Reports

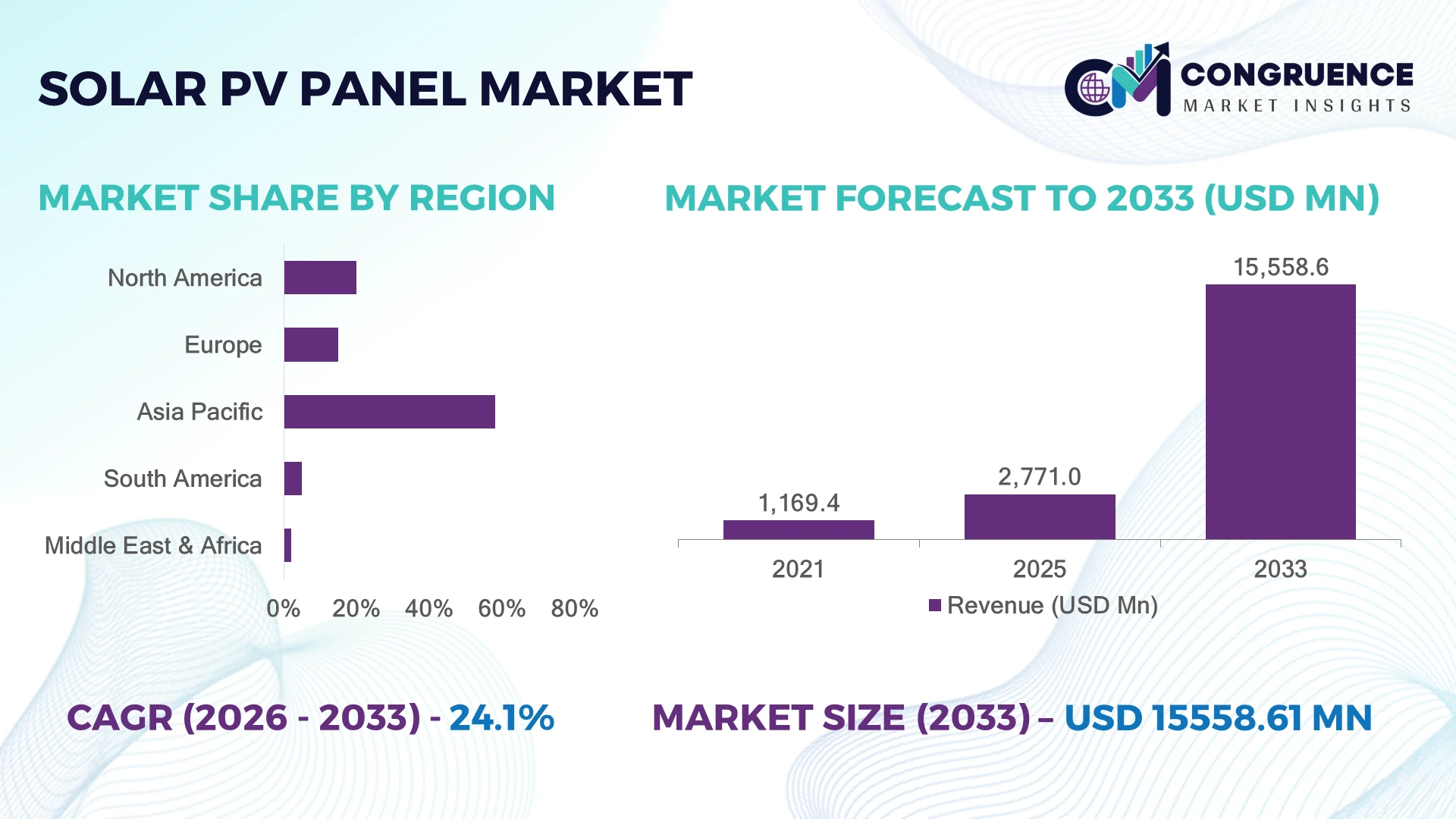

The Global Solar PV Panel Market was valued at USD 2,771.0 Million in 2025 and is anticipated to reach a value of USD 15,558.6 Million by 2033 expanding at a CAGR of 24.07% between 2026 and 2033. Growth is driven by rapid deployment of high-efficiency TOPCon and heterojunction solar modules, large-scale utility solar projects, and falling module manufacturing costs supported by expanded photovoltaic supply chains.

China dominated global solar PV panel deployment with over 60% of worldwide solar module manufacturing capacity and more than 500 GW cumulative installed solar capacity by 2025, supported by industrial-scale production and renewable energy investments. The United States followed with over 200 GW installed solar capacity, accelerated by Inflation Reduction Act incentives and domestic manufacturing expansion. China’s module output scale remains significantly higher than the U.S., while India’s solar capacity exceeded 100 GW, strengthening its role as a major emerging manufacturing and adoption hub.

Strategic investments in advanced manufacturing, storage integration, and localized supply chains will define competitive advantage in the evolving solar PV panel market.

Market Size & Growth: USD 2.77 Billion (2025) to USD 15.56 Billion (2033) at 24.07% CAGR, driven by advanced module efficiency and utility-scale solar expansion.

Top Growth Drivers: Renewable energy targets (35%+ global power capacity additions), falling solar module costs (70%+ decline since 2010), and grid decarbonization initiatives.

Short-Term Forecast: By 2028, next-generation modules are projected to deliver 5–10% higher efficiency with improved energy yield.

Emerging Technologies: AI-based solar monitoring, automated manufacturing, TOPCon cells, heterojunction technology, and recyclable PV materials are reshaping deployments.

Regional Leaders: Asia Pacific projected above USD 900 Million, North America above USD 300 Million, and Europe above USD 250 Million by 2033, supported by renewable adoption programs.

Consumer/End-User Trends: Commercial and industrial users account for over 40% of new solar installations as businesses prioritize energy cost control.

Pilot/Case Example: China’s large-scale solar projects in 2024 achieved over 20% operational efficiency gains through smart tracking and digital monitoring systems.

Competitive Landscape: Chinese manufacturers hold over 70% of global module production capacity, with leading players including LONGi, JinkoSolar, Trina Solar, JA Solar, and Canadian Solar.

Regulatory & ESG Impact: Global clean energy policies are accelerating solar adoption, with renewable targets driving more than 30% growth in annual solar installations.

Investment & Funding: Over USD 300 Billion was invested globally in solar energy in 2024, focusing on manufacturing expansion, storage integration, and supply-chain localization.

Innovation & Future Outlook: Advanced PV materials, perovskite tandem cells, and integrated solar-plus-storage solutions are shifting the market toward higher efficiency and energy independence.

The Solar PV Panel Market is expanding beyond traditional electricity generation into distributed energy systems, smart grids, and industrial decarbonization solutions. Demand is rising for bifacial modules, AI-enabled performance optimization, and lightweight photovoltaic technologies, with over 25% efficiency levels achieved by advanced commercial solar cells. Global supply-chain diversification following recent trade policies and manufacturing localization efforts is reshaping procurement strategies across major solar markets.

The Solar PV Panel Market is becoming strategically important as governments, utilities, and industries prioritize energy security, carbon reduction, and long-term electricity cost stability. The shift toward localized manufacturing, supported by policies such as the U.S. Inflation Reduction Act and European renewable energy initiatives, is restructuring global photovoltaic supply chains and encouraging regional production ecosystems.

Technology advancement is creating measurable advantages over legacy solar systems. Modern TOPCon and heterojunction modules achieve efficiency levels above 22%, compared with older crystalline silicon modules that typically operated around 18–20%, improving land utilization and project economics. Asia Pacific continues to lead through large-scale manufacturing and deployment, while North America emphasizes domestic production and grid modernization, creating a more diversified competitive landscape.

Over the next 2–3 years, solar developers are prioritizing digital monitoring, automated operations, and solar-plus-storage projects to improve reliability. Utility operators in China, India, and the United States are deploying large photovoltaic farms integrated with battery systems to stabilize renewable power supply. Companies are increasing investments in advanced cell technologies, regional factories, and strategic partnerships to secure supply advantages. Competitive success in the solar PV panel market will depend on manufacturing efficiency, technology leadership, and the ability to deliver reliable low-carbon energy solutions at scale.

The rapid adoption of high-efficiency photovoltaic technologies is strengthening solar PV panel deployment across utility, commercial, and industrial applications. Advanced TOPCon and heterojunction modules are achieving efficiency levels above 22%, improving project output by nearly 5–10% compared with conventional modules. China’s solar manufacturing ecosystem, supported by more than 70% global module production capacity, has accelerated cost optimization and supply availability. Companies are responding through gigawatt-scale factory expansions, automation investments, and technology partnerships to capture demand for higher-yield modules. The strategic shift toward domestic manufacturing in the United States and India is also reshaping procurement models and reducing dependence on concentrated supply chains.

Solar PV panel scalability faces pressure from concentrated manufacturing dependency, grid limitations, and raw material volatility. China controls over 80% of global solar wafer production, creating supply-chain exposure for international developers during trade disruptions and policy changes. Grid connection delays affect more than 20% of planned renewable projects in several emerging markets due to transmission infrastructure constraints. Companies are mitigating these risks through regional manufacturing facilities, long-term material contracts, and diversified supplier networks. The operational challenge is shifting from module availability to reliable integration, as utilities require stronger grid flexibility and storage compatibility before accelerating large-scale solar deployments.

Emerging photovoltaic technologies are creating new opportunities through higher efficiency, automation, and intelligent energy management. Perovskite tandem solar cells have demonstrated laboratory efficiencies above 30%, opening pathways for future commercial applications beyond traditional silicon modules. India’s solar manufacturing incentives and the expansion of domestic production capacity above 100 GW are creating new investment opportunities across the value chain. Companies are increasing R&D spending, forming technology partnerships, and integrating AI-based monitoring platforms to improve asset performance. A significant opportunity lies in combining solar panels with storage, smart grids, and industrial energy systems, enabling businesses to optimize renewable power usage rather than only generate electricity.

Long-term solar PV adoption faces execution challenges related to grid stability, project integration, and lifecycle management. Solar generation variability requires advanced balancing solutions, with renewable sources already representing more than 30% of electricity generation in several high-adoption markets. Large-scale projects in countries such as India and Australia require upgraded transmission networks and advanced forecasting systems to maintain reliability. Companies must invest in energy storage, predictive analytics, cybersecurity systems, and skilled technical teams to manage increasingly complex solar assets. The key operational challenge is transitioning from rapid installation growth to consistent energy delivery, requiring stronger ecosystem coordination among manufacturers, utilities, and technology providers.

Smart Solar Operations Rise: AI-driven monitoring, predictive maintenance, and automated inspection systems are transforming solar asset management, with digital tools improving operational efficiency by 15–25% and reducing maintenance downtime by nearly 20%. Utilities in China and India are deploying intelligent monitoring platforms across large solar parks, while manufacturers are partnering with software providers to optimize performance, extend panel life cycles, and improve asset reliability.

Domestic Manufacturing Expansion: Supply-chain restructuring is accelerating as countries reduce dependence on concentrated photovoltaic production. The United States is expanding domestic solar manufacturing under clean energy incentives, while India targets over 100 GW of annual module production capacity. Companies are increasing factory automation, local sourcing, and strategic partnerships to reduce logistics exposure, with localized supply chains improving procurement stability by 20–30%.

Advanced Module Adoption: Solar developers are shifting toward TOPCon, heterojunction, and bifacial technologies, with commercial module efficiencies exceeding 22% and bifacial systems delivering 5–15% additional energy yield depending on site conditions. Large-scale projects are prioritizing higher-output modules to reduce land requirements, encouraging manufacturers to accelerate research investments and upgrade production lines.

Solar Storage Integration: Hybrid solar-plus-storage projects are gaining traction as grid operators address renewable intermittency challenges. Battery-connected solar installations increased by more than 30% in major markets during recent deployment cycles, enabling improved power reliability and peak-load management. Companies are forming partnerships across storage, grid software, and energy management sectors to deliver integrated renewable solutions.

Crystalline silicon panels dominate the Solar PV Panel Market due to their established manufacturing ecosystem, cost efficiency, and widespread compatibility with utility-scale projects. Monocrystalline modules represent the leading type, supported by efficiency levels above 20–23% and strong adoption among commercial and utility developers seeking higher energy output per installation area. Polycrystalline panels continue serving price-sensitive markets but are gradually losing preference due to lower efficiency performance. Thin-film solar panels are emerging as the fastest-growing type segment, driven by lightweight designs, flexible applications, and suitability for specialized installations such as building-integrated photovoltaics. Companies are expanding thin-film production and investing in advanced materials to target new applications beyond conventional rooftop and ground-mounted systems. The shift toward high-efficiency technologies is influencing investment priorities, with manufacturers focusing on improved conversion rates, automated production, and next-generation photovoltaic materials.

Utility-scale solar installations represent the leading application segment due to large project capacity, government-backed renewable programs, and rising electricity decarbonization initiatives. Large solar farms account for more than 50% of newly installed photovoltaic capacity in several major markets, including China, India, and the United States. Developers are prioritizing high-capacity modules, digital monitoring systems, and integrated storage solutions to improve project economics and grid reliability. Commercial and industrial solar applications are the fastest-growing segment as businesses adopt renewable energy to reduce operating costs and meet sustainability targets. Corporate solar adoption has increased significantly, with enterprises increasingly using rooftop systems, power purchase agreements, and behind-the-meter solutions. Residential applications remain important through distributed energy adoption, while emerging uses such as agricultural photovoltaics and solar-integrated infrastructure are expanding market opportunities. Companies are adapting through customized financing models, installer partnerships, and scalable deployment platforms.

Utility companies remain the dominant end-user group due to their large-scale procurement capacity, grid responsibilities, and investment in renewable infrastructure. Utilities account for the majority of solar project capacity additions globally, driven by national clean energy targets and increasing electricity demand. Companies in this segment are investing in solar-plus-storage projects, grid modernization, and advanced forecasting systems to manage renewable variability. Commercial and industrial users represent the fastest-growing end-user segment as manufacturers, data centers, and large enterprises seek energy independence and carbon reduction solutions. Industrial buyers are increasingly adopting solar systems integrated with smart energy platforms, with corporate renewable procurement strategies expanding across major economies. Residential users continue adopting rooftop solar through incentives and financing models, while government institutions are accelerating solar deployment for public infrastructure. Solar providers are responding through segment-specific solutions, financing partnerships, and integrated energy management offerings.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 25.3% between 2026 and 2033.

North America is strengthening its solar PV panel position through domestic manufacturing investments, utility-scale projects, and distributed energy adoption. The region contributed nearly 20% of global solar installations in 2025, supported by the United States’ expanding photovoltaic manufacturing base and large-scale clean energy programs. Solar module production capacity in the U.S. has increased significantly, with new factories targeting advanced cells and localized supply chains. Utility operators are integrating solar with battery storage and smart grid technologies to improve reliability. Companies are responding through manufacturing partnerships, automated production facilities, and long-term supply agreements to reduce import dependency and improve project execution.

United States Market Outlook: The United States remains the key North American solar market due to strong utility-scale deployment, domestic manufacturing incentives, and technology investments. The country surpassed 200 GW of installed solar capacity, supported by rising demand from utilities, data centers, and industrial users. Manufacturers are expanding production facilities for advanced modules, while developers are increasing solar-plus-storage projects to improve grid stability and energy resilience.

Europe is accelerating solar PV adoption as governments prioritize energy security, renewable integration, and reduced dependence on imported energy sources. The region accounted for approximately 15% of global solar installations in 2025, with Germany, Spain, and Italy leading deployment activity. Regulatory initiatives supporting rooftop solar, commercial installations, and renewable power integration are reshaping market demand. Europe’s solar industry is also focusing on recycling, sustainable manufacturing, and regional supply-chain development. Companies are investing in automated module production, energy management platforms, and partnerships to strengthen competitiveness. The increasing integration of solar with storage and smart grid infrastructure is improving operational flexibility across industrial and commercial applications.

Germany Market Outlook: Germany remains Europe’s leading solar market due to strong policy support, industrial demand, and advanced distributed energy infrastructure. The country exceeded 100 GW of installed solar capacity, driven by residential rooftops, commercial projects, and utility-scale developments. German companies are focusing on energy storage integration, digital monitoring systems, and sustainable photovoltaic manufacturing to enhance long-term competitiveness.

Asia-Pacific dominates the global Solar PV Panel Market due to its manufacturing scale, supply-chain integration, and extensive solar deployment activity. The region contributed nearly 60% of global solar capacity additions in 2025, led by China, India, and Japan. China controls more than 70% of global solar module manufacturing capacity, creating significant advantages in production efficiency, technology development, and export capability. India is rapidly expanding domestic manufacturing through renewable energy initiatives, while Southeast Asian countries are increasing solar investments. Companies are scaling automated factories, improving cell technologies, and developing international supply partnerships to maintain competitiveness across global markets.

China Market Outlook: China remains the global solar manufacturing powerhouse with more than 500 GW of installed solar capacity and the world’s largest photovoltaic production ecosystem. The country’s manufacturers are leading advancements in TOPCon, heterojunction, and large-format modules while expanding overseas partnerships. Continued investment in renewable infrastructure and energy storage is strengthening China’s position across the global solar value chain.

South America is emerging as a high-potential solar PV market supported by strong solar resources, industrial electricity demand, and renewable energy diversification strategies. The region contributed around 5% of global solar capacity additions in 2025, with Brazil, Chile, and Argentina driving project activity. Utility-scale solar farms are expanding in mining, manufacturing, and energy-intensive industries seeking reliable renewable power sources. However, transmission limitations and permitting complexity continue affecting project timelines. Companies are addressing these barriers through infrastructure partnerships, hybrid renewable projects, and localized development strategies. Solar adoption is increasingly linked with industrial competitiveness, especially in regions with strong mining and manufacturing operations.

Brazil Market Outlook: Brazil represents the largest solar market in South America, supported by distributed generation growth and utility-scale solar investments. The country surpassed 50 GW of installed solar capacity, driven by residential, commercial, and industrial adoption. Developers are expanding solar projects alongside grid upgrades and financing solutions to improve renewable energy accessibility.

The Middle East & Africa solar PV panel market is advancing through utility-scale projects, energy diversification programs, and infrastructure modernization initiatives. The region accounted for approximately 2% of global solar additions in 2025, with Saudi Arabia, the United Arab Emirates, Egypt, and South Africa leading investment activity. Abundant solar resources and government-backed renewable strategies are supporting large photovoltaic developments, including solar parks connected with industrial and desalination facilities. Companies are increasing investments in large-scale engineering partnerships, regional manufacturing capabilities, and hybrid solar-storage solutions. The market is shifting from standalone solar generation toward integrated energy systems supporting industrial growth and energy security.

Saudi Arabia Market Outlook: Saudi Arabia is becoming a major solar investment hub through large-scale renewable projects under its energy diversification strategy. The country is developing multi-gigawatt solar facilities and targeting significant renewable capacity expansion. Utility developers and international technology providers are collaborating on solar infrastructure, storage integration, and advanced grid management solutions to support industrial transformation.

The Solar PV Panel Market features intense competition between global module manufacturers, vertically integrated solar companies, and regional technology providers. Leading players such as LONGi, JinkoSolar, Trina Solar, and JA Solar compete with global suppliers including Canadian Solar and First Solar through manufacturing scale, module efficiency, and supply-chain control. The top five companies collectively account for approximately 40–45% of global module shipments, reflecting a moderately consolidated structure. Competition is centered on technology advancement, pricing efficiency, production capacity, and product reliability, with high-efficiency modules improving conversion performance by 5–10% over conventional designs. Chinese manufacturers leverage cost leadership and integrated production, while companies such as First Solar differentiate through thin-film technology and localized manufacturing. Players are expanding gigawatt-scale factories, forming strategic partnerships, and investing in TOPCon, heterojunction, and recyclable module technologies. High capital requirements, supply-chain access, and technological expertise remain key entry barriers. Winning requires scale, innovation, resilient sourcing, and consistent delivery performance.

JinkoSolar Holding Co., Ltd.

Trina Solar Co., Ltd.

JA Solar Technology Co., Ltd.

Canadian Solar Inc.

First Solar, Inc.

Hanwha Q CELLS Corporation

Risen Energy Co., Ltd.

Astronergy Solar (Chint New Energy Technology)

Talesun Solar Technologies Co., Ltd.

SunPower Corporation

REC Group

Meyer Burger Technology AG

Solar PV technology is transitioning from conventional crystalline silicon modules toward high-efficiency TOPCon, heterojunction, and tandem photovoltaic solutions. TOPCon modules have achieved commercial efficiencies above 22%, improving energy yield by nearly 5–10% compared with older PERC technologies. Manufacturers including LONGi, JinkoSolar, and Trina Solar are scaling advanced cell production to improve output, reduce degradation, and strengthen competitiveness in utility-scale projects.

Digital integration is becoming a major operational differentiator, with AI-powered monitoring, predictive maintenance, and automated inspection platforms improving solar asset performance by 15–25%. Large solar operators are adopting intelligent energy management systems to optimize generation forecasting, reduce downtime, and integrate storage solutions. These technologies are particularly valuable for utility-scale installations where operational efficiency directly impacts profitability.

Disruptive technologies such as perovskite tandem cells, bifacial modules, and solar-plus-storage systems are shaping the 2026–2028 market outlook. Perovskite tandem research has demonstrated efficiency levels exceeding 30%, compared with traditional commercial silicon modules around 22–24%. Global technology leaders and specialized innovators are competing to commercialize these solutions, while vertically integrated manufacturers benefit from faster production scaling and supply-chain advantages. Companies acting now through R&D investment, automation, and strategic partnerships are positioned to capture next-generation solar demand.

April 2025 — LONGi Green Energy Technology launched the upgraded Hi-MO 9 module powered by HPBC 2.0 technology, achieving 24.8% conversion efficiency and 670W output. The innovation strengthens high-efficiency utility solar deployment by improving energy yield and reducing land-use requirements for large photovoltaic projects. Source: www.longi.com

January 2025 — JinkoSolar announced a breakthrough in N-type TOPCon-based perovskite tandem solar cell technology, achieving 33.84% conversion efficiency through independently tested laboratory results. The advancement supports next-generation photovoltaic development and strengthens JinkoSolar’s position in high-efficiency solar technology innovation. Source: www.ir.jinkosolar.com

June 2025 — LONGi Green Energy Technology introduced its HIBC technology and True 700W module at SNEC 2025, delivering over 700W power output and nearly 26% module efficiency. The launch accelerates the transition toward ultra-high-power photovoltaic modules for large-scale solar installations. Source: www.longi.com

August 2025 — JinkoSolar reported first-half 2025 business achievements, including 41.8 GW module shipments and cumulative global deliveries exceeding 350 GW. The milestone demonstrates manufacturing scale, international market penetration, and continued expansion of high-efficiency TOPCon module production capabilities.

The Solar PV Panel Market Report provides comprehensive coverage of market segmentation across type, application, and end-user categories, including monocrystalline, polycrystalline, thin-film technologies, utility-scale solar, commercial installations, residential systems, and industrial applications. The report evaluates deployment patterns, manufacturing trends, technology adoption, and competitive positioning across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The study analyzes advanced photovoltaic technologies, including TOPCon, heterojunction, bifacial modules, and solar-plus-storage integration, while assessing emerging opportunities in distributed energy, smart grids, and industrial decarbonization. With analysis of major manufacturers, supply-chain strategies, regional expansion initiatives, and innovation trends, the report supports investment decisions, market entry strategies, competitive benchmarking, and long-term business planning through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,771.0 Million |

| Market Revenue (2033) | USD 15,558.6 Million |

| CAGR (2026–2033) | 24.07% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | LONGi Green Energy Technology Co., Ltd.; JinkoSolar Holding Co., Ltd.; Trina Solar Co., Ltd.; JA Solar Technology Co., Ltd.; Canadian Solar Inc.; First Solar, Inc.; Hanwha Q CELLS Corporation; Risen Energy Co., Ltd.; Astronergy Solar; Talesun Solar Technologies Co., Ltd.; SunPower Corporation; REC Group; Meyer Burger Technology AG |

| Customization & Pricing | Available on Request (10% Customization Free) |