Reports

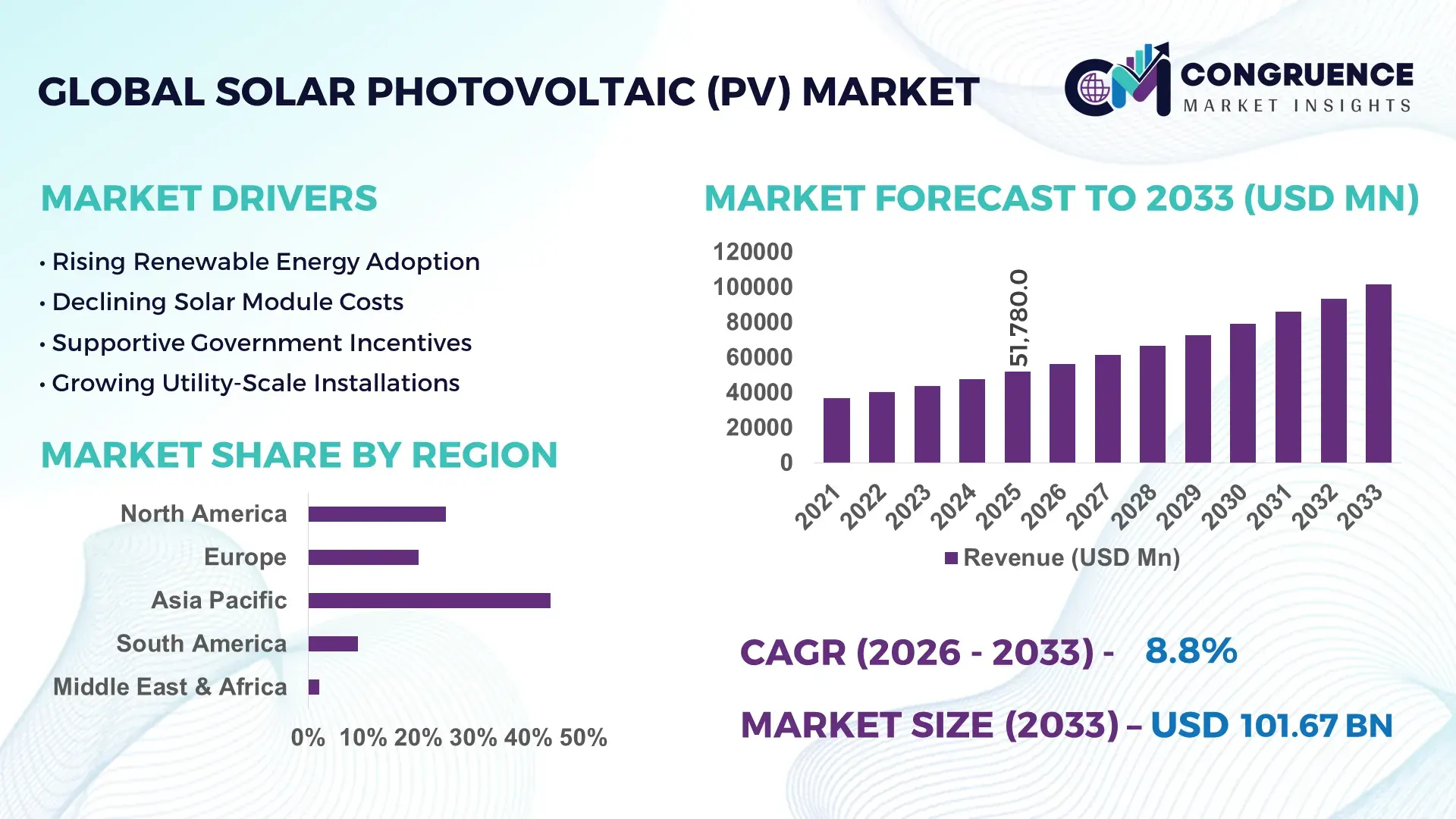

The Global Solar Photovoltaic (PV) Market was valued at USD 51780 Million in 2025 and is anticipated to reach a value of USD 101670.09 Million by 2033 expanding at a CAGR of 8.8% between 2026 and 2033. Grid-scale solar deployment, TOPCon cell expansion, and domestic module manufacturing incentives across Asia-Pacific and North America are accelerating utility procurement cycles and reducing module production costs by over 18% in large-volume projects.

China maintains market dominance with nearly 43% of global installed PV capacity in 2026, supported by over 280 GW annual module output and vertically integrated polysilicon supply chains, while the United States is accelerating localized manufacturing through Inflation Reduction Act-linked investments exceeding USD 35 billion. India is emerging as a high-growth production hub with utility-scale adoption rising above 22% year-on-year, driven by renewable auction programs, transmission upgrades, and high-efficiency bifacial module deployment across industrial and commercial sectors amid ongoing global energy security realignment after the Russia-Ukraine conflict.

Manufacturers and energy developers are prioritizing regionalized supply chains, advanced cell efficiency upgrades, and long-term power purchase agreements to secure competitive positioning in the high-growth global solar photovoltaic ecosystem.

Market Size & Growth: USD 51,780 million in 2025 reaching USD 101,670.09 million by 2033, driven by TOPCon module scaling, utility solar auctions, and localized manufacturing expansion.

Top Growth Drivers: Utility-scale deployment up 24%, commercial rooftop installations up 19%, and battery-integrated solar projects rising 27% globally.

Short-Term Forecast: By 2028, module production costs are projected to decline 16% while average conversion efficiency improves beyond 25% in advanced PV systems.

Emerging Technologies: AI-enabled predictive maintenance, perovskite tandem cells, and robotic panel cleaning are improving operational efficiency by over 14%.

Regional Leaders: Asia-Pacific exceeds USD 46 billion with manufacturing dominance, North America crosses USD 21 billion through domestic incentives, and Europe surpasses USD 18 billion via energy transition mandates.

Consumer/End-User Trends: Over 38% of commercial facilities are integrating solar-plus-storage systems to stabilize electricity costs and peak-load demand.

Pilot/Case Example: In 2026, a large-scale Middle East desert PV project improved energy yield by 12% using bifacial tracking technology and AI-driven monitoring.

Competitive Landscape: China-based manufacturers collectively control nearly 58% of global module supply, alongside major participation from U.S., Indian, and European energy technology firms.

Regulatory & ESG Impact: Carbon-reduction mandates increased renewable procurement commitments by 31%, while localized sourcing policies accelerated regional supply-chain restructuring.

Investment & Funding: Global solar infrastructure investment exceeded USD 340 billion in 2026, led by manufacturing expansion, grid modernization, and strategic energy partnerships.

Innovation & Future Outlook: Next-generation tandem solar cells and recycling-focused circular manufacturing strategies are reshaping long-term competitiveness across the advanced PV market.

Solar Photovoltaic (PV) Market demand is expanding rapidly across utility-scale power generation, industrial energy procurement, and commercial rooftop integration as high-efficiency TOPCon and bifacial modules improve output performance by nearly 15%. Domestic manufacturing incentives and polysilicon supply diversification are reshaping procurement strategies, particularly across India, Southeast Asia, and North America. Simultaneously, AI-enabled energy forecasting and storage-linked solar infrastructure are strengthening grid reliability, setting the stage for broader strategic market transformation.

Solar photovoltaic deployment is becoming strategically central to industrial competitiveness, grid modernization, and national energy security strategies as manufacturers and utilities accelerate low-cost electrification programs. Supply-chain restructuring after global trade disruptions has pushed countries including the United States, India, and Vietnam to expand domestic cell and module manufacturing capacity, while digital energy management platforms are improving solar asset utilization by nearly 13%. Industrial buyers are increasingly integrating long-term solar procurement into operational cost-control strategies, particularly across data centers, automotive manufacturing, and semiconductor production facilities.

Advanced TOPCon and heterojunction modules are delivering 4–6% higher conversion efficiency compared to conventional PERC systems while reducing balance-of-system costs through higher energy density. China continues to dominate high-volume production and polysilicon integration, whereas Germany and Japan are concentrating on smart-grid interoperability and high-efficiency rooftop systems. In 2026, multiple utility operators in India deployed AI-based predictive monitoring across large-scale solar parks, reducing maintenance downtime by approximately 18% and improving dispatch consistency during peak summer demand cycles.

Over the next two to three years, companies are prioritizing localized supply agreements, storage-linked solar infrastructure, and strategic technology partnerships to secure operational resilience and faster deployment timelines. Businesses capable of combining manufacturing scale, advanced module efficiency, and digital asset optimization will strengthen long-term positioning across the increasingly competitive global solar photovoltaic value chain.

Large-scale electrification programs and domestic manufacturing incentives are accelerating solar photovoltaic deployment across industrial and utility sectors. India increased solar module manufacturing capacity by over 38% between 2024 and 2026 through production-linked incentive schemes, while the United States expanded domestic wafer and cell investments to reduce import dependency. High-efficiency TOPCon modules are improving plant output by nearly 15% compared to older multicrystalline systems, directly lowering levelized electricity costs for utilities and commercial operators. Simultaneously, energy-intensive industries including steel, automotive, and data infrastructure are increasing renewable procurement targets to stabilize long-term power costs. In response, developers are securing vertically integrated supply partnerships, expanding storage-linked solar assets, and prioritizing localized procurement models to improve project execution speed and operational resilience.

Transmission bottlenecks and upstream material price instability continue to constrain large-scale solar deployment efficiency. In several high-growth markets, grid interconnection delays extended project commissioning timelines by 20–30%, particularly across industrial clusters with weak transmission infrastructure. Polysilicon and silver paste cost fluctuations also increased module pricing volatility by nearly 12% during recent procurement cycles, affecting project margins and utility bidding strategies. Europe and Southeast Asia remain partially dependent on imported wafers and inverter components, creating operational exposure during trade restrictions and logistics disruptions. To reduce scalability risks, manufacturers are diversifying sourcing networks, investing in localized assembly facilities, and adopting thinner wafer technologies that reduce silver consumption while maintaining energy conversion performance.

Solar-plus-storage integration and intelligent energy optimization platforms are creating high-value opportunities beyond conventional electricity generation. Commercial and industrial users adopting battery-linked solar systems reported peak-demand cost reductions exceeding 22%, while AI-driven energy forecasting improved load-balancing efficiency by nearly 17%. Japan and Australia are accelerating deployment of virtual power plant networks that combine distributed solar assets with digital grid coordination systems. Simultaneously, perovskite tandem cell development is advancing module efficiency above 30% under pilot-scale conditions, opening new opportunities for space-constrained urban installations. Companies are expanding software partnerships, investing in grid analytics capabilities, and developing integrated energy-service models that combine generation, storage, monitoring, and predictive maintenance into scalable long-term infrastructure offerings.

Long-term market expansion depends on synchronized grid modernization, skilled workforce availability, and advanced system integration capabilities. Utility operators in rapidly expanding markets including India and Brazil are facing inverter interoperability issues and transmission instability as variable renewable penetration exceeds 25% in certain networks. Large-scale projects increasingly require cybersecurity protection for digitally connected monitoring platforms, particularly as AI-enabled asset management adoption rises above 40% among utility operators. At the same time, shortages of trained installation and maintenance technicians are slowing commissioning timelines for complex hybrid solar-storage systems. Companies must strengthen engineering partnerships, invest in workforce training programs, and modernize grid-balancing infrastructure to maintain deployment consistency, operational security, and long-term competitiveness in high-capacity renewable power ecosystems.

AI-Driven Solar Asset Optimization Utility operators are increasingly deploying AI-enabled monitoring platforms that reduce predictive maintenance downtime by nearly 18% and improve energy yield forecasting accuracy by over 20%. Large-scale solar parks in India and the United States are integrating digital twin systems to automate panel diagnostics and inverter balancing. This transition is lowering operational expenditure while improving grid dispatch reliability during peak demand periods. EPC firms and asset operators are responding through software partnerships, centralized control platforms, and automation-focused operations restructuring.

Localized Manufacturing Expansion Accelerates Supply-chain diversification efforts following geopolitical trade disruptions are reshaping module and wafer production strategies. India expanded domestic module assembly capacity by more than 35% between 2024 and 2026, while U.S.-based manufacturers increased localized component sourcing to reduce import dependency. Companies are shifting procurement contracts closer to installation markets, shortening delivery cycles by nearly 14%. Manufacturers are simultaneously investing in vertically integrated facilities to stabilize polysilicon access and improve production consistency.

Bifacial and TOPCon Adoption Surges High-efficiency bifacial and TOPCon modules are replacing conventional PERC systems across utility-scale deployments due to 5–7% higher energy generation and improved thermal performance. Desert-based solar projects in the Middle East and Australia are rapidly adopting dual-glass bifacial designs to maximize irradiation capture. Developers are prioritizing advanced tracker integration and lightweight mounting systems that accelerate installation speed by approximately 12%, improving land-use productivity and project economics.

Storage-Linked Solar Deployment Expands Commercial and industrial operators are increasingly pairing photovoltaic systems with battery storage to stabilize electricity costs and improve energy resilience. Hybrid solar-storage installations grew by nearly 28% in high-load manufacturing clusters across China and Germany, particularly among automotive and semiconductor facilities facing grid volatility. This operational shift is reducing peak-demand exposure while improving backup continuity during transmission instability. Energy providers are scaling integrated infrastructure partnerships, smart inverters, and long-duration storage deployments to strengthen distributed energy ecosystems.

Monocrystalline solar modules continue to dominate the solar photovoltaic market due to superior conversion efficiency, longer operational lifespan, and stronger compatibility with utility-scale and commercial installations. In 2026, monocrystalline systems accounted for nearly 62% of new deployments as TOPCon-based architectures improved output performance by over 15% compared to conventional polycrystalline alternatives. Manufacturers in China, India, and the United States are prioritizing automated cell production lines and vertically integrated wafer manufacturing to support high-volume demand. Polycrystalline modules remain relevant in cost-sensitive projects, particularly across emerging rural electrification programs where lower upfront pricing remains operationally attractive.

Bifacial modules represent the fastest-growing segment, supported by rising adoption in desert-based utility projects and high-irradiation industrial zones. Energy generation gains of 6–9% compared to standard monofacial systems are accelerating deployment across the Middle East and Australia. Thin film technology is strengthening its position in lightweight and flexible applications, while Building-Integrated PV is gaining traction in urban infrastructure modernization projects and net-zero commercial construction. Companies are expanding R&D investments, strategic material sourcing, and premium module portfolios to secure long-term competitive differentiation.

Utility-scale applications continue to dominate global solar photovoltaic deployment due to large-capacity procurement programs, grid modernization initiatives, and competitive levelized electricity generation costs. In 2026, utility-scale projects represented approximately 58% of newly installed capacity, particularly across China, India, and the United States where large transmission-linked solar parks are supporting industrial electrification. Automated tracking systems and AI-enabled energy forecasting tools improved plant utilization efficiency by nearly 14%, enabling operators to stabilize dispatch performance during variable demand cycles. Developers are expanding storage-linked infrastructure and long-term power purchase agreements to secure operational predictability and faster project monetization.

Industrial applications are emerging as the fastest-growing segment as manufacturers seek long-term energy cost stabilization and supply resilience. Heavy industries including automotive, semiconductor fabrication, and steel processing increased captive solar deployment by over 24% between 2024 and 2026. Commercial installations are also expanding through rooftop integration and energy management platforms, while residential systems are benefiting from smart-home compatibility and battery integration. Off-grid systems remain strategically important across remote mining, agricultural, and island electrification projects where grid extension remains economically inefficient.

Utilities remain the dominant end-user group within the solar photovoltaic market due to high-capacity procurement programs, national decarbonization targets, and large-scale transmission integration strategies. In 2026, utility operators accounted for nearly 54% of total photovoltaic installations, driven by expansion of gigawatt-scale solar parks and hybrid renewable infrastructure projects. Advanced grid-balancing systems and predictive analytics improved renewable dispatch efficiency by approximately 16%, enabling higher renewable penetration across national electricity networks. Utility-focused developers are strengthening long-term equipment partnerships, expanding energy storage integration, and prioritizing localized procurement models to reduce operational exposure during supply-chain disruptions.

Industrial facilities are emerging as the fastest-growing end-user segment as electricity-intensive sectors seek energy independence and operational cost control. Semiconductor plants, logistics hubs, and automotive manufacturing sites increased solar procurement activity by nearly 26% between 2024 and 2026. Commercial buildings are adopting rooftop photovoltaic systems integrated with intelligent energy management software, while agricultural users are increasingly deploying solar-powered irrigation and microgrid systems. Government-sector demand is also accelerating through public infrastructure modernization and energy security programs, prompting suppliers to diversify financing models and deployment partnerships across multiple customer ecosystems.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 10.6% between 2026 and 2033.

Domestic Manufacturing and Grid Modernization Accelerate Deployment

North America remains a strategically important solar photovoltaic market driven by localized manufacturing expansion, grid modernization programs, and utility-scale renewable integration. The region represented nearly 22% of global photovoltaic deployment activity in 2025, supported by strong investment in domestic module assembly, battery-linked solar infrastructure, and high-capacity transmission upgrades. Utility operators across the United States and Canada are accelerating AI-enabled energy management adoption, improving solar asset utilization efficiency by approximately 15%. Large-scale procurement contracts and domestic sourcing incentives are also reducing dependence on imported wafers and modules. Energy developers are prioritizing vertically integrated partnerships and long-duration storage integration to improve grid stability during peak demand fluctuations and severe weather disruptions.

United States Market Outlook: The United States leads regional solar photovoltaic deployment through strong utility-scale project execution, manufacturing incentives, and advanced grid infrastructure investment. Domestic solar manufacturing capacity expanded by more than 30% between 2024 and 2026, while large hyperscale data center operators significantly increased renewable procurement agreements. Advanced tracker systems, battery-integrated solar farms, and localized polysilicon processing investments are strengthening supply resilience and operational scalability across industrial and utility sectors.

Energy Security and Smart Infrastructure Drive Modernization

Europe continues to strengthen its photovoltaic infrastructure through energy security policies, decarbonization mandates, and smart-grid modernization initiatives. The region accounted for approximately 19% of global photovoltaic installations in 2025, with Germany, Spain, and Italy leading utility-scale and commercial rooftop deployments. Rising electricity price volatility accelerated solar-plus-storage adoption across industrial facilities, while digital grid-balancing systems improved renewable dispatch efficiency by nearly 13%. Several European utilities are restructuring procurement frameworks to prioritize localized inverter manufacturing and supply-chain diversification. Building-integrated photovoltaic systems are also gaining traction across commercial construction projects as governments tighten net-zero building standards and accelerate renewable infrastructure permitting reforms.

Germany Market Outlook: Germany remains the region’s operational and technology leader through advanced rooftop deployment density, industrial solar adoption, and smart-grid integration capabilities. Commercial photovoltaic installations linked with battery storage increased by over 21% between 2024 and 2026 as manufacturing facilities sought greater energy independence. German energy firms are investing heavily in AI-enabled grid balancing, high-efficiency module integration, and decentralized virtual power plant systems to improve renewable energy reliability and industrial competitiveness.

Manufacturing Scale and Utility Deployment Dominate Expansion

Asia-Pacific leads the global solar photovoltaic market through unmatched manufacturing scale, vertically integrated supply chains, and large-capacity utility deployment programs. The region contributed nearly 47% of global photovoltaic installations in 2025, supported by strong production concentration across China, India, South Korea, and Vietnam. China alone maintains over 75% of global polysilicon and wafer processing capacity, enabling lower module production costs and faster export scalability. Simultaneously, India is accelerating domestic manufacturing through production-linked incentives and transmission infrastructure upgrades. Utility-scale solar parks integrated with AI-enabled monitoring systems improved operational efficiency by approximately 16%, while regional exporters are expanding automated manufacturing lines to support rising international demand.

China Market Outlook: China remains the dominant operational center of the global photovoltaic ecosystem through extensive module manufacturing, advanced cell technology development, and large-scale infrastructure deployment. In 2026, high-efficiency TOPCon production lines accounted for more than 55% of newly commissioned domestic module capacity. Chinese manufacturers are strengthening global competitiveness through vertical integration, robotic production systems, and long-term polysilicon procurement agreements while simultaneously expanding overseas project partnerships and export-oriented manufacturing ecosystems.

Industrial Electrification and Distributed Generation Expand Demand

South America is strengthening its photovoltaic deployment capacity through industrial electrification, distributed energy adoption, and utility diversification programs. The region represented nearly 6% of global photovoltaic installations in 2025, with Brazil and Chile leading large-scale solar integration and mining-sector renewable adoption. Grid instability and rising industrial electricity costs are accelerating commercial and industrial rooftop deployment, particularly across manufacturing and agricultural clusters. Utility operators are also increasing hybrid solar-storage installations to stabilize supply reliability during transmission constraints. However, uneven transmission infrastructure and project financing limitations continue to affect deployment speed in several emerging economies, prompting developers to prioritize modular and decentralized solar project structures.

Brazil Market Outlook: Brazil leads regional photovoltaic deployment through strong distributed generation adoption, utility-scale solar expansion, and industrial renewable procurement activity. Commercial and residential rooftop installations increased by approximately 25% between 2024 and 2026 as electricity-intensive industries sought long-term energy cost stability. Brazilian developers are expanding transmission-linked solar infrastructure and battery integration partnerships while leveraging favorable irradiation conditions and growing corporate renewable procurement commitments to strengthen operational competitiveness.

Mega-Project Investments Reshape Energy Infrastructure

Middle East & Africa is emerging as the fastest-transforming photovoltaic market through utility-scale mega-projects, energy diversification programs, and grid modernization investments. The region accounted for nearly 8% of global photovoltaic deployment activity in 2025, driven by high-irradiation conditions and aggressive renewable infrastructure targets. Gulf countries are accelerating gigawatt-scale solar park development integrated with battery storage and smart transmission systems, while African economies are expanding off-grid solar electrification programs to improve rural energy access. Large-scale desert installations using bifacial modules improved energy yield by approximately 10% compared to standard monofacial systems. Energy developers are increasingly forming cross-border partnerships and long-term engineering contracts to accelerate execution timelines and technology transfer.

Saudi Arabia Market Outlook: Saudi Arabia is rapidly strengthening its photovoltaic leadership position through utility-scale renewable infrastructure investments and industrial diversification initiatives under long-term energy transition strategies. In 2026, multiple gigawatt-scale solar projects advanced through public-private partnership frameworks supported by localized manufacturing plans and advanced grid integration programs. The country is prioritizing high-efficiency bifacial technologies, AI-based energy monitoring systems, and large transmission upgrades to support stable renewable integration across industrial and urban development corridors.

The solar photovoltaic market is dominated by global manufacturers including JinkoSolar, LONGi Green Energy, Trina Solar, JA Solar, and Canadian Solar, competing aggressively against regional module assemblers, inverter suppliers, and emerging bifacial technology specialists. The top five players collectively control nearly 52% of global module shipments through manufacturing scale, vertically integrated polysilicon sourcing, and rapid production expansion. Chinese manufacturers compete on cost efficiency and supply-chain control, while U.S., European, and Indian players focus on localized manufacturing, premium efficiency modules, and regulatory-compliant sourcing. TOPCon and heterojunction technologies improved module conversion efficiency by 4–6%, intensifying competition around performance optimization and land-use productivity. Companies are strengthening market position through long-term wafer procurement contracts, automated production systems reducing operating costs by nearly 12%, and strategic partnerships with utilities and storage providers. High capital intensity, technology transition pressure, and raw material access remain major entry barriers. Sustained competitiveness requires manufacturing scale, advanced efficiency architecture, localized supply resilience, and integrated digital energy capabilities.

JinkoSolar

LONGi Green Energy Technology

Trina Solar

JA Solar Technology

Canadian Solar

First Solar

Hanwha Qcells

Risen Energy

SunPower Corporation

Tongwei Solar

REC Group

Adani Solar

Vikram Solar

Maxeon Solar Technologies

High-efficiency TOPCon and bifacial solar technologies are dominating photovoltaic deployment between 2026 and 2028 as utilities and industrial operators prioritize higher output density and lower operating costs. TOPCon modules now represent nearly 85% of new global production lines, while advanced bifacial systems improve energy yield by 6–9% compared to conventional monofacial architectures. Compared with legacy PERC modules, next-generation TOPCon systems deliver approximately 4–6% higher conversion efficiency and lower long-term degradation rates. Manufacturers in China, India, and the United States are expanding automated cell processing and vertically integrated wafer production to accelerate deployment speed and strengthen supply-chain resilience.

Emerging technologies including perovskite-TOPCon tandem cells, AI-driven predictive maintenance platforms, and lightweight dual-glass modules are reshaping operational performance standards. Tandem architectures have already crossed 32% efficiency in advanced pilot systems, significantly outperforming traditional crystalline silicon platforms. Simultaneously, AI-enabled monitoring systems are reducing solar plant downtime by nearly 18% through automated fault detection and predictive asset management. Commercial operators and utility developers are increasingly integrating digital energy analytics with storage-linked solar infrastructure to improve dispatch consistency and land-use optimization.

Disruptive innovation is shifting competition away from pure manufacturing scale toward efficiency leadership, smart-grid compatibility, and integrated energy ecosystems. Companies capable of combining advanced module architecture, digital optimization, and localized production strategies will secure operational advantages as procurement standards tighten and grid-interoperability requirements accelerate through 2028.

June 2026 – JinkoSolar launched its Tiger Neo 5.0 TOPCon module series with 700 W output and 25.91% efficiency, improving power density beyond 259 W/m². The upgrade strengthened utility-scale competitiveness through higher land-use productivity and lower balance-of-system costs. Source: pv-magazine.com

April 2026 – Suniva announced a USD 350 million expansion in South Carolina, increasing U.S. solar cell manufacturing capacity from 1 GW to 5.5 GW while adding over 550 jobs. The investment strengthened domestic supply-chain resilience and reduced import dependency for federally supported renewable projects. Source: reuters.com

January 2025 – JinkoSolar achieved 33.84% conversion efficiency in its N-type TOPCon perovskite tandem solar cell platform, surpassing its previous 33.24% benchmark. The milestone accelerated next-generation high-efficiency photovoltaic commercialization and reinforced competition around advanced tandem-cell manufacturing capabilities. Source: jinkosolar.com

November 2025 – Emmvee Photovoltaic announced a USD 625 million manufacturing expansion plan targeting 16.3 GW module capacity by 2028, up from 7.8 GW. The move strengthened India’s domestic photovoltaic manufacturing ecosystem and improved regional export competitiveness amid global supply-chain diversification.

The Solar Photovoltaic (PV) Market report provides detailed analysis across module technologies, deployment models, operational trends, and competitive positioning between 2026 and 2033. The study covers key types including monocrystalline, polycrystalline, thin film, bifacial, and building-integrated photovoltaic systems, alongside application analysis spanning residential, commercial, utility-scale, industrial, and off-grid deployments. The report evaluates demand concentration across utilities, industrial facilities, government infrastructure, commercial buildings, and agricultural operations while highlighting adoption shifts linked to storage integration, AI-enabled monitoring, and localized manufacturing expansion.

Regional assessment includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level operational insights covering manufacturing scale, deployment concentration, grid modernization, and renewable infrastructure investment. More than 50% of the analysis focuses on high-efficiency technologies, integrated energy ecosystems, and supply-chain restructuring trends shaping procurement and production strategies. The report supports strategic investment planning, manufacturing expansion, technology benchmarking, partnership evaluation, and long-term competitive positioning across the evolving global photovoltaic ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 51780 Million |

|

Market Revenue in 2033 |

USD 101670.09 Million |

|

CAGR (2026 - 2033) |

8.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

JinkoSolar, LONGi Green Energy Technology, Trina Solar, JA Solar Technology, Canadian Solar, First Solar, Hanwha Qcells, Risen Energy, SunPower Corporation, Tongwei Solar, REC Group, Adani Solar, Vikram Solar, Maxeon Solar Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |