Reports

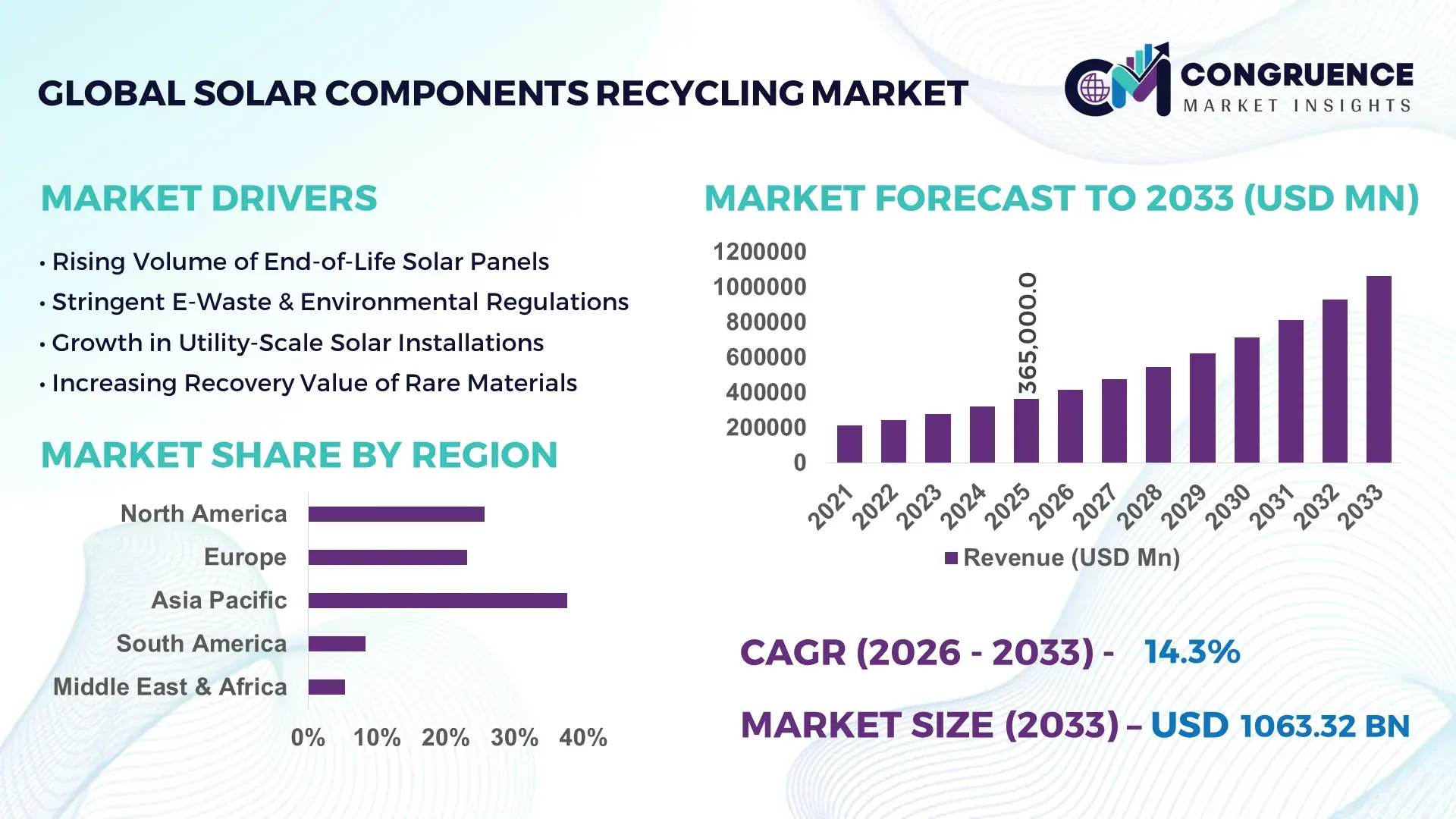

The Global Solar Components Recycling Market was valued at USD 365000 Million in 2025 and is anticipated to reach a value of USD 1063316 Million by 2033 expanding at a CAGR of 14.3% between 2026 and 2033. This growth is primarily driven by the accelerating retirement of early-generation photovoltaic (PV) systems and tightening environmental compliance mandates worldwide.

China dominates the Solar Components Recycling market with installed solar capacity exceeding 600 GW in 2025, creating a substantial pipeline of end-of-life panels. The country operates multiple large-scale recycling facilities with annual processing capacities above 100,000 metric tons each, supported by industrial clusters in Jiangsu and Zhejiang provinces. Investments in advanced thermal and chemical delamination technologies have improved material recovery rates to over 90% for glass and 95% for aluminum frames. Recovered silicon and silver are increasingly reintegrated into domestic photovoltaic manufacturing, serving utility-scale solar farms, distributed rooftop systems, and industrial energy storage projects.

Market Size & Growth: Valued at USD 365000 Million in 2025, projected to reach USD 1063316 Million by 2033 at 14.3% CAGR, fueled by large-scale PV decommissioning and circular economy mandates.

Top Growth Drivers: 35% rise in solar panel installations, 28% increase in regulatory compliance requirements, 22% improvement in material recovery efficiency.

Short-Term Forecast: By 2028, advanced recycling automation is expected to reduce processing costs by 18% and improve recovery yield by 12%.

Emerging Technologies: AI-enabled optical sorting, robotic panel dismantling, and chemical-free delamination techniques enhancing high-purity silicon recovery.

Regional Leaders: Asia-Pacific projected at USD 420000 Million by 2033 driven by utility-scale adoption; Europe at USD 310000 Million supported by strict WEEE directives; North America at USD 245000 Million with strong ESG integration.

Consumer/End-User Trends: Utility-scale solar operators account for over 45% of recycling demand, followed by commercial rooftop installations and residential solar aggregators.

Pilot or Case Example: In 2024, a European recycling pilot improved silver recovery efficiency by 15% while cutting processing downtime by 10%.

Competitive Landscape: First Solar holds approximately 18% share, followed by Veolia, Recycle PV Solar, Silcontel, and Trina Solar’s recycling division.

Regulatory & ESG Impact: Over 60% of OECD nations enforce mandatory PV waste recycling targets aligned with carbon neutrality frameworks.

Investment & Funding Patterns: More than USD 2.5 Billion invested globally in PV recycling infrastructure since 2023, including green bonds and climate-focused venture capital.

Innovation & Future Outlook: Closed-loop silicon recovery and integration with battery recycling ecosystems are shaping next-generation sustainable solar supply chains.

The Solar Components Recycling market serves key sectors including utility-scale solar farms contributing nearly 50% of recyclable volumes, commercial and industrial rooftops at approximately 30%, and residential systems covering the remainder. Technological advancements in high-temperature pyrolysis and automated material separation are increasing throughput efficiency by over 20% compared to legacy mechanical shredding. Regulatory frameworks promoting extended producer responsibility are reshaping procurement strategies, while regional consumption patterns in Asia-Pacific and Europe reflect strong alignment with decarbonization targets. Emerging trends such as circular PV manufacturing, digital waste tracking platforms, and integrated ESG reporting are reinforcing long-term market resilience and investment attractiveness.

The Solar Components Recycling Market holds strategic relevance within the global renewable energy value chain as photovoltaic waste is projected to exceed 80 million metric tons by 2050. As early-generation solar panels approach end-of-life, utilities and manufacturers are adopting structured recycling frameworks to recover high-value materials such as silver, silicon, aluminum, and copper. Advanced robotic dismantling delivers 25% higher material recovery efficiency compared to conventional mechanical shredding, while chemical delamination processes achieve over 95% glass purity compared to 80% under older thermal-only methods.

Asia-Pacific dominates in recycling volume due to its vast installed base, while Europe leads in adoption with over 70% of solar enterprises complying with formal recycling directives. By 2027, AI-enabled waste sorting systems are expected to cut operational costs by 15% and improve throughput by 20%, strengthening profit margins for recycling operators. Firms are committing to ESG metrics such as 50% recycled material integration into new modules by 2030, aligning with net-zero supply chain objectives.

In 2024, a German recycling initiative achieved a 30% reduction in landfill waste through automated silicon purification technology, setting a benchmark for circular PV manufacturing. Over the next two to three years, integration of digital traceability platforms and blockchain-based material tracking will further optimize compliance transparency. The Solar Components Recycling Market is emerging as a pillar of industrial resilience, regulatory compliance, and sustainable growth within the global clean energy ecosystem.

The exponential rise in global solar installations over the past decade has created a growing inventory of panels approaching 20–25 years of operational lifespan. By 2030, annual photovoltaic waste generation is expected to surpass 8 million metric tons. Utility-scale solar farms, which account for nearly half of installed capacity additions annually, contribute significantly to future recycling volumes. Regulatory mandates in Europe and parts of Asia require structured collection and treatment of decommissioned modules, increasing formal recycling rates above 75% in several countries. Additionally, improved recovery technologies extracting up to 95% of aluminum and 90% of glass are enhancing economic viability. These factors collectively drive demand for specialized solar components recycling infrastructure and advanced material recovery solutions.

Despite technological improvements, recycling photovoltaic modules remains capital-intensive. Advanced thermal and chemical separation systems require substantial upfront investment, often exceeding USD 20 million for mid-scale facilities. Silicon purification and silver extraction processes involve energy-intensive steps, increasing operational expenditures. Furthermore, heterogeneity in panel design—including variations in encapsulants, backsheet materials, and cell architectures—complicates standardized recycling. Transportation logistics for bulky modules add cost burdens, particularly in geographically dispersed markets. In emerging economies, informal disposal practices persist due to limited regulatory enforcement, reducing feedstock availability for formal recyclers. These financial and operational complexities continue to constrain faster expansion of the Solar Components Recycling Market.

The transition toward circular photovoltaic manufacturing presents significant opportunities for the Solar Components Recycling Market. Closed-loop silicon recovery systems can reduce reliance on virgin polysilicon by up to 20% in new module production. Growing demand for sustainable supply chains among utility developers and corporate renewable buyers is increasing procurement preference for modules with recycled content. Emerging markets in Latin America and Southeast Asia are expected to install over 150 GW of additional solar capacity by 2030, creating long-term recycling demand. Innovations such as low-temperature delamination and chemical-free separation are improving recovery efficiency while reducing environmental impact. Strategic collaborations between panel manufacturers and recycling specialists are unlocking vertically integrated business models that enhance long-term value creation.

Regulatory inconsistency across regions creates operational uncertainty for recycling firms. While the European Union enforces structured photovoltaic waste directives, several developing regions lack comprehensive policy frameworks, resulting in uneven collection systems. Differences in hazardous material classification, transportation requirements, and reporting standards complicate cross-border recycling operations. Compliance audits and environmental certifications increase administrative costs, particularly for small and medium-sized enterprises. Moreover, rapid technological evolution in panel design—such as bifacial modules and thin-film technologies—requires continuous adaptation of recycling processes. Balancing environmental compliance, cost efficiency, and technological upgrades remains a persistent challenge for stakeholders operating in the Solar Components Recycling Market.

• Over 40% Increase in Automated Panel Dismantling Facilities: Automation is transforming the Solar Components Recycling market, with more than 40% of new recycling plants commissioned in 2024 integrating robotic dismantling systems. These systems improve material recovery precision by 25% and reduce manual labor requirements by nearly 30%. Advanced optical sorting technologies now identify silicon, silver, and copper components with 98% accuracy, minimizing contamination rates below 5%. Europe and East Asia are leading adopters, where over 60% of newly licensed facilities deploy AI-enabled sorting lines to optimize throughput and ensure regulatory compliance.

• 35% Growth in High-Purity Silicon Recovery Programs: The push for circular photovoltaic manufacturing has accelerated demand for refined silicon extraction. Modern chemical delamination processes recover up to 95% of silicon content compared to 80% under older mechanical methods. In 2025, nearly 35% of recycled photovoltaic material was reintegrated into new module production, up from 22% three years earlier. This measurable improvement reduces raw polysilicon dependency by approximately 18%, supporting supply chain resilience and lowering carbon intensity in solar panel manufacturing.

• 50% Expansion in Extended Producer Responsibility (EPR) Compliance: Regulatory enforcement is intensifying across key markets, with over 50% of OECD countries mandating structured photovoltaic waste collection systems. Formal recycling rates in regulated regions now exceed 75%, compared to less than 30% in unregulated markets. Digital tracking platforms have increased waste traceability by 20%, enabling more accurate lifecycle monitoring and compliance reporting. This policy-driven transformation is accelerating investments in certified recycling infrastructure and environmentally sustainable processing technologies.

• 28% Rise in Utility-Scale Decommissioning Projects: Large solar farms installed between 2005 and 2012 are reaching end-of-life phases, resulting in a 28% increase in decommissioning contracts in 2024. Utility-scale operators now account for nearly 45% of total recyclable photovoltaic volumes. Bulk recycling agreements reduce per-unit processing costs by 15% and improve logistical efficiency by 22%. North America and China are experiencing the highest volume transitions, where grid modernization and repowering initiatives are driving structured component replacement programs.

The Solar Components Recycling market is segmented by type, application, and end-user, reflecting distinct material streams and operational demands. Crystalline silicon panel recycling accounts for the majority of processing volumes due to its dominant installed base, while thin-film module recycling represents a specialized but expanding segment. Application-wise, utility-scale solar farms generate the highest recycling volumes, followed by commercial and industrial installations. Residential systems contribute smaller but steadily increasing quantities as rooftop installations mature. From an end-user perspective, recycling service providers and photovoltaic manufacturers form the core demand base, while independent power producers and government-backed renewable agencies are strengthening participation. Material recovery efficiency, regulatory compliance requirements, and circular supply chain strategies shape segmentation dynamics, influencing procurement decisions and long-term infrastructure planning.

Crystalline silicon panel recycling leads the Solar Components Recycling market, accounting for approximately 72% of total processed volumes due to the widespread deployment of mono- and polycrystalline modules over the past two decades. These panels contain high-value recoverable materials such as aluminum frames, glass sheets, and silver contacts, enabling recovery rates above 90% for certain components. Thin-film panel recycling holds nearly 18% share, driven by installations using cadmium telluride and copper indium gallium selenide technologies. However, thin-film recycling is the fastest-growing type, expanding at an estimated 16% CAGR due to rising adoption of lightweight and flexible modules in commercial projects. Other niche categories, including bifacial and building-integrated photovoltaic modules, collectively contribute around 10% of recycling volumes but are gaining attention due to complex material compositions.

Utility-scale solar farms represent the leading application segment, contributing nearly 48% of total recycling demand due to the large volume of panels installed in centralized power plants. Commercial and industrial rooftop installations account for approximately 32%, supported by structured decommissioning cycles and corporate ESG mandates. Residential rooftop systems hold close to 20% share, reflecting the gradual aging of distributed solar infrastructure. While utility-scale recycling currently dominates, commercial and industrial applications are the fastest-growing segment, advancing at nearly 15% CAGR as businesses accelerate panel replacement programs to improve energy efficiency by 12–18%. Large enterprises increasingly prioritize certified recycling partners to meet sustainability benchmarks.

Recycling service providers and specialized waste management firms lead the Solar Components Recycling market, accounting for approximately 44% of operational control across processing facilities. Photovoltaic manufacturers represent around 30% of end-user participation, increasingly integrating backward recycling capabilities to secure raw material supply. Independent power producers contribute nearly 16%, while government-backed renewable agencies and research institutions collectively hold about 10%. Photovoltaic manufacturers are the fastest-growing end-user group, expanding at roughly 17% CAGR as vertical integration strategies strengthen circular production models. Over 55% of large module producers have announced commitments to incorporate recycled materials into next-generation panels.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 16.1% between 2026 and 2033.

Asia-Pacific processed more than 1.8 million metric tons of end-of-life photovoltaic modules in 2025, supported by over 600 GW of installed solar capacity. Europe followed with a 27% market share, handling approximately 1.1 million metric tons, driven by strict waste electrical and electronic equipment directives and structured take-back systems. North America represented nearly 22% of global recycling volumes, with the United States contributing over 85% of regional capacity. South America and the Middle East & Africa collectively accounted for 10%, reflecting emerging but expanding recycling infrastructure. Across all regions, material recovery efficiency exceeded 90% for glass and aluminum in regulated markets, while digital traceability adoption surpassed 65% among licensed recycling operators, reinforcing compliance and circular economy integration.

North America holds approximately 22% of the global Solar Components Recycling market volume, with the United States representing nearly 85% of regional processing capacity. Utility-scale solar farms and commercial rooftop installations drive over 60% of recyclable volumes as early installations from 2008–2012 reach replacement cycles. Federal clean energy incentives and state-level landfill restrictions have increased formal recycling rates above 70% in key states such as California and Texas. Automation adoption in recycling facilities has risen by 35% since 2023, integrating AI-based optical sorting systems that improve material purity levels to 95%. First Solar operates specialized recycling lines capable of recovering up to 90% of semiconductor materials from cadmium telluride modules. Regional consumer behavior reflects higher enterprise adoption among utilities and corporate energy buyers, with over 50% of large-scale operators committing to certified recycling partnerships to meet ESG disclosure standards.

Europe accounts for approximately 27% of the global Solar Components Recycling market, with Germany, the UK, and France collectively contributing more than 60% of regional volumes. Mandatory take-back obligations under structured electronic waste directives have pushed formal recycling rates above 75%. Over 80% of decommissioned photovoltaic modules are processed through certified facilities equipped with automated separation technologies. Adoption of chemical-free delamination methods has improved silicon recovery efficiency by 20% compared to legacy systems. Veolia operates advanced photovoltaic recycling plants capable of processing over 4,000 tons annually with material recovery rates exceeding 90%. Regional consumer behavior is strongly influenced by regulatory pressure, leading to higher demand for transparent lifecycle documentation and explainable recycling processes. Approximately 68% of solar asset owners require documented proof of recycled material reintegration into new manufacturing cycles, reinforcing compliance-led procurement strategies.

Asia-Pacific leads global recycling volume, accounting for 41% of processed photovoltaic waste in 2025. China, India, and Japan are the top consuming countries, with China alone exceeding 600 GW of installed solar capacity and generating more than 1 million metric tons of recyclable modules annually. Infrastructure expansion includes over 20 industrial-scale recycling plants commissioned since 2022, each with capacities above 50,000 tons per year. Automation penetration in new facilities surpasses 60%, improving throughput efficiency by 25%. Trina Solar has expanded its in-house recycling initiatives to recover up to 95% of aluminum and glass components for reintegration into module manufacturing. Regional innovation hubs in Jiangsu and Tokyo are focusing on high-purity silicon refinement technologies. Consumer behavior is characterized by strong industrial participation, with over 70% of large manufacturers integrating backward recycling to secure raw material supply continuity.

South America represents nearly 6% of the global Solar Components Recycling market, with Brazil and Argentina leading regional adoption. Brazil accounts for more than 65% of regional installed solar capacity, surpassing 40 GW in 2025, creating a growing pipeline of end-of-life modules. Government-backed renewable energy auctions have accelerated solar farm development by 30% over the past five years. Recycling infrastructure remains developing, with fewer than 15 certified facilities operating region-wide, but planned capacity expansion is projected to double processing volumes by 2028. Trade policies encouraging local manufacturing are stimulating investments in circular energy projects. Regional consumer behavior reflects cost sensitivity, with nearly 55% of asset owners prioritizing recycling partners offering bundled decommissioning and logistics services to reduce total project expenditure.

The Middle East & Africa accounts for approximately 4% of global Solar Components Recycling volumes but shows rising demand tied to rapid solar project deployment. The UAE and South Africa are key growth countries, together representing over 60% of regional installed photovoltaic capacity. Utility-scale projects exceeding 5 GW in the Gulf region are expected to enter phased replacement cycles within the next decade. Technological modernization includes adoption of automated dismantling units in pilot facilities, improving recovery efficiency by 18%. Trade partnerships supporting renewable infrastructure have increased cross-border recycling agreements by 20%. In South Africa, emerging waste management firms are collaborating with solar developers to establish structured take-back programs. Consumer behavior in this region is influenced by national diversification agendas, with over 50% of new solar tenders including sustainability clauses requiring certified recycling compliance.

China – 34% share in the Solar Components Recycling market: Dominance supported by over 600 GW installed solar capacity and extensive industrial-scale recycling infrastructure.

Germany – 12% share in the Solar Components Recycling market: Leadership driven by strict electronic waste regulations and high formal recycling compliance exceeding 75%.

The Solar Components Recycling market exhibits a moderately fragmented structure with over 120 active competitors globally, including specialized recyclers, photovoltaic manufacturers with in-house recovery units, and integrated waste management firms. The top five companies collectively account for approximately 38% of total processing capacity, indicating competitive intensity alongside consolidation trends. Strategic initiatives include partnerships between module manufacturers and recycling operators, with more than 25 collaboration agreements signed since 2023 to secure circular supply chains. Automation-driven facility upgrades have increased operational efficiency by 20% across leading plants, while investments in chemical-free delamination technologies have improved silicon purity recovery to above 95%. Mergers and acquisitions activity has risen by 15% year-over-year as firms seek geographic expansion and technology acquisition. Competitive positioning increasingly depends on recovery yield, ESG certification, digital traceability systems, and cost optimization, reinforcing innovation as a primary differentiator within the Solar Components Recycling market.

First Solar

Veolia

Trina Solar

Recycle PV Solar

Silcontel

Canadian Solar

Envaris

Rinovasol

Solarcycle

Remondis

Sharp Energy Solutions

Technological advancement is redefining operational efficiency and material recovery performance across the Solar Components Recycling market. Automated robotic dismantling systems are now capable of processing up to 60 panels per hour, improving throughput by nearly 30% compared to manual disassembly lines. AI-driven optical sorting technologies achieve material identification accuracy levels above 98%, significantly reducing cross-contamination and increasing the resale value of recovered glass and aluminum. Advanced thermal delamination systems operate at controlled temperatures between 450°C and 600°C, enabling encapsulant removal without damaging high-purity silicon wafers.

Chemical etching and hydrometallurgical processes are increasingly adopted to extract silver and copper with recovery rates exceeding 95%, compared to less than 80% under conventional shredding methods. Laser-based separation techniques are also emerging, reducing silicon wafer breakage by 15% and enhancing reuse potential in secondary photovoltaic production. Digital traceability platforms integrated with blockchain technology are improving compliance documentation efficiency by 25%, particularly in regulated European and North American markets.

Innovations in closed-loop recycling are gaining traction, where up to 20% of recovered silicon is directly reintegrated into new module manufacturing. Additionally, modular recycling plants with scalable capacities ranging from 10,000 to 100,000 metric tons annually are enabling decentralized processing models. Integration of predictive analytics tools helps optimize facility maintenance cycles, reducing downtime by 18% and increasing asset utilization rates beyond 85%, strengthening the long-term sustainability of the Solar Components Recycling market.

• In October 2024, First Solar announced the expansion of its advanced photovoltaic recycling facility in Ohio, increasing annual recycling capacity to over 12,000 metric tons. The upgraded facility enhances semiconductor material recovery rates to approximately 90%, supporting closed-loop manufacturing for its cadmium telluride modules. Source: www.firstsolar.com

• In March 2025, Solarcycle completed the commissioning of a new solar panel recycling plant in Georgia with a processing capacity exceeding 1 million panels annually. The facility incorporates automated glass separation systems that recover up to 95% of glass materials for reintegration into domestic supply chains. Source: www.solarcycle.us

• In July 2024, Veolia expanded its photovoltaic panel recycling operations in France, integrating high-precision separation technology capable of achieving 90% material recovery efficiency. The upgrade aligns with European electronic waste directives and strengthens the company’s renewable energy circularity portfolio. Source: www.veolia.com

• In February 2025, Trina Solar announced the launch of a dedicated module take-back and recycling program targeting large-scale utility customers in Asia. The initiative focuses on recovering over 95% of aluminum frames and glass components, reinforcing sustainable supply chain practices. Source: www.trinasolar.com

The Solar Components Recycling Market Report provides a comprehensive evaluation of material recovery ecosystems across crystalline silicon, thin-film, bifacial, and emerging photovoltaic module types. The study examines recycling capacities ranging from small-scale facilities processing 10,000 metric tons annually to industrial plants exceeding 100,000 metric tons. It analyzes applications spanning utility-scale solar farms, which contribute nearly 48% of recyclable volumes, commercial and industrial installations accounting for approximately 32%, and residential rooftop systems representing about 20%.

Geographically, the report covers Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, highlighting regional processing volumes, regulatory penetration rates exceeding 75% in structured markets, and automation adoption levels above 60% in advanced facilities. Technology assessment includes robotic dismantling systems, hydrometallurgical silver extraction, laser-assisted silicon recovery, and digital traceability integration. Material-specific insights evaluate recovery rates surpassing 90% for glass and aluminum and up to 95% for semiconductor elements.

The scope further addresses ESG compliance trends, extended producer responsibility frameworks implemented in over 50% of regulated economies, and emerging circular manufacturing models integrating recycled silicon into new modules. Strategic analysis includes competitive positioning, partnership activity, infrastructure investments exceeding several billion dollars globally, and innovation pipelines supporting long-term photovoltaic waste management resilience.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

14.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

First Solar, Veolia, Trina Solar, Recycle PV Solar, Silcontel, Canadian Solar, Envaris, Rinovasol, Solarcycle, Remondis, Sharp Energy Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |