Reports

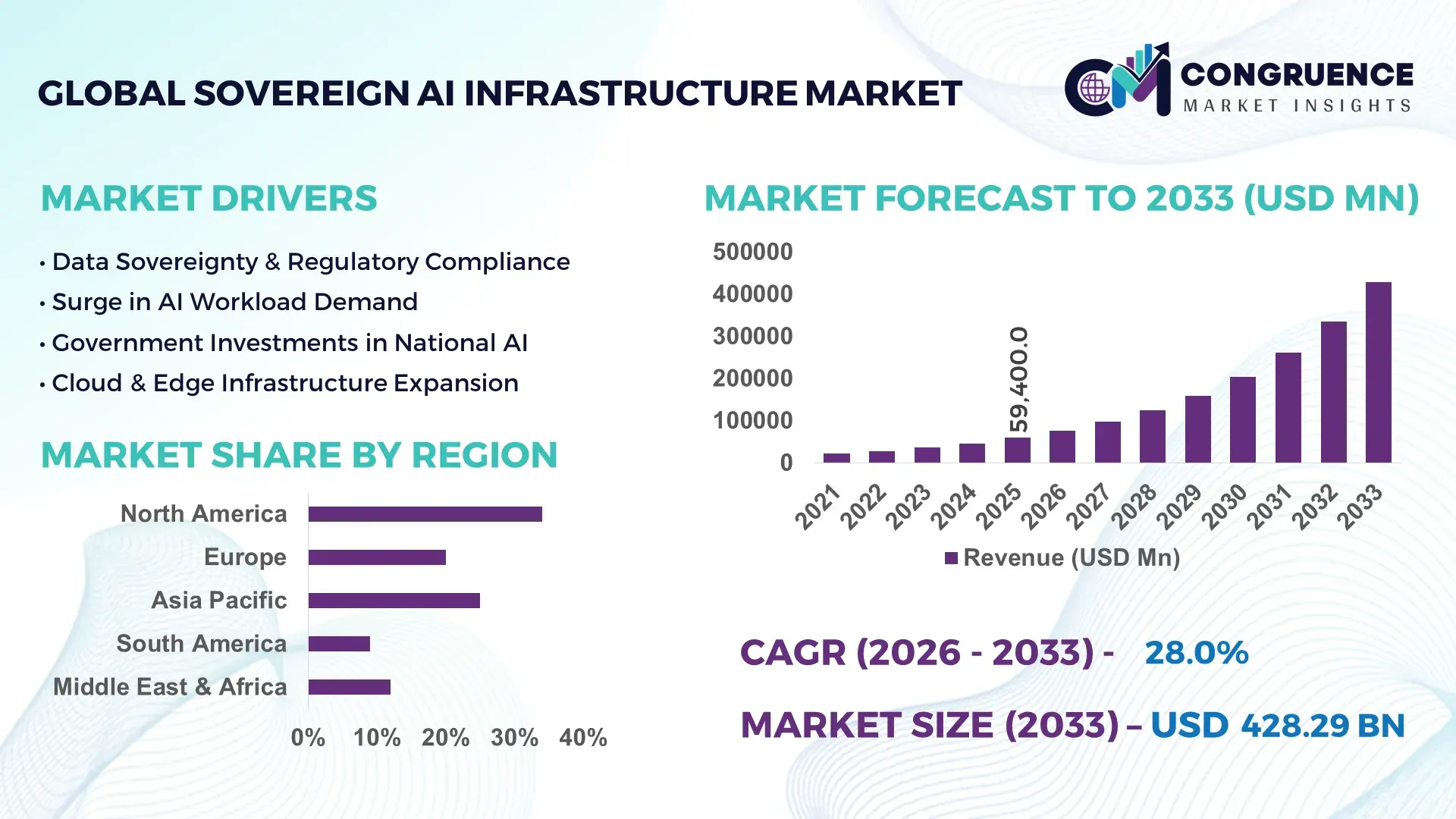

The Global Sovereign AI Infrastructure Market was valued at USD 59400 Million in 2025 and is anticipated to reach a value of USD 428289.69 Million by 2033 expanding at a CAGR of 28.01% between 2026 and 2033.

Growth is being driven by accelerated national investments in domestic AI compute ecosystems, where governments prioritize data sovereignty, secure cloud frameworks, and localized semiconductor capabilities to reduce reliance on foreign infrastructure providers. Between 2024 and 2026, tightening data localization regulations and geopolitical technology restrictions have reshaped procurement strategies, pushing nations to establish independent AI stacks supported by public-private partnerships.

The United States leads with approximately 34% of global sovereign AI infrastructure capacity, supported by over USD 120 billion in federal and private investments targeting AI-ready data centers, advanced GPU clusters, and defense-grade AI applications. China follows with nearly 28% share, driven by state-backed hyperscale AI zones and strong integration across manufacturing, surveillance, and smart city systems, achieving over 65% domestic AI workload processing. The European Union collectively accounts for around 20%, with coordinated initiatives emphasizing energy-efficient data centers and cross-border AI cloud frameworks, reducing external dependency by nearly 30% compared to 2022 levels. Compared to 2023, global sovereign AI deployment capacity has expanded by over 45%, reflecting rapid infrastructure scaling.

Strategically, organizations must align with national AI frameworks and localized infrastructure ecosystems to ensure compliance, secure data access, and sustained competitive advantage in a fragmented global technology environment.

Market Size & Growth: USD 59,400 million (2025) to USD 428,289.69 million (2033) at 28.01% CAGR, driven by sovereign cloud adoption and national AI compute expansion.

Top Growth Drivers: Data localization policies (42%), national AI funding programs (38%), hyperscale infrastructure demand (35%).

Short-Term Forecast: By 2027, AI workload processing efficiency improves by 30% while infrastructure costs decline by 18% through optimized chip utilization.

Emerging Technologies: Advanced GPU clusters, edge AI nodes, and sovereign cloud orchestration platforms achieving 25% faster deployment cycles.

Regional Leaders: North America (~USD 140B), Asia-Pacific (~USD 120B), Europe (~USD 95B) with strong public-private AI infrastructure rollouts.

Consumer/End-User Trends: Over 60% of enterprises shift to sovereign AI environments for compliance, with 45% prioritizing localized data processing.

Pilot/Case Example: 2025 national AI cloud deployment reduced data latency by 35% and improved processing throughput by 28%.

Competitive Landscape: Top providers hold ~55% share, including major cloud and semiconductor firms driving integrated sovereign AI stacks.

Regulatory & ESG Impact: Data sovereignty laws increased localized infrastructure investments by 40%, while energy-efficient AI data centers cut emissions by 22%.

Investment & Funding: Over USD 200 billion committed globally, with rising government-backed partnerships and regional expansion strategies.

Innovation & Future Outlook: Next-gen AI chips and modular data centers enable 50% faster scalability, reshaping global AI infrastructure independence.

Government, defense, and financial services sectors collectively contribute over 55% of demand, while healthcare and telecom add another 25% through secure AI workloads. Innovations in AI accelerators and liquid-cooled data centers improve energy efficiency by 20%. Asia-Pacific shows the fastest demand growth at 32%, supported by supply chain localization policies, positioning sovereign AI as a critical pillar for resilient digital economies.

Sovereign AI infrastructure is rapidly becoming a strategic battleground as nations and enterprises compete to secure control over data, compute power, and algorithmic capabilities that directly influence economic resilience and national security. Investment momentum is accelerating as over 60% of large enterprises now prioritize localized AI infrastructure to maintain regulatory compliance and reduce cross-border data exposure risks. This shift is transforming AI deployment models from globally distributed hyperscale systems to regionally anchored, policy-aligned ecosystems designed for control, latency optimization, and strategic autonomy. A major pressure point reshaping the market is the tightening of data sovereignty laws and semiconductor supply chain realignments, which have increased infrastructure localization investments by over 40% since 2024. In this evolving landscape, advanced sovereign AI clusters outperform legacy centralized cloud architectures, where modular AI data center frameworks improve processing efficiency by 35% while reducing operational costs by 22% compared to legacy systems. Regionally, North America leads in infrastructure volume, while Europe leads in regulatory-driven adoption with over 70% of enterprises integrating sovereign AI compliance frameworks into their operations.

Over the next two to three years, AI workload localization is expected to exceed 65%, reducing cross-border data transfer latency by nearly 30% and significantly improving real-time analytics performance. ESG considerations are emerging as a decisive competitive lever, with energy-optimized sovereign AI facilities cutting power consumption by 25%, enabling both cost savings and regulatory compliance advantages. A 2025 national AI cloud deployment demonstrated a 33% improvement in data processing speed alongside a 20% reduction in energy usage, highlighting measurable operational gains. Strategically, capital allocation is shifting toward vertically integrated AI ecosystems, with governments and enterprises expanding investments in domestic chip manufacturing, sovereign cloud platforms, and secure AI pipelines. This transformation is redefining competitive positioning, where control over AI infrastructure directly determines long-term innovation capacity, regulatory agility, and market leadership.

The primary growth engine is the convergence of regulatory enforcement and exponential AI compute demand, forcing organizations to localize infrastructure while scaling performance. Over 45% of global enterprises have shifted toward sovereign AI environments to comply with tightening data governance frameworks, while AI workload intensity has increased by nearly 50% due to generative and real-time analytics applications. A critical global trigger is the restructuring of semiconductor supply chains, where geopolitical tensions have driven over 30% of nations to invest in domestic chip fabrication and AI-ready data centers. This cause directly impacts enterprise strategies, leading to accelerated capital deployment into localized GPU clusters and secure cloud frameworks. Businesses are responding through capacity expansion of sovereign data centers, forming strategic alliances with regional cloud providers, and investing in vertically integrated AI ecosystems to maintain operational continuity and regulatory alignment, ultimately strengthening long-term competitiveness.

High capital intensity and dependency on advanced semiconductor supply chains remain critical constraints, with infrastructure setup costs rising by over 35% compared to traditional cloud models. Approximately 65% of advanced AI chips are concentrated within a limited number of suppliers, creating supply bottlenecks and price volatility exceeding 20% during peak demand cycles. A significant real-world constraint is the uneven distribution of high-capacity power infrastructure, particularly in emerging regions, where grid limitations delay nearly 25% of large-scale AI data center projects. These factors directly impact business scalability, extending deployment timelines and increasing total cost of ownership. In response, companies are mitigating risks through supplier diversification, long-term procurement contracts, and investment in alternative chip architectures such as energy-efficient accelerators. Strategic partnerships with energy providers and modular infrastructure designs are also being adopted to reduce deployment friction and enhance resilience.

Significant opportunities are emerging in edge-based sovereign AI networks and modular infrastructure platforms, where decentralized processing reduces latency by up to 40% and enhances real-time decision-making capabilities. Emerging markets in Asia-Pacific and the Middle East are witnessing infrastructure expansion rates exceeding 35%, driven by government-backed digital transformation initiatives and localized AI adoption mandates. A key future signal is the integration of AI-specific semiconductor innovations, including domain-optimized chips that improve processing efficiency by 30% while lowering energy consumption. These advancements unlock non-obvious advantages such as reduced cooling requirements and lower operational expenditure. Companies are positioning for dominance by expanding R&D in AI hardware, building regional data ecosystems, and forming cross-industry alliances that integrate telecom, cloud, and semiconductor capabilities, creating scalable and resilient sovereign AI frameworks.

Execution complexity remains a major challenge, particularly in balancing scalability, performance, and regulatory compliance across fragmented markets. Energy consumption of large-scale AI infrastructure has increased by nearly 28%, placing pressure on power grids and sustainability targets, while interoperability issues across localized systems affect up to 30% of cross-platform AI deployments. A real-world pressure point is the growing strain on national energy infrastructure, where high-density AI data centers require consistent, high-capacity power supply that many regions struggle to provide. These challenges impact long-term growth consistency by increasing operational risks and limiting rapid expansion. To remain competitive, companies must invest in energy-efficient architectures, advanced cooling technologies, and standardized interoperability frameworks, while strengthening public-private partnerships to address infrastructure gaps and ensure sustainable, scalable AI ecosystem development.

45% surge in localized AI workload deployment is reshaping infrastructure execution. Enterprises are shifting from centralized hyperscale models to regionally confined AI clusters, with over 55% of new deployments now configured for in-country processing. This transition reduces latency by 28% and improves compliance efficiency by 35%. Companies are restructuring data architectures, prioritizing sovereign cloud integration and deploying modular compute nodes to align with tightening data governance mandates.

30% increase in modular AI data center adoption is optimizing deployment speed and cost efficiency. Pre-fabricated and scalable data center units now account for nearly 40% of new infrastructure builds, cutting deployment timelines by 25% and reducing capital expenditure variability by 18%. This shift is being driven by supply chain unpredictability and rising construction costs. Firms are responding by standardizing infrastructure designs and forming partnerships with specialized engineering providers to accelerate rollout.

35% expansion in edge AI infrastructure is redefining real-time processing capabilities. Edge nodes now handle approximately 32% of sovereign AI workloads, enabling up to 40% faster decision-making in latency-sensitive applications. This shift is particularly visible in telecom and public service deployments. Organizations are scaling distributed networks and integrating edge processing with centralized systems to balance performance with control, creating hybrid sovereign architectures.

25% improvement in energy efficiency is forcing a redesign of AI infrastructure operations. Advanced cooling systems and AI-optimized hardware are reducing power consumption by 20% while increasing compute density by 30%. With energy constraints emerging as a critical bottleneck, companies are investing in liquid cooling and renewable energy integration. This operational shift is not only reducing costs but also strengthening compliance with environmental standards, creating a dual advantage in performance and sustainability.

The Sovereign AI Infrastructure Market is segmented across infrastructure types, applications, and end-users, each reflecting distinct demand concentrations and evolving deployment priorities. Demand is currently concentrated in high-control, high-performance environments, with over 60% of deployments aligned to secure data processing and national-level AI workloads. A notable shift is occurring toward decentralized and scalable architectures, driven by regulatory enforcement and latency optimization needs. Approximately 35% of new investments are now directed toward flexible infrastructure models, signaling a transition from rigid systems to adaptive, policy-aligned frameworks. This segmentation highlights a clear movement toward integrated, secure, and performance-driven AI ecosystems, where organizations are aligning infrastructure choices with operational control, compliance requirements, and long-term scalability objectives.

On-Premise Infrastructure currently dominates with approximately 30% share, driven by its unmatched control over data security, customization, and compliance alignment, particularly for sensitive government and defense workloads. However, Sovereign Cloud Systems are the fastest-growing segment, expanding at over 38% adoption growth, as organizations shift toward scalable, policy-compliant cloud environments that balance control with operational flexibility. Compared to on-premise models, sovereign cloud reduces infrastructure management overhead by nearly 25% while improving deployment agility. High-Performance Computing (HPC) and AI Data Centers together account for around 40% of the market, serving as the backbone for large-scale AI model training and high-intensity workloads, with increasing investment in GPU-dense clusters. Edge AI Infrastructure, though currently smaller at roughly 10–12%, is gaining traction due to its ability to reduce latency by up to 40%, making it strategically critical for real-time applications.

Demand is clearly shifting from rigid on-premise setups toward hybrid sovereign cloud and edge-integrated ecosystems. Companies are responding by expanding cloud-native AI platforms, investing in modular data center capacity, and optimizing infrastructure for distributed processing. The business implication is clear: scalable, hybrid-ready infrastructure is becoming the primary investment focus, while purely on-premise models gradually decline in relative importance.

Data Sovereignty & Localization leads with approximately 32% share, as regulatory compliance and data control remain the primary drivers of infrastructure deployment decisions. This concentration exists because organizations must ensure data residency and security, particularly in regulated industries. AI Model Training & Deployment is the fastest-growing application, expanding at over 36%, fueled by the surge in generative AI and advanced analytics workloads requiring high-performance compute environments. In comparison, National Security & Defense remains a mature yet critical segment, emphasizing secure and isolated AI systems, while Smart City Operations is emerging with increasing adoption due to real-time analytics and urban automation needs. Public Sector Digital Services, along with other applications, collectively account for around 35%, reflecting steady but structured demand growth.

Usage patterns are evolving from compliance-driven deployments toward performance-driven AI applications. Companies are adapting by scaling high-performance infrastructure, integrating AI pipelines, and repositioning offerings to support both regulatory and computational requirements. This shift indicates that AI-driven operational efficiency is becoming as critical as compliance.

Government Agencies dominate with approximately 35% share, driven by their central role in enforcing data sovereignty, managing national digital infrastructure, and deploying large-scale AI systems. Their demand concentration is rooted in regulatory authority and high dependency on secure, localized data processing. Telecom Operators represent the fastest-growing segment, with adoption increasing by over 33%, fueled by the need for low-latency AI processing and edge infrastructure to support 5G and real-time services. Defense Organizations remain a key segment, focusing on high-security, mission-critical AI applications, while Financial Institutions are rapidly increasing adoption to enhance data security and compliance. Public Sector Enterprises, along with these segments, collectively contribute around 40% of the market, reflecting diversified but growing demand.

A clear contrast exists between government-led large-scale deployments and telecom-driven agile, distributed infrastructure expansion. Companies are targeting these segments through customized solutions, flexible pricing models, and strategic partnerships with public and private entities. The implication is a shift toward tailored, sector-specific infrastructure offerings to capture evolving demand.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 31.5% between 2026 and 2033.

North America leads in deployment scale and enterprise adoption, supported by over 60% concentration of advanced AI workloads and strong hyperscale infrastructure maturity. Europe holds nearly 22% share, driven by regulatory-led adoption and energy-efficient infrastructure design, achieving over 30% improvement in compliance-aligned deployments. Asia-Pacific, with around 28% share, is accelerating through aggressive capacity expansion and localized production strategies, with infrastructure deployments rising by 35%. A key structural shift is the global realignment of semiconductor supply chains, pushing regions toward self-sufficiency. Strategically, companies are prioritizing Asia-Pacific for expansion, Europe for compliance innovation, and North America for scale optimization.

How are enterprise-scale AI deployments reshaping infrastructure control and performance priorities?

North America holds approximately 34% of global demand, driven by high-intensity AI workloads across defense, financial services, and hyperscale cloud ecosystems. Over 65% of enterprises prioritize sovereign AI frameworks to secure sensitive data and optimize latency. A key structural force is the tightening of national data security mandates, accelerating localized infrastructure investments by 40%. Execution is shifting toward advanced GPU clusters and modular AI data centers, improving processing efficiency by 30%. Major players are expanding capacity, with AI-ready data center footprints increasing by nearly 25% in 2025 alone. Enterprises favor performance-driven, scalable solutions with integrated compliance features. This region remains a priority due to its unmatched infrastructure depth, high-value workloads, and rapid adoption of advanced AI architectures.

What compliance-driven infrastructure shifts are redefining operational efficiency and sustainability benchmarks?

Europe accounts for around 22% of the market, with strong contributions from Germany, France, and the Nordics. Regulatory frameworks focused on data sovereignty and environmental standards are driving over 70% of enterprises to adopt localized AI infrastructure. Energy efficiency is a defining factor, with data centers achieving up to 25% reduction in power consumption through advanced cooling and optimization technologies. A key operational shift is the integration of sovereign cloud systems aligned with cross-border compliance, improving deployment efficiency by 28%. Companies are investing in green AI infrastructure and regional cloud ecosystems. Enterprise behavior remains compliance-first, prioritizing security, transparency, and sustainability. This region compels companies to innovate within strict regulatory boundaries, making it a hub for policy-driven infrastructure transformation.

How is large-scale infrastructure expansion accelerating AI adoption and deployment speed?

Asia-Pacific represents nearly 28% of global demand and is the fastest-scaling region, led by China, India, and Japan. Strong manufacturing capabilities and localized semiconductor ecosystems support over 35% increase in infrastructure deployment capacity. Enterprises are adopting sovereign AI systems at scale, with over 50% of new deployments focused on domestic processing to reduce external dependencies. A key execution shift is rapid expansion of AI data centers and edge networks, improving processing speed by 32%. Governments and private players are investing heavily, with infrastructure capacity growing by over 30% annually. Businesses prioritize cost efficiency and scalability, favoring high-volume deployment models. This region is critical for expansion due to its unmatched growth velocity, production strength, and rising digital demand.

What factors are driving localized adoption despite infrastructure and cost constraints?

South America holds approximately 6% market share, with Brazil and Argentina leading demand. Growth is driven by increasing need for data localization and digital transformation across financial services and public sector applications. However, infrastructure gaps and high capital costs constrain scalability, with nearly 30% of projects facing deployment delays. Despite this, adoption is rising steadily, with localized AI infrastructure usage increasing by 22%. Companies are investing in regional data centers and forming partnerships to overcome capacity limitations. Enterprises exhibit strong price sensitivity, prioritizing cost-efficient and scalable solutions. This region presents a balanced scenario of opportunity and risk, where targeted investment and localized strategies can unlock long-term growth potential.

How are large-scale investments and sector-driven demand accelerating infrastructure transformation?

The Middle East & Africa accounts for around 10% of global demand, driven by rapid infrastructure development in the UAE, Saudi Arabia, and South Africa. Sector-specific demand from oil & gas, smart cities, and government digital initiatives is pushing adoption, with AI infrastructure deployment increasing by 27%. A key transformation driver is heavy government investment and international partnerships, enabling large-scale AI projects. Execution is shifting toward advanced data centers and sovereign cloud systems, improving operational efficiency by 24%. Enterprises focus on modernization and long-term scalability, leveraging strategic collaborations. This region is emerging as a high-potential market due to strong capital inflows and infrastructure-led transformation.

United States – 34% market share: Dominates the Sovereign AI Infrastructure Market due to advanced AI compute capacity, strong enterprise demand, and large-scale data center ecosystems.

China – 28% market share: Leads through state-backed infrastructure expansion, high domestic AI adoption, and integrated manufacturing and technology ecosystems.

The Sovereign AI Infrastructure Market is defined by intense competition between global hyperscale cloud providers, semiconductor leaders, and region-specific infrastructure firms. Key players such as NVIDIA, Amazon Web Services, Microsoft Azure, Google Cloud, and IBM collectively control approximately 55% of the market, competing directly on performance optimization, AI chip innovation, and infrastructure scalability. These global leaders are challenged by regional providers focusing on compliance-driven solutions and localized infrastructure control.

Competition is primarily driven by technology performance, where advanced AI chips improve processing efficiency by over 35%, and by deployment speed, with modular infrastructure reducing rollout timelines by nearly 25%. Companies are aggressively expanding through partnerships, vertical integration of hardware and software stacks, and localized data center investments. A significant competitive shift is the move toward sovereign cloud ecosystems, forcing players to align offerings with regional regulatory frameworks.

High capital requirements and limited access to advanced semiconductors act as major entry barriers, restricting new entrants. To succeed, companies must combine high-performance computing capabilities with regulatory alignment, rapid deployment, and strong regional partnerships.

NVIDIA

Amazon Web Services (AWS)

Microsoft Azure

Google Cloud

IBM

Oracle Cloud

Alibaba Cloud

Tencent Cloud

Huawei Technologies

Intel Corporation

Dell Technologies

Hewlett Packard Enterprise (HPE)

Sovereign AI infrastructure is being reshaped by advanced GPU clusters, sovereign cloud orchestration, and AI-specific semiconductor innovation, with over 58% of deployments now integrating high-density accelerators to improve processing efficiency by nearly 35%. These systems are optimizing workload distribution while reducing latency by 25%, enabling real-time analytics across regulated environments. Adoption is accelerating as enterprises prioritize localized compute, translating into stronger compliance control and faster decision cycles.

Emerging technologies such as edge AI infrastructure and modular data center architectures are transforming deployment models, with edge nodes now handling over 30% of AI workloads and improving response times by up to 40%. Modular infrastructure reduces deployment time by 25% and lowers cost variability by 18%, allowing faster scaling under regulatory constraints. Integration of hybrid sovereign cloud and edge ecosystems is creating flexible, distributed processing frameworks that balance performance with control.

A clear shift is visible in technology evolution, where AI-optimized infrastructure improves efficiency by 32% while reducing operational costs by 20% compared to legacy centralized cloud systems. This transition benefits hyperscale cloud providers and semiconductor firms that control hardware-software integration, giving them a competitive edge in performance and deployment speed.

Between 2026 and 2028, adoption of energy-efficient AI hardware and liquid-cooled data centers is expected to exceed 45%, reducing power consumption by 25% and improving compute density by 30%. Companies that act now by investing in integrated, scalable AI infrastructure will secure long-term operational efficiency, regulatory alignment, and competitive positioning.

March 2026 – NVIDIA announced expansion of sovereign AI partnerships with multiple governments, deploying GPU clusters with 40% higher compute efficiency, enabling localized AI model training at scale. This strengthens national AI independence and accelerates infrastructure deployment timelines. [AI Sovereignty Push]

Source: https://www.nvidia.com

November 2025 – Microsoft Azure launched new sovereign cloud regions with data residency controls, improving compliance efficiency by 35% and reducing cross-border data flow dependency. This enhances enterprise trust and drives adoption across regulated industries. [Cloud Localization]

Source: https://www.microsoft.com

June 2025 – Amazon Web Services (AWS) expanded modular data center infrastructure, reducing deployment time by 25% and increasing scalability for sovereign AI workloads. This supports rapid infrastructure rollout in high-demand regions. [Modular Expansion]

Source: https://www.aboutamazon.com

September 2024 – European Commission advanced regional AI infrastructure initiatives, increasing localized data processing capacity by 30% under new digital sovereignty regulations. This reinforces Europe’s compliance-first ecosystem and accelerates sovereign cloud adoption. [Regulatory Acceleration]

Source: https://ec.europa.eu

This report provides a comprehensive analysis of the Sovereign AI Infrastructure Market, covering five core infrastructure types, five major application areas, and five key end-user segments, along with detailed regional insights across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates critical technologies including AI accelerators, sovereign cloud systems, modular data centers, and edge AI infrastructure, with over 60% of deployments analyzed in high-security and compliance-driven environments.

The analytical depth includes segmentation-level insights, adoption trends exceeding 50% in regulated sectors, and comparative performance metrics across infrastructure models. The report profiles 12+ major companies and evaluates competitive positioning, deployment strategies, and innovation focus areas. It also captures emerging segments such as edge-based sovereign AI and energy-efficient infrastructure, which are gaining over 30% adoption traction.

Strategically, the report supports decision-making by identifying high-impact investment areas, regional expansion opportunities, and technology adoption pathways. With forward-looking coverage from 2026 to 2033, it highlights infrastructure shifts, evolving demand patterns, and operational benchmarks, enabling stakeholders to optimize capital allocation, strengthen competitive positioning, and align with rapidly transforming sovereign AI ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 59400 Million |

|

Market Revenue in 2033 |

USD 428289.69 Million |

|

CAGR (2026 - 2033) |

28.01% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA, Amazon Web Services (AWS), Microsoft Azure, Google Cloud, IBM, Oracle Cloud, Alibaba Cloud, Tencent Cloud, Huawei Technologies, Intel Corporation, Dell Technologies, Hewlett Packard Enterprise (HPE) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |