Reports

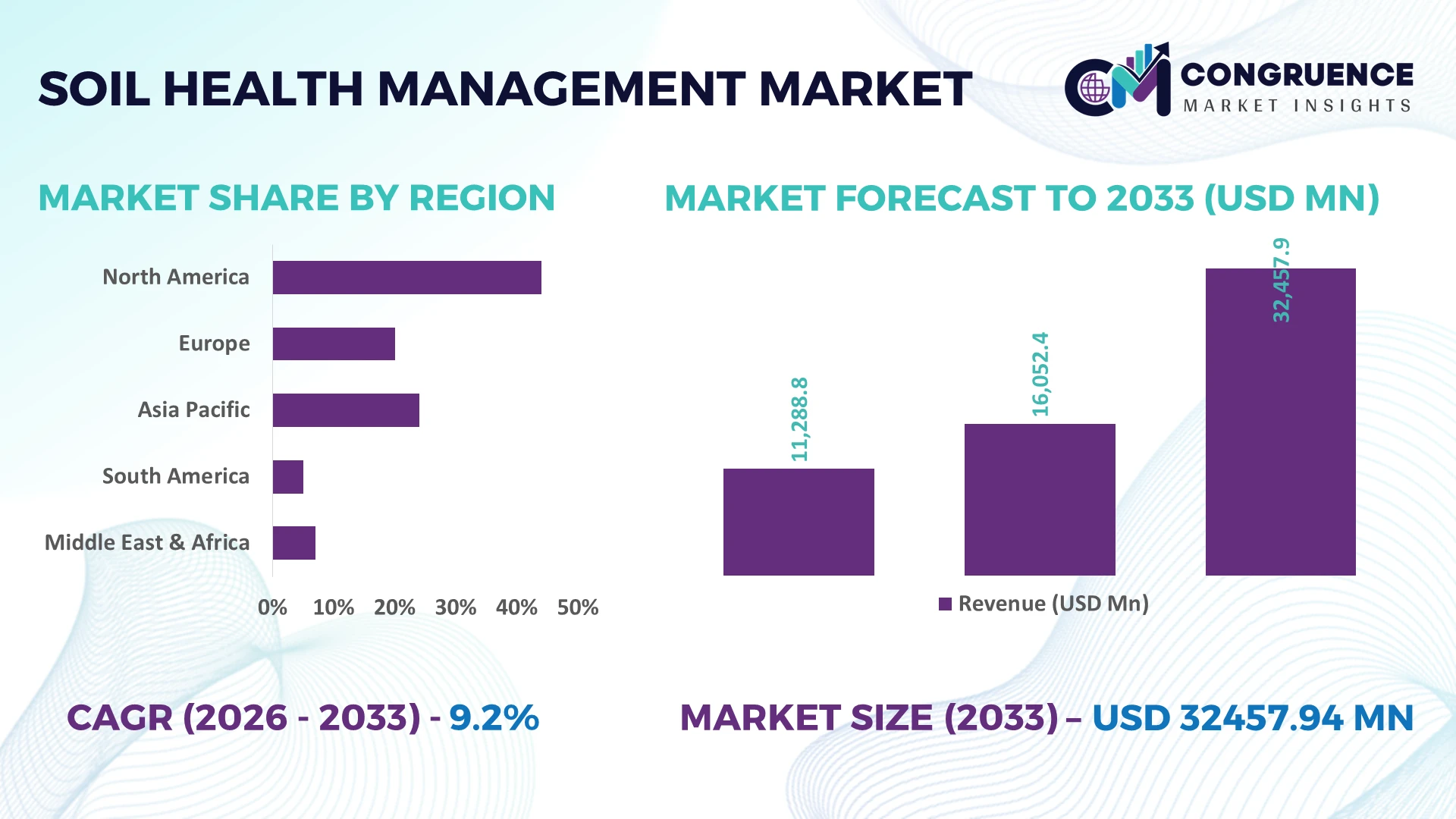

The Global Soil Health Management Market was valued at USD 16052.4 Million in 2025 and is anticipated to reach a value of USD 32457.94 Million by 2033 expanding at a CAGR of 9.2% between 2026 and 2033. Growth is driven by precision agriculture adoption, regenerative farming programs, biological soil input innovations, and digital soil analytics that improve nutrient efficiency while supporting food security and climate-resilient crop production.

The United States leads the global soil health management market with approximately 31% share, supported by large-scale precision farming across more than 370 million acres, strong public-private investments, and rapid deployment of AI-enabled soil monitoring technologies. Compared with India, where adoption is accelerating through government-backed soil health initiatives and expanding agri-tech platforms, U.S. growers maintain higher digital integration and biological input penetration. Continued agricultural resilience efforts following global fertilizer supply disruptions reinforce long-term investment priorities.

Strategic investments should prioritize digital soil intelligence, biological solutions, and region-specific nutrient management platforms to strengthen productivity and long-term agricultural sustainability.

Market Size & Growth: USD 16052.4 Million (2025) to USD 32457.94 Million (2033) at 9.2% CAGR, driven by precision agriculture and biological soil enhancement technologies.

Top Growth Drivers: Precision farming adoption +24%, biological inputs +19%, regenerative agriculture programs +21%.

Short-Term Forecast: By 2028, nutrient-use efficiency improves by 18% while input costs decline by nearly 12% through advanced soil monitoring.

Emerging Technologies: AI analytics, IoT soil sensors, and microbial biostimulants improve field productivity by over 20%.

Regional Leaders: North America exceeds USD 10 Billion, Europe approaches USD 8 Billion, Asia-Pacific surpasses USD 9 Billion, supported by expanding precision farming adoption.

Consumer/End-User Trends: More than 46% of commercial farms integrate digital soil assessment for fertilizer optimization and yield improvement.

Pilot/Case Example: 2026 precision soil mapping programs improved nutrient efficiency by 22% across large commercial farming operations.

Competitive Landscape: Top companies hold approximately 38% combined market share, led by Bayer, Syngenta, BASF, Corteva, and Yara International.

Regulatory & ESG Impact: Sustainable agriculture policies reduce synthetic fertilizer dependence by nearly 15% while strengthening soil conservation targets.

Investment & Funding: Global investments exceed USD 4 Billion through agri-tech partnerships, biological innovation, and regional manufacturing expansion.

Innovation & Future Outlook: Next-generation microbial formulations, autonomous field analytics, and digital agronomy platforms accelerate high-growth market transformation amid evolving agricultural supply chains.

Increasing demand for biological soil amendments, precision nutrient management, and AI-powered soil diagnostics is reshaping agricultural operations. Nearly 42% of large-scale farming projects now integrate digital soil monitoring to optimize resource efficiency and improve long-term productivity. Expanding regenerative farming programs and stricter environmental compliance continue to accelerate innovation while strengthening resilient agricultural supply chains, setting the stage for deeper strategic market evaluation.

Soil health management has become a strategic priority as agricultural producers seek higher productivity while reducing dependence on volatile fertilizer supply chains. Digital soil intelligence, biological crop inputs, and precision nutrient planning are reshaping competitive positioning across commercial farming. Governments are strengthening soil conservation policies, while agribusinesses increasingly integrate measurable soil performance indicators into procurement, sustainability, and operational planning to improve resilience against climate variability and input cost fluctuations.

AI-enabled soil analytics process field conditions nearly 45% faster than conventional laboratory-led assessment while reducing unnecessary fertilizer application by approximately 20%, delivering lower operating costs and improved nutrient efficiency. The United States leads large-scale deployment through advanced precision farming infrastructure, whereas India is expanding adoption through digital agriculture initiatives and soil health monitoring programs across smallholder farming systems. Over the next two to three years, digital soil mapping and biological input integration are expected to exceed 50% adoption among large commercial farms in several developed agricultural markets.

Leading companies are deploying integrated platforms combining satellite imagery, IoT sensors, and microbial soil products while expanding partnerships with agri-tech providers and research institutions. For example, commercial grain producers increasingly use variable-rate nutrient application linked to real-time soil analytics to improve field performance and reduce waste. Organizations prioritizing data-driven agronomy, localized biological solutions, and digital ecosystem partnerships will strengthen long-term competitiveness and operational resilience.

Rapid deployment of precision agriculture technologies is transforming soil health management from periodic assessment to continuous field optimization. More than 52% of large commercial farms in the United States now utilize digital soil mapping, while biological soil input adoption has increased by approximately 24% across intensive farming operations. Stricter nutrient management regulations and continued fertilizer supply-chain restructuring are encouraging growers to optimize every application. Companies are responding through investments in AI-powered soil analytics, microbial product portfolios, and strategic collaborations with precision equipment manufacturers. A notable operational advantage is the integration of real-time soil intelligence with automated nutrient application, enabling measurable productivity improvements while reducing unnecessary field inputs and strengthening long-term farm profitability.

High implementation costs and uneven digital infrastructure continue to restrict widespread adoption, particularly among small and medium-sized farms. Precision soil monitoring systems can increase initial deployment costs by 18–30%, while nearly 40% of smaller agricultural operations still lack reliable digital connectivity for continuous field analytics. India and several emerging agricultural economies also face fragmented landholdings that reduce technology scalability. These constraints affect operational efficiency, investment returns, and technology standardization. Companies are mitigating risks by developing modular subscription-based platforms, expanding local manufacturing partnerships, and introducing lower-cost biological soil solutions that reduce dependence on imported agricultural inputs while improving accessibility for broader farming communities.

Next-generation microbial formulations, predictive soil modeling, and integrated farm management platforms are opening high-value opportunities beyond conventional fertilizer optimization. Field trials indicate biological soil products improve nutrient availability by approximately 18%, while AI-assisted agronomic recommendations increase decision accuracy by over 30%. Australia and Brazil are accelerating regenerative farming initiatives supported by digital monitoring and carbon-focused agricultural policies. Industry leaders are expanding R&D investments, partnering with agricultural technology startups, and building interoperable digital ecosystems that combine satellite imagery, sensor networks, and biological inputs. An emerging competitive advantage lies in transforming verified soil health data into measurable sustainability and productivity outcomes for commercial agriculture.

Long-term market expansion depends on integrating diverse technologies across fragmented agricultural ecosystems. More than 35% of precision agriculture deployments encounter interoperability challenges between equipment, software platforms, and field data systems, while the shortage of skilled digital agronomy professionals exceeds 20% in several advanced farming markets. Growing cybersecurity requirements for connected agricultural platforms further increase operational complexity as farms become increasingly data-driven. Companies must strengthen cloud infrastructure, invest in standardized data architectures, and expand technical training through partnerships with equipment manufacturers and agricultural institutions. Successfully resolving these execution challenges will determine deployment consistency, operational scalability, and sustainable competitive differentiation.

AI-Driven Soil Intelligence: AI-powered soil analytics platforms are reducing field assessment time by nearly 45%, while variable-rate nutrient application has improved fertilizer efficiency by approximately 20% and lowered unnecessary input use by 15%. Stricter nutrient management regulations in the United States are accelerating deployment, prompting companies to integrate satellite imagery, sensor networks, and predictive agronomy software through strategic technology partnerships that streamline field decision-making.

Biological Input Portfolio Expansion: Bio-based soil enhancement products now represent one of the fastest-expanding product categories, with microbial formulation adoption increasing by around 28% and chemical input dependency declining by nearly 16% across commercial farms. Manufacturers are restructuring production toward region-specific microbial strains, while partnerships with agricultural distributors improve localized product availability and reduce logistics risks created by global fertilizer supply-chain disruptions.

Carbon-Focused Soil Monitoring: Carbon accounting requirements are encouraging continuous soil monitoring, with approximately 35% more commercial farming enterprises incorporating digital soil verification into sustainability programs. Australia and Canada are expanding regenerative farming initiatives that reward measurable soil improvements, leading technology providers to bundle soil analytics with carbon reporting platforms. This creates an additional value stream beyond conventional agronomic performance, strengthening long-term customer retention.

Integrated Precision Farming Platforms: More than 48% of large farming enterprises are deploying unified platforms combining irrigation management, soil diagnostics, and crop analytics, reducing operational planning time by nearly 25%. Equipment manufacturers are expanding interoperability partnerships to simplify digital workflows, while agribusinesses increasingly prioritize integrated field management systems over standalone monitoring tools, improving operational consistency across multi-location farming operations.

Organic Amendments remain the leading segment because of their broad compatibility with conventional and regenerative farming systems, cost-effective soil improvement, and large-scale deployment across cereal, oilseed, and horticultural production. Nearly 41% of commercial soil improvement programs continue to incorporate organic amendments as a foundational practice. Biofertilizers represent the fastest-growing segment as growers seek higher nutrient efficiency and reduced dependence on synthetic fertilizers. Adoption of biofertilizers has increased by approximately 27%, supported by advances in microbial science and precision application technologies. Soil Conditioners continue expanding in degraded agricultural land, while Soil Testing solutions benefit from digital agriculture adoption. Microbial Products are gaining strategic importance through customized formulations designed for specific crops and soil conditions. Companies are expanding biological product portfolios, strengthening research collaborations, and integrating digital diagnostics with nutrient management recommendations to improve long-term farm productivity.

Investment priorities increasingly favor integrated solutions that combine Soil Testing with Biofertilizers and Microbial Products, allowing companies to deliver complete soil management programs instead of standalone products. This shift improves customer retention while creating recurring service opportunities through data-driven agronomy platforms.

Crop Production remains the dominant application because large-scale farming operations require continuous soil monitoring, nutrient optimization, and productivity improvement across extensive cultivation areas. Approximately 58% of precision soil management deployments support broad-acre crop production, making this segment the primary demand center. Precision Farming is the fastest-growing application as AI-based field analytics, sensor integration, and variable-rate nutrient application become standard operational practices. Adoption of precision farming technologies has expanded by nearly 30%, improving fertilizer efficiency while reducing unnecessary field operations. Organic Farming continues gaining momentum under sustainability programs, whereas Horticulture increasingly utilizes specialized biological products to improve soil quality for high-value crops. Turf Management remains a stable niche supported by commercial landscaping and sports infrastructure projects. Companies continue expanding integrated digital agronomy platforms and precision service offerings to strengthen operational performance.

Demand is shifting toward application-specific recommendations that combine satellite monitoring, predictive analytics, and biological inputs, enabling differentiated service models across commercial agriculture and specialty crop production while improving long-term resource efficiency.

Farmers represent the largest end-user segment because they directly manage field operations, nutrient planning, and soil productivity decisions across diverse agricultural systems. More than 61% of commercial soil management investments originate from farm-level purchasing decisions. Agribusiness Companies constitute the fastest-growing end-user group as they expand integrated agronomy services, digital advisory platforms, and biological product portfolios. Adoption among agribusiness service providers has increased by approximately 26% through technology partnerships and ecosystem expansion. Agricultural Cooperatives continue strengthening collective procurement and technical support, while Government Agencies invest in national soil monitoring initiatives. Research Institutes accelerate innovation through microbial development and precision agronomy research, whereas Greenhouses increasingly deploy advanced soil diagnostics to maximize high-value crop productivity. Companies are tailoring pricing models, subscription services, and bundled digital platforms to address varying operational requirements across customer groups.

Competitive positioning increasingly depends on ecosystem development rather than individual product sales, encouraging suppliers to integrate advisory services, biological products, and digital analytics into long-term customer engagement strategies that improve operational value.

North America accounted for the largest market share at 35.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 10.4% CAGR between 2026 and 2033.

Precision Agriculture Drives Large-Scale Soil Optimization

North America maintains its leadership through widespread precision agriculture deployment, advanced biological input adoption, and strong digital farming infrastructure. Large commercial farms increasingly integrate AI-based soil diagnostics with automated nutrient management to improve productivity and reduce operational costs. Nearly 60% of large-scale farming enterprises use precision soil monitoring technologies, while biological product deployment continues expanding across row crop production. Investment in agricultural software platforms, sensor networks, and microbial product manufacturing strengthens enterprise competitiveness. Equipment manufacturers and agri-tech providers are accelerating strategic collaborations that integrate field analytics with automated application systems, improving operational efficiency and supporting sustainable agricultural production.

United States Market Outlook: The United States remains the regional leader due to its highly mechanized agricultural sector, extensive precision farming infrastructure, and strong commercialization of biological soil technologies. More than 370 million acres are managed using advanced precision agriculture practices, supporting rapid deployment of AI-enabled soil analytics and digital nutrient planning. Federal conservation initiatives and private-sector investment continue encouraging integrated soil management platforms, while leading agribusinesses expand partnerships focused on microbial innovation and field automation to improve long-term agricultural productivity.

Sustainability Policies Accelerate Biological Adoption

Europe continues strengthening soil health management through environmental regulations, regenerative agriculture programs, and digital farm modernization. Sustainable nutrient management strategies encourage greater adoption of biological products and precision soil assessment across commercial farming operations. Approximately 47% of large agricultural enterprises have incorporated digital soil monitoring into nutrient planning programs. Investment in climate-smart farming technologies and collaborative agricultural research supports innovation throughout the value chain. Technology providers increasingly align product development with carbon reduction objectives and resource-efficient farming systems, reinforcing long-term operational resilience.

Germany Market Outlook: Germany leads the regional market through advanced agricultural engineering, strong digital farming adoption, and well-developed research capabilities. Commercial farms increasingly deploy integrated soil monitoring platforms linked with automated nutrient management systems, improving fertilizer efficiency and operational consistency. Precision farming technology adoption exceeds 40% among large agricultural enterprises, while continued collaboration between research institutions, machinery manufacturers, and agribusiness companies accelerates commercialization of advanced soil management solutions.

Agricultural Modernization Expands Market Scale

Asia-Pacific represents the fastest-expanding regional market as governments accelerate agricultural modernization, digital farming initiatives, and sustainable crop management programs. Rapid mechanization, expanding biological input production, and increasing investment in precision agriculture are improving soil productivity across major farming economies. Precision agriculture deployment has increased by nearly 28% across commercial farming operations in key countries. Local manufacturers continue expanding production capacity for microbial products and digital soil assessment technologies while strengthening regional distribution networks to improve accessibility across diverse agricultural systems.

China Market Outlook: China dominates the regional market through extensive agricultural production, large-scale digital agriculture investments, and expanding biological input manufacturing. National initiatives promoting high-standard farmland development encourage rapid adoption of precision soil monitoring technologies across commercial farming regions. Large domestic agribusinesses continue investing in AI-enabled agronomy platforms, automated nutrient management, and microbial product innovation, strengthening operational efficiency while supporting long-term agricultural sustainability objectives.

Regenerative Farming Strengthens Commercial Adoption

South America is experiencing steady expansion as commercial agriculture increasingly adopts regenerative farming practices and precision nutrient management. Large soybean, corn, and sugarcane production systems are driving demand for soil testing, organic amendments, and biological products. Approximately 33% of commercial farming enterprises have expanded investment in digital soil assessment technologies to improve productivity and reduce fertilizer losses. Despite infrastructure disparities across rural areas, companies continue strengthening regional distribution, technical advisory services, and localized biological product development to improve deployment efficiency.

Brazil Market Outlook: Brazil leads the regional market through its extensive commercial farming sector, expanding biological agriculture industry, and strong focus on soil productivity. Large agricultural enterprises increasingly integrate microbial products with precision farming systems to enhance nutrient availability and reduce operational costs. Continued investment in agricultural research, local production facilities, and digital farm management platforms supports widespread adoption across grain-producing regions while strengthening export-oriented agricultural competitiveness.

Smart Agriculture Supports Resource Efficiency

The Middle East & Africa market is advancing through agricultural modernization programs, water-efficient farming practices, and increasing investment in digital agriculture. Soil monitoring technologies are gaining importance as governments prioritize food security and sustainable land management under resource constraints. Around 22% of newly established commercial farming projects now integrate digital soil assessment into operational planning. Public-private partnerships continue supporting deployment of precision agriculture technologies, biological inputs, and advanced irrigation systems that improve long-term agricultural resilience despite climatic challenges.

Saudi Arabia Market Outlook: Saudi Arabia leads regional investment through large-scale agricultural modernization initiatives, precision irrigation deployment, and controlled-environment farming expansion. National food security strategies continue encouraging adoption of advanced soil diagnostics, biological amendments, and digital farm management platforms across commercial agricultural projects. Investment in smart agriculture infrastructure and technology partnerships strengthens operational efficiency while supporting sustainable production under arid environmental conditions.

The competitive landscape is led by Bayer, Syngenta, BASF, Corteva Agriscience, and Yara International, competing against regional biological-input specialists and digital agronomy providers. Global leaders leverage integrated crop nutrition portfolios, while regional manufacturers compete through localized formulations and lower production costs. The top five companies collectively control approximately 38% of the market, leaving significant competition in specialized soil solutions. Technology leadership, customized recommendations, and supply-chain reliability increasingly outweigh price-only strategies. AI-enabled soil analytics improve nutrient management efficiency by nearly 20%, while advanced microbial formulations increase nutrient availability by approximately 18%, creating measurable product differentiation. Companies continue expanding biological manufacturing, acquiring agri-tech capabilities, forming precision agriculture partnerships, and integrating digital advisory platforms with product portfolios. Competition is shifting from standalone fertilizer products toward integrated soil intelligence ecosystems combining diagnostics, biological inputs, and predictive analytics. High R&D requirements, regulatory approvals, and validated agronomic performance remain major entry barriers. Sustainable competitive advantage depends on delivering measurable field outcomes, scalable digital services, localized biological innovation, and resilient distribution networks.

Bayer AG

Syngenta Group

BASF SE

Corteva Agriscience

Yara International ASA

Nutrien Ltd.

UPL Limited

The Mosaic Company

Novonesis

Eurofins Scientific

Bioceres Crop Solutions

FMC Corporation

K+S AG

Nufarm Limited

Artificial intelligence, IoT-enabled soil sensors, satellite imagery, and cloud-based agronomic platforms are becoming the operational foundation of modern soil health management. AI-driven analytics reduce soil assessment time by nearly 45% and improve nutrient recommendation accuracy by approximately 30% compared with conventional laboratory-centered workflows. More than 46% of large commercial farming operations now integrate at least one digital soil intelligence platform, enabling faster field decisions, optimized fertilizer use, and stronger operational consistency across multiple locations.

Emerging technologies include microbial bioengineering, predictive soil modeling, autonomous sampling equipment, and digital twin platforms for agricultural land. Advanced microbial formulations improve nutrient availability by around 18% over traditional soil conditioners, while predictive analytics lower unnecessary fertilizer application by nearly 20%. Agribusiness companies, precision farming providers, and integrated crop solution manufacturers gain the strongest competitive advantage by combining biological innovation with real-time digital agronomy, creating differentiated service ecosystems rather than standalone input products.

Between 2026 and 2028, interoperability between machinery, sensors, drones, and farm management software will become a primary competitive differentiator. Companies investing early in unified digital ecosystems, automated nutrient optimization, and scalable biological technologies will strengthen customer retention and operational efficiency. As regulatory reporting and sustainability metrics become increasingly data-driven, technology-enabled soil management will shift from an optional productivity tool to an essential enterprise capability for commercial agriculture.

March 2024: Bayer strengthened its regenerative agriculture ecosystem by expanding collaboration within the Coalition for Sustainable and Regenerative Agriculture alongside Purdue University, supporting long-term soil health research across multiple production systems with real-world farm data. Business impact: accelerated validation of scalable soil management solutions. Source: bayer.com

October 2024: Yara expanded the reach of its YaraFX Insight API to more than 10 new partners, enabling wider integration of digital agronomic recommendations into third-party farming platforms. Business impact: strengthened precision nutrient management capabilities and improved digital soil decision support across commercial agriculture. Source: yara.com

October 2025: Bayer and Ginkgo Bioworks extended their multi-year strategic partnership to accelerate next-generation microbial nitrogen fixation technologies for agriculture, reinforcing biological alternatives to conventional fertilizers. Business impact: expanded innovation pipeline and strengthened commercialization of advanced soil health solutions.

February 2026: Yara reported that 55% of fresh grass samples analyzed after the 2024 wet season were sulphur deficient, prompting updated nutrient management guidance for growers. Business impact: reinforced demand for precision soil nutrient diagnostics and optimized fertilizer planning under changing climatic conditions. Source: yara.co.uk

This report provides a comprehensive assessment of the global Soil Health Management Market across Organic Amendments, Soil Conditioners, Biofertilizers, Soil Testing, and Microbial Products, covering Crop Production, Horticulture, Organic Farming, Precision Farming, and Turf Management applications. It further evaluates demand across Farmers, Agricultural Cooperatives, Greenhouses, Research Institutes, Government Agencies, and Agribusiness Companies while examining market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of commercial deployments now combine biological inputs with digital soil assessment technologies, reflecting accelerating operational transformation.

The analysis evaluates competitive positioning, precision agriculture technologies, AI-enabled soil analytics, microbial innovation, digital agronomy platforms, and evolving deployment strategies between 2026 and 2033. It delivers actionable insights supporting investment prioritization, product portfolio expansion, regional market entry, partnership development, supply-chain optimization, and long-term competitive differentiation while identifying emerging niche opportunities in regenerative agriculture, carbon-focused soil management, and integrated biological farming ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 16052.4 Million |

Market Revenue in 2033 | USD 32457.94 Million |

CAGR (2026 - 2033) | 9.2% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, Yara International ASA, Nutrien Ltd., UPL Limited, The Mosaic Company, Novonesis, Eurofins Scientific, Bioceres Crop Solutions, FMC Corporation, K+S AG, Nufarm Limited |

Customization & Pricing | Available on Request (10% Customization is Free) |