanced protein extraction facilities, and over USD 2 billion in recent food manufacturing investments. More than 68% of large food manufacturers integrate soy protein into high-protein product portfolios, while China continues rapid expansion with over 25% processing capacity backed by food security initiatives following ongoing global agricultural supply-chain realignments and geopolitical trade adjustments.

Companies expanding processing capacity near stable soybean supply hubs while investing in advanced protein technologies will secure stronger margins, supply resilience, and long-term competitive positioning.

Market Size & Growth: USD 9808.25 Million (2025) to USD 13526.88 Million (2033) at 4.1%, driven by advanced protein processing and value-added food manufacturing.

Top Growth Drivers: Plant-based nutrition (+34%), sports nutrition (+22%), processed food protein fortification (+18%).

Short-Term Forecast: By 2028, protein extraction efficiency improves 12% while manufacturing waste declines 9%.

Emerging Technologies: AI-driven quality control, enzymatic extraction, and membrane filtration improve protein yield by up to 15%.

Regional Leaders: North America exceeds USD 4.4 billion, Asia-Pacific USD 3.9 billion, Europe USD 2.8 billion with expanding food-processing investments.

Consumer/End-User Trends: Over 61% of premium protein product launches incorporate plant-based protein formulations.

Pilot/Case Example: 2026 processing modernization project improved protein recovery by 14% and reduced energy consumption by 11%.

Competitive Landscape: Top five companies control nearly 47% market share through capacity expansion, innovation, and global supply-chain integration.

Regulatory & ESG Impact: Sustainable processing initiatives reduce manufacturing emissions by approximately 13% while strengthening export compliance.

Investment & Funding: More than USD 1.6 billion supports facility expansion, automation, and regional production diversification amid supply-chain shifts.

Innovation & Future Outlook: High-purity isolates, precision processing, and clean-label formulations accelerate premium product development and long-term global competitiveness.

Soy protein ingredients continue expanding across functional beverages, dairy alternatives, meat analogs, bakery, and clinical nutrition applications as manufacturers prioritize higher protein density and clean-label formulations. Advanced low-flavor processing technologies improve product acceptance, while nearly 19% of new protein product launches emphasize enhanced functionality. Regional sourcing diversification and evolving food quality regulations are strengthening supply resilience, setting the foundation for broader strategic market expansion.

Soy protein ingredients have become a strategic component of global food manufacturing as processors seek resilient protein supply chains, cost-efficient formulations, and diversified raw material sourcing. Industry competitiveness increasingly depends on securing vertically integrated soybean procurement while complying with evolving food labeling and sustainability standards. Supply-chain restructuring following recent agricultural trade disruptions has accelerated investments in regional processing facilities, allowing manufacturers to shorten procurement cycles and improve inventory stability by nearly 18%.

Modern membrane filtration and enzyme-assisted extraction systems deliver around 14% higher protein recovery while reducing processing energy consumption by approximately 11% compared with conventional extraction technologies. The United States continues leading large-scale industrial processing through automated manufacturing, whereas China emphasizes rapid capacity expansion and localized ingredient production to strengthen food security. Over the next two to three years, automated quality inspection is expected to exceed 55% adoption among newly commissioned processing facilities, improving operational consistency and reducing production variability.

A practical example is the deployment of integrated digital monitoring across protein extraction lines, enabling manufacturers to reduce process deviations by nearly 10% while improving batch traceability. Companies are expanding regional processing plants, strengthening farmer partnerships, and investing in specialty soy protein formulations for premium applications. Organizations combining operational efficiency, localized sourcing, and technology-driven production will establish stronger competitive positioning and long-term supply resilience.

Food manufacturers are increasing soy protein utilization as high-protein product development expands across beverages, meat alternatives, dairy substitutes, and clinical nutrition. More than 63% of new protein-enriched food launches now incorporate plant-derived ingredients, while advanced extraction technologies improve protein yield by approximately 15% and lower processing waste by nearly 10%. Food security initiatives in China and manufacturing modernization in the United States are accelerating investment in domestic processing capacity. In response, companies are expanding isolate production, forming long-term soybean procurement partnerships, and developing specialty formulations with enhanced solubility and texture. This vertically integrated approach strengthens supply reliability while improving manufacturing efficiency and premium product differentiation.

Soy protein manufacturers continue facing fluctuations in soybean pricing, transportation expenses, and energy-intensive processing operations. Raw material costs account for nearly 55% of total production expenditure, while logistics costs have increased by approximately 12% in several export-dependent supply chains. Weather-related crop variability in South America further affects procurement consistency and production planning. These pressures compress operating margins and complicate long-term pricing agreements with food manufacturers. Companies are mitigating risk through diversified sourcing across multiple producing countries, localized processing investments, and multi-year procurement contracts while improving production efficiency through automation to offset escalating operating costs and stabilize commercial performance.

Growing demand for clean-label, functional nutrition products creates significant opportunities for differentiated soy protein ingredients with improved taste, texture, and digestibility. Enzyme-assisted processing increases functional performance by nearly 16%, while digital process optimization reduces manufacturing downtime by approximately 9%. Japan and the United States are expanding research into specialty protein applications for medical nutrition and premium beverage formulations. Companies are strengthening R&D partnerships with food manufacturers, investing in precision processing technologies, and commercializing customized protein solutions for value-added applications. This transition from commodity ingredients toward specialized formulations enables stronger margins and deeper customer integration across advanced food manufacturing ecosystems.

Maintaining uniform protein functionality across multiple processing facilities remains a major execution challenge as manufacturers expand internationally. Batch-to-batch quality variation can affect formulation performance, while over 40% of processors continue upgrading legacy production systems to meet stricter food quality requirements. Increasing regulatory scrutiny for traceability, allergen management, and sustainability reporting adds operational complexity, particularly for exporters serving multiple countries. Companies must invest in advanced laboratory testing, digital quality management platforms, workforce training, and standardized production protocols to maintain consistent product performance. Organizations that successfully integrate these capabilities will strengthen customer confidence, operational resilience, and long-term competitiveness in global ingredient markets.

Soy Protein Isolates remain the leading segment because of their high protein purity, superior functional properties, and broad compatibility across beverages, dairy alternatives, sports nutrition, and meat formulations. The segment accounts for nearly 39% of industrial utilization, supported by excellent solubility, emulsification, and processing consistency. Soy Protein Concentrates continue serving processed food manufacturers seeking balanced functionality and cost efficiency, while Soy Protein Flour maintains stable demand in bakery products and conventional food applications because of its economical formulation advantages.

Textured Soy Protein is the fastest-growing type, with industrial adoption increasing by approximately 18% as manufacturers expand plant-based meat production using advanced extrusion technologies. Hydrolyzed Soy Protein is steadily gaining acceptance in specialized nutrition products due to improved digestibility and rapid absorption characteristics. Companies are investing in advanced purification systems, expanding production capacity, and strengthening partnerships with food manufacturers to develop premium protein solutions. Investment priorities continue shifting from commodity ingredients toward value-added specialty proteins that improve manufacturing efficiency, product performance, and long-term competitiveness.

Food & Beverages remain the dominant application due to extensive utilization across dairy alternatives, functional beverages, processed foods, snacks, and nutrition products, representing nearly 48% of commercial demand. Manufacturers increasingly incorporate soy protein to enhance nutritional value, improve texture, and extend shelf stability while maintaining formulation efficiency. Bakery Products continue expanding through protein-enriched formulations, whereas Animal Feed maintains stable demand because of its balanced amino acid profile and dependable large-scale availability.

Meat Alternatives represent the fastest-growing application, with product development activity increasing by approximately 21% as manufacturers invest in advanced extrusion technologies and high-performance plant protein formulations. Dietary Supplements continue strengthening demand for highly purified soy protein ingredients used in sports and clinical nutrition. Companies are expanding production capacity, introducing customized formulations, and strengthening partnerships with food brands to support specialized applications, improve operational efficiency, and build differentiated premium product portfolios.

Food Manufacturers remain the dominant end-user segment because of continuous demand across packaged foods, dairy alternatives, functional beverages, processed meals, and protein-enriched products. This group accounts for nearly 52% of industrial purchasing volume, supported by integrated production infrastructure and large-scale formulation requirements. Beverage Companies continue increasing procurement of highly soluble soy protein ingredients for ready-to-drink protein beverages and fortified drinks, while Animal Feed Producers maintain stable purchasing volumes due to consistent livestock nutrition requirements and efficient feed formulation.

Nutraceutical Companies represent the fastest-growing end-user segment as demand for sports nutrition, healthy aging, and clinical nutrition products expands. Enterprise adoption has increased by approximately 17%, while customized protein ingredient sourcing has grown by nearly 13% to support premium formulations. Foodservice operators are also expanding soy protein utilization across commercial meal solutions and institutional catering as plant-based menu offerings increase. Suppliers are responding through customized ingredient development, long-term supply agreements, technical formulation support, and strategic partnerships, strengthening customer retention while positioning for sustained demand across high-value nutrition applications.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.0% between 2026 and 2033.

Advanced Processing and Product Innovation Drive Regional Leadership

North America maintains the largest share of the Soy Protein Ingredients Market through a highly integrated soybean value chain, advanced processing infrastructure, and strong demand from food, beverage, and nutrition manufacturers. The region contributes approximately 36.4% of global consumption, supported by automated extraction technologies and large-scale manufacturing operations. More than 65% of premium protein product launches incorporate plant-based protein formulations, encouraging processors to expand specialty ingredient production. Manufacturers continue investing in digital quality control, capacity upgrades, and long-term sourcing partnerships to improve manufacturing efficiency, strengthen supply resilience, and accelerate commercialization of high-functionality soy protein ingredients.

United States Market Outlook: The United States leads regional production through extensive soybean cultivation, advanced ingredient processing facilities, and continuous investment in food manufacturing innovation. Over 70% of large-scale soy protein production facilities have implemented automated quality monitoring and process optimization technologies to improve manufacturing consistency. Companies continue expanding specialty protein capacity, strengthening farmer partnerships, and developing customized formulations for functional foods, beverages, and clinical nutrition, reinforcing the country's position as the region's primary innovation and manufacturing hub.

Sustainability Standards Reshape Ingredient Manufacturing

Europe continues strengthening its position through sustainable food production, regulatory alignment, and investment in clean-label ingredient innovation. The region accounts for approximately 24% of global market activity, with manufacturers prioritizing traceable sourcing and energy-efficient processing systems. Nearly 52% of newly developed plant-based food products utilize functional soy protein ingredients to meet nutritional and labeling requirements. Companies are modernizing production facilities, improving resource efficiency, and expanding strategic partnerships with food manufacturers to support premium applications while maintaining compliance with evolving sustainability and food quality standards.

Germany Market Outlook: Germany represents the leading country market due to its advanced food processing industry, strong research capabilities, and expanding plant-based food manufacturing ecosystem. More than 60% of major food manufacturers continue investing in protein formulation technologies to improve product functionality and production efficiency. Enterprise collaboration between ingredient suppliers and food manufacturers is accelerating commercial deployment of specialized soy protein solutions across dairy alternatives, bakery products, and nutritional foods.

Manufacturing Scale Accelerates Commercial Expansion

Asia-Pacific is experiencing the strongest expansion, supported by large-scale food manufacturing, growing protein consumption, and increasing investment in domestic processing infrastructure. The region contributes nearly 30% of global production capacity, while integrated soybean processing facilities continue expanding across key industrial hubs. Automated production technologies have improved manufacturing efficiency by approximately 14%, encouraging enterprises to increase specialty ingredient output. Companies are strengthening local supply chains, expanding processing capacity, and investing in advanced extraction technologies to improve product quality, operational efficiency, and export competitiveness.

China Market Outlook: China remains the region's largest market through extensive food manufacturing capacity, government support for food security, and continued modernization of soybean processing facilities. More than 62% of newly established protein processing projects incorporate automated manufacturing and digital quality management systems. Domestic manufacturers continue expanding localized production, reducing import dependency, and strengthening strategic partnerships with food processors to improve supply stability and accelerate commercialization of value-added soy protein ingredients.

Agricultural Strength Supports Industrial Expansion

South America benefits from abundant soybean production, competitive raw material availability, and increasing investment in value-added ingredient processing. The region contributes approximately 15% of global soy protein ingredient production, supported by expanding crushing and processing infrastructure. Modern processing investments have improved production efficiency by nearly 10%, although logistics bottlenecks and transportation infrastructure continue affecting distribution performance. Companies are increasing investments in localized processing facilities, strengthening export partnerships, and improving supply-chain integration to enhance operational flexibility while capturing growing demand for functional protein ingredients.

Brazil Market Outlook: Brazil dominates the regional market through its position as one of the world's largest soybean producers and exporters. Processing companies continue expanding domestic protein ingredient manufacturing to capture greater value beyond commodity soybean exports. Approximately 58% of recently commissioned soybean processing projects include upgraded protein extraction technologies, enabling manufacturers to improve production efficiency, strengthen export competitiveness, and expand supply to international food and nutrition companies.

Food Industry Modernization Expands Market Potential

The Middle East & Africa market is advancing through food manufacturing modernization, increasing investment in protein ingredient processing, and growing demand for functional nutrition products. The region accounts for approximately 7% of global market activity, with food processors expanding localized production to improve supply security. Investments in modern food processing facilities have increased by nearly 12% over recent years, supporting greater deployment of advanced ingredient technologies. Companies are strengthening regional distribution partnerships, improving processing infrastructure, and expanding product portfolios to reduce import dependence and improve manufacturing efficiency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through large-scale investment in food manufacturing, industrial diversification, and food security initiatives. Modern food processing facilities continue adopting advanced ingredient technologies to improve production quality and operational efficiency. Nearly 40% of recently announced food manufacturing expansion projects include enhanced protein processing capabilities, positioning the country as an important regional hub for value-added food ingredient production and long-term industrial development.

The Soy Protein Ingredients Market is led by ADM, Cargill, International Flavors & Fragrances, Kerry Group, and Fuji Oil Holdings, whose combined market share is approximately 47%. Global ingredient leaders compete with regional soybean processors on processing technology, supply-chain integration, and customized formulation capabilities, while specialty protein innovators challenge cost-focused bulk suppliers through higher-value applications. Companies achieving 12% greater extraction efficiency and 10% lower production costs through advanced membrane filtration strengthen competitive positioning. Vertical integration with soybean sourcing, strategic processing expansion, and long-term food manufacturer partnerships are replacing price competition as primary differentiators. Consolidation continues as processors acquire specialty capabilities and expand premium protein portfolios to secure resilient supply chains. The principal entry barrier is capital-intensive processing infrastructure combined with strict food quality and traceability requirements. Success increasingly depends on scalable production, differentiated functional ingredients, reliable raw material procurement, and continuous technology investment that delivers consistent performance across global food manufacturing operations.

ADM

Cargill Incorporated

International Flavors & Fragrances Inc.

Kerry Group plc

Fuji Oil Holdings Inc.

Bunge Global SA

CHS Inc.

Burcon NutraScience Corporation

The Scoular Company

Foodchem International Corporation

Sonic Biochem Extractions Limited

Axiom Foods Inc.

Advanced membrane filtration, enzyme-assisted extraction, and automated process control are transforming soy protein manufacturing by improving protein recovery, functionality, and production consistency. Membrane filtration increases extraction efficiency by nearly 15%, while enzyme-assisted processing reduces energy consumption by approximately 11% compared with conventional extraction methods. Around 58% of newly upgraded processing facilities now deploy automated quality monitoring, enabling manufacturers to reduce production variability and strengthen commercial-scale manufacturing performance.

Emerging technologies include AI-enabled quality inspection, digital formulation platforms, and real-time production analytics integrated across ingredient processing operations. AI-based process optimization improves production accuracy by approximately 10%, while predictive maintenance reduces equipment downtime by nearly 12%. Compared with legacy production systems, digitally integrated facilities achieve approximately 14% higher operational efficiency through continuous monitoring and automated process adjustments. Large multinational ingredient manufacturers benefit most because integrated digital infrastructure accelerates commercialization of premium protein formulations while improving manufacturing flexibility.

Disruptive innovation between 2026 and 2028 will focus on precision protein modification, continuous extraction systems, and intelligent manufacturing platforms supporting application-specific ingredient development. More than 65% of newly commissioned premium processing lines are expected to incorporate digital production management, strengthening traceability, reducing operational costs, and accelerating product customization. Companies investing early in advanced processing technologies and intelligent automation will establish stronger competitive differentiation, higher operational resilience, and faster response to evolving food manufacturing requirements.

August 2025: ADM announced the streamlining of its global soy protein production network by consolidating operations around its recommissioned Decatur facility, strengthening manufacturing efficiency and customer service. The move optimizes multiple production assets within one integrated network, improving operational competitiveness and supply reliability. Source: nasdaq.com

March 2026: Bunge completed the acquisition of selected soy protein concentrate, lecithin, and soy crush businesses from IFF, adding the Response, Alpha, Procon, and Solec product portfolios. The acquired businesses generated approximately USD 240 million in 2024 sales, significantly expanding Bunge's functional protein ingredient portfolio. Source: ingredients-insight.com

May 2026: ADM launched eight new soy and pea protein ingredients across North America and Europe, expanding solutions for beverages, meat alternatives, dairy substitutes, bakery products, and specialized nutrition. The broader portfolio strengthens formulation flexibility while supporting manufacturers developing next-generation high-protein food applications. Source: adm.com

May 2026: ADM introduced an expanded portfolio featuring eight innovative soy- and pea-based protein ingredients with improved solubility, texture, and yield for commercial food manufacturers. The innovation strengthens premium ingredient differentiation and accelerates product development across multiple plant-based food categories. Source: proteinproductiontechnology.com

This report provides comprehensive coverage of the global Soy Protein Ingredients Market through detailed evaluation of product types, applications, end-users, competitive positioning, technology evolution, and regional performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It assesses Soy Protein Isolates, Soy Protein Concentrates, Soy Protein Flour, Textured Soy Protein, and Hydrolyzed Soy Protein, while analyzing deployment across Food & Beverages, Dietary Supplements, Animal Feed, Bakery Products, and Meat Alternatives. More than 10 leading industry participants are benchmarked to evaluate operational strategies, manufacturing capabilities, and market positioning.

The report further examines production technologies, supply-chain transformation, automation trends, sustainability initiatives, and investment priorities expected to influence industry development between 2026 and 2033. It highlights adoption patterns, segment performance, regional manufacturing concentration, and enterprise expansion strategies while delivering actionable intelligence for competitive benchmarking, capacity planning, investment evaluation, product portfolio optimization, market entry decisions, and long-term business positioning across established and emerging application areas.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9808.25 Million |

|

Market Revenue in 2033 |

USD 13526.88 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ADM, Cargill Incorporated, International Flavors & Fragrances Inc., Kerry Group plc, Fuji Oil Holdings Inc., Bunge Global SA, CHS Inc., Burcon NutraScience Corporation, The Scoular Company, Foodchem International Corporation, Sonic Biochem Extractions Limited, Axiom Foods Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |