Reports

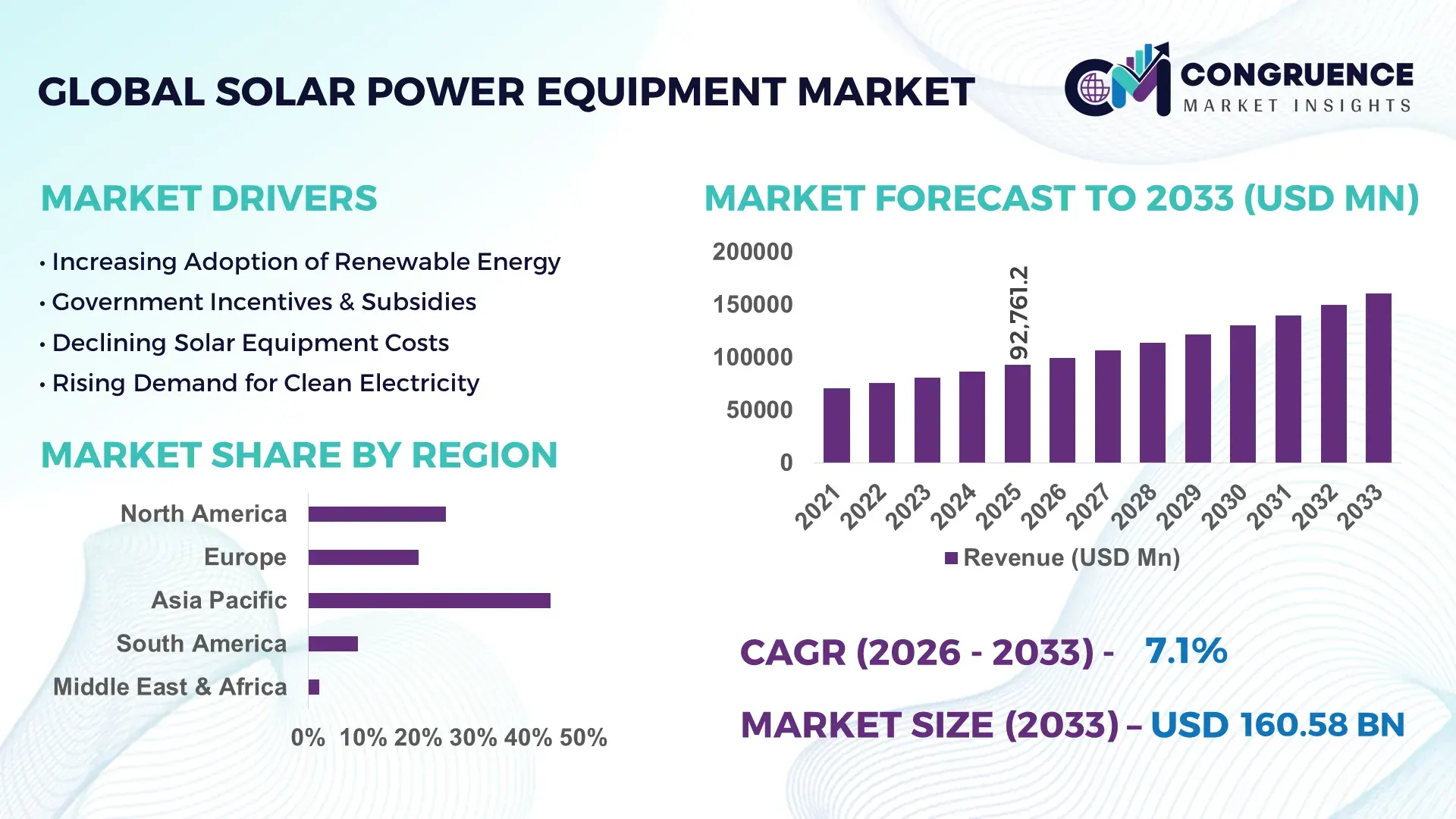

The Global Solar Power Equipment Market was valued at USD 92761.2 Million in 2025 and is anticipated to reach a value of USD 160576.56 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033. This growth is primarily driven by accelerating renewable energy adoption supported by government incentives and declining photovoltaic component costs.

China continues to lead the solar power equipment landscape with extensive manufacturing capacity exceeding 500 GW annually across photovoltaic modules, inverters, and related components. The country has invested over USD 130 billion in solar manufacturing and deployment infrastructure in recent years, with utility-scale installations accounting for over 65% of domestic solar deployments. Industrial applications such as grid-scale energy production and smart solar farms dominate usage, while distributed rooftop installations are growing steadily, contributing nearly 30% of installations. Technological advancements include high-efficiency TOPCon and HJT cell technologies achieving efficiencies above 25%, alongside rapid deployment of AI-enabled monitoring systems improving operational performance by over 15%.

Market Size & Growth: Valued at USD 92761.2 Million in 2025, projected to reach USD 160576.56 Million by 2033, growing at 7.1% driven by renewable energy expansion and cost-efficient solar technologies.

Top Growth Drivers: Renewable adoption increased by 32%, module efficiency improvements of 18%, grid integration demand rising by 27%.

Short-Term Forecast: By 2028, solar module production costs are expected to decline by 22%, improving project viability.

Emerging Technologies: Bifacial solar panels, AI-powered predictive maintenance, and perovskite solar cells are transforming efficiency benchmarks.

Regional Leaders: Asia-Pacific projected to reach USD 78000 Million by 2033 with large-scale installations, North America at USD 42000 Million driven by tax incentives, Europe at USD 36000 Million with strong decarbonization policies.

Consumer/End-User Trends: Industrial and utility sectors account for over 60% usage, while residential adoption is increasing due to rooftop solar incentives.

Pilot or Case Example: In 2024, a utility-scale solar farm achieved 19% efficiency improvement through AI-driven energy optimization systems.

Competitive Landscape: Market leader holds approximately 21% share, followed by major players including global inverter and module manufacturers driving innovation.

Regulatory & ESG Impact: Carbon neutrality targets and renewable mandates are pushing adoption, with over 45% of countries implementing solar incentives.

Investment & Funding Patterns: Over USD 300 billion invested globally in solar infrastructure, with rising green financing and public-private partnerships.

Innovation & Future Outlook: Integration of energy storage, smart grids, and digital twin technologies is shaping next-generation solar ecosystems.

The Solar Power Equipment market is characterized by strong contributions from utility-scale power generation accounting for nearly 58% of total installations, followed by commercial applications at 25% and residential usage at 17%. Technological innovations such as advanced inverter systems with over 98% efficiency, floating solar farms, and hybrid solar-wind systems are reshaping operational dynamics. Regulatory frameworks emphasizing carbon reduction, combined with economic incentives like feed-in tariffs and tax credits, are accelerating deployment. Regionally, Asia-Pacific leads in production and consumption, while Europe focuses on sustainable integration and North America on grid modernization. Emerging trends include decentralized solar networks, integration with battery storage, and AI-driven asset management, indicating a future defined by smart, scalable, and efficient solar infrastructure.

The Solar Power Equipment Market holds strategic importance as nations increasingly align energy policies with decarbonization targets and energy security priorities. Advanced photovoltaic technologies such as perovskite tandem cells deliver 30% efficiency improvement compared to traditional silicon-based modules, significantly enhancing output per installation area. Asia-Pacific dominates in production volume due to large-scale manufacturing ecosystems, while Europe leads in adoption with over 40% of enterprises integrating solar into energy portfolios.

In the near term, digitalization is transforming operations, with AI-enabled asset management expected to reduce maintenance costs by 25% by 2028. Smart inverter technologies and grid integration systems are enhancing energy distribution efficiency by over 20%, enabling better load balancing and reduced transmission losses. Firms are committing to ESG targets, including 50% reduction in lifecycle emissions and 35% increase in recyclable solar components by 2030, reflecting strong sustainability alignment.

A measurable example emerged in 2025 when a large-scale solar deployment in India improved energy output by 18% through AI-based predictive analytics and real-time monitoring systems. This demonstrates the practical application of digital transformation in optimizing solar infrastructure performance. Looking ahead, the Solar Power Equipment Market is positioned as a cornerstone of resilient energy systems, supporting regulatory compliance, driving cost efficiencies, and enabling sustainable growth across industrial and commercial sectors.

The rapid increase in renewable energy adoption is a primary driver of the Solar Power Equipment Market, supported by global commitments to reduce carbon emissions. Solar energy installations have grown by over 35% in the past five years, with solar power accounting for nearly 60% of newly added renewable capacity worldwide. Government incentives such as subsidies, tax credits, and feed-in tariffs have significantly reduced the cost burden for both industrial and residential users. Additionally, advancements in photovoltaic efficiency, now exceeding 25% in high-performance modules, have improved energy output and return on investment. Industrial sectors are increasingly adopting solar solutions to reduce energy costs, with large-scale solar farms delivering over 20% cost savings compared to conventional energy sources.

The Solar Power Equipment Market faces significant restraints due to supply chain disruptions and dependency on critical raw materials such as polysilicon, silver, and rare earth elements. Fluctuations in polysilicon prices have impacted production costs, with price volatility exceeding 40% during peak demand periods. Additionally, geopolitical tensions and trade restrictions have disrupted global supply chains, leading to delays in equipment delivery and increased project timelines. Manufacturing concentration in specific regions further exacerbates supply risks, limiting diversification. Logistics challenges and rising transportation costs have also affected the availability of components, creating bottlenecks that slow down large-scale project deployment and hinder consistent market expansion.

The integration of energy storage systems presents a significant opportunity for the Solar Power Equipment Market, enhancing the reliability and efficiency of solar power generation. Battery storage technologies have improved by over 30% in efficiency, enabling better energy retention and distribution during non-sunny periods. Hybrid systems combining solar panels with advanced lithium-ion batteries are gaining traction, particularly in regions with unstable grid infrastructure. The demand for off-grid and microgrid solutions is increasing, especially in developing economies, where nearly 20% of populations still face inconsistent electricity access. Additionally, innovations in solid-state batteries and grid-scale storage solutions are expected to further optimize energy utilization, creating new growth avenues for solar equipment manufacturers.

Regulatory complexities and grid integration challenges remain critical obstacles for the Solar Power Equipment Market. Variations in policy frameworks across regions create uncertainty for investors and developers, delaying project approvals and increasing compliance costs. Grid infrastructure in many regions is not fully equipped to handle intermittent solar energy, leading to inefficiencies and energy curtailment rates exceeding 10% in certain markets. Additionally, integrating large volumes of solar power into existing grids requires significant upgrades, including smart grid technologies and advanced inverters, which can increase capital expenditure by up to 25%. These challenges necessitate coordinated policy reforms and infrastructure investments to ensure seamless integration and sustained market growth.

• Rapid Efficiency Gains Through Advanced Cell Technologies:

Solar module efficiency has significantly improved, with TOPCon and heterojunction (HJT) technologies achieving conversion efficiencies above 25%, compared to 20%–21% in conventional PERC modules. Over 60% of newly installed utility-scale projects in 2025 adopted high-efficiency modules, increasing energy output per square meter by nearly 18%. This shift is enabling developers to optimize land use while reducing balance-of-system costs by approximately 12%. The transition toward next-generation cell architectures is also driving a 30% increase in demand for precision manufacturing equipment, particularly in Asia-Pacific production hubs.

• Expansion of Floating Solar Installations and Hybrid Systems:

Floating solar installations are gaining traction, with installed capacity exceeding 7 GW globally and growing by over 25% annually in deployment volume. These systems improve energy yield by 10%–15% due to natural cooling effects from water surfaces. Hybrid solar-wind projects are also expanding, with integrated systems improving capacity utilization rates by 20%. Regions with land constraints are prioritizing floating solar, with over 35% of new projects in densely populated markets incorporating water-based installations.

• Digitalization and AI-Driven Solar Asset Management:

AI-based monitoring systems are now integrated into over 45% of large-scale solar plants, enabling predictive maintenance and reducing downtime by up to 30%. Smart inverters with real-time analytics capabilities have improved grid synchronization efficiency by 22%, while automated fault detection systems reduce operational losses by nearly 18%. Digital twin technology adoption has increased by 28%, allowing operators to simulate performance scenarios and optimize energy output across complex solar installations.

• Growth in Decentralized and Rooftop Solar Adoption:

Decentralized solar systems, particularly rooftop installations, account for approximately 40% of new solar deployments in urban regions. Residential solar adoption has increased by 27%, driven by net metering policies and declining installation costs. Commercial and industrial users are installing on-site solar systems to reduce energy expenses, achieving savings of up to 25% on electricity bills. Microgrid integration is expanding rapidly, with over 15% of new distributed systems incorporating battery storage to ensure uninterrupted power supply and improved energy independence.

The Solar Power Equipment Market demonstrates a diversified segmentation structure across types, applications, and end-user industries, reflecting the complexity and scalability of solar energy systems. Equipment types such as photovoltaic modules, inverters, mounting systems, and energy storage solutions form the backbone of the market, with modules dominating due to their central role in energy generation. Application-wise, utility-scale solar installations lead due to large energy output requirements, while distributed solar systems are gaining traction in urban and semi-urban environments. End-user segmentation highlights strong adoption across utilities, commercial enterprises, and residential consumers, each contributing uniquely to demand patterns. Increasing electrification, policy incentives, and technological advancements are reshaping segment contributions, with energy storage and smart grid integration emerging as key differentiators across all categories.

Photovoltaic (PV) modules represent the leading segment, accounting for approximately 52% of total equipment adoption due to their fundamental role in solar energy generation and continuous efficiency improvements. In comparison, solar inverters contribute around 23% of installations, while mounting and tracking systems hold nearly 15%. However, energy storage systems are the fastest-growing segment, expanding at an estimated CAGR of 18%, driven by increasing demand for grid stability and off-grid solutions. Battery-integrated solar systems are witnessing rapid adoption, particularly in regions with intermittent grid supply. Other equipment types, including monitoring systems, cabling, and balance-of-system components, collectively contribute about 10% of the market, supporting system optimization and operational efficiency. Technological advancements in bifacial modules and smart inverters are further strengthening the dominance of core equipment segments.

Utility-scale solar installations dominate the application segment, accounting for nearly 58% of total deployments due to their ability to generate large volumes of electricity for grid supply. Commercial and industrial (C&I) applications hold approximately 27%, driven by enterprises seeking to reduce operational energy costs and improve sustainability metrics. Residential applications represent around 15%, reflecting steady growth supported by rooftop solar adoption. While utility-scale remains dominant, distributed solar systems in the commercial sector are the fastest-growing application, with an estimated CAGR of 16%, fueled by corporate sustainability goals and energy cost optimization strategies. Increasing adoption of hybrid solar systems combining storage and grid connectivity is further accelerating this segment. Other applications, including off-grid and rural electrification projects, contribute the remaining 10%, playing a critical role in expanding energy access in underserved regions.

Utilities remain the leading end-user segment, accounting for approximately 55% of total solar power equipment demand, driven by large-scale grid-connected solar projects and national renewable energy targets. Commercial and industrial users contribute around 30%, leveraging solar installations to reduce energy costs and meet ESG commitments. Residential users account for nearly 15%, with adoption supported by incentives and decreasing installation costs. Among these, commercial and industrial users represent the fastest-growing segment, with an estimated CAGR of 17%, as businesses increasingly integrate solar systems to achieve energy independence and cost savings. Adoption rates in manufacturing and logistics sectors have exceeded 35%, reflecting strong alignment with sustainability goals. Other end-users, including government institutions and agricultural sectors, collectively account for about 10% of the market, utilizing solar solutions for irrigation, public infrastructure, and remote operations.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2026 and 2033.

Asia-Pacific dominates due to large-scale manufacturing and installation capacity exceeding 700 GW of cumulative solar deployments, with China alone contributing over 55% of regional installations. North America holds approximately 22% of the global Solar Power Equipment market, supported by strong policy incentives and rising utility-scale projects exceeding 40 GW annually. Europe represents nearly 20% share, driven by aggressive carbon neutrality targets and over 30% renewable energy penetration across key economies. South America contributes around 7%, with Brazil accounting for more than 65% of regional solar capacity, while the Middle East & Africa collectively hold approximately 5%, supported by mega solar projects exceeding 10 GW capacity in key countries. Increasing electrification rates, declining equipment costs by nearly 18% over recent years, and grid modernization initiatives are shaping regional growth patterns across all major markets.

How are policy incentives and corporate energy transitions accelerating advanced solar infrastructure adoption?

North America accounts for approximately 22% of the global Solar Power Equipment market, with installations exceeding 40 GW annually. Key industries such as utilities, commercial real estate, and manufacturing are driving demand, with corporate renewable energy procurement increasing by over 25% in recent years. Government initiatives, including tax credits covering up to 30% of installation costs, are accelerating solar adoption across both residential and industrial sectors. Technological advancements such as AI-driven energy management systems and smart inverters have improved operational efficiency by 20%. A notable example includes a major U.S.-based solar developer deploying grid-scale battery-integrated systems that increased energy reliability by 18%. Consumer behavior reflects higher enterprise adoption, particularly in sectors like healthcare and finance, where sustainability commitments and cost optimization strategies are key drivers.

What factors are driving rapid adoption of sustainable and high-efficiency solar systems across advanced economies?

Europe holds nearly 20% of the Solar Power Equipment market, with leading countries such as Germany, the United Kingdom, and France contributing over 65% of regional installations. Strong regulatory frameworks and sustainability initiatives, including carbon neutrality targets and renewable energy directives, are pushing adoption rates beyond 30% across industrial sectors. The region is witnessing increased deployment of high-efficiency bifacial modules and energy storage systems, improving energy output by 15%–20%. Digital monitoring and grid integration technologies are also gaining traction, with over 35% of solar plants using advanced analytics. A key example includes a European solar manufacturer expanding production of high-efficiency modules, achieving a 22% improvement in output performance. Consumer behavior is shaped by regulatory pressure, leading to increased demand for transparent, efficient, and environmentally compliant solar solutions.

Why is large-scale manufacturing and infrastructure expansion reshaping global solar supply chains?

Asia-Pacific leads the Solar Power Equipment market in volume, contributing over 46% of global installations, with China, India, and Japan as the top consuming countries. China alone has installed more than 350 GW of solar capacity, while India is rapidly expanding with annual additions exceeding 15 GW. The region serves as the global manufacturing hub, producing over 80% of photovoltaic modules and related components. Infrastructure development, including ultra-large solar parks and grid expansion projects, is driving equipment demand. Technological innovation hubs are focusing on next-generation cell technologies, with efficiency improvements exceeding 25%. A regional manufacturer recently scaled production capacity by 30%, enhancing supply chain resilience. Consumer behavior reflects strong adoption driven by industrial demand and government-backed electrification programs, particularly in emerging economies.

How are energy diversification and policy incentives shaping solar infrastructure expansion?

South America accounts for approximately 7% of the global Solar Power Equipment market, with Brazil and Argentina leading regional adoption. Brazil alone represents over 65% of regional installations, supported by distributed solar systems exceeding 25 GW capacity. Infrastructure trends indicate increasing investment in grid-connected and off-grid solar solutions, particularly in remote areas. Government incentives such as tax exemptions and net metering policies are encouraging residential and commercial adoption, resulting in a 28% increase in rooftop installations. A regional solar developer has expanded its portfolio by integrating hybrid solar-storage systems, improving energy reliability by 20%. Consumer behavior varies across the region, with demand closely tied to energy cost savings and localized energy independence initiatives.

What role do mega projects and energy diversification strategies play in accelerating solar adoption?

The Middle East & Africa region holds around 5% of the Solar Power Equipment market, with major growth driven by countries such as the United Arab Emirates and South Africa. Large-scale solar projects exceeding 10 GW capacity are transforming the energy landscape, particularly in desert regions with high solar irradiance levels. Demand is driven by sectors such as oil & gas, construction, and utilities seeking to diversify energy sources. Technological modernization, including high-capacity inverters and tracking systems, has improved efficiency by over 18%. Trade partnerships and government-backed initiatives are facilitating large-scale investments in renewable infrastructure. A regional project developer recently implemented a solar plant that reduced operational energy costs by 25%. Consumer behavior is influenced by industrial demand and government-led sustainability programs.

China – 34% market share in the Solar Power Equipment market, driven by large-scale manufacturing capacity and extensive solar infrastructure deployment.

United States – 18% market share in the Solar Power Equipment market, supported by strong policy incentives and high demand from utility and commercial sectors.

The Solar Power Equipment market is moderately consolidated, with the top five companies accounting for approximately 48% of the total market share, while over 150 active global and regional players contribute to competitive dynamics. Leading companies are focusing on vertical integration strategies, controlling everything from raw material sourcing to module production and system deployment. Strategic initiatives such as mergers, acquisitions, and joint ventures have increased by nearly 20% over the past three years, aimed at expanding production capacity and geographic reach.

Innovation remains a key competitive factor, with over 60% of major players investing heavily in research and development to enhance photovoltaic efficiency and develop next-generation technologies such as perovskite solar cells. Product differentiation is also evident in the increasing adoption of bifacial modules and AI-integrated inverters, improving system performance by up to 25%.

Partnerships between equipment manufacturers and energy developers are rising, with more than 35% of large-scale projects involving collaborative agreements. Additionally, companies are focusing on sustainability initiatives, including recyclable solar components and reduced carbon footprints, aligning with global ESG standards. The competitive landscape is further shaped by pricing strategies, supply chain optimization, and technological innovation, making it highly dynamic and performance-driven.

First Solar Inc.

Trina Solar Co., Ltd.

Canadian Solar Inc.

JinkoSolar Holding Co., Ltd.

LONGi Green Energy Technology Co., Ltd.

JA Solar Technology Co., Ltd.

SMA Solar Technology AG

ABB Ltd.

Siemens Energy AG

Huawei Technologies Co., Ltd.

Technological advancements in the Solar Power Equipment Market are centered on improving efficiency, durability, and system integration across photovoltaic and energy management systems. High-efficiency cell technologies such as TOPCon (Tunnel Oxide Passivated Contact) and heterojunction (HJT) are achieving module efficiencies exceeding 25%, compared to traditional polycrystalline modules at 17%–19%. Bifacial solar panels are gaining widespread adoption, contributing up to 12% additional energy yield by capturing reflected sunlight from ground surfaces, particularly in utility-scale installations.

Inverter technology is also evolving rapidly, with modern string inverters achieving efficiency levels above 98% and integrating AI-based diagnostics that reduce system downtime by nearly 30%. Smart inverters now support grid-forming capabilities, enabling better voltage regulation and frequency stability in renewable-heavy grids. Additionally, module-level power electronics (MLPE), including microinverters and power optimizers, are improving system performance by up to 20% in shaded or complex rooftop installations.

Energy storage integration is becoming a critical technological component, with lithium-ion battery systems delivering round-trip efficiencies above 90%. Emerging solid-state batteries are under development, promising 40% higher energy density and improved safety. Digital technologies such as IoT-enabled monitoring platforms and digital twin simulations are being deployed in over 35% of large solar plants, allowing predictive maintenance and real-time performance optimization.

Manufacturing innovations are also reshaping the market, with automated production lines increasing throughput by 25% and reducing defect rates by 15%. Advanced materials such as perovskite-silicon tandem cells are under pilot deployment, demonstrating potential efficiencies above 30%, indicating a strong technological pipeline that will define the next phase of solar power equipment evolution.

• In May 2025, First Solar announced the commercial production of its next-generation Series 7 thin-film modules, achieving over 22% efficiency and reducing manufacturing emissions by approximately 30%, strengthening its position in sustainable large-scale solar deployment. Source: www.firstsolar.com

• In March 2025, LONGi Green Energy introduced its Hi-MO 9 module based on advanced HPBC cell technology, delivering module efficiency exceeding 24.5% and improving power output by 6% compared to previous-generation products. Source: www.longi.com

• In September 2024, JinkoSolar unveiled its N-type TOPCon Tiger Neo modules with mass production efficiency surpassing 23%, enabling energy yield improvements of nearly 5% in utility-scale solar installations. Source: www.jinkosolar.com

• In July 2024, Trina Solar deployed its Vertex N 700W+ high-power modules in a large-scale solar project, increasing system output density by over 20% and reducing land usage requirements by approximately 10%. Source: www.trinasolar.com

The Solar Power Equipment Market Report provides a comprehensive analysis of key segments, technologies, and regional dynamics shaping the global solar industry. The scope encompasses a wide range of equipment types including photovoltaic modules, inverters, mounting structures, tracking systems, and energy storage solutions, collectively supporting installations exceeding 1,500 GW of global solar capacity. It examines application areas such as utility-scale power generation, commercial and industrial systems, and residential rooftop installations, each contributing distinct demand patterns and technology adoption rates.

Geographically, the report covers major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, representing over 95% of global solar deployment activity. It highlights regional variations in infrastructure development, policy frameworks, and technological adoption, with Asia-Pacific leading in manufacturing output exceeding 80% of global module production.

The report also addresses emerging segments such as floating solar installations, agrivoltaics, and hybrid renewable systems, which are gaining traction due to land optimization and multi-use capabilities. Technology coverage includes advanced cell architectures, energy storage integration, smart grid connectivity, and digital asset management systems. Additionally, it evaluates industry trends such as decentralized energy generation, electrification initiatives, and sustainability-driven investments. With a focus on operational efficiency, system performance, and innovation trends, the report serves as a strategic resource for stakeholders, offering insights into evolving market structures, competitive positioning, and future-ready solar infrastructure development.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

First Solar Inc., Trina Solar Co., Ltd., Canadian Solar Inc., JinkoSolar Holding Co., Ltd., LONGi Green Energy Technology Co., Ltd., JA Solar Technology Co., Ltd., SMA Solar Technology AG, ABB Ltd., Siemens Energy AG, Huawei Technologies Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |