Reports

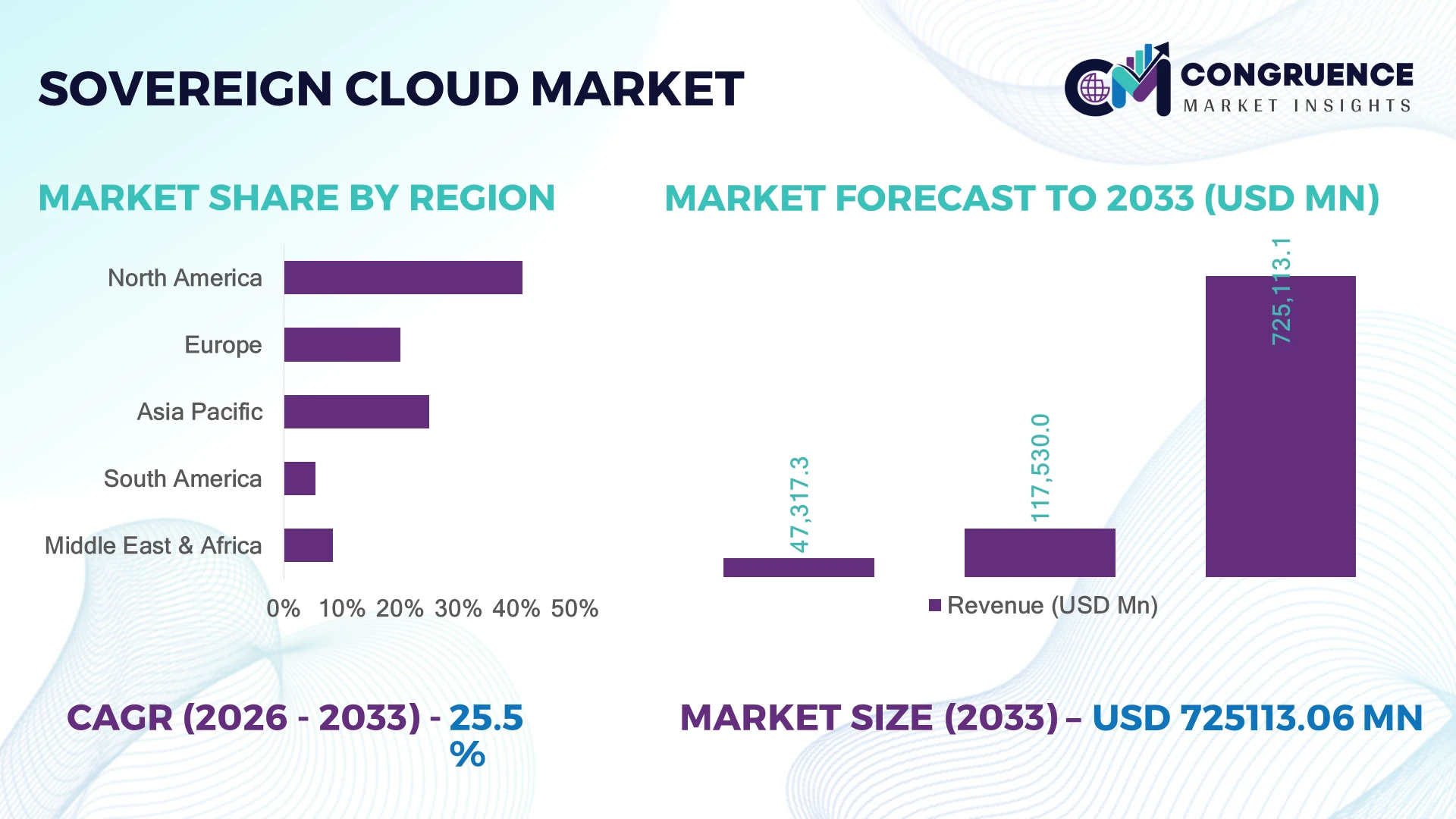

The Global Sovereign Cloud Market was valued at USD 117530 Million in 2025 and is anticipated to reach a value of USD 725113.06 Million by 2033 expanding at a CAGR of 25.54% between 2026 and 2033. Accelerated national data localization mandates, defense-grade digital infrastructure programs, and AI workload sovereignty requirements are driving rapid enterprise migration toward compliant sovereign cloud environments across regulated sectors.

