Reports

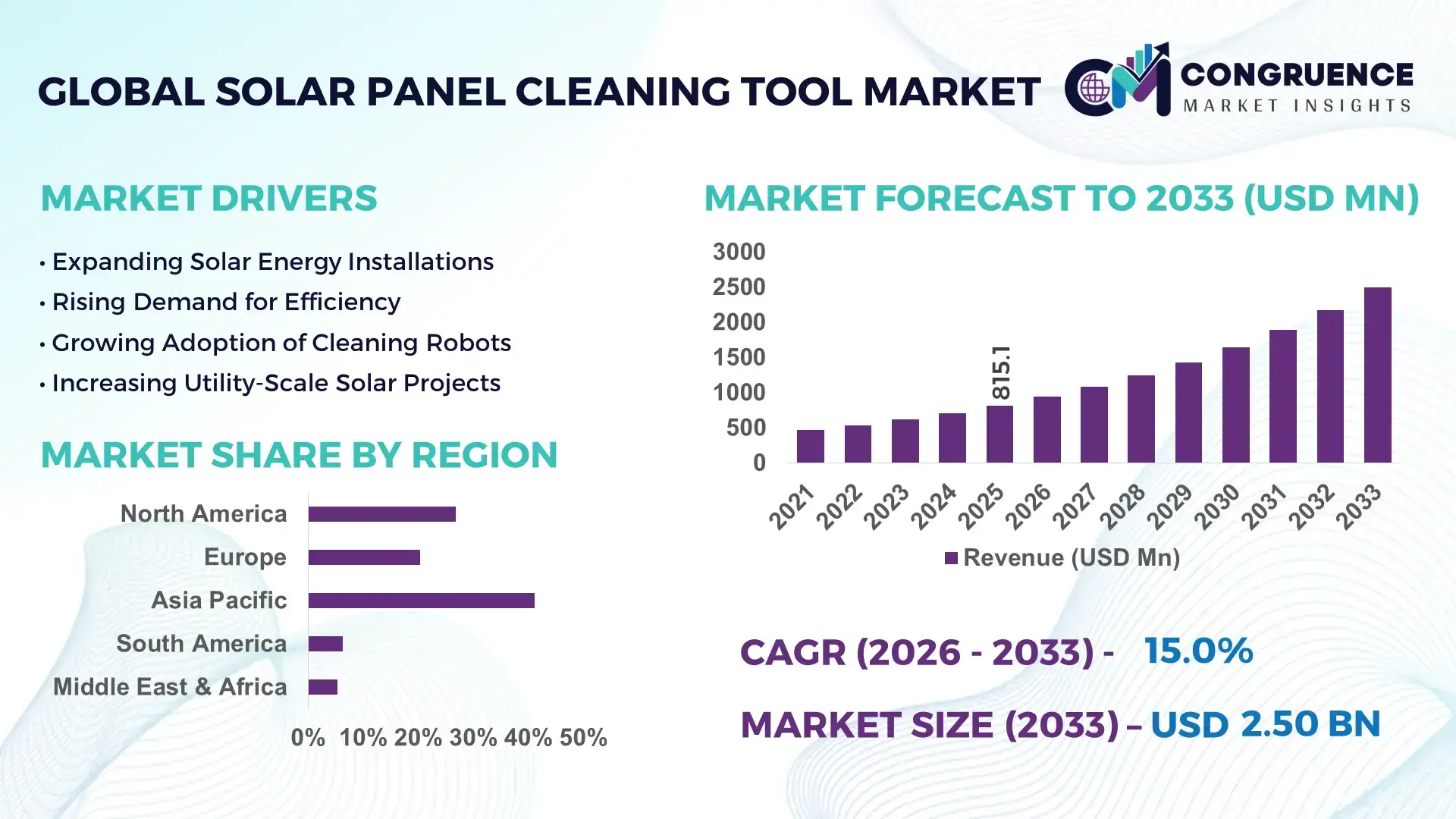

The Global Solar Panel Cleaning Tool Market was valued at USD 815.1 Million in 2025 and is anticipated to reach a value of USD 2,496.9 Million by 2033 expanding at a CAGR of 15.02% between 2026 and 2033. The market is being accelerated by the rapid expansion of utility-scale solar installations, increasing deployment of waterless robotic cleaning systems, and growing focus on maximizing photovoltaic output, where panel contamination can reduce energy generation by 15–30% in high-dust environments. Between 2024 and 2026, global energy transition policies, localization of solar supply chains, and large-scale renewable infrastructure investments have intensified demand for advanced maintenance technologies across mature and emerging solar markets.

China remains the dominant country in the global Solar Panel Cleaning Tool Market, accounting for approximately 38.4% of total installed solar capacity worldwide. The country added more than 270 GW of new solar capacity in a single year, operates extensive desert-based solar projects, and continues investing heavily in automated cleaning technologies to maintain performance efficiency. Compared with most developed markets, Chinese utility-scale projects deploy robotic cleaning solutions at nearly 2.5 times higher rates due to larger plant sizes and labor optimization requirements. More than 65% of newly commissioned large-scale solar facilities incorporate automated or semi-automated cleaning systems, supported by domestic manufacturing ecosystems and strong renewable energy targets.

As solar assets become larger, more geographically dispersed, and increasingly performance-driven, cleaning tool manufacturers that prioritize automation, water conservation, and operational efficiency are securing stronger competitive positioning across global energy infrastructure projects.

Market Size & Growth: USD 815.1 million in 2025 reaching USD 2,496.9 million by 2033 at 15.02% CAGR, driven by utility-scale solar expansion and robotic cleaning adoption.

Top Growth Drivers: Automated cleaning deployment (+42%), utility-scale solar expansion (+36%), and water-saving technologies (+31%) are accelerating demand.

Short-Term Forecast: By 2028, cleaning-related maintenance costs are projected to decline by 18% while panel efficiency recovery improves by 22%.

Emerging Technologies: AI-guided navigation, autonomous robotic cleaners, and waterless brush systems are improving cleaning productivity by over 25%.

Regional Leaders: Asia-Pacific (~USD 1,020 million), North America (~USD 620 million), and Europe (~USD 510 million) benefit from solar fleet expansion and automation adoption.

Consumer/End-User Trends: More than 58% of utility-scale operators now prioritize automated cleaning over manual methods to reduce operational downtime.

Pilot/Case Example: In 2025, a desert solar project achieved 27% higher energy yield and reduced water consumption by 90% using robotic cleaning systems.

Competitive Landscape: Top manufacturers collectively control nearly 46% market share, with innovation concentrated among specialized automation providers.

Regulatory & ESG Impact: Water-conservation initiatives have increased adoption of dry-cleaning technologies by over 34% across arid solar regions.

Investment & Funding: More than USD 1.2 billion has been directed toward solar maintenance automation, partnerships, and smart infrastructure deployment.

Innovation & Future Outlook: Sensor-enabled predictive cleaning and AI-driven maintenance scheduling are redefining high-performance solar asset management.

Utility-scale solar farms contribute approximately 52% of total demand, followed by commercial installations at 29% and residential deployments at 19%. Demand is increasingly shifting toward autonomous and water-efficient cleaning technologies as operators prioritize asset optimization and operational consistency. Automated systems improve cleaning productivity by over 25% while reducing water consumption by up to 90% in arid environments. Asia-Pacific remains the largest demand center, while North America is witnessing faster adoption of intelligent maintenance platforms. Ongoing supply chain localization and sustainability-driven procurement strategies are further influencing purchasing decisions, setting the stage for deeper strategic investments and competitive differentiation across the market.

The Solar Panel Cleaning Tool Market is rapidly transforming from a maintenance-support category into a critical operational optimization segment within the global renewable energy ecosystem. As solar developers, utilities, and asset managers increasingly focus on maximizing energy yield and minimizing lifecycle costs, cleaning efficiency has become a direct determinant of project profitability, asset utilization, and long-term competitiveness. Even modest soiling losses of 10–20% can materially affect electricity output, forcing operators to adopt more advanced and scalable cleaning solutions.

The market is also being reshaped by tightening water conservation requirements, labor shortages in remote solar locations, and the expansion of utility-scale solar facilities across desert and semi-arid regions. These pressures are accelerating investment into autonomous and intelligent cleaning technologies. Robotic cleaning systems improve efficiency by 35% while reducing operating costs by 28% compared to legacy manual cleaning systems, creating a compelling value proposition for large-scale operators.

Asia-Pacific leads in deployment volume due to massive solar infrastructure expansion, while North America leads in automation adoption, with nearly 61% of newly commissioned utility-scale projects integrating intelligent cleaning technologies. Over the next two to three years, automated cleaning penetration is expected to exceed 55% of new large-scale solar installations, significantly improving operational consistency and reducing maintenance-related downtime. ESG performance is emerging as a competitive advantage, particularly where waterless cleaning technologies reduce water consumption by up to 90%, supporting regulatory compliance and sustainability targets. In a recent utility-scale deployment, automated robotic cleaning improved panel output by 24% while reducing maintenance labor requirements by 32%.

Leading manufacturers and solar service providers are increasingly shifting capital allocation toward AI-enabled maintenance platforms, robotic fleets, and predictive cleaning analytics. Strategic partnerships between solar developers and automation providers are accelerating, optimizing asset performance while lowering operational risk. Companies that successfully integrate automation, sustainability, and data-driven maintenance capabilities will secure stronger competitive advantage as the global solar infrastructure landscape continues accelerating, shifting, transforming, and optimizing toward higher-performance energy generation systems.

The Solar Panel Cleaning Tool Market is evolving alongside the rapid expansion of global solar infrastructure and increasing pressure to maximize photovoltaic performance. As solar assets scale across utility, commercial, and industrial environments, cleaning efficiency is becoming a critical operational parameter rather than a routine maintenance activity. Dust accumulation, pollen, industrial pollutants, and environmental debris can reduce solar output by 10–30%, forcing operators to adopt more advanced cleaning technologies. Automation, robotics, and water-efficient cleaning systems are redefining maintenance practices across large-scale installations. Simultaneously, labor shortages, sustainability requirements, and performance-based asset management models are influencing procurement decisions. Market participants are responding through technology innovation, strategic partnerships, and expanded manufacturing capacity. The result is a market increasingly shaped by performance optimization, operational efficiency, and sustainability-driven infrastructure investments.

The strongest growth driver is the rapid expansion of utility-scale solar projects combined with increasing focus on performance optimization. In high-dust regions, solar soiling losses can exceed 25%, directly impacting project economics and energy generation targets. More than 58% of large-scale solar operators now evaluate cleaning technology based on lifecycle efficiency rather than upfront cost alone. Simultaneously, robotic cleaning systems can reduce labor requirements by approximately 40% while improving cleaning frequency by over 30%. Global solar deployment acceleration, particularly across Asia and the Middle East, is creating sustained demand for scalable maintenance infrastructure. As solar farms become larger and geographically dispersed, manual cleaning approaches are becoming operationally inefficient. In response, companies are expanding robotic production capacity, increasing R&D spending, and establishing technology partnerships to deliver autonomous, predictive, and water-efficient cleaning solutions capable of supporting next-generation solar asset portfolios.

Despite strong demand fundamentals, adoption remains constrained by capital expenditure requirements, technology integration complexity, and operational variability across project types. Automated cleaning systems can require 20–35% higher initial investment compared with conventional manual alternatives, creating purchasing hesitation among smaller operators. Furthermore, approximately 30% of existing solar installations were not originally designed for robotic cleaning integration, increasing retrofit complexity. Supply concentration for specialized motors, sensors, and control components continues to expose manufacturers to procurement risks and pricing volatility. These challenges can delay deployment schedules and increase implementation costs. To mitigate exposure, manufacturers are diversifying supplier networks, entering long-term procurement agreements, and developing modular systems that reduce retrofit requirements. Companies are also introducing flexible financing models and service-based contracts to lower adoption barriers and improve accessibility for smaller solar asset operators.

The largest opportunity lies in combining autonomous robotics, predictive analytics, and waterless cleaning technologies into integrated maintenance ecosystems. Waterless cleaning systems can reduce resource consumption by up to 90%, creating a significant advantage in regions facing water scarcity. AI-enabled maintenance platforms improve cleaning scheduling accuracy by nearly 35%, helping operators maximize panel performance while minimizing operational interventions. Emerging solar markets across Africa, Southeast Asia, and Latin America are expanding solar infrastructure at rates exceeding 20% annually, creating new demand pockets for advanced cleaning technologies. Companies are increasingly positioning for long-term dominance through robotics R&D, software integration, and ecosystem partnerships. A particularly important opportunity is the shift toward predictive maintenance models where cleaning occurs based on real-time performance data rather than fixed schedules, creating measurable efficiency gains and differentiated service offerings.

One of the most significant challenges is maintaining consistent cleaning performance across varying climates, panel configurations, and environmental conditions. Dust composition, humidity levels, panel tilt angles, and site accessibility can influence cleaning effectiveness by more than 20%. In some regions, maintenance budgets remain constrained despite increasing solar capacity, limiting adoption of advanced solutions. Infrastructure limitations and workforce skill gaps further complicate large-scale deployment. Additionally, operators increasingly demand measurable performance outcomes rather than equipment sales alone, forcing manufacturers to demonstrate long-term value. To remain competitive, companies must invest in adaptable technologies, performance analytics, and strategic service partnerships. Solving scalability, reliability, and performance verification challenges will be essential for sustaining market momentum and ensuring consistent operational outcomes across expanding global solar infrastructure networks.

34% Rise in Waterless Cleaning Deployment Across Utility Projects Waterless cleaning systems are reshaping maintenance operations as solar operators reduce resource consumption and operational complexity. Adoption has increased by 34% over the past two years, while water usage per cleaning cycle has fallen by as much as 90%. Companies are scaling dry-brush and electrostatic technologies to address water scarcity concerns. The shift is improving sustainability metrics and reducing recurring maintenance costs, particularly in desert-based solar facilities.

61% of New Utility Installations Integrate Robotic Cleaning Platforms Automation is redefining field operations as robotic cleaning deployment accelerates across large-scale solar farms. More than 61% of newly commissioned utility projects now incorporate robotic cleaning technologies, increasing cleaning frequency by nearly 30% and reducing labor dependency by over 40%. Companies are expanding robotic fleets and integrating predictive software to optimize maintenance execution while improving asset performance consistency.

27% Increase in AI-Driven Maintenance Scheduling Adoption AI-enabled monitoring platforms are shifting maintenance from calendar-based activity to performance-based execution. Operators using predictive cleaning analytics report approximately 27% better scheduling accuracy and nearly 18% lower operational downtime. Companies are restructuring maintenance workflows around real-time performance monitoring, improving productivity while responding to stricter operational efficiency requirements and evolving asset management expectations.

22% Growth in Regional Manufacturing Localization Initiatives Supply chain diversification is forcing manufacturers to localize production and sourcing strategies. Regional manufacturing investments have increased by 22%, reducing component lead times by nearly 15% and improving delivery reliability. A less obvious outcome is enhanced customization capability for local environmental conditions. Companies are forming strategic partnerships and expanding assembly operations to improve responsiveness while mitigating global supply chain disruptions.

The Solar Panel Cleaning Tool Market is segmented by type, application, and end-user, reflecting diverse operational requirements across the solar value chain. Demand remains concentrated in automated and semi-automated solutions as operators prioritize efficiency, labor optimization, and performance consistency. Utility-scale deployments account for a significant portion of market consumption, while commercial and industrial applications are gaining traction due to rising asset management requirements. Approximately 58% of demand originates from large-scale installations where cleaning frequency directly influences energy output and operational profitability. Demand is increasingly shifting toward intelligent, water-efficient technologies that support sustainability objectives and lower maintenance costs. For decision-makers, understanding how adoption patterns differ across product categories, usage environments, and customer groups is becoming essential for capturing emerging growth opportunities and aligning investment strategies with evolving market requirements.

The Solar Panel Cleaning Tool Market is segmented into Manual Cleaning Tools, Semi-Automatic Cleaning Tools, Robotic Cleaning Systems, Water-Based Cleaning Systems, and Dry Cleaning Systems. Robotic Cleaning Systems dominate the market with approximately 36.8% share, driven by their ability to deliver consistent cleaning performance across utility-scale solar installations while significantly reducing labor dependency. Their scalability advantage has become increasingly important as solar farm sizes expand and operators prioritize performance optimization. Meanwhile, Dry Cleaning Systems represent the fastest-growing segment, recording adoption growth of approximately 19.4%, fueled by rising water conservation requirements and increasing deployment across arid regions in the Middle East, North Africa, and Western United States. A clear market shift is emerging between traditional Water-Based Cleaning Systems and next-generation Dry Cleaning Systems. While Water-Based Cleaning Systems continue serving established installations due to familiarity and lower upfront implementation complexity, dry technologies are gaining traction because they can reduce water usage by up to 90%. Semi-Automatic and Manual Cleaning Tools collectively account for nearly 31.5% of market demand, maintaining strategic relevance in small-scale commercial and residential applications where automation economics are less compelling. Manufacturers are responding by expanding robotic production capacity, integrating AI-based navigation capabilities, and developing hybrid cleaning platforms that combine dry-cleaning efficiency with automated operation. The strongest investment opportunities remain concentrated in robotic and water-efficient technologies where long-term operational advantages are increasingly influencing purchasing decisions.

The Solar Panel Cleaning Tool Market serves Utility-Scale Solar Farms, Commercial Solar Installations, Industrial Solar Installations, and Residential Solar Installations. Utility-Scale Solar Farms remain the leading application segment, accounting for approximately 52.4% of total demand due to the extensive maintenance requirements associated with large photovoltaic assets. Cleaning frequency directly impacts energy generation performance, making advanced cleaning tools operationally essential for large-scale solar operators. Industrial Solar Installations represent the fastest-growing application segment, expanding at an estimated 18.1% adoption rate as manufacturers, logistics operators, and industrial facilities increasingly deploy onsite renewable energy infrastructure. Compared with Residential Solar Installations, industrial users place greater emphasis on operational efficiency, performance monitoring, and lifecycle optimization. Commercial Solar Installations and Residential Solar Installations collectively contribute approximately 38.6% of market demand, supported by rising awareness regarding performance degradation caused by dust accumulation and environmental contaminants. Usage patterns are evolving from periodic maintenance toward data-driven cleaning schedules based on panel performance monitoring. Companies are adapting through service-based business models, automated cleaning subscriptions, and integrated maintenance solutions. Demand is increasingly shifting toward applications where operational uptime and performance optimization directly influence energy economics, creating strong opportunities for advanced cleaning technology providers.

The Solar Panel Cleaning Tool Market is categorized into Solar Farm Operators, Commercial Building Owners, Industrial Enterprises, Residential Consumers, and Solar Maintenance Service Providers. Solar Farm Operators hold the largest market share at approximately 47.3%, reflecting their reliance on high-frequency cleaning activities to maximize electricity generation and protect asset performance. The scale of utility solar projects creates continuous demand for advanced cleaning technologies capable of supporting large deployment footprints. Solar Maintenance Service Providers are emerging as the fastest-growing end-user segment, with adoption increasing by nearly 20.2% as outsourced maintenance models gain acceptance across both mature and emerging solar markets. Compared with Residential Consumers, service providers prioritize automation, operational scalability, and performance guarantees, driving stronger demand for robotic and intelligent cleaning platforms. Commercial Building Owners, Industrial Enterprises, and Residential Consumers collectively account for approximately 52.7% of market demand, supported by increasing awareness of solar asset optimization and maintenance efficiency. Buying behavior is becoming increasingly performance-driven. Large operators prioritize lifecycle cost reduction and operational reliability, while smaller users focus on affordability and ease of deployment. Manufacturers are responding through tiered pricing structures, service partnerships, and customized product portfolios. Future demand is expected to shift toward professionalized maintenance ecosystems where cleaning performance becomes an integral component of solar asset management strategies.

Asia-Pacific accounted for the largest market share at 41.2% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 17.1% between 2026 and 2033.

Market demand remains concentrated in North America due to extensive utility-scale solar deployments, advanced maintenance practices, and strong adoption of automated cleaning technologies. Europe follows with 20.4% market share, supported by sustainability-driven solar asset optimization and regulatory emphasis on renewable energy performance. Asia-Pacific accounts for approximately 41.2% of demand and is rapidly accelerating due to expanding solar capacity additions across China, India, and Southeast Asia. South America contributes 6.3%, while the Middle East & Africa represent 5.3%, driven by desert-based solar developments and increasing infrastructure investments. Supply chain localization, water conservation initiatives, and large-scale renewable energy programs are reshaping regional competition. Globally, companies are increasingly prioritizing Asia-Pacific expansion while maintaining innovation leadership and premium technology deployment across North America and Europe.

North America commands approximately 26.8% of global market demand, supported by extensive utility-scale solar installations across the United States and growing renewable infrastructure investments. Solar operators increasingly prioritize automated cleaning technologies as performance losses from panel contamination can exceed 20% in high-exposure environments. A significant structural force is the continued expansion of utility-scale renewable projects alongside stricter operational efficiency targets. More than 61% of newly commissioned large solar facilities now evaluate robotic cleaning solutions during project planning stages. Enterprise buyers increasingly favor lifecycle cost reduction and predictive maintenance capabilities over traditional labor-intensive approaches. Companies continue expanding service networks and deploying AI-integrated cleaning systems, making the region a strategic priority for advanced technology commercialization and premium product adoption.

Europe represents approximately 20.4% of global market demand, with Germany, Spain, Italy, and France serving as key adoption centers. Sustainability mandates and renewable energy performance targets continue driving investment into efficient maintenance technologies. Water conservation objectives have accelerated adoption of dry-cleaning systems, which reduce water consumption by up to 90% while supporting ESG compliance goals. Nearly 54% of large commercial solar operators prioritize environmental performance metrics when evaluating maintenance technologies. Enterprises increasingly favor automated solutions that improve operational transparency and support sustainability reporting requirements. Companies are responding through eco-efficient product development and service innovation. The region remains strategically important because regulatory expectations consistently force technology adaptation, operational optimization, and continuous innovation.

Asia-Pacific accounts for approximately 41.2% of global market demand and ranks as the fastest-expanding regional market. China, India, Japan, and Australia are leading adoption due to massive solar infrastructure expansion and growing energy security priorities. The region benefits from strong manufacturing capabilities, competitive production economics, and localized supply chains. More than 45% of global solar installations are concentrated within key Asia-Pacific markets, creating substantial maintenance requirements. Automated cleaning deployment has increased by nearly 28% across large-scale projects as operators seek improved efficiency and reduced labor costs. Enterprises prioritize scale, speed, and operational consistency, encouraging suppliers to localize production and expand service networks. The region remains critical for companies seeking volume growth, manufacturing scale, and long-term market expansion.

South America contributes approximately 6.3% of global market demand, with Brazil and Chile representing the primary growth centers. Utility-scale solar development and increasing industrial renewable adoption continue supporting market expansion. However, infrastructure limitations and financing constraints remain important structural challenges for technology deployment. Adoption of automated cleaning systems has increased by nearly 17%, particularly within large commercial and utility projects where performance optimization directly influences energy output. Enterprises remain highly cost-conscious and frequently prioritize affordability alongside operational effectiveness. Companies are responding through localized partnerships, flexible service offerings, and targeted deployment strategies. The region presents a compelling balance of growth opportunity and execution risk, making selective market expansion increasingly attractive.

The Middle East & Africa account for approximately 5.3% of global market demand yet represent one of the most strategically important markets for advanced cleaning technologies. Saudi Arabia, the United Arab Emirates, and South Africa are driving regional demand through large-scale renewable energy investments and infrastructure modernization initiatives. Desert environments can reduce solar performance by more than 25% without effective cleaning practices, accelerating adoption of robotic and dry-cleaning solutions. Waterless cleaning technologies have recorded adoption growth exceeding 30% across major solar developments. Enterprises increasingly prioritize efficiency, resource conservation, and operational resilience. Companies are expanding regional partnerships and technology deployment programs, positioning the region as a high-value market for long-term infrastructure-driven growth.

China – 38.4% Market share: Supported by the world's largest solar installation base, extensive utility-scale projects, and strong adoption of automated cleaning technologies.

United States – 18.7% Market share: Driven by large-scale renewable energy investments, advanced maintenance practices, and rapid deployment of robotic cleaning solutions.

The Solar Panel Cleaning Tool Market is characterized by competition between technology-focused robotic specialists such as Ecoppia, Airtouch Solar, and SolarCleano versus regional equipment suppliers and traditional cleaning tool manufacturers competing primarily on price and distribution reach. The top five players collectively account for approximately 44–48% of global market activity, reflecting a moderately concentrated structure where innovation leadership carries significant competitive weight.

Competition is increasingly based on automation capability, water efficiency, deployment speed, and lifecycle operating costs rather than equipment pricing alone. Robotic systems can reduce labor requirements by over 40%, while waterless technologies lower water consumption by up to 90% and improve maintenance efficiency by nearly 25%. As a result, companies are aggressively investing in AI-enabled navigation, predictive maintenance platforms, and autonomous cleaning fleets.

Leading players are strengthening their positions through utility-scale project partnerships, geographic expansion, localized manufacturing, and vertically integrated service models. The current competitive shift favors automation providers as large solar operators increasingly prioritize performance optimization and resource conservation. High product development costs, technology validation requirements, and long procurement cycles create substantial barriers to entry. Winning in this market requires demonstrable efficiency gains, scalable automation capabilities, and strong relationships with utility-scale solar asset owners.

Airtouch Solar

SolarCleano

Kärcher

Saint-Gobain Solar Cleaning Solutions

Nomadd Desert Solar Solutions

Serbot AG

Sol-Bright Technology

Washpanel Group

RST Cleantech Solutions

SunBrush Mobil

IPC Eagle

Automation is becoming the defining technology layer across the Solar Panel Cleaning Tool Market. Autonomous robotic cleaning systems are now deployed across approximately 45% of newly commissioned utility-scale solar projects, particularly in desert and high-soiling environments. These systems reduce manual intervention by over 40% while increasing cleaning frequency by nearly 30%, enabling operators to maintain more consistent energy generation performance. Companies with strong robotics portfolios are securing strategic advantages in large-scale infrastructure projects where operational efficiency directly impacts asset profitability.

Waterless cleaning technology is emerging as another critical innovation category. Advanced microfiber brushes, electrostatic cleaning mechanisms, and air-assisted systems can reduce water consumption by up to 90% while maintaining cleaning effectiveness comparable to traditional methods. Compared with conventional water-based cleaning processes, modern waterless robotic platforms improve maintenance efficiency by approximately 25% while significantly lowering resource dependency. These advantages are particularly important across the Middle East, North Africa, Australia, and other water-constrained solar markets.

Artificial intelligence and predictive maintenance platforms are increasingly integrated with cleaning systems. AI-driven monitoring tools improve cleaning schedule accuracy by approximately 27% by identifying soiling patterns, weather conditions, and panel performance deviations. More than 35% of large solar operators are evaluating predictive cleaning frameworks as part of broader digital asset management strategies.

Between 2026 and 2028, cloud-connected cleaning fleets, autonomous navigation, and real-time performance analytics are expected to redefine competitive positioning. Companies that combine robotics, software intelligence, and sustainability-focused technologies will capture disproportionate value as solar operators increasingly transition toward performance-based maintenance ecosystems.

February 2024 – Airtouch Solar secured a partnership with Vena Energy to deploy water-free robotic cleaning systems at a 48 MW solar facility in India. The deployment expanded Airtouch's presence in Asia-Pacific while supporting higher energy yield through automated cleaning operations. [Waterless Expansion] Source: www.pv-magazine-india.co

April 2024 – Airtouch Solar signed a US$6 million contract with Adani Green Energy for deployment of AT 4.1 robotic cleaning systems. The project is expected to save approximately 50 million liters of water annually while improving maintenance efficiency across utility-scale solar assets. [Mega Contract Win]

June 2025 – Sol-Bright showcased its next-generation fully automated robotic cleaning system at SNEC 2025 in Shanghai, highlighting intelligent waterless operation and expanded global partnership initiatives. The launch strengthened competitive positioning in advanced solar maintenance automation. [Automation Showcase]

September 2025 – SolarCleano launched the L1 semi-automatic cleaning platform featuring a cleaning capacity of 2,000 m² per hour and operating speeds of up to 40 meters per minute. The solution targets large-scale photovoltaic projects requiring faster maintenance execution. [High-Speed Launch]

The Solar Panel Cleaning Tool Market Report delivers comprehensive coverage across the full value chain of solar maintenance technologies. The study evaluates major product categories including manual cleaning tools, semi-automatic systems, robotic cleaning solutions, water-based technologies, and dry-cleaning systems. It further analyzes demand across utility-scale solar farms, commercial installations, industrial facilities, and residential deployments while assessing purchasing behavior among solar farm operators, maintenance service providers, commercial asset owners, and industrial enterprises. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed regional and country-level insights.

The report examines more than 15 key market indicators, including adoption trends, technology penetration rates, competitive positioning, demand concentration patterns, and regional deployment dynamics. Approximately 52% of market demand is concentrated within utility-scale applications, while automated and robotic solutions account for an increasing share of advanced maintenance deployments. The analysis also covers emerging technologies such as AI-enabled cleaning platforms, predictive maintenance systems, waterless cleaning solutions, and cloud-connected robotic fleets.

From a strategic perspective, the report supports investment evaluation, market entry planning, product development, geographic expansion, and competitive benchmarking. Special attention is given to high-growth technology segments, sustainability-driven adoption patterns, and evolving maintenance models expected to influence industry direction between 2026 and 2033. The resulting framework enables decision-makers to identify scalable opportunities, prioritize innovation investments, and strengthen competitive positioning in a rapidly evolving solar infrastructure environment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 815.1 Million |

| Market Revenue (2033) | USD 2,496.9 Million |

| CAGR (2026–2033) | 15.02% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ecoppia; Airtouch Solar; SolarCleano; Kärcher; Saint-Gobain Solar Cleaning Solutions; Nomadd Desert Solar Solutions; Serbot AG; Sol-Bright Technology; Washpanel Group; RST Cleantech Solutions; SunBrush Mobil; IPC Eagle |

| Customization & Pricing | Available on Request (10% Customization Free) |