Reports

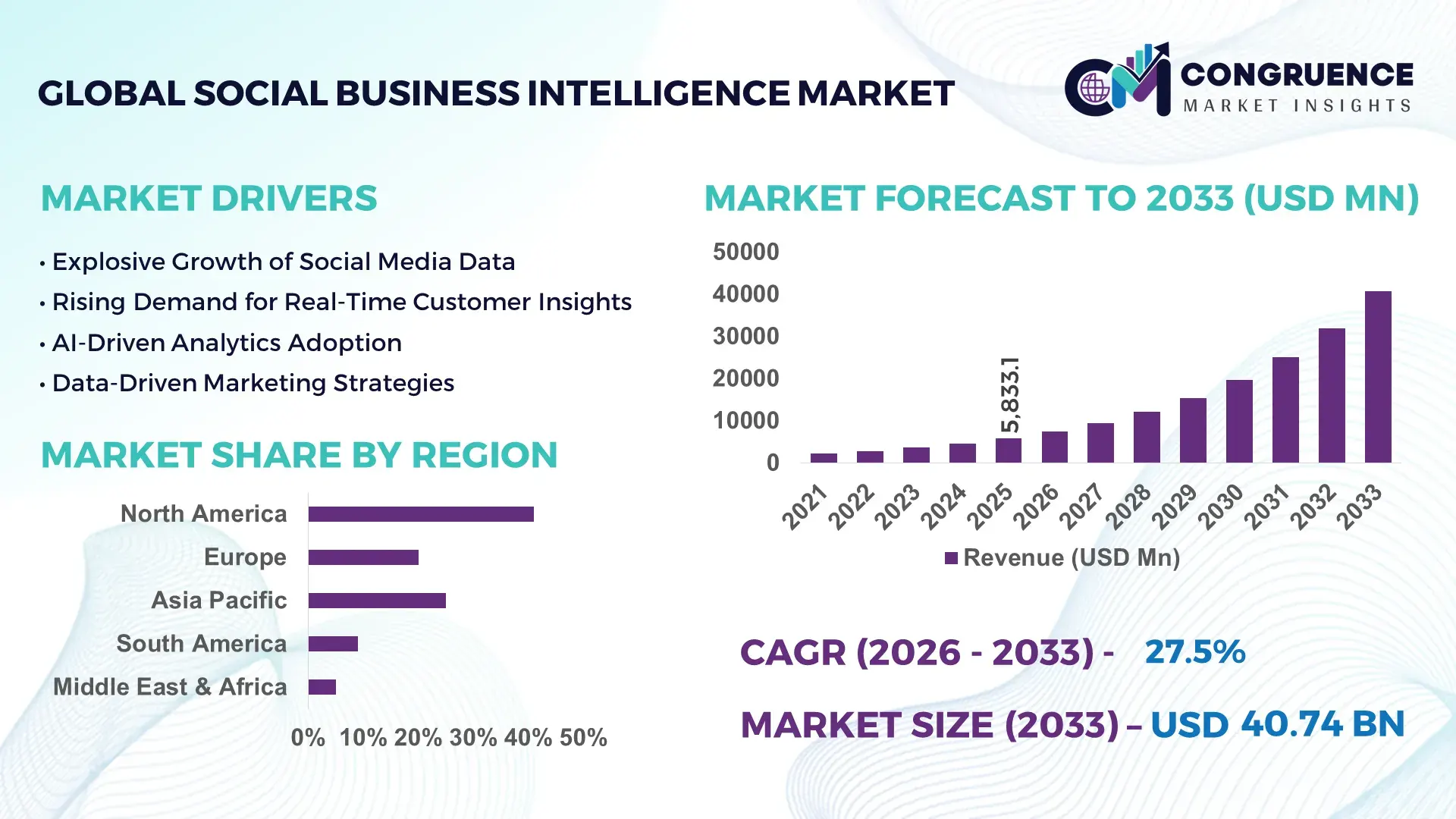

The Global Social Business Intelligence Market was valued at USD 5833.06 Million in 2025 and is anticipated to reach a value of USD 40736.01 Million by 2033 expanding at a CAGR of 27.5% between 2026 and 2033. This growth is driven by rapid enterprise adoption of AI-driven analytics to convert social data into real-time business decisions.

The United States leads the Social Business Intelligence ecosystem with enterprise-scale deployment capacity and sustained investment in cloud analytics. Over 72% of large U.S. enterprises integrate social analytics into CRM and marketing automation workflows, processing billions of social interactions monthly. Annual private and public investments in AI and data platforms exceeded USD 120 billion in 2024, accelerating NLP, sentiment analysis, and predictive analytics. Key applications span retail personalization, BFSI risk intelligence, media monitoring, and public-sector citizen engagement, with over 65% of Fortune 500 companies using social intelligence dashboards for executive decision-making.

Market Size & Growth: USD 5.83B (2025) to USD 40.74B (2033), CAGR 27.5%, fueled by AI-led real-time social insight adoption.

Top Growth Drivers: AI adoption 68%, omnichannel analytics uptake 61%, decision-cycle efficiency gain 42%.

Short-Term Forecast: By 2028, campaign ROI optimization improves by 35% through automated sentiment scoring and predictive alerts.

Emerging Technologies: Generative AI-based analytics, real-time natural language processing, graph-based social listening platforms.

Regional Leaders: North America projected at USD 15.2B by 2033 with deep enterprise BI integration; Europe at USD 11.4B driven by compliant analytics frameworks; Asia-Pacific at USD 9.8B supported by mobile-first social data consumption.

Consumer/End-User Trends: Marketing, customer experience, and risk intelligence teams account for nearly 70% of deployments, with daily operational dashboard usage becoming standard.

Pilot or Case Example: A 2024 omnichannel retail pilot reduced customer churn by 18% using predictive social sentiment alerts integrated into CRM systems.

Competitive Landscape: Salesforce leads with approximately 18% share, followed by Microsoft, IBM, SAP, and Oracle as major platform providers.

Regulatory & ESG Impact: Data protection laws, AI governance frameworks, and ESG reporting requirements are shaping compliant analytics architectures and vendor strategies.

Investment & Funding Patterns: Around USD 32B invested between 2023 and 2025, with strong momentum in SaaS-based analytics platforms and venture-backed AI startups.

Innovation & Future Outlook: Expansion of autonomous insight generation, multimodal data fusion, and deeper integration with enterprise AI ecosystems.

The Social Business Intelligence Market is primarily driven by marketing and advertising applications, contributing close to 40% of overall enterprise demand, followed by BFSI at around 22% and media and entertainment at nearly 15%. Technological advancements such as real-time emotion analytics, multilingual sentiment engines, and AI copilots embedded within BI platforms are reshaping competitive differentiation. Regulatory compliance, data privacy enforcement, and economic pressure for measurable ROI continue to accelerate adoption. Regionally, North America and Europe dominate enterprise consumption, while Asia-Pacific demonstrates the fastest growth due to social commerce expansion and mobile-centric user behavior. Emerging trends indicate a shift toward autonomous decision intelligence, cross-platform social graph analytics, and tighter integration with enterprise data lakes and AI models.

The Social Business Intelligence Market has become strategically relevant as enterprises increasingly rely on real-time social data to guide brand positioning, customer engagement, risk mitigation, and policy decisions. Organizations are integrating social intelligence into core business strategy to shorten decision cycles and improve predictive accuracy. AI-driven social analytics delivers up to 45% improvement compared to traditional rule-based sentiment monitoring, enabling faster detection of consumer behavior shifts and reputational risks. North America dominates in data processing volume due to enterprise-scale deployments, while Asia-Pacific leads in adoption with over 62% of large digital-first enterprises actively using social intelligence platforms.

From a forward-looking perspective, the market’s future pathways are closely tied to automation, compliance, and measurable efficiency gains. By 2028, generative AI–powered social analytics is expected to improve campaign performance optimization KPIs by nearly 38% through autonomous insight generation and scenario modeling. Firms are also committing to ESG improvements such as a 30% reduction in data processing energy intensity by 2030 through cloud optimization and AI workload efficiency. In 2024, a U.S.-based retail analytics program achieved a 21% reduction in customer churn through AI-driven social listening integrated with CRM workflows. As regulatory scrutiny on data ethics intensifies, the Social Business Intelligence Market is positioned as a core pillar of enterprise resilience, compliance assurance, and sustainable, insight-led growth.

Enterprises face constant pressure to understand customer sentiment and behavior in real time, driving strong demand for Social Business Intelligence solutions. Over 80% of digital consumers interact with brands via social platforms weekly, generating massive data streams that traditional BI tools cannot analyze effectively. Social Business Intelligence platforms enable automated sentiment detection, trend forecasting, and influencer mapping, reducing response times by up to 40%. Marketing and customer experience teams increasingly depend on these insights to personalize engagement and protect brand reputation. As customer expectations for instant, relevant responses continue to rise, real-time social analytics has become essential to maintaining competitive positioning and operational agility.

Strict data protection regulations and heightened consumer awareness around privacy significantly constrain Social Business Intelligence adoption. Compliance with frameworks such as GDPR and emerging AI governance laws requires complex consent management, anonymization, and audit capabilities. Studies indicate that nearly 35% of enterprises delay social analytics deployments due to regulatory uncertainty and internal compliance gaps. Additionally, cross-border data transfer restrictions complicate global analytics operations. These governance challenges increase implementation complexity, extend deployment timelines, and raise operational costs, limiting adoption among highly regulated industries and smaller organizations with limited compliance resources.

AI-driven automation presents substantial growth opportunities by transforming social data into actionable intelligence with minimal human intervention. Automated insight generation can reduce analyst workload by nearly 50% while improving consistency and scalability. Industries such as retail, BFSI, and public sector communications are increasingly adopting predictive social analytics to anticipate demand shifts, fraud signals, and public sentiment trends. Emerging opportunities also exist in integrating social intelligence with enterprise AI copilots and decision-support systems. As organizations seek efficiency gains and faster insights, AI automation is expanding the addressable use cases and strategic value of Social Business Intelligence platforms.

Integration complexity remains a major challenge as Social Business Intelligence platforms must connect with CRM, ERP, marketing automation, and data lake environments. Nearly 45% of enterprises report delays due to system incompatibility or lack of standardized data models. Additionally, there is a persistent shortage of skilled professionals capable of interpreting advanced AI-driven social insights. Training and talent acquisition costs increase deployment risk and slow realization of value. These challenges can limit scalability and reduce ROI, particularly for organizations without mature data governance and analytics capabilities.

Platform Modularization and Composable Analytics Architectures

Enterprises are increasingly adopting modular and composable Social Business Intelligence architectures to improve deployment flexibility and reduce implementation risk. Around 58% of large organizations now prefer plug-and-play analytics modules that can be integrated with existing CRM, ERP, and marketing platforms. Modular deployment models have reduced average implementation timelines by nearly 32% and lowered internal customization workloads by 27%, enabling faster time-to-insight across multi-departmental use cases.

Automation of Insight Generation Through Advanced AI Models

Automation is reshaping how organizations extract value from social data. Nearly 64% of enterprises deploying Social Business Intelligence platforms now rely on automated insight generation rather than manual analysis. AI-driven models have improved sentiment classification accuracy by approximately 41% and reduced analyst intervention by 46%. This shift allows teams to process millions of daily interactions while maintaining consistent insight quality and faster response cycles.

Expansion of Real-Time Monitoring for Risk and Reputation Management

Real-time monitoring capabilities are gaining prominence as organizations prioritize proactive risk detection. Approximately 52% of enterprises now use Social Business Intelligence for real-time brand and crisis monitoring, compared to under 30% three years ago. Continuous monitoring systems have shortened incident detection times by 39% and reduced reputational impact severity by nearly 24%, particularly in highly visible consumer-facing industries.

Increased Alignment with Compliance, ESG, and Data Governance Objectives

Social Business Intelligence platforms are increasingly aligned with compliance and ESG mandates. Around 47% of new deployments include built-in data anonymization, audit logging, and ethical AI controls. Organizations report a 28% reduction in compliance review cycles and a 22% improvement in data governance efficiency by embedding regulatory controls directly into social analytics workflows, reinforcing responsible and sustainable intelligence practices.

The Social Business Intelligence Market is segmented by type, application, and end-user, reflecting the diverse ways organizations extract value from social data. By type, platforms vary based on analytical depth, data processing capability, and integration models, ranging from basic social monitoring tools to advanced AI-driven predictive intelligence systems. Application-wise, demand spans marketing optimization, customer experience management, risk and compliance monitoring, and strategic planning, with each use case requiring different analytical sophistication. From an end-user perspective, adoption is strongest among large enterprises with high-volume data needs, while SMEs and public-sector organizations are increasingly entering the market as cloud-based solutions reduce complexity and cost. Across all segments, measurable performance improvements—such as faster decision cycles, improved sentiment accuracy, and operational efficiency gains—are shaping purchasing decisions and platform differentiation.

The Social Business Intelligence Market by type includes descriptive social analytics, diagnostic and sentiment analysis platforms, predictive intelligence systems, and prescriptive or AI-augmented decision engines. Descriptive and diagnostic analytics currently represent the leading type, accounting for approximately 44% of total adoption, as organizations prioritize real-time dashboards, sentiment scoring, and trend visualization to monitor brand performance and public perception. Predictive intelligence platforms, which apply machine learning to forecast consumer behavior and reputational risks, are the fastest-growing type, expanding at an estimated CAGR of 31% due to rising demand for proactive decision-making and early-warning systems. Prescriptive and autonomous intelligence tools are emerging rapidly, driven by integration with enterprise AI copilots and workflow automation, while niche monitoring-only tools and legacy analytics collectively account for around 25% of adoption.

By application, marketing and brand management is the dominant segment, contributing close to 39% of overall usage, as organizations rely on social intelligence to optimize campaigns, influencer strategies, and audience targeting. Customer experience management follows, with approximately 26% share, supported by real-time feedback analysis and churn prediction capabilities. Risk, compliance, and public affairs monitoring is the fastest-growing application area, expanding at an estimated CAGR of 29%, driven by heightened regulatory scrutiny, misinformation risks, and reputational exposure across digital platforms. Strategic planning and product innovation applications, including demand sensing and feature feedback analysis, along with niche use cases such as HR branding and investor relations, together represent nearly 35% of the market.

Large enterprises remain the leading end-user segment, accounting for roughly 48% of Social Business Intelligence adoption, supported by their need to process high-volume, multi-language social data across global markets. These organizations leverage advanced analytics to align marketing, risk, and executive decision-making functions. Small and medium-sized enterprises represent the fastest-growing end-user group, expanding at an estimated CAGR of 33%, fueled by affordable cloud-based platforms and preconfigured analytics models. Government and public-sector bodies, media organizations, and non-profits collectively contribute around 30% of adoption, using social intelligence for citizen engagement, policy feedback, and reputation management.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 31% between 2026 and 2033.

Regional performance reflects differences in digital maturity, enterprise analytics adoption, regulatory environments, and data infrastructure readiness. North America processed over 45% of global enterprise social data volumes in 2025, supported by advanced cloud penetration above 85%. Europe followed with approximately 27% share, driven by compliance-focused analytics demand across regulated industries. Asia-Pacific contributed nearly 22% of global adoption, supported by more than 3.2 billion active social media users and strong mobile-first analytics usage. South America and the Middle East & Africa together represented close to 10%, with growth fueled by media digitization, public-sector engagement, and expanding e-commerce ecosystems.

How is advanced enterprise analytics shaping decision-making maturity across industries?

North America held approximately 41% of the Social Business Intelligence Market in 2025, supported by high enterprise adoption across healthcare, finance, retail, and technology sectors. More than 70% of large organizations in the region use social intelligence platforms for real-time customer sentiment and risk monitoring. Regulatory frameworks around data privacy and AI governance have encouraged investment in compliant analytics architectures rather than slowed adoption. Cloud-native AI platforms, real-time NLP engines, and integration with CRM systems are widely deployed. A leading regional software provider expanded AI-driven sentiment automation in 2024, reducing client response times by 36%. Consumer behavior shows stronger usage in healthcare and financial services, where reputation management and compliance monitoring are critical.

Why is explainability becoming a core requirement for advanced analytics adoption?

Europe accounted for nearly 27% of global Social Business Intelligence adoption in 2025, with Germany, the UK, and France representing over 60% of regional demand. Regulatory bodies enforcing strict data protection and AI transparency standards are shaping purchasing decisions. More than 65% of European enterprises prioritize explainable analytics models to meet compliance and audit requirements. Sustainability initiatives and ESG reporting mandates are increasing demand for sentiment and stakeholder intelligence tools. A regional analytics firm introduced explainable AI dashboards in 2024, improving regulatory reporting efficiency by 29%. Consumer behavior reflects cautious adoption, with preference for transparent, interpretable insights over black-box automation.

How is mobile-first digital behavior accelerating analytics adoption at scale?

Asia-Pacific ranked as the fastest-growing region, contributing about 22% of global Social Business Intelligence usage in 2025. China, India, and Japan collectively accounted for more than 68% of regional demand, driven by massive social media penetration and e-commerce activity. Over 75% of analytics interactions in the region originate from mobile platforms. Rapid expansion of cloud infrastructure and AI innovation hubs is enabling scalable social data processing. A regional technology firm deployed multilingual sentiment engines in 2024, supporting analytics across 12 local languages. Consumer behavior is strongly driven by e-commerce, influencer marketing, and mobile AI applications.

Why is localized content analysis critical for market relevance?

South America represented approximately 6% of global Social Business Intelligence adoption in 2025, with Brazil and Argentina accounting for nearly 70% of regional usage. Media, telecom, and consumer goods sectors are the primary adopters, using social intelligence for language-specific sentiment and campaign optimization. Government-led digital transformation programs and cross-border trade initiatives are supporting analytics adoption. A regional media analytics provider enhanced Spanish and Portuguese NLP accuracy by 33% in 2024. Consumer behavior highlights strong demand for localized language processing and culturally relevant sentiment interpretation.

How is digital modernization reshaping stakeholder engagement strategies?

The Middle East & Africa region contributed close to 4% of global Social Business Intelligence usage in 2025, with the UAE and South Africa leading adoption. Demand is rising across oil & gas, construction, tourism, and public-sector communications. National digital transformation strategies are accelerating cloud analytics investments, with enterprise adoption growing above 25% year-over-year in key markets. A regional digital services provider integrated social intelligence into smart city platforms, improving public feedback response rates by 21%. Consumer behavior varies widely, with higher enterprise usage in government and infrastructure-driven economies.

United States – 34% market share; driven by high enterprise-scale deployment, advanced AI infrastructure, and strong demand across finance, healthcare, and retail.

China – 16% market share; supported by massive social media user volumes, mobile-first analytics adoption, and strong integration with e-commerce ecosystems.

The Social Business Intelligence market exhibits a moderately fragmented competitive structure, characterized by a mix of global technology providers, specialized analytics vendors, and emerging AI-native firms. More than 120 active competitors operate globally, offering solutions ranging from social listening and sentiment analysis to advanced predictive and prescriptive intelligence platforms. The top five companies collectively account for approximately 55% of total market adoption, reflecting partial consolidation driven by enterprise-scale deployments and platform ecosystems.

Competition is increasingly shaped by innovation intensity rather than price alone. Over 60% of leading vendors launched AI-enhanced features between 2023 and 2025, including generative insight summaries, real-time multilingual sentiment engines, and automated risk alerts. Strategic partnerships are common, with nearly 40% of major players integrating their platforms with CRM, marketing automation, or cloud hyperscaler ecosystems to expand enterprise reach. Mergers and acquisitions activity remains selective, focusing on niche AI capabilities and regional data expertise rather than large-scale consolidation.

Market positioning varies by depth of analytics and compliance readiness. Enterprise-focused vendors emphasize scalability, governance, and explainable AI, while mid-market players compete on ease of deployment and modular pricing. Innovation trends such as autonomous analytics, social graph intelligence, and ESG-aligned reporting continue to redefine competitive differentiation and long-term positioning.

Salesforce

Microsoft

IBM

SAP

Oracle

Sprinklr

Meltwater

Brandwatch

Talkwalker

Sprout Social

Technology evolution is a central force shaping the Social Business Intelligence Market, with enterprises increasingly deploying advanced analytics to extract value from high-volume, unstructured social data. Artificial intelligence and machine learning remain foundational, with more than 65% of deployed platforms now using deep learning models to classify sentiment, intent, and emotion across text, image, and video formats. Natural language processing capabilities have advanced significantly, supporting real-time analysis in over 40 languages and improving sentiment accuracy by approximately 35% compared to earlier keyword-based systems.

Generative AI is emerging as a transformative layer within Social Business Intelligence platforms. Nearly 48% of large enterprises now use generative models to automatically summarize social trends, generate executive-ready insights, and simulate campaign or crisis scenarios. These capabilities have reduced analyst workload by close to 45% and shortened insight delivery cycles by 30%. Computer vision technologies are also gaining traction, enabling logo detection, visual sentiment scoring, and brand exposure analysis across image- and video-based social content, which now represents more than 55% of total social media interactions.

Cloud-native architectures and real-time data streaming frameworks are further enhancing scalability and responsiveness. Over 70% of new deployments are cloud-based, allowing platforms to process millions of social interactions per hour with latency below two seconds. From a governance perspective, explainable AI, data anonymization, and automated compliance controls are increasingly embedded, with 52% of platforms offering built-in audit trails and ethical AI monitoring. Together, these technologies position Social Business Intelligence as a strategic, future-ready capability for insight-driven and compliant enterprise decision-making.

• In September 2024, Salesforce launched an upgraded version of its Social Studio platform, introducing enhanced predictive analytics and seamless integration with Customer 360 across social channels, enabling automated journey mapping based on social engagement and personalized multi-touchpoint strategies.

• In March 2025, Microsoft expanded its business intelligence ecosystem with two AI-driven tools—Researcher and Analyst—within Microsoft 365 Copilot, aimed at deep research and advanced data analysis for enterprise strategy and performance reporting, incorporating internal and third-party social data.

• In May 2025, Meltwater launched Mira, an AI-powered conversational assistant designed to streamline social and media intelligence workflows, delivering faster trend analysis, automated brand monitoring, and simplified insights for enterprise and mid-market users.

• In June 2025, Adobe and IBM expanded their strategic collaboration by integrating IBM’s Watson AI into the Adobe Experience Platform, strengthening personalized marketing, governance controls, and workflow automation for enhanced social intelligence across hybrid environments.

The scope of the Social Business Intelligence Market Report encompasses a comprehensive assessment of solution types, deployment models, applications, end-user sectors, and geographic regions, offering decision-makers clear visibility into strategic trends and operational priorities. The report segments the market by type, including core analytics platforms, social listening modules, predictive intelligence systems, and AI-augmented insight engines that support real-time sentiment interpretation and trend forecasting. By deployment, both cloud-native and hybrid offerings are evaluated, highlighting how scalability, latency improvements, and data streaming technologies are influencing adoption across industries.

Application coverage includes marketing optimization, customer experience and loyalty measurement, risk and compliance monitoring, competitive benchmarking, and strategic planning. The report provides industry breakdowns such as retail and e-commerce, BFSI, healthcare, IT & telecommunications, and public sector intelligence programs, showing how tailored social intelligence use cases vary in frequency and impact. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with numerical insights into adoption intensity, mobile-driven analytics usage, and regional technology readiness. Emerging niches like multimodal social analytics (text + image + video), generative insight summarization, and cross-system CRM integration are also examined.

The report’s breadth includes evaluation of technological enablers—AI/ML, NLP, automated compliance, and governance frameworks—and end-user behavior patterns such as real-time engagement monitoring and sentiment-triggered alerts. Its structured focus on both strategic priorities and operational metrics makes it a valuable resource for executives, analysts, and IT leaders planning investments, platform selection, or competitive positioning in social-driven business intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

27.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Salesforce, Microsoft, IBM, SAP, Oracle, Sprinklr, Meltwater, Brandwatch, Talkwalker, Sprout Social |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |