Reports

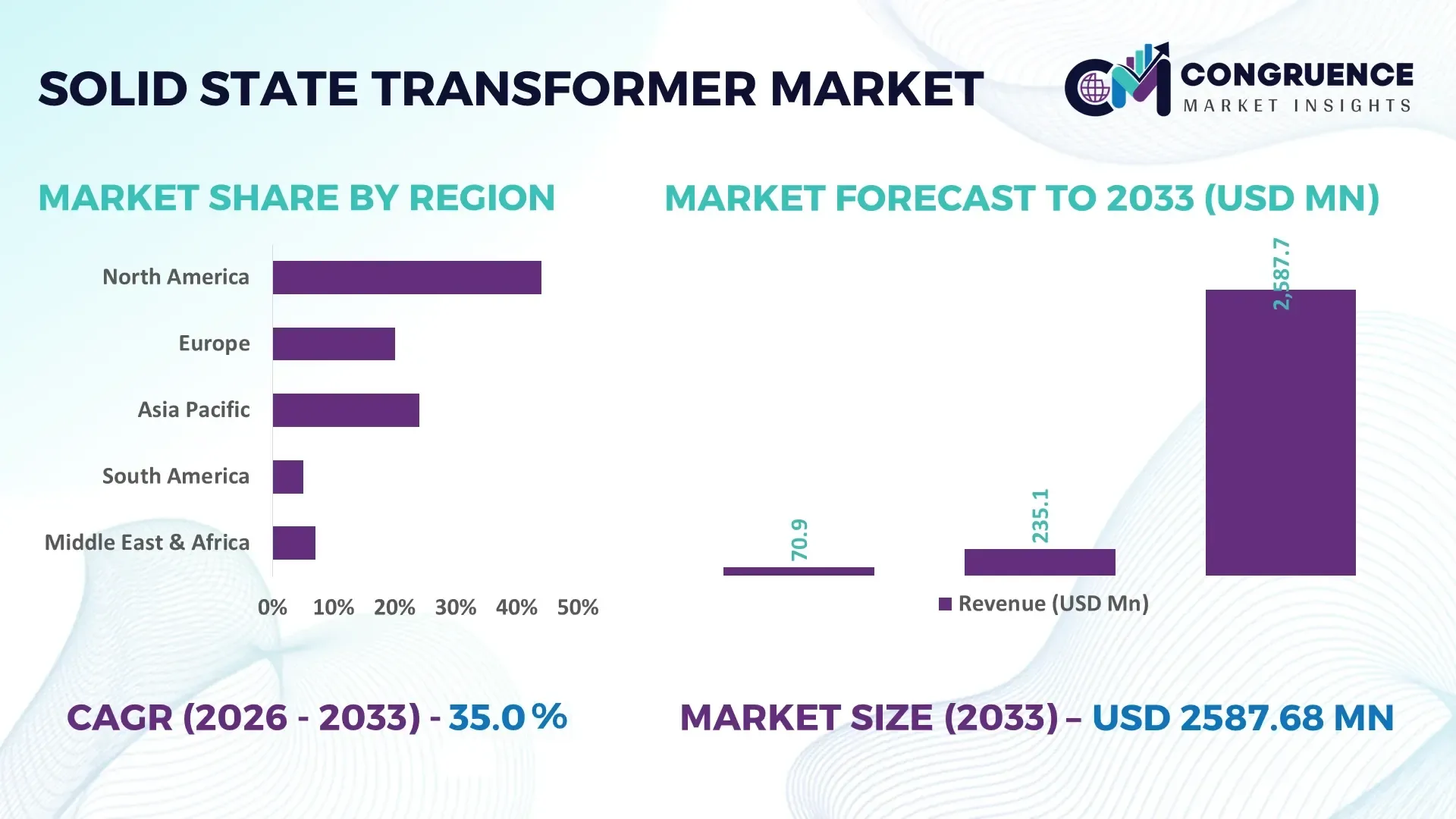

The Global Solid-state Transformer Market was valued at USD 235.11 Million in 2025 and is anticipated to reach a value of USD 2587.68 Million by 2033 expanding at a CAGR of 34.96% between 2026 and 2033. Rapid deployment of smart grids, high-power EV charging infrastructure, silicon carbide power electronics, and renewable energy integration is accelerating commercial adoption of advanced solid-state transformer technologies across modern electricity networks.

China dominates the global Solid-state Transformer Market with nearly 38% of ongoing grid modernization deployments, supported by extensive investment in ultra-high-voltage transmission, advanced power electronics manufacturing, and EV infrastructure. In comparison, the United States is strengthening deployment through utility-led demonstration programs and domestic semiconductor initiatives, while more than 65% of newly installed high-capacity charging corridors are evaluating intelligent power conversion systems amid continued global supply-chain diversification.

Strategic investments in localized manufacturing, wide-bandgap semiconductor capabilities, and utility partnerships will define long-term competitive leadership across the global Solid-state Transformer Market.

Market Size & Growth: USD 235.11 Million in 2025, projected to reach USD 2587.68 Million by 2033 at a CAGR of 34.96%, driven by smart grid expansion and next-generation power electronics.

Top Growth Drivers: Grid modernization (42%), EV charging infrastructure (37%), and renewable energy integration (33%) remain the primary market accelerators.

Short-Term Forecast: By 2028, power conversion efficiency is expected to improve by over 20% while operational maintenance costs decline by approximately 18%.

Emerging Technologies: AI-enabled grid control, silicon carbide semiconductors, and modular converter architectures are improving efficiency, reliability, and system intelligence.

Regional Leaders: Asia-Pacific leads with over USD 1.1 Billion potential, followed by North America above USD 720 Million and Europe exceeding USD 510 Million through advanced grid investments.

Consumer/End-User Trends: More than 55% of utility modernization projects are incorporating bidirectional power flow and intelligent distribution technologies.

Pilot/Case Example: A 2026 utility demonstration reduced conversion losses by nearly 30% while improving voltage regulation across distributed renewable energy assets.

Competitive Landscape: The top five companies collectively account for approximately 48% of the market, with competition centered on digital grid technologies and power conversion efficiency.

Regulatory & ESG Impact: Grid decarbonization initiatives have increased investment in advanced electrical infrastructure by more than 35% across major economies.

Investment & Funding: More than USD 3 Billion has been directed toward manufacturing expansion, strategic partnerships, and wide-bandgap semiconductor development amid ongoing regional supply-chain realignment.

Innovation & Future Outlook: Digital substations, hybrid AC/DC networks, and high-frequency transformer platforms are reshaping future grid architectures and accelerating commercialization.

The Solid-state Transformer Market is expanding across renewable energy integration, EV fast-charging networks, rail electrification, and intelligent distribution systems. Recent advances in silicon carbide devices, modular converter platforms, and AI-enabled grid monitoring have improved operating efficiency by over 20%. Increasing localization of semiconductor production and grid resilience programs in 2026 is strengthening supply security while supporting broader deployment, setting the stage for deeper strategic market competition.

Solid-state transformers are becoming a strategic investment priority as utilities, industrial operators, and transport networks modernize electrical infrastructure for digital, decentralized power systems. The market is gaining competitive importance because conventional transformers cannot efficiently manage bidirectional energy flows required by renewable generation, battery storage, and ultra-fast EV charging. Continued semiconductor supply-chain restructuring and government-backed grid resilience programs in 2026 are accelerating procurement of intelligent power conversion equipment across critical infrastructure projects.

Compared with conventional transformers, solid-state transformer platforms typically improve power conversion efficiency by 3–5% while reducing equipment footprint by nearly 40% through high-frequency operation and advanced silicon carbide semiconductors. China leads commercial-scale pilot deployment through large smart-grid investments, whereas Germany focuses on industrial automation and DC factory networks, and the United States prioritizes utility demonstration projects and defense-related microgrid applications. Over the next two to three years, digital substation deployments are expected to increase by more than 30%, with utilities expanding medium-voltage DC integration across urban distribution networks.

A practical example is the deployment of solid-state transformers within EV charging corridors, where dynamic voltage regulation improves charging stability while lowering maintenance requirements. Manufacturers are expanding partnerships with semiconductor suppliers, utilities, and system integrators to accelerate commercialization and localized production. Companies that strengthen power electronics capabilities, digital grid integration, and manufacturing resilience will establish stronger competitive positioning as electricity networks transition toward intelligent, flexible, and decentralized architectures.

Grid modernization programs, renewable energy integration, and high-power EV charging infrastructure remain the primary structural drivers for solid-state transformer adoption. More than 60% of newly planned digital substations are evaluating power-electronics-based architectures, while silicon carbide devices improve conversion efficiency by up to 5% and reduce system footprint by approximately 40%. China continues expanding ultra-high-voltage transmission and intelligent distribution networks, encouraging suppliers to scale domestic manufacturing and component sourcing. In response, leading companies are increasing investment in modular converter platforms, localized semiconductor partnerships, and advanced digital control software. A key strategic outcome is the ability to support bidirectional power flow, improving grid flexibility while reducing operational losses across distributed energy networks.

Commercial deployment remains constrained by high equipment costs, limited manufacturing scale, and compatibility challenges with legacy electrical infrastructure. Solid-state transformer systems typically require 30–45% higher initial capital investment than conventional transformer installations, while specialized power semiconductors account for nearly 35% of total system cost. The global dependence on advanced silicon carbide fabrication continues to expose manufacturers to component supply fluctuations, particularly during semiconductor allocation cycles. Companies are addressing these constraints through localized sourcing, long-term supplier agreements, modular product standardization, and design optimization. Strengthening interoperability with existing substations has become a critical operational priority to improve project economics and accelerate commercial acceptance.

Emerging medium-voltage DC distribution systems, intelligent microgrids, and industrial electrification present substantial long-term opportunities for solid-state transformer suppliers. More than 50% of planned industrial energy modernization projects now incorporate digital monitoring platforms, while AI-assisted power management improves network utilization by approximately 20%. Japan and South Korea continue investing in advanced factory automation and resilient energy infrastructure, creating demand for compact, intelligent power conversion systems. Manufacturers are expanding R&D programs, collaborating with software developers, and integrating predictive diagnostics into transformer platforms. An important strategic opportunity lies in delivering hardware combined with digital energy management services, creating higher-value recurring business models beyond equipment sales.

Moving from demonstration projects to large-scale deployment remains the industry's most significant execution challenge. Integrating solid-state transformers into existing transmission and distribution networks requires advanced protection systems, digital communication standards, and skilled engineering resources. More than 40% of utilities identify grid integration complexity as a major implementation barrier, while cybersecurity requirements for intelligent substations continue to expand. The United States and several European industrial markets are tightening grid security standards, increasing engineering and compliance requirements. Companies must invest in software validation, workforce development, standardized control platforms, and utility partnerships to ensure reliable deployment while maintaining operational consistency and long-term infrastructure resilience.

Advanced Silicon Carbide Integration: Silicon carbide power devices are replacing conventional silicon components across new solid-state transformer platforms, improving conversion efficiency by 4–6% while reducing thermal losses by nearly 30%. Japanese and U.S. manufacturers are expanding long-term wafer procurement agreements and vertically integrating semiconductor supply chains following continued component shortages, enabling faster production cycles and improved product reliability for utility-scale deployments.

Digital Substation Intelligence Expands: Utilities are embedding AI-driven monitoring, predictive diagnostics, and edge-based control into solid-state transformer installations, reducing unplanned maintenance by approximately 25% and improving asset utilization by nearly 20%. Grid digitalization policies and cybersecurity upgrades are accelerating deployment, prompting equipment manufacturers to strengthen software partnerships and integrate cloud-enabled operational analytics into next-generation transformer platforms.

Medium-Voltage DC Networks Scale: Industrial operators and transport infrastructure developers are increasing adoption of medium-voltage DC architectures, lowering distribution losses by around 8% while improving renewable integration efficiency by more than 15%. China and Germany are prioritizing pilot deployments in manufacturing clusters, encouraging transformer suppliers to redesign modular systems that simplify installation and reduce lifecycle engineering costs across complex electrical networks.

Localized Manufacturing Strategies Rise: Manufacturers are restructuring production footprints to reduce semiconductor sourcing risks, with localized component procurement increasing by nearly 35% and average lead times falling about 18%. Supply-chain diversification following global trade disruptions is driving partnerships between transformer producers, semiconductor companies, and system integrators. A notable shift is the growing emphasis on regional engineering support alongside manufacturing capacity, strengthening customer retention and accelerating project commissioning.

Smart Transformers represent the leading segment because they combine intelligent monitoring, bidirectional power management, and seamless integration with digital substations and distributed energy resources. Utilities increasingly prioritize these systems for operational visibility and automated grid balancing, with nearly 45% of new demonstration projects incorporating digital communication capabilities. Distribution Transformers remain widely deployed across conventional distribution networks due to lower installation complexity, while Power Transformers continue serving high-capacity transmission applications where reliability remains the primary procurement criterion.

Hybrid Transformers are emerging as the fastest-growing segment as operators seek gradual modernization without replacing entire electrical infrastructures. Traction Transformers continue expanding alongside railway electrification programs, particularly in China and Europe, while advanced Distribution Transformers remain essential for urban grid expansion. Manufacturers are investing in modular product platforms, digital diagnostics, and silicon carbide converter integration, reducing maintenance requirements by nearly 20% and improving operational flexibility. These shifting investment priorities reflect growing preference for intelligent power conversion over conventional transformer architectures.

Smart Grids remain the largest application segment because they require intelligent voltage regulation, bidirectional power flow, and real-time grid control to integrate distributed renewable generation. Approximately 60% of advanced grid modernization initiatives now evaluate power-electronics-based transformer technologies to improve operational resilience. Renewable Energy applications continue expanding through solar and battery storage integration, while Industrial Power deployments emphasize stable voltage quality and improved power efficiency for automated manufacturing facilities.

Electric Vehicles represent the fastest-growing application as ultra-fast charging infrastructure requires compact, high-efficiency power conversion capable of dynamic load management. Railways continue adopting solid-state transformer technologies to improve traction efficiency and reduce maintenance intervals, while Renewable Energy installations increasingly integrate digital transformer architectures for decentralized energy systems. Companies are strengthening collaborations with utilities, charging network operators, and industrial automation providers while expanding localized manufacturing capacity to support rapidly evolving deployment requirements and improve system interoperability.

Utilities account for the largest share of demand because they operate extensive transmission and distribution infrastructure requiring intelligent voltage regulation, renewable integration, and grid resilience upgrades. Nearly 55% of ongoing digital substation projects are led by electric utilities upgrading aging infrastructure with advanced power electronics. Industrial facilities remain significant buyers where uninterrupted power quality directly influences manufacturing productivity, while Commercial Buildings increasingly adopt intelligent energy management systems to improve operational efficiency.

Renewable Energy operators are the fastest-growing end-user group as battery storage, solar parks, and hybrid energy systems require bidirectional power conversion and flexible grid interaction. Transportation organizations continue investing in electrified rail systems and high-capacity charging infrastructure, encouraging equipment suppliers to customize compact transformer designs and integrated monitoring platforms. Companies are expanding strategic partnerships with utilities, engineering firms, and renewable developers while introducing application-specific product portfolios that improve deployment speed, lifecycle performance, and operational reliability across multiple infrastructure environments.

Asia-Pacific accounted for the largest market share at 43.8% in 2025 however, North America is expected to register the fastest growth, expanding at a 36.8% CAGR between 2026 and 2033.

Advanced Grid Digitalization Accelerates Commercial Deployment

North America is strengthening its position through utility modernization, high-power EV charging deployment, and expanding medium-voltage DC infrastructure. The region represents approximately 27% of global deployment activity, supported by strong investment in digital substations and resilient electricity networks. Utilities continue replacing aging equipment with intelligent power conversion platforms capable of integrating distributed renewable resources. More than 45% of recently approved smart grid demonstration programs now evaluate solid-state transformer technology. Strategic partnerships between semiconductor manufacturers, utilities, and electrical equipment suppliers are shortening commercialization timelines while strengthening domestic supply-chain resilience and improving deployment consistency across critical infrastructure projects.

United States Market Outlook: The United States remains the regional technology leader through large-scale grid modernization, defense microgrid deployment, and rapid expansion of ultra-fast EV charging infrastructure. Federal support for domestic semiconductor manufacturing has strengthened the availability of advanced silicon carbide devices essential for solid-state transformer production. More than 60% of utility-funded intelligent grid pilot programs are concentrated in the United States, encouraging manufacturers to expand engineering centers, localized assembly, and strategic collaborations with transmission operators and digital energy solution providers.

Industrial Electrification Drives Infrastructure Modernization

Europe accounts for nearly 24% of global market activity, supported by industrial electrification, renewable integration, and cross-border electricity modernization initiatives. Utilities increasingly deploy intelligent transformer technologies to improve voltage stability and grid flexibility while supporting decentralized energy systems. More than 40% of newly modernized substations across key industrial economies incorporate digital monitoring capabilities. Strong environmental regulations and investment in resilient electricity infrastructure continue encouraging manufacturers to accelerate innovation, establish regional engineering partnerships, and expand advanced power electronics production capacity.

Germany Market Outlook: Germany leads European deployment through advanced industrial automation, factory electrification, and smart manufacturing initiatives. The country's extensive renewable integration strategy has increased demand for intelligent distribution equipment capable of managing variable energy flows. More than 35% of large industrial energy modernization projects include advanced digital power management technologies, encouraging transformer manufacturers to expand local R&D, software integration capabilities, and collaborative development programs with industrial automation companies.

Manufacturing Scale Strengthens Global Leadership

Asia-Pacific dominates the global Solid-state Transformer Market through extensive manufacturing capacity, large-scale utility investments, and rapid expansion of electric mobility infrastructure. The region contributes approximately 44% of global deployment activity and remains the primary production hub for advanced power electronics. Massive smart grid expansion, railway electrification, and renewable integration programs continue driving equipment demand. Manufacturing localization and semiconductor ecosystem development have reduced production lead times by nearly 20%, enabling suppliers to scale commercial deliveries while supporting export-oriented growth across international infrastructure markets.

China Market Outlook: China remains the world's largest market owing to extensive ultra-high-voltage transmission development, advanced semiconductor manufacturing, and rapid deployment of digital substations. The country accounts for nearly 38% of global smart grid demonstration capacity while continuously expanding high-power charging infrastructure and renewable integration projects. Domestic manufacturers are increasing investment in silicon carbide technologies, automated production facilities, and vertically integrated supply chains, reinforcing China's leadership in intelligent transformer commercialization.

Renewable Infrastructure Expands Deployment Potential

South America is experiencing gradual adoption as renewable energy expansion, transmission upgrades, and industrial electrification create demand for advanced power conversion technologies. The region contributes approximately 4% of global installations, with deployment concentrated in utility modernization and renewable integration projects. Transmission infrastructure limitations continue slowing broader commercialization, although recent investment in digital substations and grid reliability programs is improving project execution. Equipment suppliers are strengthening partnerships with regional utilities while introducing modular transformer solutions designed for flexible deployment and simplified maintenance requirements.

Brazil Market Outlook: Brazil leads regional demand through expanding renewable generation, national transmission upgrades, and industrial electricity modernization. Large hydroelectric resources combined with increasing solar capacity require more flexible grid management technologies capable of supporting bidirectional power flow. Utilities continue evaluating intelligent transformer platforms for high-capacity transmission corridors, while manufacturers are strengthening local technical support, engineering partnerships, and assembly operations to improve deployment efficiency across geographically diverse electricity networks.

Grid Modernization Supports Infrastructure Transformation

The Middle East & Africa market is advancing through utility modernization, smart city development, and investment in resilient electricity infrastructure. The region accounts for approximately 3% of global deployment, with demand concentrated around large infrastructure projects and renewable energy integration. Governments continue investing in intelligent transmission systems capable of improving power quality and operational efficiency. Several national grid modernization initiatives now include advanced digital substations, encouraging global manufacturers to establish technology partnerships, regional service networks, and localized engineering capabilities for long-term market expansion.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's strongest strategic market due to extensive investment in smart grid infrastructure, industrial diversification, and renewable energy development. Large-scale urban infrastructure and industrial projects are increasing demand for intelligent electrical equipment capable of supporting digital power management. More than 30% of recently announced grid modernization initiatives include advanced automation technologies, prompting international equipment suppliers to expand regional partnerships, technical training programs, and localized engineering support for critical energy infrastructure.

The competitive landscape is led by Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, and Mitsubishi Electric, collectively controlling approximately 48% of global market activity. Global technology leaders compete against regional power equipment manufacturers on digital intelligence, while semiconductor specialists compete with conventional OEM suppliers through silicon carbide innovation and converter integration. Competition is driven by conversion efficiency, lifecycle cost, engineering customization, and supply-chain resilience rather than equipment pricing alone. Advanced platforms deliver 3–5% higher efficiency, localized manufacturing reduces component lead times by nearly 20%, and modular architectures shorten installation schedules by approximately 25%. Companies are strengthening positions through semiconductor partnerships, utility alliances, localized production, and vertical integration of power electronics. The competitive shift is moving toward software-defined grid equipment and secured semiconductor supply instead of traditional transformer manufacturing scale. High certification requirements, semiconductor expertise, and utility qualification cycles create substantial entry barriers. Sustainable competitive advantage depends on integrated hardware, intelligent control software, resilient supply networks, and rapid commercialization capabilities.

Hitachi Energy

Siemens Energy

GE Vernova

Schneider Electric

Mitsubishi Electric

Eaton

ABB

Toshiba Energy Systems & Solutions

Fuji Electric

Hyosung Heavy Industries

CG Power and Industrial Solutions

Bharat Heavy Electricals Limited (BHEL)

Alstom

SPX Technologies

Wide-bandgap semiconductor technologies are transforming solid-state transformer performance. Silicon carbide devices have become the preferred platform because they improve conversion efficiency by 3–5%, reduce switching losses by nearly 30%, and enable significantly higher power density than conventional silicon-based systems. More than 45% of advanced demonstration projects now incorporate silicon carbide power modules, allowing utilities and industrial operators to reduce equipment footprint while improving thermal management. Companies with integrated semiconductor capabilities gain stronger control over product performance and supply continuity.

Artificial intelligence, digital twins, edge computing, and predictive diagnostics are becoming core differentiators across intelligent transformer platforms. AI-enabled monitoring reduces unplanned maintenance by approximately 25%, while digital asset management improves equipment utilization by nearly 20%. Compared with legacy transformer monitoring systems, integrated digital platforms deliver faster fault detection and more accurate asset health prediction. Utilities, charging infrastructure operators, and industrial manufacturers increasingly prioritize software-enabled transformer platforms that support remote operation and predictive maintenance.

Between 2026 and 2028, medium-voltage DC architectures, modular converter platforms, and cybersecurity-enhanced control systems will define next-generation deployments. Standardized digital interfaces are expected to support more than 35% of new intelligent grid projects, enabling faster interoperability and simplified integration. Manufacturers investing early in software-defined power electronics, semiconductor partnerships, and secure digital ecosystems will strengthen operational competitiveness, accelerate commercial deployment, and establish long-term leadership as intelligent electricity networks continue expanding.

January 2025: Hitachi Energy secured an agreement with Siemens Mobility to supply 360 RESIBLOC Rail traction transformers for Munich's new S-Bahn fleet, expanding advanced transformer deployment for electrified rail infrastructure while strengthening long-term collaboration in sustainable transportation.

August 2025: Eaton completed the acquisition of Resilient Power Systems for USD 86 million, adding advanced medium-voltage solid-state transformer intellectual property and strengthening its position in next-generation power conversion technologies through expanded engineering capabilities and product innovation. Source: mgrid.org

February 2026: Lotus Wireless Technologies India and AIT Austrian Institute of Technology advanced their partnership to industrialize medium-voltage solid-state transformers for megawatt EV charging, targeting megawatt-scale passenger and heavy-duty vehicle applications, accelerating commercialization through international technology collaboration. Source: machinist.in

February 2026: Exowatt selected DG Matrix's Interport solid-state transformer platform for gigawatt-scale solar-powered data center deployments, enabling gigawatt-scale behind-the-meter power architectures that reduce grid dependency and accelerate high-density AI infrastructure expansion. Source: datacenterdynamics.com

The report provides comprehensive assessment of the global Solid-state Transformer Market across technology evolution, deployment strategies, competitive positioning, and operational developments between 2026 and 2033. It evaluates five major product types, five core application areas, and five principal end-user groups while covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The analysis incorporates deployment trends, technology adoption patterns, manufacturing developments, and participation of leading equipment suppliers shaping industry competitiveness.

The study delivers strategic insights into power electronics, silicon carbide integration, digital grid technologies, intelligent substations, and medium-voltage DC networks. It evaluates segment performance through deployment concentration, adoption rates exceeding 50% in key utility modernization programs, and evolving investment priorities. The report supports expansion planning, product portfolio optimization, partnership strategies, competitive benchmarking, and long-term infrastructure decision-making by identifying emerging deployment opportunities, technology shifts, and operational priorities across established and developing electricity markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 235.11 Million |

Market Revenue in 2033 | USD 2587.68 Million |

CAGR (2026 - 2033) | 34.96% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Hitachi Energy, Siemens Energy, GE Vernova, Schneider Electric, Mitsubishi Electric, Eaton, ABB, Toshiba Energy Systems & Solutions, Fuji Electric, Hyosung Heavy Industries, CG Power and Industrial Solutions, Bharat Heavy Electricals Limited (BHEL), Alstom, SPX Technologies |

Customization & Pricing | Available on Request (10% Customization is Free) |