Germany maintains a dominant position within the global sovereign cloud ecosystem, accounting for nearly 24% of Europe’s sovereign cloud infrastructure capacity in 2026, supported by over USD 8 billion in public-private digital sovereignty investments focused on manufacturing, BFSI, and public administration workloads. France follows with approximately 18% regional capacity share, driven by defense and telecom modernization initiatives under the European digital autonomy agenda. Germany’s enterprise sovereign cloud adoption exceeds France by nearly 11%, particularly across Industry 4.0 deployments integrating confidential computing and AI governance controls. Rising geopolitical concerns linked to cross-border data transfer restrictions after intensified EU-U.S. compliance scrutiny continue reshaping hyperscale deployment strategies and multi-region cloud architecture investments.

Organizations prioritizing sovereign cloud partnerships with localized AI processing, compliance automation, and domestic infrastructure ownership are positioned to secure stronger regulatory resilience and long-term digital control advantages.

Market Size & Growth: USD 117530 Million in 2025 rising to USD 725113.06 Million by 2033, supported by 25.54% expansion from AI sovereignty mandates and regulated cloud modernization.

Top Growth Drivers: Data localization compliance demand up 41%, government cloud spending up 33%, and confidential computing deployment growth exceeding 29% globally.

Short-Term Forecast: By 2028, sovereign cloud infrastructure reduces cross-border data processing risks by 37% while improving compliance audit efficiency by 31%.

Emerging Technologies: AI governance platforms, confidential computing, and zero-trust cloud architecture improve workload security efficiency by nearly 35% across high-security industries.

Regional Leaders: Europe surpasses USD 285 billion with public-sector adoption acceleration, Asia-Pacific exceeds USD 176 billion through domestic hyperscale expansion, and North America crosses USD 148 billion via defense-cloud modernization.

Consumer/End-User Trends: More than 62% of BFSI and healthcare enterprises prioritize sovereign-by-design cloud frameworks for regulated AI and analytics workloads.

Pilot/Case Example: In 2026, a national sovereign cloud deployment in the Middle East reduced sensitive workload latency by 28% and improved operational visibility by 34%.

Competitive Landscape: Leading providers control nearly 46% market share, with strong competition among advanced hyperscalers, telecom-cloud alliances, cybersecurity vendors, and regional infrastructure operators.

Regulatory & ESG Impact: Sovereign cloud-enabled energy optimization lowers data-center compliance reporting time by 26% while supporting stricter regional cybersecurity directives.

Investment & Funding: Global sovereign cloud investments exceed USD 52 billion in 2026, driven by strategic partnerships, regional expansion programs, and AI infrastructure localization.

Innovation & Future Outlook: Quantum-resistant encryption, sovereign AI clusters, and edge-cloud federation architectures are reshaping high-growth digital sovereignty strategies worldwide.

Sovereign Cloud Market demand is accelerating across defense, banking, healthcare, and public-sector digital transformation programs requiring localized data governance and secure AI processing environments. Advanced confidential computing platforms and sovereign AI infrastructure orchestration tools improved regulated workload isolation efficiency by nearly 32% in 2026. Increasing geopolitical scrutiny around cross-border data transfers and national cybersecurity resilience is also accelerating regional cloud infrastructure partnerships, creating a strong foundation for long-term strategic expansion.

Sovereign cloud infrastructure has become strategically critical as governments, financial institutions, and defense operators restructure digital ecosystems around jurisdiction-controlled data processing and AI governance. Tightened cross-border compliance frameworks, including European digital sovereignty mandates and national cybersecurity modernization programs, are accelerating localized cloud deployment strategies. More than 58% of regulated enterprises in 2026 are prioritizing sovereign-by-design architecture to reduce external dependency risks and strengthen operational continuity. This transition is also reshaping cloud supply chains, with telecom operators, domestic data-center providers, and cybersecurity firms forming integrated sovereign infrastructure alliances.

Confidential computing-enabled sovereign cloud environments are delivering nearly 34% faster secure workload verification compared with legacy private-cloud systems while reducing compliance management overhead by approximately 27%. Germany and France continue emphasizing state-backed infrastructure ownership and defense-grade hosting capabilities, while Singapore and the UAE are scaling hybrid sovereign cloud corridors focused on AI-intensive financial and smart-city applications. Over the next two to three years, sovereign AI processing clusters and localized edge-cloud frameworks are expected to support more than 45% of public-sector advanced analytics workloads globally.

A major telecom-cloud partnership launched in 2026 reduced sensitive government application latency by 29% through localized sovereign edge nodes integrated with zero-trust orchestration platforms. Enterprises are increasing investments in domestic cloud regions, encryption-focused partnerships, and sovereign SaaS ecosystems to secure long-term regulatory resilience. Companies establishing interoperable, compliance-driven cloud infrastructure with localized AI governance capabilities are strengthening competitive positioning across high-security digital economies.

National digital sovereignty mandates and AI governance frameworks are accelerating sovereign cloud deployment across regulated industries. More than 61% of European public-sector organizations shifted critical workloads toward jurisdiction-controlled infrastructure in 2026, while sovereign AI processing demand increased by nearly 38% across banking and defense environments. Germany expanded domestic sovereign data-center capacity by approximately 22% following stricter compliance alignment requirements for sensitive industrial data processing. This regulatory shift is directly increasing enterprise investment in localized encryption, confidential computing, and compliance automation platforms. Telecom operators and hyperscale providers are responding through joint sovereign cloud ventures, domestic infrastructure expansion, and cybersecurity-focused partnerships. A notable operational trend involves manufacturing firms integrating sovereign edge-cloud systems to secure industrial IoT data pipelines, reducing external exposure risks while improving real-time operational visibility by nearly 26%.

Sovereign cloud deployment remains constrained by elevated infrastructure localization expenses, fragmented compliance frameworks, and interoperability limitations between domestic and hyperscale cloud ecosystems. Dedicated sovereign hosting environments increase operational infrastructure costs by nearly 31% compared with conventional multi-tenant cloud architectures, particularly in countries with limited domestic semiconductor and networking supply chains. In Japan, energy-intensive sovereign data-center operations raised enterprise cloud operating expenditures by approximately 18% during recent infrastructure expansion cycles. Regulatory fragmentation across jurisdictions is also slowing workload portability and cross-border application integration. These pressures directly affect scalability, deployment consistency, and long-term profitability for cloud operators serving multinational enterprises. Companies are mitigating exposure through regional infrastructure partnerships, modular cloud-stack standardization, and localized procurement agreements designed to reduce dependency on imported hardware and external cybersecurity layers.

The integration of sovereign AI infrastructure with localized edge computing platforms is creating high-value opportunities across industrial automation, healthcare analytics, and defense intelligence processing. More than 47% of enterprises deploying regulated AI workloads are prioritizing sovereign edge-cloud architecture to improve jurisdictional control and low-latency analytics performance. India and Saudi Arabia are rapidly expanding sovereign digital infrastructure corridors through national AI modernization programs and domestic cloud-region investments. AI-enabled compliance orchestration platforms are reducing audit-processing time by nearly 33%, creating measurable operational efficiency advantages for financial institutions and government agencies. Cloud providers are increasing R&D investments in quantum-resistant encryption, sovereign AI clusters, and interoperable multi-cloud frameworks. A significant strategic shift involves telecom providers evolving into sovereign infrastructure orchestrators, enabling vertically integrated services for public-sector digital transformation programs.

Long-term sovereign cloud scalability is increasingly challenged by integration complexity, cybersecurity escalation, and shortages of specialized cloud-governance expertise. Nearly 42% of enterprises managing multi-country sovereign deployments reported operational delays linked to incompatible compliance controls and fragmented orchestration standards in 2026. France and South Korea are experiencing intensified demand for sovereign cybersecurity specialists as advanced zero-trust environments and AI governance systems require continuous policy adaptation. Rising ransomware targeting of regulated infrastructure is also increasing pressure on sovereign cloud resilience engineering and workload isolation capabilities. These execution barriers directly affect deployment consistency, vendor interoperability, and service sustainability across highly regulated sectors. Companies must strengthen automated compliance intelligence, sovereign SOC infrastructure, and cross-platform orchestration capabilities through strategic partnerships, domestic workforce development, and advanced cyber-resilience investments to maintain long-term operational competitiveness.

• Localized AI Infrastructure Expansion Sovereign AI clusters and jurisdiction-controlled GPU environments are expanding rapidly as governments tighten national data processing requirements. In 2026, more than 44% of regulated enterprises shifted sensitive AI workloads toward sovereign cloud environments, while secure edge-node deployment increased by nearly 31% across Germany and the UAE. Companies are restructuring infrastructure partnerships with telecom operators and domestic data-center providers to reduce latency by approximately 27% and strengthen compliance automation for AI-driven analytics operations.

• Telecom-Hyperscaler Alliance Acceleration Telecom providers are becoming strategic sovereign cloud orchestrators through integrated hosting, cybersecurity, and edge-compute partnerships with hyperscale operators. France and India recorded over 36% growth in telecom-led sovereign infrastructure projects during 2026 following intensified digital sovereignty mandates. This transition is shortening enterprise deployment cycles by nearly 24% while improving workload localization efficiency. Operators are scaling neutral-host infrastructure models and sovereign SaaS ecosystems to capture public-sector and BFSI modernization contracts.

• Confidential Computing Adoption Surge Confidential computing frameworks integrated with zero-trust orchestration platforms are reshaping regulated cloud security operations. More than 52% of financial institutions deploying sovereign cloud architecture adopted hardware-based encryption environments in 2026, reducing sensitive workload exposure risks by nearly 33%. Rising ransomware pressure and stricter cybersecurity certification rules are pushing cloud providers to automate threat isolation, secure containerization, and encrypted AI inference capabilities across hybrid sovereign deployments.

• Energy-Efficient Sovereign Operations Energy optimization is emerging as a critical operational differentiator as sovereign data-center expansion intensifies power utilization pressures. Nordic sovereign cloud facilities improved cooling efficiency by approximately 22% through AI-enabled workload balancing and liquid-cooling integration in 2026. Companies are restructuring infrastructure design around modular low-energy compute zones and renewable-backed hosting environments to control operating expenditures and comply with tightening national sustainability benchmarks tied to public-sector procurement eligibility.

Hybrid Cloud maintains the leading position within the sovereign cloud market due to its ability to balance regulatory compliance, operational flexibility, and workload scalability across public and private infrastructure layers. More than 48% of regulated enterprises in 2026 adopted hybrid sovereign environments to manage sensitive data localization while retaining scalable analytics and AI-processing capabilities. Germany’s manufacturing and BFSI sectors increasingly prefer hybrid deployments because they reduce infrastructure transition costs by nearly 26% compared with full private-cloud migration strategies. Public Cloud environments continue supporting non-sensitive operational workloads, particularly across telecom and digital citizen-service platforms requiring elastic computing capacity and lower deployment overhead.

Multi-Cloud is emerging as the fastest-growing segment as enterprises seek vendor diversification, geopolitical risk reduction, and stronger workload resilience. Adoption of sovereign multi-cloud orchestration frameworks increased by approximately 37% in 2026 among defense and healthcare operators managing cross-platform compliance obligations. Private Cloud deployments remain strategically relevant for classified government applications and defense intelligence processing, while Community Cloud models are gaining traction among public institutions sharing national cybersecurity frameworks. Providers are expanding interoperable sovereign cloud stacks, encryption-focused partnerships, and localized edge integrations to strengthen deployment flexibility and competitive positioning.

Data Security represents the leading application segment as governments, BFSI institutions, and healthcare providers intensify investments in encrypted sovereign infrastructure and jurisdiction-controlled digital operations. In 2026, over 58% of enterprises deploying sovereign cloud environments identified data sovereignty and cyber-resilience as primary procurement priorities. Advanced confidential computing integration improved sensitive workload protection efficiency by nearly 34%, particularly across defense and financial transaction systems in France and Singapore. Compliance Management continues expanding steadily as enterprises automate audit controls, policy orchestration, and localized reporting obligations linked to evolving national cybersecurity regulations.

Healthcare Data Management is emerging as the fastest-growing application segment due to rising digital patient record volumes, AI-enabled diagnostics, and stricter medical data governance mandates. Healthcare organizations deploying sovereign cloud frameworks reduced secure data retrieval latency by approximately 29% during large-scale digital modernization programs. Government Services remain operationally critical for digital identity systems and public infrastructure management, while Digital Banking deployments are accelerating through secure AI-driven fraud analytics and localized transaction processing. Providers are strengthening vertical-specific sovereign cloud platforms through automation, cybersecurity integration, and compliance-centric SaaS deployment strategies.

The Government Sector remains the dominant end-user group due to large-scale deployment of sovereign digital infrastructure for national cybersecurity, citizen data governance, and public administration modernization. More than 54% of sovereign cloud deployments in 2026 were linked to government-backed infrastructure programs, particularly across Germany, India, and the UAE. National digital sovereignty policies and defense-grade hosting requirements accelerated secure workload migration while reducing external cloud dependency risks by nearly 32%. Public Institutions are also expanding adoption for education, digital identity management, and smart governance systems requiring localized compliance control and operational transparency.

Healthcare is emerging as the fastest-growing end-user segment as medical systems digitize patient records, AI-assisted diagnostics, and secure telehealth infrastructure. Healthcare sovereign cloud deployments increased by approximately 36% in 2026 following tighter clinical data protection mandates and rising cyberattack exposure. BFSI organizations continue prioritizing encrypted transaction environments and localized analytics platforms, while Defense Sector deployments focus on classified intelligence processing and resilient communication infrastructure. IT and Telecom providers are positioning competitively through sovereign edge infrastructure partnerships, customized compliance frameworks, and sector-specific pricing models supporting long-term enterprise retention.

Europe accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28.12% between 2026 and 2033.

Federal AI Sovereignty and Secure Cloud Expansion

North America maintains strong sovereign cloud deployment momentum through defense modernization, regulated AI adoption, and expansion of jurisdiction-controlled digital infrastructure. The region contributed nearly 29% of global sovereign cloud deployment activity in 2025, supported by large-scale migration across BFSI, healthcare, and federal workloads. The United States and Canada are prioritizing sovereign AI processing environments integrated with zero-trust cybersecurity frameworks and confidential computing architecture. In 2026, sovereign edge-node deployment across regulated enterprises increased by approximately 27%, reducing critical application response latency and improving localized compliance management. Cloud providers are accelerating telecom partnerships, encrypted cloud-region development, and sovereign SaaS integration to strengthen operational resilience and domestic infrastructure control.

United States Market Outlook: The United States leads the regional market through large-scale sovereign defense cloud programs, advanced hyperscale infrastructure, and strong enterprise AI adoption. More than 59% of regulated enterprises expanded sovereign cloud integration during 2026, particularly across financial services, aerospace, and federal digital modernization initiatives. Domestic providers are scaling classified cloud zones, sovereign AI compute clusters, and encrypted edge infrastructure to support mission-critical workload localization and national cybersecurity resilience requirements.

Regulatory Sovereignty Reshaping Enterprise Infrastructure

Europe remains the largest sovereign cloud market due to strict data localization mandates, advanced cybersecurity governance, and accelerating public-sector digital sovereignty programs. Nearly 41% of regulated enterprises across Europe migrated sensitive workloads toward sovereign cloud architecture in 2026 following intensified scrutiny around cross-border data transfers and AI governance compliance. Germany, France, and the Netherlands continue leading sovereign infrastructure deployment through localized data-center expansion and confidential computing integration. A major operational shift involves sovereign hybrid-cloud adoption improving regulated workload verification efficiency by approximately 31% across industrial and banking environments. Telecom operators and domestic infrastructure providers are strengthening partnerships with hyperscale cloud firms to develop interoperable sovereign ecosystems aligned with regional digital autonomy objectives.

Germany Market Outlook: Germany maintains leadership through its advanced manufacturing ecosystem, Industry 4.0 deployment scale, and strong enterprise cybersecurity standards. Sovereign hybrid-cloud adoption among German industrial enterprises increased by approximately 34% in 2026 to secure AI-enabled operational data and factory automation systems. Domestic infrastructure operators are expanding localized hosting capacity, encrypted edge-cloud deployment, and sovereign compliance frameworks to support automotive, industrial automation, and public administration modernization strategies.

National Digital Infrastructure Scaling Accelerates

Asia-Pacific is emerging as the fastest-growing sovereign cloud market driven by AI industrialization, national cybersecurity modernization, and rapid expansion of localized cloud infrastructure. More than 46% of regulated enterprise cloud deployments across the region incorporated sovereign architecture controls in 2026, particularly within banking, telecom, and public-sector digital operations. India, Japan, and Singapore are increasing investments in sovereign AI compute clusters and low-latency edge-cloud corridors to support data localization mandates and advanced analytics workloads. Sovereign edge-cloud deployment activity across the region expanded by nearly 39% during 2026, improving operational visibility and localized transaction processing efficiency. Providers are prioritizing telecom alliances, encrypted cloud regions, and interoperable sovereign infrastructure ecosystems to strengthen deployment flexibility.

India Market Outlook: India is rapidly strengthening its sovereign cloud position through national digital governance initiatives, expanding domestic data-center infrastructure, and AI-focused cloud modernization programs. Enterprise sovereign cloud deployment increased by approximately 37% in 2026 as BFSI institutions, healthcare providers, and telecom operators accelerated localized data-processing strategies. Infrastructure firms are forming partnerships with global hyperscale providers to scale sovereign hosting environments, encrypted AI processing capabilities, and jurisdiction-controlled digital service platforms aligned with national cybersecurity objectives.

Localized Banking and Public Cloud Modernization

South America is witnessing increasing sovereign cloud deployment through financial-sector digitization, public-service modernization, and enterprise cybersecurity restructuring. Brazil and Chile remain the primary infrastructure hubs due to growing hyperscale investment activity and expanding domestic cloud-hosting ecosystems. Approximately 33% of regulated enterprises across the region expanded sovereign cloud integration during 2026 to strengthen localized control over transaction processing and sensitive enterprise data. Infrastructure scalability limitations and power-cost volatility continue affecting deployment consistency outside major urban centers. Cloud providers are responding through modular data-center expansion, telecom-driven sovereign cloud alliances, and hybrid-cloud deployment models supporting secure banking and public-sector workloads.

Brazil Market Outlook: Brazil leads the regional sovereign cloud market through its expanding fintech ecosystem, large enterprise infrastructure base, and strengthening data-localization frameworks. Sovereign cloud deployment across digital banking operations increased by nearly 29% in 2026 as financial institutions accelerated encrypted transaction processing and compliance automation initiatives. Telecom operators and domestic cloud providers are scaling localized hosting capacity, sovereign edge infrastructure, and AI-enabled operational analytics capabilities to support enterprise modernization and public administration digitization programs.

State-Backed Infrastructure Transformation Expands

Middle East & Africa sovereign cloud adoption is accelerating through government-led digital transformation programs, smart-city deployment, and localized cybersecurity modernization initiatives. The UAE and Saudi Arabia continue leading sovereign infrastructure investment activity through aggressive sovereign AI and cloud-localization strategies. In 2026, sovereign data-center deployment activity across Gulf economies increased by approximately 35%, supported by national digital sovereignty frameworks and hyperscale cloud partnerships. Financial institutions and public-sector operators are prioritizing encrypted sovereign cloud environments to improve jurisdiction-controlled analytics, operational resilience, and secure citizen-data management. Providers are investing in renewable-powered hosting infrastructure, sovereign edge-cloud architecture, and telecom-integrated digital ecosystems to support large-scale modernization projects.

United Arab Emirates Market Outlook: The UAE is strengthening its sovereign cloud leadership through advanced AI governance initiatives, large-scale smart-city infrastructure deployment, and strategic sovereign digital investment programs. Government-backed sovereign cloud adoption increased by approximately 32% in 2026, particularly across aviation, financial services, and public administration sectors. Telecom operators and cloud providers are forming long-term alliances to expand sovereign edge infrastructure, AI-ready hosting environments, and low-latency digital service platforms aligned with national cybersecurity and digital resilience priorities.

The sovereign cloud market is highly concentrated among global hyperscalers, regional infrastructure providers, telecom-cloud alliances, and cybersecurity-focused sovereign operators. Microsoft, Amazon Web Services, Google Cloud, Oracle, and IBM collectively account for nearly 58% of sovereign cloud deployment activity, competing aggressively against regional providers specializing in jurisdiction-controlled hosting and compliance-driven infrastructure. Competition is increasingly based on sovereign AI capability, workload localization speed, encryption efficiency, and interoperability performance, with confidential computing integration improving regulated workload protection efficiency by approximately 34%. Telecom operators are vertically integrating edge infrastructure and sovereign connectivity services, while regional players compete through domestic partnerships and public-sector deployment specialization. Strategic sovereign infrastructure alliances increased by nearly 29% in 2026 following stricter data-localization mandates and rising geopolitical compliance pressures. High infrastructure localization costs, cybersecurity certification complexity, and operational scalability requirements continue creating strong entry barriers. Competitive advantage now depends on localized infrastructure control, AI-ready sovereign architecture, compliance automation, and deep enterprise integration capability.

Microsoft Corporation

Amazon Web Services

Google Cloud

Oracle Corporation

IBM Corporation

VMware

OVHcloud

Deutsche Telekom AG

Orange Business

Alibaba Cloud

Tencent Cloud

Rackspace Technology

SAP SE

T-Systems International GmbH

Sovereign cloud technology is rapidly shifting from basic localized hosting toward AI-enabled, policy-driven infrastructure with integrated confidential computing and zero-trust orchestration. In 2026, nearly 52% of regulated enterprises adopted hardware-level encryption frameworks to secure workloads during processing, reducing unauthorized-access exposure by approximately 33%. Sovereign hybrid-cloud deployment improved workload portability efficiency by nearly 28% compared with legacy isolated private-cloud systems. Governments and BFSI operators are increasingly integrating policy-as-code governance tools, localized identity management, and sovereign SaaS ecosystems to strengthen operational resilience and compliance automation across mission-critical environments.

Emerging technologies including sovereign AI clusters, disconnected edge-cloud infrastructure, and quantum-resistant encryption are reshaping infrastructure strategy between 2026 and 2028. Deployment of sovereign AI processing nodes increased by approximately 37% during 2026 as healthcare, defense, and industrial enterprises accelerated localized AI inference operations. Confidential computing-enabled sovereign infrastructure delivers nearly 31% faster regulated workload verification than traditional virtualized environments, while reducing compliance management overhead by approximately 24%. Telecom operators and hyperscalers are expanding sovereign edge partnerships to support low-latency analytics, secure industrial IoT processing, and real-time digital governance operations.

Disruptive sovereign cloud models integrating fully disconnected AI environments and localized GPU orchestration are creating competitive advantages for providers with domestic infrastructure control and advanced cybersecurity capabilities. Enterprises investing early in interoperable sovereign AI architecture, edge-compute integration, and automated compliance intelligence are expected to achieve stronger operational sovereignty, faster deployment scalability, and lower long-term regulatory exposure through 2028.

February 2026 – Microsoft expanded its Sovereign Cloud portfolio with disconnected Azure Local and Foundry Local AI capabilities supporting fully offline AI processing environments. The infrastructure supports deployment across thousands of servers within sovereign boundaries, strengthening operational continuity for regulated sectors. Business impact included accelerated classified AI deployment and stronger jurisdiction-controlled infrastructure resilience.

April 2026 – The European Commission awarded a €180 million sovereign cloud framework contract to StackIT, Scaleway, Post Telecom, and Proximus under the EU Cloud Sovereignty Framework. The initiative strengthened European digital autonomy through localized infrastructure partnerships and sovereign compliance governance. Business impact included increased regional cloud independence and stronger domestic infrastructure positioning.

February 2025 – Oracle launched Oracle Fusion Cloud Applications on Oracle EU Sovereign Cloud across all 27 EU member states, enabling regulated organizations to operate AI-enabled finance, HR, and supply-chain workloads within EU-controlled infrastructure. Business impact included expanded enterprise AI adoption under localized governance requirements and stronger compliance-driven SaaS deployment capability. Source: (Oracle)

May 2026 – TCS expanded its SovereignSecure Cloud into the European Union through a three-layer sovereign infrastructure model supporting GDPR, DORA, and Cyber Resilience Act compliance. The framework integrated national sovereign cloud and enterprise cloud orchestration capabilities, improving workload localization flexibility for regulated industries. Business impact included accelerated sovereign AI deployment and stronger telecom-cloud service integration.

The Sovereign Cloud Market report provides detailed analysis across Public Cloud, Private Cloud, Hybrid Cloud, Community Cloud, and Multi-Cloud deployment models, with strategic assessment of evolving workload localization trends and sovereign AI infrastructure integration. The study evaluates operational adoption across Data Security, Compliance Management, Government Services, Digital Banking, and Healthcare Data Management applications while analyzing enterprise deployment intensity across Government Sector, BFSI, Healthcare, Defense Sector, IT and Telecom, and Public Institutions. More than 58% of regulated enterprise deployments assessed within the report involve hybrid or multi-cloud sovereign architecture frameworks integrated with confidential computing and zero-trust security layers.

The report delivers region-wise intelligence covering North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting infrastructure modernization, sovereign AI deployment, and localized compliance ecosystems between 2026 and 2033. It includes competitive benchmarking of hyperscalers, telecom-cloud alliances, and regional sovereign providers while identifying investment priorities, operational scalability trends, deployment bottlenecks, and strategic expansion opportunities across high-security digital infrastructure environments.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 117530 Million |

Market Revenue in 2033 | USD 725113.06 Million |

CAGR (2026 - 2033) | 25.54% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Microsoft Corporation, Amazon Web Services, Google Cloud, Oracle Corporation, IBM Corporation, VMware, OVHcloud, Deutsche Telekom AG, Orange Business, Alibaba Cloud, Tencent Cloud, Rackspace Technology, SAP SE, T-Systems International GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |