Reports

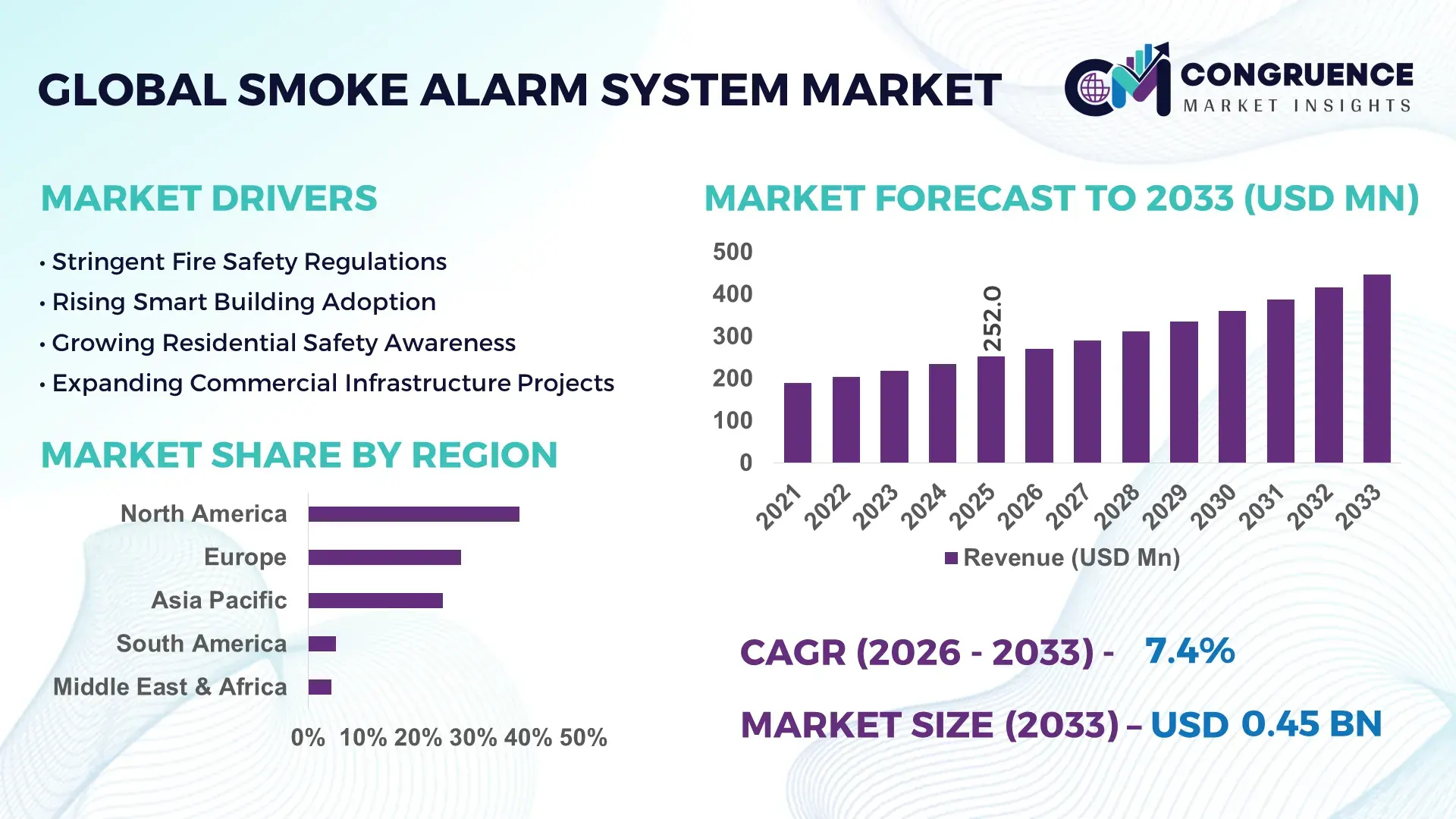

The Global Smoke Alarm System Market was valued at USD 252.0 Million in 2025 and is anticipated to reach a value of USD 447.1 Million by 2033 expanding at a CAGR of 7.43% between 2026 and 2033. Growth is being driven by stricter residential fire-safety mandates, accelerated smart-building deployments, and rising integration of wireless interconnected alarm networks across commercial infrastructure.

The United States dominates the global smoke alarm system landscape, accounting for approximately 32% of installed smoke alarm units worldwide, supported by more than 145 million housing units and widespread compliance with National Fire Protection Association (NFPA) standards. Smart alarm penetration in new residential construction exceeds 38%, compared with approximately 24% in Germany, highlighting faster digital safety adoption. Following recent building-safety upgrades and wildfire-related preparedness measures, large-scale retrofitting activity has further strengthened deployment density across urban and suburban properties.

This positions manufacturers to prioritize connected-device ecosystems, compliance-driven product portfolios, and retrofit-focused distribution strategies to secure long-term competitive advantage.

Market Size & Growth: USD 252.0 Million in 2025 reaching USD 447.1 Million by 2033, supported by 7.43% CAGR and accelerated adoption of interconnected smart safety systems.

Top Growth Drivers: Smart-home installations +38%, commercial building compliance activity +31%, wireless alarm adoption +27%.

Short-Term Forecast: By 2028, cloud-connected monitoring deployments are expected to improve incident response efficiency by nearly 22%.

Emerging Technologies: AI-powered smoke differentiation, IoT-enabled wireless networking, and predictive maintenance analytics are reshaping advanced fire detection.

Regional Leaders: North America exceeds USD 145 Million, Europe approaches USD 108 Million, and Asia-Pacific surpasses USD 95 Million, driven by modernization and urban safety investments.

Consumer/End-User Trends: More than 41% of new residential projects incorporate interconnected alarm systems as standard installations.

Pilot/Case Example: In 2024, smart-building fire safety deployments reduced false alarm incidents by approximately 18% through sensor analytics integration.

Competitive Landscape: Top manufacturers collectively control nearly 45% market share, led by Kidde, Honeywell, Siemens, Johnson Controls, and Schneider Electric.

Regulatory & ESG Impact: Updated building codes improved compliance-driven installations by over 20% across major developed markets.

Investment & Funding: More than USD 800 Million has been directed toward smart-building safety technologies, digital monitoring platforms, and manufacturing expansion.

Innovation & Future Outlook: Multi-sensor detection, edge analytics, and remote diagnostics are accelerating the shift toward intelligent fire-safety ecosystems.

Smoke Alarm System Market demand is expanding across residential complexes, commercial facilities, healthcare campuses, educational institutions, and smart-city infrastructure projects. Manufacturers are introducing AI-assisted detection, wireless mesh connectivity, and smartphone-integrated monitoring solutions to reduce nuisance alarms and improve response accuracy. Nearly 35% of newly launched premium systems now include remote diagnostics capabilities. Increasing building-code enforcement and localized electronics manufacturing initiatives are further reshaping procurement priorities, setting the stage for broader strategic market transformation.

Smoke alarm systems are becoming strategically important as governments, insurers, developers, and facility operators place greater emphasis on life-safety compliance and asset protection. Building modernization programs, stricter fire-safety regulations, and smart infrastructure investments are transforming smoke detection from a standalone safety product into a connected operational technology platform. The market is increasingly linked to digital building management ecosystems, creating new competitive opportunities for technology-focused manufacturers.

Modern multi-sensor smoke alarms deliver up to 30% fewer false alarms than conventional ionization-based systems while improving detection accuracy in mixed-use environments. The United States leads large-scale deployment through stringent code enforcement and retrofit activity, whereas China is rapidly expanding production capacity and smart-building integration. Over the next two to three years, wireless interconnected installations are expected to represent more than 45% of newly deployed systems, reflecting a clear shift toward networked safety infrastructure.

A practical example is the deployment of cloud-connected smoke alarm networks across educational and healthcare facilities, enabling centralized monitoring and faster maintenance scheduling. Companies are responding through strategic partnerships with IoT platform providers, software developers, and building automation specialists. Organizations that successfully combine compliance expertise, digital connectivity, and scalable product ecosystems will strengthen competitive positioning and secure lasting operational advantages.

Mandatory smoke alarm installation requirements and building-safety modernization initiatives remain the strongest market catalyst. More than 70% of developed economies enforce residential smoke alarm regulations, while smart-building investments have increased by approximately 25% over the past three years. The United States continues expanding retrofit programs following updated fire-safety assessments, and Australia has strengthened interconnected alarm requirements in residential properties. This regulatory push directly increases replacement cycles and technology upgrades. In response, manufacturers are expanding wireless product portfolios, investing in cloud-based monitoring capabilities, and partnering with construction firms. A notable strategic insight is that compliance-driven retrofits generate higher recurring replacement demand than new construction projects, improving long-term market stability and product lifecycle revenues.

Installation costs remain a significant barrier, particularly in price-sensitive residential markets and aging commercial facilities. Connected smoke alarm systems can cost 20–35% more than conventional standalone devices, while integration expenses account for nearly 15% of total deployment budgets in retrofit projects. Supply-chain disruptions affecting semiconductor components and wireless communication modules have periodically increased procurement lead times. These constraints impact deployment scalability and delay modernization initiatives. To mitigate risk, manufacturers are localizing production, securing multi-year component contracts, and developing modular architectures that reduce installation complexity. A critical operational insight is that interoperability limitations between legacy fire systems and new smart devices continue to restrict adoption speed in older building stock.

The convergence of IoT, artificial intelligence, and building automation creates substantial expansion opportunities beyond traditional alarm hardware. Nearly 40% of commercial property operators are evaluating centralized safety-monitoring platforms that integrate smoke detection with broader facility management systems. China and India are accelerating smart-city investments, while advanced wireless technologies can reduce installation labor requirements by approximately 25%. AI-powered smoke classification and predictive maintenance solutions represent the next innovation wave, improving operational efficiency and reducing nuisance alarms. Companies are increasing R&D spending, forming software partnerships, and building ecosystem-based service models. A unique strategic opportunity lies in subscription-based monitoring services, which generate recurring value beyond one-time hardware sales.

As smoke alarm systems become increasingly connected, maintaining cybersecurity, interoperability, and operational consistency presents a major execution challenge. More than 60% of facility managers identify integration complexity as a key concern when deploying smart safety infrastructure. Connected devices expand potential cyberattack surfaces, while fragmented communication standards complicate multi-vendor deployments. Large commercial campuses often require integration across dozens of safety and building-management subsystems, increasing implementation complexity and maintenance requirements. Companies must invest in secure firmware architectures, standardized communication protocols, and workforce training programs to ensure reliable performance. The strongest strategic challenge is balancing advanced connectivity with system resilience, as long-term competitiveness increasingly depends on secure and seamless ecosystem integration rather than hardware capability alone.

Smart Interconnected Alarm Networks Wireless interconnected smoke alarm deployments increased by nearly 34% across newly constructed residential and mixed-use buildings during 2025. Property developers are replacing standalone devices with networked systems capable of whole-building alerts and centralized monitoring. Updated housing safety regulations in the United States and the United Kingdom accelerated adoption, while manufacturers expanded cloud-enabled platforms and installer partnerships. The shift improves response coordination, reduces maintenance visits by approximately 20%, and strengthens lifecycle service opportunities.

AI-Driven False Alarm Reduction Advanced multi-sensor systems using AI-assisted smoke differentiation recorded false alarm reductions of 25–30% compared with conventional detectors. Commercial facilities increasingly prioritize nuisance-alarm mitigation due to operational disruption costs and compliance requirements. Enterprise customers are integrating smoke detection with building management software, enabling automated event verification. In response, technology providers are investing in machine-learning algorithms and edge-processing capabilities to improve detection precision while lowering unnecessary emergency dispatches.

Retrofit-Focused Compliance Upgrades More than 40% of smoke alarm installations in mature housing markets now originate from retrofit projects rather than new construction. Aging building stock and stricter fire-safety inspections are accelerating replacement cycles. Large property owners are standardizing interconnected alarm infrastructure across portfolios to simplify maintenance workflows. Manufacturers are responding through modular product designs, faster installation architectures, and expanded contractor networks that reduce deployment time by nearly 18%.

Integration With Building Automation Approximately 37% of newly deployed commercial smoke alarm systems are connected to broader building automation ecosystems. Facility operators increasingly link fire detection, HVAC controls, access management, and emergency notification systems into unified platforms. Labor shortages in facility management are driving demand for centralized operational visibility. Companies are forming partnerships with automation vendors and software integrators, creating scalable safety ecosystems that improve monitoring efficiency while supporting predictive maintenance and compliance reporting.

Photoelectric smoke alarm systems hold the largest market share, accounting for approximately 46% of global installations due to superior performance in detecting smoldering fires, lower nuisance alarm rates, and strong alignment with evolving residential safety standards. Their scalability across residential, commercial, and institutional facilities supports widespread adoption, particularly in the United States and Australia where code-driven installation requirements continue expanding. Manufacturers are prioritizing photoelectric product portfolios through sensor enhancements, wireless connectivity, and smart-home integration capabilities. Ionization alarms remain relevant in cost-sensitive deployments, representing nearly 28% of installed units, although replacement activity is gradually reducing their share in mature markets. Dual-sensor smoke alarm systems are the fastest-growing segment, supported by growing demand for comprehensive fire detection capabilities across commercial infrastructure and healthcare facilities. Combining photoelectric and ionization technologies improves detection coverage while reducing operational risks. Adoption within large enterprise projects increased by nearly 22% during 2025 as facility managers emphasized regulatory compliance and occupant safety. Smart multi-sensor products incorporating heat and carbon monoxide detection are also gaining traction, prompting manufacturers to expand R&D investments and strengthen distribution partnerships focused on premium safety solutions.

Residential applications represent the largest segment, contributing approximately 55% of global smoke alarm system deployments. Demand concentration stems from mandatory building-code compliance, replacement cycles, and increasing smart-home adoption. More than 60% of newly constructed housing units in developed markets now incorporate interconnected smoke alarm configurations as standard installations. Manufacturers are scaling direct-to-consumer channels, expanding retail partnerships, and introducing app-enabled monitoring features to strengthen engagement and replacement demand. Residential adoption continues benefiting from insurance incentives and government-led fire-safety awareness programs. Commercial applications are the fastest-growing segment, supported by digital building modernization and stricter safety compliance requirements. Deployment activity across offices, hospitality facilities, healthcare institutions, and educational campuses increased by approximately 24% during 2025. Industrial applications maintain strategic relevance where smoke detection is integrated into broader facility risk-management frameworks, while public infrastructure projects are increasingly adopting centralized monitoring systems. Vendors are responding through cloud-connected monitoring platforms, enterprise service agreements, and integrated safety-management solutions that improve operational oversight and maintenance efficiency.

Residential building owners remain the dominant end-user group, accounting for nearly 48% of total purchasing activity due to extensive housing inventories, recurring replacement requirements, and regulatory compliance obligations. Demand is particularly concentrated in the United States, Canada, and the United Kingdom, where interconnected alarm standards continue expanding. Property owners increasingly prioritize wireless systems that simplify installation and reduce maintenance complexity. Manufacturers are supporting this segment through cost-optimized product lines, smart-home compatibility, and expanded installer ecosystems designed to improve customer retention and lifecycle engagement. Commercial facility operators represent the fastest-growing end-user category, supported by infrastructure modernization initiatives and enterprise risk-management priorities. Adoption across healthcare facilities, educational institutions, logistics centers, and hospitality assets increased by approximately 21% during 2025. Industrial operators remain important buyers due to safety-critical operational environments, while government and public-sector organizations continue upgrading aging safety infrastructure. Companies are responding through customized enterprise solutions, long-term maintenance agreements, and strategic partnerships with building automation providers to strengthen competitive positioning and capture higher-value contracts.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America maintains its leadership position with approximately 38.4% of global market demand, supported by mature fire-safety regulations, extensive residential deployment, and rapid adoption of interconnected alarm technologies. The region benefits from a large installed base requiring periodic upgrades, creating consistent replacement demand. More than 60% of newly constructed residential properties now incorporate interconnected smoke alarm systems as standard safety infrastructure. Commercial facility modernization programs are further accelerating deployment across healthcare, education, and hospitality sectors. Manufacturers are expanding cloud-enabled monitoring capabilities and strengthening partnerships with building automation providers to improve operational visibility. A notable trend is the growing integration of smoke detection with centralized facility management platforms to streamline compliance and maintenance workflows.

United States Market Outlook: The United States represents the region’s largest deployment hub due to stringent fire-safety standards, extensive housing stock, and strong smart-home adoption. More than 145 million housing units create significant replacement and retrofit opportunities. Interconnected alarm penetration exceeds 38% in new residential developments, while commercial property operators increasingly deploy centralized monitoring systems. Technology providers are investing in AI-enabled detection, wireless networking, and remote diagnostics solutions to improve detection accuracy and lifecycle efficiency. Strong insurance-driven compliance requirements continue reinforcing long-term market demand.

Europe accounts for approximately 27.8% of global smoke alarm system demand, supported by strict building-safety frameworks, modernization initiatives, and increasing adoption of intelligent fire-detection technologies. Regulatory enforcement across residential and public infrastructure projects continues driving replacement activity. More than 55% of large commercial renovation projects now include upgrades to integrated fire-safety systems. Sustainability-focused building modernization programs are also encouraging deployment of energy-efficient connected devices. Companies are responding through expanded wireless product portfolios, localized manufacturing strategies, and partnerships with facility-management providers. Growing demand for interoperable systems is encouraging wider integration with smart-building infrastructure and emergency communication platforms.

Germany Market Outlook: Germany remains the region’s most strategically significant market due to its strong regulatory environment, advanced building infrastructure, and leadership in industrial automation. Smoke alarm installation mandates across federal states have strengthened penetration rates in residential properties. More than 70% of multi-family housing developments include modern interconnected detection systems. German enterprises increasingly prioritize integration between smoke detection and building-management technologies, creating demand for intelligent monitoring solutions. Domestic engineering expertise and strong compliance culture continue supporting premium product adoption and technological advancement.

Asia-Pacific represents approximately 24.5% of global market activity and is emerging as the fastest-expanding regional market. Rapid urbanization, large-scale residential construction, and expanding smart-city investments are increasing deployment volumes across multiple countries. The region also serves as a major manufacturing base for electronic safety devices, supporting cost competitiveness and supply-chain efficiency. During 2025, smart-building safety deployments increased by nearly 28% across key metropolitan markets. Governments are strengthening fire-safety standards for high-density developments, while manufacturers are expanding production facilities and distribution networks. Increased adoption of wireless systems is improving installation speed and reducing infrastructure complexity.

China Market Outlook: China leads regional demand through its extensive construction sector, manufacturing scale, and smart-city development programs. The country accounts for a substantial share of global smoke alarm production capacity and continues investing heavily in digital infrastructure. More than 40% of newly approved smart-building projects incorporate connected fire-safety technologies. Domestic manufacturers are strengthening sensor innovation capabilities and expanding export operations. Government-backed urban modernization programs and increasing enterprise safety requirements continue supporting sustained deployment across residential, industrial, and commercial environments.

South America contributes approximately 5.1% of global market demand, with adoption increasingly driven by commercial construction, industrial modernization, and evolving safety standards. Deployment activity remains concentrated in major urban centers where infrastructure investments and compliance awareness are highest. Nearly 22% of recent commercial building projects incorporated upgraded smoke detection systems as part of broader safety modernization efforts. However, uneven regulatory enforcement and budget limitations continue affecting deployment consistency across several countries. Suppliers are addressing these challenges through distributor partnerships, localized support networks, and cost-efficient wireless product offerings that reduce installation complexity.

Brazil Market Outlook: Brazil is the largest and most influential market within South America due to its industrial scale, commercial infrastructure base, and growing focus on workplace safety compliance. Large metropolitan regions continue investing in healthcare, hospitality, and mixed-use development projects requiring advanced fire-safety systems. Commercial installation activity increased by approximately 18% during recent modernization initiatives. Vendors are strengthening local partnerships and expanding technical support capabilities to improve market penetration. Increasing awareness of property-risk management is also encouraging broader adoption among enterprise customers.

The Middle East & Africa region accounts for approximately 4.2% of global market demand, supported by infrastructure expansion, urban development projects, and modernization of commercial facilities. Large-scale construction initiatives are increasing demand for advanced smoke detection systems integrated with intelligent building platforms. More than 30% of newly commissioned premium commercial developments now include connected life-safety ecosystems. Investments in transportation hubs, hospitality assets, and mixed-use developments continue driving deployment activity. Companies are expanding regional distribution networks and forming strategic alliances with engineering and construction firms to support complex project requirements.

Saudi Arabia Market Outlook: Saudi Arabia serves as the region’s primary growth engine due to extensive infrastructure investments, smart-city initiatives, and large-scale real estate development programs. Major urban development projects are accelerating deployment of integrated fire-safety technologies across residential, commercial, and public facilities. More than 35% of new high-value construction projects include advanced interconnected alarm systems linked to centralized monitoring platforms. Regulatory modernization and strong investment momentum are encouraging technology adoption, while international suppliers continue expanding partnerships and localized service capabilities to support long-term project pipelines.

The Smoke Alarm System Market is characterized by competition between global fire-safety leaders such as Honeywell International, Johnson Controls, Siemens, Schneider Electric, and Carrier Global against regional manufacturers and cost-focused suppliers. The top five players collectively control approximately 42–47% of global market activity. Competition is increasingly centered on connected detection platforms, where smart-enabled products command adoption rates nearly 30% higher than conventional alarms. Premium vendors compete through cloud connectivity, AI-enabled diagnostics, and integrated building-management ecosystems, while regional manufacturers emphasize pricing advantages often 15–20% lower. Companies are expanding through technology partnerships, software integration, localized manufacturing, and vertical service offerings.

The competitive shift is moving from standalone hardware toward intelligent life-safety ecosystems with predictive maintenance capabilities. Certification requirements, regulatory compliance, and established distribution networks remain significant entry barriers. Winning requires superior interoperability, regulatory credibility, connected-service capabilities, and scalable deployment support rather than competing solely on device cost.

Johnson Controls

Siemens Smart Infrastructure

Carrier Global (Kidde)

Schneider Electric

Halma plc

Hochiki Corporation

Nittan Company Ltd.

Gentex Corporation

BRK Brands (First Alert)

Robert Bosch GmbH

ABB Ltd.

Eaton Corporation

Hikvision Digital Technology

Current technology development is centered on photoelectric detection, wireless interconnectivity, and cloud-enabled monitoring platforms. More than 40% of newly deployed premium smoke alarm systems now include wireless networking capabilities that enable synchronized alerts and centralized monitoring. Compared with traditional standalone alarms, interconnected systems improve occupant notification coverage by approximately 25% while reducing maintenance inspection time by nearly 20%. Manufacturers benefit through recurring service opportunities and stronger customer retention.

Emerging technologies include AI-assisted smoke classification, edge analytics, and multi-sensor detection combining smoke, heat, and carbon monoxide monitoring. These systems reduce nuisance alarms by 25–30% compared with legacy detection technologies, improving user confidence and operational reliability. Adoption is accelerating within healthcare facilities, educational institutions, and smart commercial buildings, where integrated life-safety infrastructure is becoming operationally critical. Technology leaders such as Siemens, Honeywell, and Johnson Controls are leveraging software-driven differentiation to strengthen competitive positioning.

Between 2026 and 2028, disruptive innovation will increasingly focus on predictive maintenance, cloud diagnostics, and autonomous building integration. IoT-connected detectors capable of continuous self-testing and remote diagnostics can reduce service interventions by more than 15%. Growing integration with building management systems will create operational advantages through automated incident response and compliance reporting. Organizations adopting these technologies early will benefit from faster deployment, lower lifecycle costs, and stronger facility-wide safety visibility as intelligent fire-safety ecosystems become the industry standard.

January 2025 – Carrier Global (Kidde) partnered with Ring to launch smart smoke and smoke/CO alarms with Wi-Fi connectivity and mobile notifications. Devices entered the market at prices starting around USD 54.97, expanding connected home safety adoption and strengthening Kidde’s smart-device ecosystem.

March 2025 – Johnson Controls introduced expanded industry-specific fire and safety solutions for healthcare and correctional facilities, integrating connected sprinkler and digital monitoring technologies. The initiative targets operational efficiency improvements through centralized building safety management and supports modernization of aging infrastructure. Source: www.johnsoncontrols.com

June 2025 – Johnson Controls relaunched its Connected Sprinkler service featuring real-time monitoring and predictive maintenance capabilities. The platform enables continuous system visibility and reduces emergency maintenance requirements, helping facility operators shift from reactive to proactive fire-safety management.

March 2026 – Siemens unveiled the Sinteso Nova and Cerberus Nova detector portfolio featuring full IoT connectivity, 24/7 self-checks, real-time monitoring, remote diagnostics, and predictive maintenance. The launch advances autonomous building readiness and strengthens Siemens’ position in connected fire-safety infrastructure.

The report provides comprehensive coverage of the global Smoke Alarm System Market across major product types, applications, end-user categories, and regional markets. It evaluates deployment trends across residential, commercial, industrial, and public infrastructure environments while assessing adoption patterns for photoelectric, ionization, dual-sensor, and smart interconnected technologies. The analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global deployment activity.

The study examines competitive positioning, technology evolution, regulatory developments, supply-chain dynamics, and enterprise adoption strategies between 2026 and 2033. It includes detailed assessment of connected safety platforms, AI-enabled detection systems, cloud-based monitoring solutions, and building automation integration trends. With analysis of leading manufacturers, emerging technology providers, deployment concentrations, and investment priorities, the report supports market-entry planning, product development decisions, partnership evaluation, expansion strategies, and long-term competitive positioning within the evolving life-safety ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 252.0 Million |

| Market Revenue (2033) | USD 447.1 Million |

| CAGR (2026–2033) | 7.43% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Honeywell International; Johnson Controls; Siemens Smart Infrastructure; Carrier Global (Kidde); Schneider Electric; Halma plc; Hochiki Corporation; Nittan Company Ltd.; Gentex Corporation; BRK Brands (First Alert); Robert Bosch GmbH; ABB Ltd.; Eaton Corporation; Hikvision Digital Technology |

| Customization & Pricing | Available on Request (10% Customization Free) |