Reports

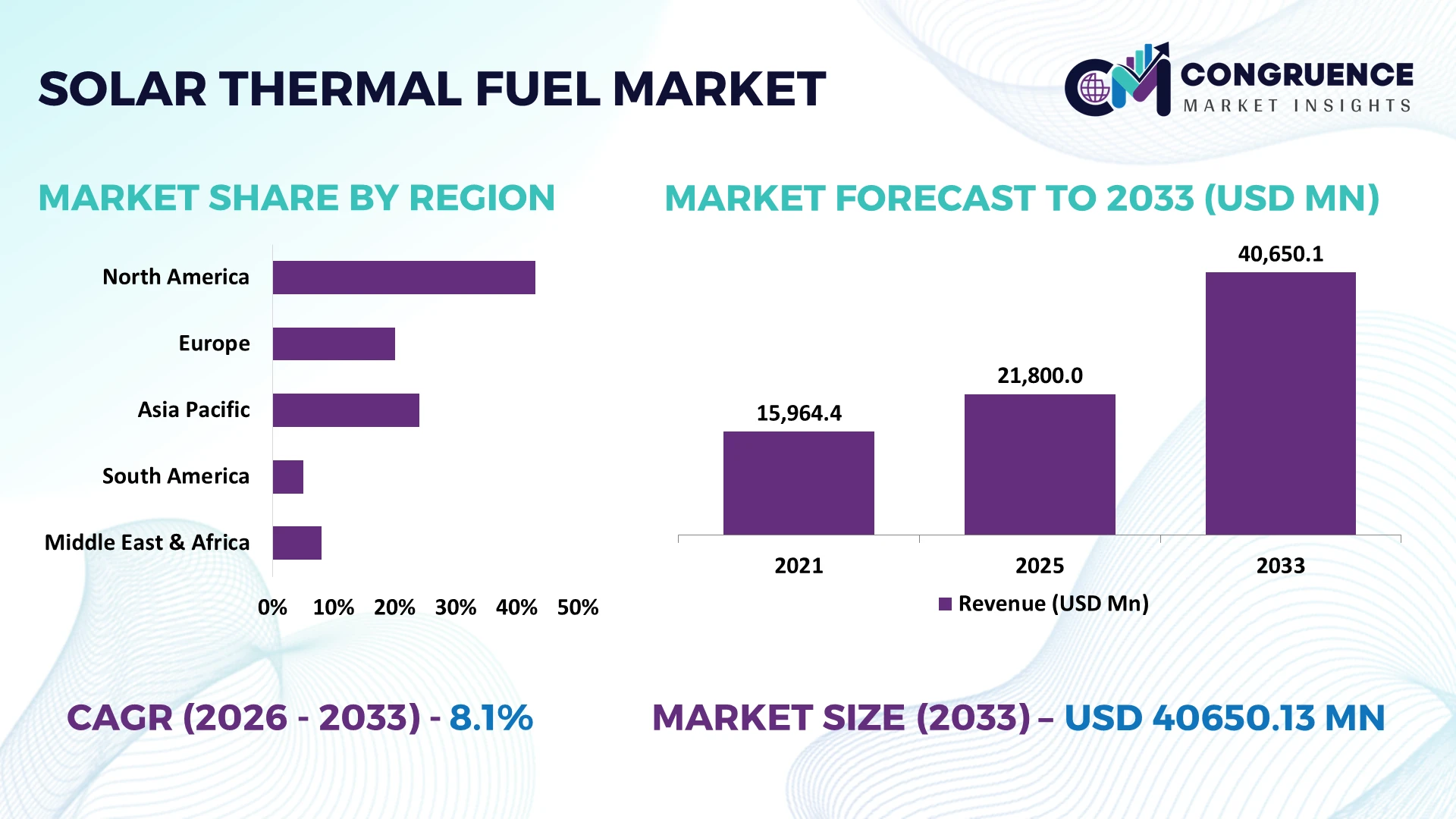

The Global Solar Thermal Fuel Market was valued at USD 21800 Million in 2025 and is anticipated to reach a value of USD 40650.13 Million by 2033 expanding at a CAGR of 8.1% between 2026 and 2033. Growth is being accelerated by breakthroughs in molecular solar thermal energy storage materials, industrial decarbonization initiatives, and increased deployment of long-duration renewable heat storage technologies.

Germany remains a leading innovation hub, accounting for approximately 24% of advanced solar thermal fuel research activity, supported by strong industrial decarbonization programs and chemical manufacturing investments. China continues expanding commercialization through large-scale clean energy manufacturing, with renewable energy installations exceeding 60% of new power capacity additions in 2026, creating stronger deployment momentum than European markets amid accelerating energy security strategies following the global energy transition reshaped by geopolitical supply disruptions.

This competitive landscape reinforces the importance of prioritizing technology partnerships, scalable manufacturing, and regional commercialization strategies to secure long-term market positioning.

Market Size & Growth: USD 21,800 Million in 2025 is projected to reach USD 40,650.13 Million by 2033 at an 8.1% CAGR, driven by advanced molecular energy-storage materials and industrial decarbonization initiatives.

Top Growth Drivers: Industrial clean-heat adoption (+32%), R&D investment (+21%), and renewable energy integration (+18%) continue strengthening global market expansion.

Short-Term Forecast: By 2028, thermal energy storage efficiency improves by nearly 16% while system operating costs decline by approximately 12%.

Emerging Technologies: AI-assisted material discovery, automated molecular synthesis, and advanced photochromic materials accelerate commercialization and performance optimization.

Regional Leaders: Europe approaches USD 13.2 Billion, Asia-Pacific USD 14.8 Billion, and North America USD 8.6 Billion, supported by industrial electrification and regional manufacturing expansion.

Consumer/End-User Trends: More than 41% of industrial renewable heat projects increasingly evaluate long-duration solar thermal fuel technologies for continuous operations.

Pilot/Case Example: A 2026 demonstration project achieved approximately 27% higher thermal storage efficiency through next-generation molecular switching materials.

Competitive Landscape: Leading participants collectively control nearly 38% of technology development, with competition driven by research alliances, specialty chemical firms, energy technology developers, and advanced materials innovators.

Regulatory & ESG Impact: Clean-energy regulations reduce lifecycle carbon emissions by roughly 30%, encouraging wider deployment across industrial facilities and strategic infrastructure.

Investment & Funding: More than USD 2.9 Billion in public-private funding supports pilot plants, commercialization partnerships, and regional manufacturing capacity amid supply-chain diversification.

Innovation & Future Outlook: High-performance molecular storage systems, scalable manufacturing, and integrated renewable heat solutions position the market for accelerated industrial adoption and global technology expansion.

Solar Thermal Fuel Market demand is increasingly concentrated in industrial process heating, sustainable chemical manufacturing, and long-duration renewable energy storage. Material engineering innovations have improved energy retention performance by nearly 20%, while manufacturers continue localizing advanced component production in response to evolving supply-chain resilience initiatives and clean-energy regulations. These developments establish a stronger foundation for the strategic market assessment that follows.

Solar Thermal Fuel Market development is becoming strategically important as industries seek dispatchable renewable heat solutions that reduce dependence on fossil fuels while strengthening energy security. Infrastructure modernization and supply-chain restructuring following recent global energy disruptions have accelerated investment in advanced thermal storage materials. Heavy industries, including specialty chemicals, steel, and advanced manufacturing, increasingly view molecular solar thermal fuel technologies as a competitive asset for lowering operational emissions without compromising production continuity, creating stronger differentiation through resilient energy management.

Compared with conventional molten-salt thermal storage, advanced molecular solar thermal fuel systems demonstrate up to 20% higher energy retention over extended storage periods while reducing thermal losses during repeated charge-discharge cycles. Germany continues leading high-value research and industrial validation, whereas China is scaling pilot manufacturing through integrated clean-energy industrial parks, enabling faster commercialization. During the next two to three years, industrial demonstration projects are expected to increase by nearly 25%, supported by digital monitoring platforms that improve storage optimization and predictive system performance.

A growing number of technology developers are partnering with specialty chemical manufacturers to establish localized production capacity and accelerate commercialization. One recent deployment integrated solar thermal fuel storage into an industrial heat network, reducing conventional fuel consumption by approximately 18% during peak operating periods. Companies expanding collaborative innovation ecosystems, manufacturing capability, and advanced materials expertise will strengthen competitive positioning while creating durable operational advantages in the evolving clean-energy landscape.

Industrial decarbonization policies and long-duration renewable heat requirements are accelerating adoption of solar thermal fuel technologies across energy-intensive sectors. More than 42% of industrial energy consumption remains heat-related, encouraging investment in advanced thermal storage systems capable of delivering stable process heat. Material performance improvements of nearly 18% have enhanced storage durability and operational flexibility. Germany continues expanding industrial demonstration facilities, while Japan is increasing research partnerships between universities and specialty chemical companies. These developments improve commercialization readiness, prompting technology providers to expand pilot manufacturing, establish strategic licensing agreements, and strengthen collaborations with industrial end users to secure first-mover advantages in high-value clean manufacturing applications.

Commercial deployment remains constrained by the high production cost of advanced photoresponsive molecules and limited large-scale manufacturing infrastructure. Specialty material costs remain approximately 25% above conventional thermal storage materials, while pilot-scale production accounts for less than 15% of projected industrial demand. Dependence on specialized chemical intermediates creates procurement complexity, particularly for European manufacturers managing evolving supply-chain diversification strategies. To improve scalability and protect operating margins, companies are localizing component sourcing, negotiating long-term raw material agreements, and investing in process optimization that lowers manufacturing intensity while improving production consistency across commercial facilities.

Artificial intelligence-driven molecular design is opening new commercial pathways by accelerating material discovery and reducing laboratory development cycles by nearly 35%. Automated testing platforms improve candidate screening efficiency by approximately 30%, enabling faster validation for industrial applications. South Korea is strengthening advanced materials innovation through coordinated research clusters linking chemical producers with clean-energy technology developers. Companies are responding through expanded R&D investments, intellectual property partnerships, and pilot-scale manufacturing ecosystems that shorten commercialization timelines. A significant opportunity lies in integrating solar thermal fuel systems into industrial waste-heat recovery networks, creating additional operational value beyond renewable energy storage alone.

Transitioning from successful pilot projects to standardized industrial deployment remains a major execution challenge. Integration with existing process heating infrastructure often increases implementation complexity by nearly 22%, while engineering customization extends project delivery schedules by approximately 18%. The shortage of specialized thermal materials engineers and system integration expertise is particularly evident in emerging manufacturing markets. Companies must also ensure long-term performance validation across diverse industrial operating conditions before widespread adoption. Leading technology developers are addressing these challenges through standardized system architectures, workforce training programs, engineering partnerships, and modular deployment strategies that simplify installation while improving operational reliability and long-term competitiveness.

Advanced Molecular Material Scale-Up Advanced molecular storage compounds are moving from laboratory validation to pilot manufacturing, with material stability improving by nearly 22% and thermal retention increasing by about 18%. Germany and Japan are expanding industrial collaboration to standardize production, while specialty chemical companies are forming joint development partnerships to shorten qualification timelines and improve commercial readiness for high-temperature industrial applications.

Localized Manufacturing Expansion Supply-chain diversification is reshaping production strategies as more than 35% of technology developers increase regional sourcing to reduce dependence on imported specialty chemicals. Geopolitical trade adjustments and raw material security concerns are driving localized manufacturing investments, allowing companies to lower procurement risks, improve production continuity, and accelerate customer delivery through vertically integrated manufacturing networks.

Digital Performance Optimization AI-enabled material screening and digital monitoring platforms are reducing development cycles by approximately 30% while improving operating efficiency by nearly 16%. Companies increasingly integrate predictive analytics into thermal storage management, enabling continuous performance optimization, reduced maintenance intervals, and faster deployment decisions. This digital transition is strengthening commercial confidence and supporting broader industrial implementation across energy-intensive sectors.

Industrial Heat Integration Accelerates Industrial heat applications are becoming a primary commercialization pathway, with renewable process-heat projects increasing by nearly 24% across chemical and advanced manufacturing facilities. Companies are restructuring deployment strategies by combining solar thermal fuel technologies with existing heat infrastructure rather than replacing entire systems, reducing implementation complexity while improving energy resilience and operational flexibility.

Molecular Solar Thermal Fuels represent the leading segment with an estimated 38% market share, supported by superior long-duration energy storage capability, reversible molecular switching, and compatibility with advanced industrial heat systems. Their scalability and high energy retention make them the preferred choice for commercial demonstrations and specialty manufacturing projects. Thermochemical Fuels continue serving high-temperature industrial processes, while Phase Change Materials remain valuable for established thermal storage applications requiring lower implementation complexity. Organic Solar Thermal Fuels maintain strategic importance for research-driven applications emphasizing sustainable material development.

Hybrid Solar Thermal Fuels are the fastest-growing segment as enterprises combine multiple storage mechanisms to improve operational flexibility and system efficiency. Adoption has increased by approximately 26% in new pilot projects, while collaborative product development has expanded by nearly 20%. Technology providers are strengthening partnerships with specialty chemical manufacturers, increasing pilot-scale production, and prioritizing integrated product portfolios to address industrial performance requirements. These investment patterns indicate a gradual transition from single-technology solutions toward multifunctional thermal energy storage platforms.

Industrial Heat remains the dominant application, accounting for approximately 41% of market demand because energy-intensive industries require continuous renewable heat solutions for chemicals, metals, and advanced manufacturing. Energy Storage follows closely as organizations prioritize long-duration thermal storage to stabilize renewable energy utilization. Building Heating continues expanding through energy-efficient infrastructure upgrades, while Power Generation maintains strategic relevance where integrated renewable systems support grid flexibility. Transportation remains an emerging application focused on future thermal energy management technologies.

Energy Storage is the fastest-growing application, with deployment activity increasing by nearly 28% as industries seek resilient alternatives for balancing intermittent renewable energy. Integration efficiency has improved by around 17% through digital monitoring and advanced thermal management technologies. Companies are expanding deployment partnerships, integrating intelligent control platforms, and developing modular systems tailored to industrial operations. Demand is increasingly shifting toward applications delivering both operational continuity and measurable decarbonization outcomes, reinforcing the strategic importance of integrated thermal energy ecosystems.

Energy & Utilities represent the largest end-user segment with an estimated 43% share, supported by extensive renewable infrastructure investments and increasing deployment of long-duration thermal storage assets. Large-scale utility projects require reliable heat storage technologies that complement renewable electricity generation while strengthening grid resilience. Industrial Manufacturing is expanding rapidly through process decarbonization initiatives, whereas Construction increasingly integrates advanced thermal storage into sustainable building designs. Automotive companies continue evaluating thermal management applications, while Research Institutions remain essential for technology validation and next-generation material development.

Industrial Manufacturing is the fastest-growing end-user category, with adoption expanding by approximately 29% as manufacturers modernize production facilities and improve energy efficiency. Collaborative development agreements have increased by nearly 18%, reflecting stronger cooperation between technology developers and industrial operators. Companies are introducing customized thermal storage solutions, expanding engineering partnerships, and strengthening application-specific product portfolios. Competitive positioning increasingly depends on delivering industry-tailored performance, faster deployment, and integrated technical support rather than standardized technology offerings.

North America accounted for the largest market share at 35% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 9.4% CAGR between 2026 and 2033.

Advanced Industrial Decarbonization Accelerates Commercial Deployment

North America represents the most established Solar Thermal Fuel Market, supported by advanced research capabilities, industrial decarbonization programs, and strong public-private collaboration. The region contributes approximately 35% of global deployment activity, with specialty chemicals, renewable energy, and industrial manufacturing leading commercial adoption. Pilot-scale manufacturing capacity continues expanding as enterprises prioritize long-duration thermal storage technologies for process heat applications. More than 30% of newly announced industrial clean-energy demonstration projects now evaluate advanced thermal storage integration. Technology developers are strengthening partnerships with material science companies and engineering firms to accelerate commercialization while expanding domestic manufacturing capabilities that improve supply-chain resilience and deployment consistency.

United States Market Outlook: The United States remains the regional innovation leader through strong university research, national laboratory programs, and industrial pilot deployments. Advanced manufacturing initiatives continue supporting commercialization of molecular thermal storage materials, while collaboration between specialty chemical companies and energy technology developers has increased by nearly 22%. Large industrial facilities are integrating renewable thermal storage into decarbonization roadmaps, encouraging companies to expand demonstration projects, strengthen intellectual property portfolios, and establish domestic production networks that improve long-term competitiveness.

Research Leadership Supports Industrial Commercialization

Europe maintains a strong competitive position through advanced materials research, industrial sustainability targets, and coordinated clean-energy policy frameworks. The region accounts for nearly 31% of global market activity, with industrial heat decarbonization driving sustained deployment across chemical processing and manufacturing sectors. Cross-border technology partnerships continue expanding commercialization pathways, while demonstration projects increasingly integrate advanced molecular thermal storage into renewable energy infrastructure. Industrial collaboration has increased by approximately 24% over recent years, strengthening technology validation and accelerating transition from laboratory innovation to commercial implementation. Companies continue investing in localized production, advanced material development, and engineering partnerships that enhance operational reliability.

Germany Market Outlook: Germany leads European commercialization through its advanced chemical industry, engineering expertise, and strong industrial innovation ecosystem. Manufacturing companies increasingly integrate renewable thermal technologies into production operations, while research collaboration between industrial enterprises and academic institutions continues expanding. Approximately 26% of regional advanced thermal storage pilot activities are concentrated in Germany, supporting faster technology qualification, localized manufacturing capability, and stronger export potential for next-generation thermal storage solutions.

Manufacturing Scale Drives Rapid Adoption

Asia-Pacific is emerging as the fastest-expanding regional market through large-scale manufacturing capacity, accelerating renewable infrastructure investment, and expanding industrial energy demand. The region represents approximately 27% of global market activity while steadily increasing production capability for advanced thermal materials. Industrial clean-energy projects have expanded by nearly 28%, supported by integrated manufacturing ecosystems and government-backed technology programs. Companies are strengthening regional supply chains, expanding pilot production facilities, and forming strategic partnerships that improve commercialization speed while reducing production costs through manufacturing scale and process optimization.

China Market Outlook: China remains the regional manufacturing powerhouse through extensive renewable energy deployment, specialty material production, and integrated industrial supply chains. Domestic enterprises continue expanding advanced thermal material manufacturing while increasing investment in pilot-scale commercialization. More than one-third of new regional clean-energy manufacturing projects incorporate advanced thermal storage research, enabling companies to accelerate product development, improve production efficiency, and strengthen export competitiveness across emerging clean-energy markets.

Renewable Infrastructure Expands Industrial Demand

South America is strengthening its position through renewable energy diversification, increasing industrial electrification, and gradual investment in advanced energy storage technologies. The region contributes approximately 4% of global market activity, with mining, industrial processing, and utility-scale renewable projects creating demand for long-duration thermal storage solutions. Renewable infrastructure investment has increased by nearly 19%, although commercialization remains constrained by limited advanced manufacturing capacity and technology localization. Companies are responding through regional partnerships, engineering collaboration, and phased deployment strategies that align with existing renewable infrastructure while minimizing operational risk.

Brazil Market Outlook: Brazil leads regional development through its diversified renewable energy portfolio and expanding industrial manufacturing base. Industrial operators are increasingly evaluating renewable thermal storage technologies to improve energy flexibility within mining and process industries. Utility modernization programs and industrial partnerships continue supporting pilot deployment activity, while domestic engineering capability strengthens commercialization opportunities for advanced thermal energy systems across strategic industrial sectors.

Energy Diversification Strengthens Investment Momentum

The Middle East & Africa market is evolving through energy diversification strategies, industrial modernization, and increasing investment in renewable infrastructure. The region represents approximately 3% of global market activity but is steadily expanding demonstration projects supporting long-duration thermal storage technologies. Utility operators and industrial enterprises are integrating renewable heat solutions into broader energy transition programs, while infrastructure investments have increased by nearly 21% across strategic clean-energy initiatives. Companies continue establishing regional partnerships and evaluating localized manufacturing opportunities to improve deployment efficiency while supporting national sustainability priorities.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's leading market through large-scale energy transition initiatives, industrial diversification, and investment in advanced clean-energy technologies. Industrial development zones increasingly evaluate renewable thermal storage to complement expanding renewable power capacity. National infrastructure programs and collaboration with international technology developers are accelerating pilot implementation, while localized industrial investment supports future manufacturing capability and strengthens the country's position as a regional clean-energy innovation hub.

Competition in the Solar Thermal Fuel Market is led by Kyoto Group, Azelio, Brenmiller Energy, Siemens Energy, and BASF, while university spin-offs, specialty material developers, and regional thermal-storage innovators compete through niche technologies. Global technology leaders challenge emerging material innovators on commercialization speed, whereas engineering firms compete with component suppliers on integrated system delivery. The top five participants collectively account for approximately 48% of market activity, reflecting a technology-driven competitive structure. Performance leadership depends on molecular stability, energy retention, and manufacturing scalability rather than pricing alone. Advanced storage materials improve thermal efficiency by nearly 20%, while automated material development reduces validation cycles by around 30%, creating faster commercialization advantages. Companies are expanding pilot manufacturing, forming chemical-industry partnerships, and vertically integrating material development with system engineering. Competition is shifting toward proprietary molecular formulations and secure specialty-material supply chains, increasing intellectual property and production barriers. Winning requires scalable manufacturing, differentiated thermal performance, strategic industrial partnerships, and rapid deployment capability across commercial energy applications.

BASF

Siemens Energy

Brenmiller Energy

Kyoto Group

Azelio

Aalborg CSP

Rondo Energy

Antora Energy

EnergyNest

Synhelion

Heliogen

Malta Inc.

CEA

Empa

Advanced molecular solar thermal storage materials are becoming the defining technology for commercial deployment, enabling energy storage over extended periods with approximately 20% higher thermal retention than conventional molten-salt systems. AI-assisted molecular discovery shortens material screening cycles by nearly 35%, accelerating commercialization and reducing laboratory development costs. Around 40% of new pilot projects now integrate digital simulation platforms before physical testing, improving design accuracy and reducing engineering iterations. Technology developers with advanced material science capabilities are securing stronger industrial partnerships and competitive licensing opportunities.

Emerging innovation is centered on hybrid solar thermal fuels, automated manufacturing, and digital monitoring platforms. Compared with legacy thermal storage technologies, hybrid molecular systems improve operational flexibility by approximately 18% while lowering thermal degradation during repeated operating cycles. Intelligent monitoring platforms have been adopted in nearly 32% of advanced demonstration projects, enabling predictive maintenance and performance optimization. Engineering firms and specialty chemical manufacturers benefit most because integrated solutions simplify industrial deployment and strengthen long-term operating reliability.

Between 2026 and 2028, commercialization will increasingly depend on modular production methods, high-throughput material synthesis, and integrated industrial heat networks. Automated manufacturing is expected to reduce production complexity by roughly 15%, while standardized system architectures accelerate project deployment across industrial facilities. Companies investing early in scalable molecular technologies, digital engineering platforms, and strategic manufacturing partnerships will establish stronger intellectual property positions, faster commercialization pathways, and sustainable competitive advantages in advanced renewable thermal energy markets.

June 2024 Synhelion inaugurated the DAWN solar fuel plant in Jülich, Germany, the world's first industrial-scale facility for producing solar fuels using concentrated solar heat. The plant features a 20-meter solar tower, marking a major commercialization milestone and accelerating industrial deployment.

June 2025 Synhelion and INERATEC signed a Memorandum of Understanding to integrate solar syngas production with synthetic fuel manufacturing. The collaboration combines industrial-scale thermochemical technology with commercial e-fuel production, strengthening Europe's renewable fuel value chain. Source: https://ineratec.de/en/news/

July 2025 SWISS International Air Lines became the first airline to use Synhelion's solar-produced fuel in regular flight operations, validating compatibility with existing aviation infrastructure and advancing commercial adoption of sustainable aviation fuels. Source: https://www.swiss.com/

The Solar Thermal Fuel Market report provides comprehensive analysis across Molecular Solar Thermal Fuels, Phase Change Materials, Thermochemical Fuels, Hybrid Solar Thermal Fuels, and Organic Solar Thermal Fuels, covering Energy Storage, Building Heating, Industrial Heat, Power Generation, and Transportation applications. It evaluates demand across Energy & Utilities, Industrial Manufacturing, Construction, Automotive, and Research Institutions while assessing competitive dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Industrial heat applications account for a significant share of deployment activity, while hybrid technologies continue expanding across pilot-scale projects.

The report delivers strategic intelligence on technology innovation, manufacturing trends, supply-chain evolution, commercialization pathways, competitive positioning, and investment priorities between 2026 and 2033. It examines enterprise partnerships, deployment patterns, technology readiness, and regional adoption differences while profiling major market participants. The analysis supports expansion planning, product development, competitive benchmarking, investment evaluation, and long-term business strategy through detailed segmentation and operational market assessment.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 21800 Million |

Market Revenue in 2033 | USD 40650.13 Million |

CAGR (2026 - 2033) | 8.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | BASF, Siemens Energy, Brenmiller Energy, Kyoto Group, Azelio, Aalborg CSP, Rondo Energy, Antora Energy, EnergyNest, Synhelion, Heliogen, Malta Inc., CEA, Empa |

Customization & Pricing | Available on Request (10% Customization is Free) |