Reports

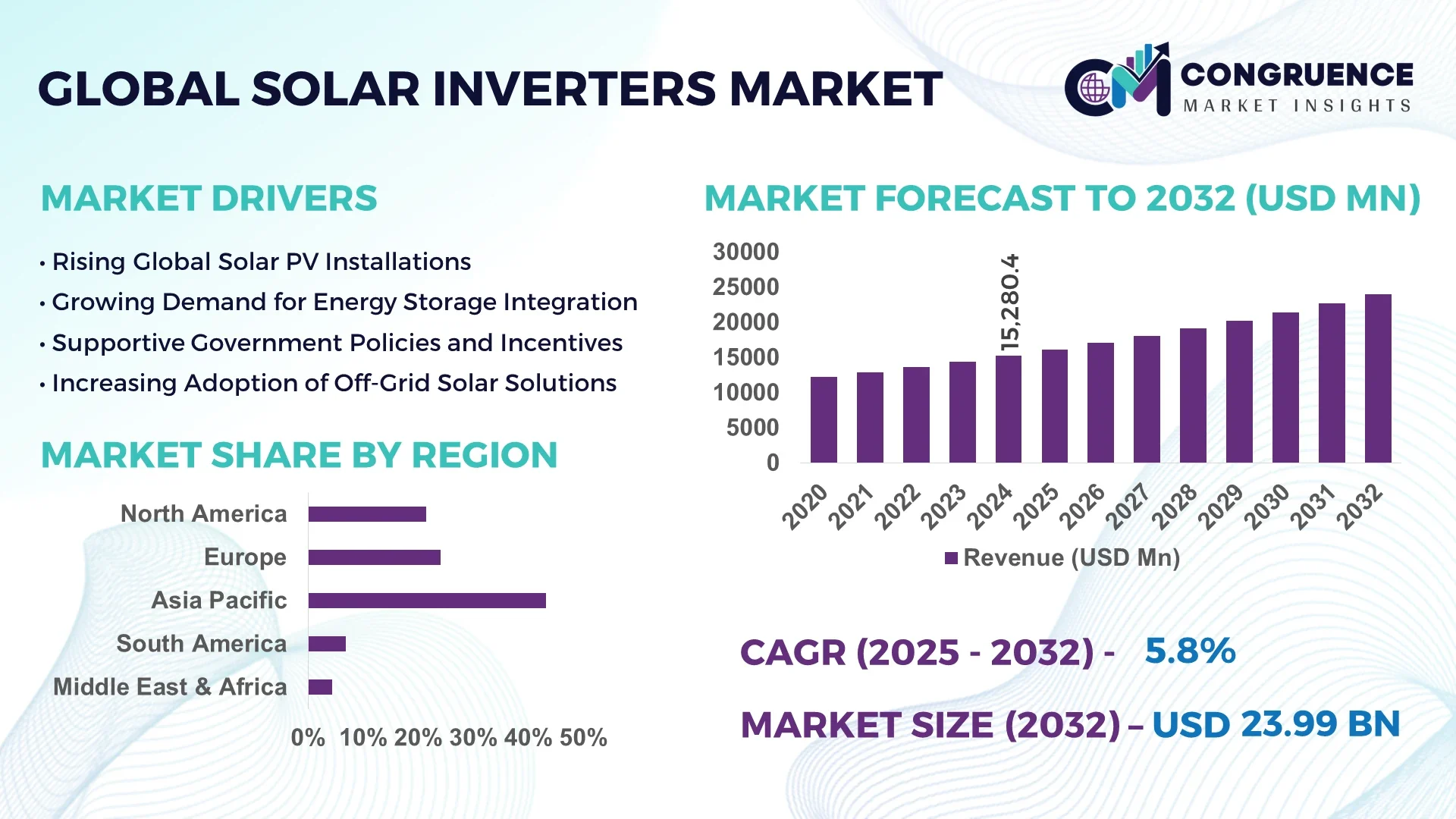

The Global Solar Inverters Market was valued at USD 15,280.4 Million in 2024 and is anticipated to reach a value of USD 23,989.4 Million by 2032 expanding at a CAGR of 5.8% between 2025 and 2032.

China continues to dominate the Solar Inverters market with extensive manufacturing capabilities, advanced production infrastructure, and high levels of investment in smart grid integration and renewable power infrastructure across both utility-scale and distributed energy projects.

The Solar Inverters Market is undergoing significant transformation driven by rising demand across residential, commercial, and utility-scale applications. Rapid advancements in hybrid and string inverter technologies, coupled with the integration of digital monitoring systems, are reshaping operational performance. Governments across Asia-Pacific, Europe, and North America are pushing strong regulatory frameworks to accelerate renewable deployment, creating demand for efficient inverters that can meet grid stability requirements. Additionally, the integration of Internet of Things (IoT)-enabled inverters is enabling remote monitoring, predictive maintenance, and performance optimization. Environmental sustainability mandates, combined with falling solar installation costs, are further expanding adoption. Emerging trends such as hybrid inverters for energy storage integration and AI-enabled optimization are expected to play a central role in shaping the future outlook of the Solar Inverters Market.

Artificial intelligence is transforming the Solar Inverters Market by optimizing performance, improving predictive maintenance, and enhancing real-time energy management. AI-enabled inverters are equipped with machine learning algorithms that forecast load demands, balance grid fluctuations, and identify faults before they occur. For utility-scale installations, this reduces downtime and ensures higher efficiency in energy transmission. Advanced AI systems are also enabling adaptive power conversion, allowing inverters to adjust dynamically to changing solar irradiance levels and varying energy consumption patterns.

In residential and commercial sectors, AI-driven monitoring platforms provide actionable insights into energy usage, reducing losses and enhancing consumer energy savings. Manufacturers are embedding AI into digital twins of inverters, simulating real-world operations for better asset management. AI integration is also playing a key role in distributed generation systems, ensuring seamless connectivity between rooftop solar units and smart grids. As demand for flexible, efficient, and reliable renewable energy solutions grows, AI is set to become a cornerstone technology in inverter development, influencing design strategies, regulatory compliance, and long-term market competitiveness in the Solar Inverters Market.

“In March 2024, Huawei introduced an AI-powered smart inverter system capable of increasing energy yield by 2–3% through advanced string-level monitoring and real-time optimization algorithms, reducing operational losses in utility-scale solar projects.”

The Solar Inverters Market is driven by the global shift toward renewable energy, rapid technological innovation, and government-backed clean energy initiatives. Expanding solar installations across utility, residential, and commercial segments continue to create strong demand for advanced inverter solutions. Innovations such as hybrid inverters for solar-plus-storage systems, IoT-enabled monitoring platforms, and AI-driven predictive analytics are reshaping operational efficiency. At the same time, grid integration challenges, component standardization, and fluctuating raw material costs are influencing manufacturer strategies. While supportive policies and subsidies drive adoption, competition among global and regional players is intensifying, making technological differentiation and service innovation essential to sustain growth.

The rapid expansion of utility-scale solar farms is a major driver for the Solar Inverters Market. Countries in Asia-Pacific, Europe, and North America are investing in large solar parks to reduce carbon emissions and meet renewable energy targets. Advanced central inverters are in high demand due to their capacity to handle megawatt-scale projects with grid synchronization features. The development of smart grids is also amplifying demand for highly efficient, AI-enabled inverters that improve energy conversion rates. This large-scale deployment is pushing inverter manufacturers to innovate with higher efficiency ratings and grid support functions to meet the rising global demand.

One of the major restraints in the Solar Inverters Market is the increasing complexity of grid integration. As renewable penetration rises, maintaining grid stability becomes challenging, requiring inverters with advanced features such as reactive power control, frequency regulation, and real-time communication with grid operators. These requirements increase design costs and demand high investment in R&D. Smaller manufacturers often struggle to meet stringent compliance standards across multiple regions, which limits their competitive positioning. Additionally, inconsistent policies across countries add another layer of complexity, restricting seamless adoption and creating cost burdens for manufacturers and project developers.

The integration of solar power with energy storage solutions presents a strong opportunity for the Solar Inverters Market. Hybrid inverters that combine photovoltaic conversion with battery management are gaining traction in both developed and emerging economies. With rising electricity demand and increasing focus on energy independence, residential and commercial sectors are adopting storage-enabled inverters for backup power and peak load management. This trend is also accelerating in utility-scale applications where hybrid systems improve grid reliability and flexibility. The growth of electric vehicles and demand for decentralized energy systems further enhances opportunities for hybrid inverters with smart control features.

The Solar Inverters Market faces challenges from high upfront costs and intense price competition among global and regional players. Although technological advancements are improving efficiency, inverter systems require significant capital investment, especially in hybrid and AI-enabled models. Manufacturers in countries with high production capacities, such as China, often engage in aggressive pricing strategies, squeezing margins for competitors in Europe and North America. Additionally, the need for after-sales services, warranty provisions, and component replacements adds to overall costs. These challenges make it difficult for small and medium enterprises to scale and maintain profitability in a highly competitive landscape.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Solar Inverters Market. Pre-bent and cut elements are prefabricated off-site using automated systems, reducing labor intensity and accelerating solar farm installations. This is particularly evident in Europe and North America, where project efficiency is a top priority.

• Growth of Hybrid and Storage-Integrated Inverters: The increasing adoption of solar-plus-storage systems is driving demand for hybrid inverters. These devices manage both photovoltaic conversion and battery storage, enabling higher reliability and energy independence for residential, commercial, and utility-scale users.

• Digitalization and IoT-Enabled Monitoring: The Solar Inverters Market is witnessing a surge in demand for IoT-enabled monitoring platforms. Remote performance tracking, real-time fault detection, and predictive maintenance capabilities are helping operators reduce downtime and optimize energy output across multiple installations.

• Rising Adoption of High-Efficiency String Inverters: String inverters are becoming increasingly popular in distributed solar systems due to their modular design, flexibility, and ease of maintenance. Their deployment is rising across residential and small commercial projects, particularly in Asia-Pacific, where rooftop solar installations are scaling rapidly.

The Solar Inverters Market is segmented by type, application, and end-user, each playing a crucial role in shaping industry dynamics. Types of inverters include central, string, micro, and hybrid inverters, each catering to specific project sizes and operational requirements. Applications span residential, commercial, and utility-scale projects, with varied demand drivers and installation preferences. End-user adoption is influenced by factors such as cost-effectiveness, grid integration needs, and energy storage compatibility. While utility-scale projects dominate demand, rapid uptake in residential and commercial segments is diversifying the market landscape. These insights highlight how segmentation provides clarity for strategic planning, product innovation, and regional expansion within the Solar Inverters Market.

Central inverters continue to lead the Solar Inverters Market, particularly for utility-scale projects requiring high-capacity solutions and advanced grid synchronization. Their ability to handle large-scale energy conversion makes them indispensable for solar farms exceeding megawatt capacities. String inverters, however, are the fastest-growing type due to their modular nature, flexibility, and cost-effectiveness, especially in residential and commercial installations. Micro inverters also play a significant role, offering panel-level optimization and better energy yields, though they remain niche in larger projects. Hybrid inverters, which integrate photovoltaic systems with energy storage, are gaining strong momentum as solar-plus-storage adoption expands worldwide. Together, these types reflect a balanced mix of established demand and emerging growth opportunities.

Utility-scale projects dominate the Solar Inverters Market, driven by global investments in solar parks and renewable infrastructure. Central inverters are particularly critical in this segment, providing grid support and handling high-power outputs. Residential applications, however, are rapidly expanding with the growth of rooftop solar installations and government incentives promoting clean energy adoption. Commercial and industrial applications are also growing, supported by cost-saving benefits and the integration of storage-enabled inverters. Emerging off-grid applications in remote areas are creating new opportunities for hybrid and micro inverters, further diversifying the landscape. This mix of applications highlights both steady utility demand and rising distributed generation trends.

Utilities are the leading end-users in the Solar Inverters Market, driven by large-scale solar farm deployments and grid-connected projects worldwide. Their demand for central inverters with high efficiency and grid support features solidifies their market position. The fastest-growing end-user segment is residential consumers, propelled by rooftop solar adoption, energy independence goals, and government subsidies that make installations more affordable. Commercial and industrial users also contribute significantly, investing in solar-plus-storage systems to reduce operational costs and meet sustainability targets. Rural communities and off-grid users represent niche but expanding markets, particularly in developing regions seeking energy access solutions.

Asia-Pacific accounted for the largest market share at 43.2% in 2024 however, Region Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

The Asia-Pacific region benefits from large-scale solar power installations in China, India, and Japan, combined with strong government incentives that support renewable adoption. Meanwhile, Middle Eastern countries are rapidly diversifying their energy portfolios beyond fossil fuels, driving investments into advanced solar infrastructure and grid integration technologies. This dynamic creates a dual-center of growth, where Asia-Pacific dominates by installed capacity while Middle East & Africa leads in speed of adoption.

Digital Grid Modernization Driving Utility Transformation

North America accounted for nearly 21.5% of the global solar inverters market in 2024, driven by utility-scale solar farms and the adoption of residential rooftop systems. Key industries fueling demand include commercial real estate, manufacturing, and urban housing. Regulatory support, such as federal tax credits and state-level renewable mandates, continues to encourage adoption. The U.S. has seen significant digital transformation trends, with AI-powered predictive analytics enhancing solar inverter performance and reducing downtime. Canada has also been advancing grid integration, making solar power a stable and scalable contributor to the region’s clean energy future.

Decentralized Solar Adoption Accelerating Grid Stability

Europe represented 24.1% of the global solar inverters market in 2024, with Germany, the UK, and France leading deployment. The region benefits from ambitious renewable energy targets, particularly under the EU’s Green Deal framework. Regulatory bodies have introduced strict efficiency and carbon neutrality standards, pushing manufacturers to integrate smart monitoring and digital twin technologies into solar inverters. Countries like Spain and Italy are increasing investments in decentralized rooftop solar, while advanced storage integration ensures greater grid reliability. These advancements position Europe as a hub for sustainable innovation in inverter technologies.

Massive Installations Fueling Renewable Expansion

Asia-Pacific held the dominant 43.2% share of the solar inverters market in 2024, with China, India, and Japan being the top consumers. China leads in both manufacturing and deployment, supported by significant government subsidies and global export capabilities. India’s expansion of large-scale solar parks and Japan’s investment in hybrid solar-storage systems highlight the region’s forward momentum. Infrastructure advancements, including high-voltage transmission and AI-integrated energy management platforms, are rapidly scaling operations. Innovation hubs across South Korea and Taiwan are further contributing by introducing high-efficiency semiconductor components tailored for solar inverter applications.

Government Incentives Enhancing Renewable Deployment

South America accounted for 6.8% of the global solar inverters market in 2024, with Brazil and Argentina leading adoption. Brazil’s booming renewable sector is supported by government incentives for clean energy auctions and large-scale solar farms. Argentina has focused on hybrid solar-grid projects, driving steady growth in inverter demand. Regional infrastructure development, such as grid modernization projects, ensures better solar energy integration. Local trade policies promoting solar component imports also create favorable conditions for expanding solar installations across residential and commercial segments, supporting gradual market expansion.

Diversification from Fossil Fuels Driving Growth

The Middle East & Africa accounted for 4.4% of the solar inverters market in 2024, with the UAE, Saudi Arabia, and South Africa leading demand. The UAE is prioritizing renewable diversification under long-term energy transition plans, while South Africa focuses on mitigating grid instability with decentralized solar adoption. Saudi Arabia’s mega-projects, such as NEOM, are incorporating high-efficiency inverters for large-scale deployment. Regulatory partnerships and cross-border energy trade agreements are accelerating investment in solar infrastructure, driving strong demand for advanced inverter technologies tailored for desert and high-temperature environments.

China – 29.4% share: Dominance driven by vast production capacity, strong domestic demand, and global exports of high-efficiency solar inverters.

Germany – 11.7% share: Leadership supported by advanced engineering, strong regulatory frameworks, and widespread adoption of residential and commercial solar systems.

The Solar Inverters market is highly competitive, with more than 45 active global and regional players offering diverse portfolios across utility-scale, commercial, and residential segments. Leading firms maintain strong positions through extensive R&D investments, patent filings, and strategic mergers. Recent trends indicate a rise in partnerships between inverter manufacturers and energy storage companies to deliver integrated solutions. Market players are actively pursuing AI-enabled monitoring systems, grid-compatibility upgrades, and modular designs to differentiate offerings. Competitive pressure has intensified in Asia-Pacific, where local firms challenge established European and North American brands with cost-effective products. Meanwhile, premium players emphasize sustainability, introducing inverters with recyclable components and reduced carbon footprints, catering to environmentally conscious customers.

Huawei Technologies Co., Ltd.

SMA Solar Technology AG

Sungrow Power Supply Co., Ltd.

FIMER S.p.A

Delta Electronics, Inc.

ABB Ltd.

Schneider Electric SE

TMEIC (Toshiba Mitsubishi-Electric Industrial Systems Corporation)

KACO New Energy GmbH

Ginlong Technologies Co., Ltd. (Solis)

Technological advancements are reshaping the Solar Inverters market, with efficiency, durability, and digital intelligence at the forefront. The introduction of hybrid inverters capable of managing both solar energy and battery storage is enhancing grid resilience. Manufacturers are now producing models that operate at conversion efficiencies exceeding 98%, reducing energy losses significantly. Wide bandgap semiconductors, such as silicon carbide (SiC) and gallium nitride (GaN), are increasingly integrated into inverter designs to support higher power density, reduced size, and lower thermal losses.

Artificial intelligence and IoT-based systems are driving predictive maintenance, enabling operators to identify inverter faults before they cause outages. Blockchain technology is also emerging as a means to facilitate peer-to-peer energy trading, allowing solar-equipped households to monetize excess power. Furthermore, digital twin technology is being applied for real-time simulation of inverter performance under varying conditions, offering operators advanced planning capabilities. With innovations in smart grids and energy storage, solar inverters are evolving beyond traditional power conversion devices to become central nodes of intelligent energy ecosystems.

In March 2024, Huawei launched its next-generation residential hybrid inverter series with integrated AI-driven energy management, enabling households to achieve up to 15% higher self-consumption efficiency compared to conventional models.

In May 2024, Sungrow introduced a 3.6 MW central inverter system optimized for ultra-large solar farms, featuring high-voltage ride-through capability to ensure grid stability during fluctuations.

In July 2023, SMA Solar Technology unveiled a commercial-scale inverter platform designed for modular scalability, allowing multiple units to operate seamlessly in parallel for large rooftop projects.

In December 2023, Delta Electronics expanded its solar inverter manufacturing facility in Taiwan, boosting annual production capacity by 25% to meet rising regional demand.

The scope of the Solar Inverters Market Report encompasses a comprehensive analysis of product types, applications, end-user industries, and geographic regions. It examines major categories such as string inverters, central inverters, and microinverters, along with their role in utility, commercial, and residential installations. The report evaluates regional markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in adoption trends, regulatory frameworks, and technological integration.

Applications analyzed include rooftop solar, utility-scale power plants, and hybrid solar-storage systems. The study further explores the impact of smart grid integration, digital transformation, and advancements in semiconductor materials on inverter performance. Key end-user insights span utilities, industrial sectors, commercial enterprises, and households, reflecting the broad scope of market influence. By capturing both established and emerging trends, the report provides stakeholders with a holistic view of market opportunities, challenges, and innovation pathways, making it a critical resource for decision-makers navigating the evolving renewable energy landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 15280.4 Million |

|

Market Revenue in 2032 |

USD 23989.4 Million |

|

CAGR (2025 - 2032) |

5.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Huawei Technologies Co., Ltd., SMA Solar Technology AG, Sungrow Power Supply Co., Ltd., FIMER S.p.A, Delta Electronics, Inc., ABB Ltd., Schneider Electric SE, TMEIC (Toshiba Mitsubishi-Electric Industrial Systems Corporation), KACO New Energy GmbH, Ginlong Technologies Co., Ltd. (Solis) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |