Reports

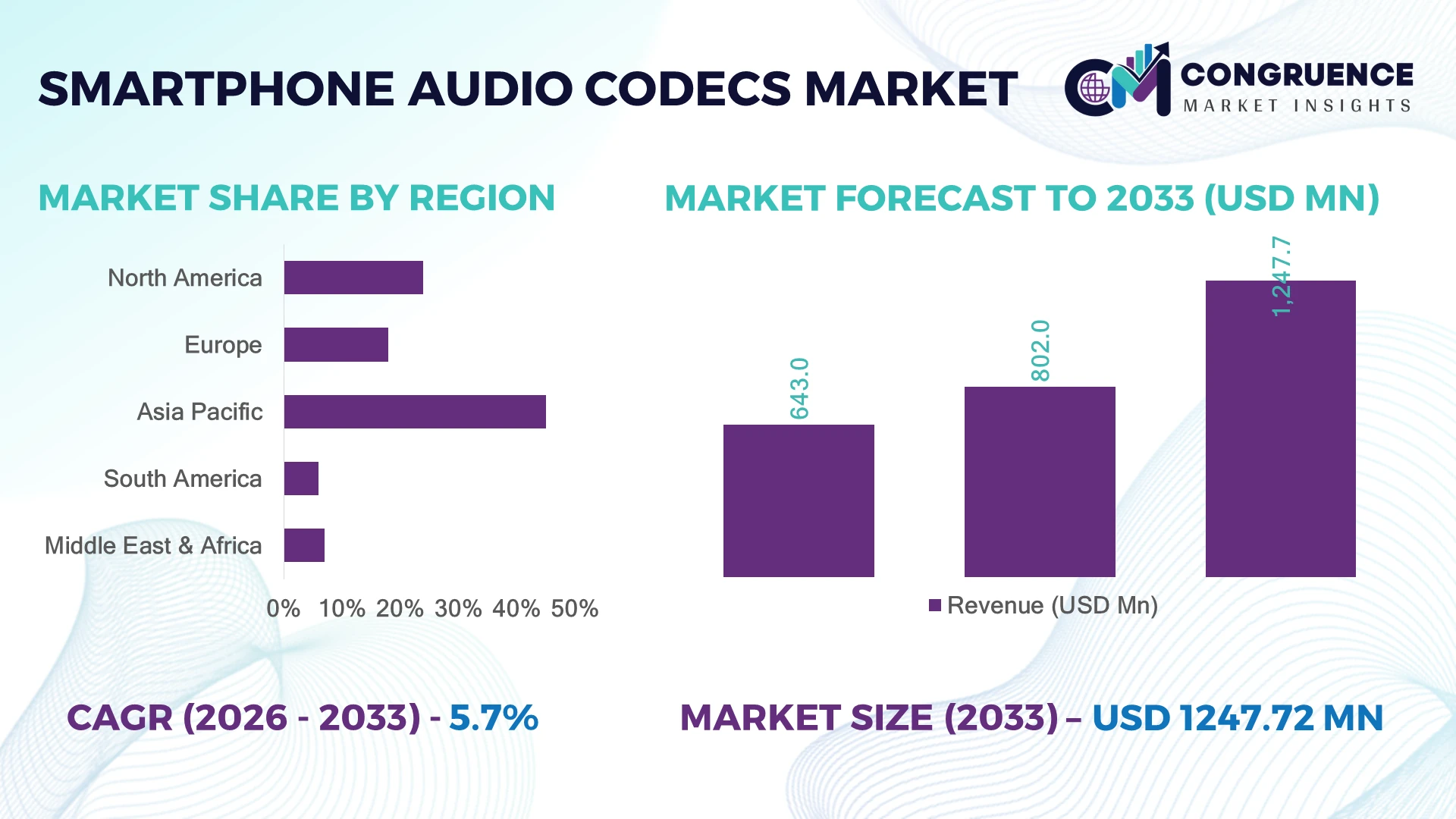

The Global Smartphone Audio Codecs Market was valued at USD 802.0 Million in 2025 and is anticipated to reach a value of USD 1,247.7 Million by 2033 expanding at a CAGR of 5.68% between 2026 and 2033. Growth is driven by rising adoption of high-resolution audio smartphones, advanced Bluetooth codecs, AI-powered sound optimization, and integration of low-power audio processing chips in premium and mid-range devices.

China dominates the market with approximately 32% share, supported by large-scale smartphone manufacturing capacity, semiconductor investments, and advanced consumer electronics ecosystems. The country produced over 1.4 billion smartphones historically and continues expanding domestic chip capabilities under initiatives such as China’s semiconductor self-reliance programs. India follows with around 12% share, driven by smartphone assembly expansion and 5G adoption, while South Korea maintains leadership in premium audio innovation.

Strategic implication: Companies strengthening codec efficiency, chip integration, and regional supply networks will gain competitive advantage in the evolving smartphone audio ecosystem.

Market Size & Growth: The global market reaches USD 802.0 Million in 2025 and USD 1,247.7 Million by 2033 at 5.68% CAGR, driven by AI audio processing and high-resolution mobile entertainment.

Top Growth Drivers: Wireless audio adoption 35%, premium smartphone upgrades 28%, and AI-enabled audio features 22% are key growth contributors.

Short-Term Forecast: By 2028, smartphone audio codec integration efficiency improves 20% through optimized chip architectures and advanced compression technologies.

Emerging Technologies: AI noise cancellation, Bluetooth LE Audio, and next-generation low-power codec designs are reshaping high-growth smartphone audio experiences.

Regional Leaders: Asia Pacific reaches USD 720 Million by 2033 through manufacturing expansion; North America reaches USD 280 Million through premium device adoption; Europe reaches USD 190 Million through advanced audio standards.

Consumer/End-User Trends: Over 60% of premium smartphone users prioritize enhanced audio quality, spatial sound, and wireless audio compatibility.

Pilot/Case Example: In 2024, smartphone manufacturers implementing AI-based audio enhancement achieved up to 30% improvement in voice clarity and noise reduction performance.

Competitive Landscape: Qualcomm leads with approximately 25% share, alongside Cirrus Logic, MediaTek, Realtek, and Dolby Laboratories shaping codec innovation.

Regulatory & ESG Impact: Energy-efficient codec architectures reduce audio processing power consumption by nearly 15%, supporting sustainability goals across electronics supply chains.

Investment & Funding: Over USD 2 billion in semiconductor and mobile technology investments accelerate codec development, partnerships, and regional manufacturing expansion.

Innovation & Future Outlook: Next-generation codecs focus on immersive audio, edge AI processing, and integrated smartphone-to-device audio ecosystems.

The Smartphone Audio Codecs Market is advancing through demand for immersive entertainment, improved communication quality, and efficient mobile audio processing. Recent innovations include AI-driven sound personalization, adaptive noise cancellation, and Bluetooth LE Audio integration, with wireless audio device usage exceeding 70% among smartphone users in leading markets. Supply-chain diversification across Asia and semiconductor localization initiatives are accelerating technology availability and product innovation.

The Smartphone Audio Codecs Market is becoming strategically important as smartphone manufacturers compete through differentiated user experiences beyond displays and processors. Advanced audio capabilities, including immersive sound, AI-based enhancement, and ultra-low-power processing, are becoming major factors influencing premium device positioning and consumer loyalty. Supply-chain restructuring and regional semiconductor expansion are also reshaping sourcing strategies.

Modern audio codecs deliver significant advantages over legacy solutions by improving compression efficiency and reducing processing power requirements by approximately 15–25% while maintaining higher sound quality. Asia Pacific leads in manufacturing scale, supported by China, South Korea, and India, whereas North America emphasizes advanced chip design and software-driven audio innovation.

Over the next 2–3 years, smartphone brands will prioritize integrated audio platforms, strategic semiconductor partnerships, and localized component ecosystems. For example, manufacturers adopting AI-powered codec solutions are improving real-time voice communication and gaming audio performance while reducing energy consumption. Companies are increasing investments in chipset alliances, Bluetooth technology development, and customized audio solutions to strengthen market differentiation.

The long-term strategic pathway depends on combining efficient hardware architectures, intelligent software algorithms, and resilient supply networks to achieve stronger competitive positioning in the global smartphone ecosystem.

The rapid integration of AI-powered audio algorithms and advanced wireless connectivity is accelerating smartphone audio codec adoption. Premium smartphones increasingly incorporate intelligent noise cancellation, spatial audio, and adaptive sound processing, with AI audio features expanding across more than 40% of flagship devices. Bluetooth LE Audio adoption is improving power efficiency by nearly 20% compared with previous wireless standards. Companies such as Qualcomm, MediaTek, and Cirrus Logic are expanding codec partnerships and investing in low-power semiconductor architectures. The shift toward immersive mobile entertainment and gaming ecosystems is pushing manufacturers to prioritize integrated codec solutions as a key product differentiation strategy.

Smartphone audio codec development faces challenges from semiconductor supply dependency, interoperability issues, and rising component complexity. Advanced codec chips require specialized fabrication capabilities, while supply disruptions have affected approximately 10–15% of electronics component planning cycles in recent years. Differences among Android manufacturers, operating systems, and wireless audio standards create additional integration costs. Companies in China, South Korea, and Taiwan are addressing these limitations through supplier diversification, localized chip development, and long-term manufacturing agreements. A critical operational challenge remains balancing higher audio performance with affordable device pricing, especially as mid-range smartphone manufacturers manage component cost pressures.

Emerging opportunities are developing through AI-driven personalization, spatial audio adoption, and smart device ecosystem integration. More than 50% of premium smartphone users increasingly engage with wireless audio products, creating demand for advanced codec compatibility and optimized sound experiences. India’s expanding 5G smartphone market and growing digital entertainment sector provide new opportunities for codec suppliers to scale affordable high-performance solutions. Companies are increasing R&D investments in edge AI audio processing, Bluetooth LE Audio platforms, and integrated chipset solutions. The strategic opportunity lies in developing energy-efficient codecs that enable premium audio features in mass-market smartphones without significantly increasing hardware complexity.

Long-term growth faces execution challenges related to hardware-software integration, cybersecurity requirements, and evolving audio standards. Modern smartphones combine multiple audio technologies, increasing validation complexity by nearly 30% compared with traditional codec architectures. Manufacturers must ensure compatibility across smartphones, earbuds, gaming devices, and connected platforms while maintaining consistent performance. Regulatory developments around device efficiency and electronic sustainability are also influencing chipset design priorities. Companies are responding through ecosystem partnerships, expanded testing infrastructure, and investments in adaptable codec frameworks. The key strategic challenge is creating scalable audio platforms that support future technologies without increasing manufacturing complexity or reducing device reliability.

AI Audio Optimization Growth: Smartphone manufacturers are integrating AI-based audio enhancement engines, with more than 40% of flagship devices adopting intelligent noise reduction and adaptive sound processing features. This shift improves voice clarity, gaming performance, and personalized listening experiences while reducing manual audio tuning requirements. Companies are expanding AI partnerships and embedding machine-learning algorithms directly into audio chipsets to accelerate premium device differentiation.

Bluetooth LE Audio Transition: The adoption of Bluetooth LE Audio and advanced wireless codec standards is increasing, improving energy efficiency by approximately 20–30% compared with earlier wireless audio technologies. Smartphone brands are restructuring audio ecosystems around earbuds, wearables, and connected devices, while suppliers are scaling low-power codec solutions to support multi-device connectivity and longer battery performance.

Chip Integration Expansion: Smartphone chipset suppliers are moving toward integrated audio architectures, reducing component complexity by nearly 15% and improving manufacturing efficiency. Companies in China, South Korea, and Taiwan are strengthening semiconductor partnerships to address supply-chain pressure and shorten product development cycles. This integration trend is enabling faster deployment of advanced audio features across mid-range smartphones.

Immersive Audio Ecosystem Shift: Spatial audio, gaming sound enhancement, and high-fidelity streaming are reshaping smartphone audio priorities, with premium audio feature adoption increasing by over 25% among high-end device users. Regulatory focus on energy efficiency and supply-chain resilience is encouraging manufacturers to adopt optimized codec designs that balance performance, cost, and sustainability.

The market is primarily segmented into Lossless Audio Codecs, Lossy Audio Codecs, and Hybrid Audio Codecs. Lossy Audio Codecs represent the leading segment due to their scalability, lower processing requirements, and widespread integration across entry-level and mid-range smartphones. These codecs support efficient storage and streaming performance, with adoption exceeding 60% across global smartphone shipments. Their cost advantage enables manufacturers to deliver reliable audio experiences while maintaining competitive device pricing. Hybrid Audio Codecs are emerging as the fastest-growing segment as smartphone brands seek improved sound quality without increasing hardware complexity. Hybrid solutions combine compression efficiency with enhanced audio fidelity and are gaining adoption in premium smartphones, gaming devices, and AI-enabled applications. Lossless Audio Codecs remain strategically important for high-end devices focused on music streaming and professional audio experiences. Companies are increasing investments in hybrid architectures and chipset-level optimization to capture demand for premium mobile entertainment.

The market is segmented into Smartphones, Tablets, Wearable Devices, and Other Consumer Electronics. Smartphones remain the leading application segment due to their dominant global installed base and continuous demand for improved communication, streaming, gaming, and multimedia experiences. More than 70% of mobile users consume audio-based content regularly, strengthening demand for efficient codec technologies. Manufacturers are integrating advanced codecs to improve call quality, reduce latency, and enhance entertainment capabilities. Wearable Devices represent the fastest-growing application segment as smart earbuds, connected accessories, and health-focused wearables expand rapidly. Adoption of wireless audio products has increased by over 30% in major consumer markets, creating demand for low-power codec solutions. Tablets and other consumer electronics continue supporting codec expansion through productivity and entertainment use cases. Companies are developing cross-device audio platforms and ecosystem partnerships to improve compatibility and strengthen consumer engagement.

The market is segmented into Smartphone Manufacturers, Audio Equipment Manufacturers, Telecom Operators, and Enterprise Users. Smartphone Manufacturers represent the leading end-user group because codec performance directly influences device differentiation, user experience, and premium positioning. Major manufacturers allocate significant resources toward audio optimization, with more than 50% of flagship smartphone launches emphasizing enhanced sound, wireless connectivity, or AI-based audio features. Audio Equipment Manufacturers are the fastest-growing end-user segment as demand increases for advanced earbuds, headphones, and smart audio products. These companies are adopting customized codec solutions to improve battery efficiency, latency performance, and compatibility with mobile platforms. Telecom Operators and Enterprise Users are expanding adoption through voice communication optimization, conferencing solutions, and connected workplace applications. Companies are responding through strategic chipset collaborations, ecosystem partnerships, and customized codec development programs to strengthen market positioning.

Asia-Pacific accounted for the largest market share at 45% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of7.1% between 2026 and 2033.

North America holds a significant position in the Smartphone Audio Codecs Market, supported by strong demand for premium smartphones, wireless audio products, and AI-enhanced communication technologies. The region contributes approximately 24% of global market activity, with deployment concentrated across the United States through advanced consumer electronics and semiconductor ecosystems. More than 65% of flagship smartphone users prioritize enhanced audio features, accelerating adoption of spatial audio and intelligent noise processing. Companies are strengthening partnerships between chipset developers, smartphone brands, and audio technology providers to improve low-power codec performance and accelerate next-generation device launches.

United States Market Outlook: The United States remains the key market due to its leadership in semiconductor design, software innovation, and premium smartphone adoption. Major technology companies are investing heavily in AI-based audio processing and integrated chipset solutions, with over 70% of high-end smartphone models supporting advanced wireless audio capabilities. Strong R&D infrastructure and ecosystem partnerships continue driving innovation.

Europe’s Smartphone Audio Codecs Market is shaped by demand for efficient electronics, sustainability-focused technology development, and advanced wireless audio adoption. The region accounts for nearly 18% of global demand, supported by strong consumer preference for premium smartphones and connected audio devices. Regulatory emphasis on energy efficiency and electronic waste reduction is encouraging manufacturers to optimize low-power codec architectures. Germany, the United Kingdom, and France represent key deployment markets, with wireless audio adoption exceeding 60% among smartphone users in major economies. Companies are investing in efficient semiconductor designs and ecosystem partnerships to meet evolving performance and sustainability expectations.

Germany Market Outlook: Germany leads European technology adoption through its strong engineering ecosystem, industrial electronics capabilities, and focus on sustainable digital infrastructure. Smartphone and semiconductor companies are increasing investments in energy-efficient components, while more than 50% of consumers use wireless audio accessories, supporting demand for advanced codec integration and optimized mobile experiences.

Asia-Pacific dominates the Smartphone Audio Codecs Market due to its extensive smartphone production base, semiconductor manufacturing capabilities, and rapidly expanding consumer electronics sector. The region represents approximately 45% of global market share, driven by China, South Korea, Japan, and India. China remains the largest production hub, contributing more than 60% of global smartphone manufacturing capacity, while local semiconductor investments are improving supply-chain resilience. Companies are expanding chipset partnerships and integrating advanced codec solutions into mid-range and premium devices to address rising demand for mobile entertainment, gaming, and wireless connectivity.

China Market Outlook: China maintains strategic leadership through large-scale smartphone manufacturing, semiconductor investments, and strong domestic technology ecosystems. The country produces over 1 billion smartphones annually across its manufacturing network, creating significant demand for integrated audio solutions. Government-backed semiconductor initiatives and supplier localization efforts are strengthening codec development capabilities and reducing dependency on external components.

South America is experiencing gradual expansion in smartphone audio codec adoption as affordable smartphones, mobile entertainment, and digital communication services continue developing. The region contributes around 6% of global demand, with Brazil and Argentina representing major consumption centers. Increasing smartphone penetration and expanding 4G/5G networks are supporting demand for efficient audio processing technologies. However, component import dependency and limited local semiconductor production remain operational constraints. Companies are responding through distributor partnerships, localized device assembly strategies, and cost-optimized codec solutions targeting value-focused consumers.

Brazil Market Outlook: Brazil represents the largest smartphone market in South America, supported by a population exceeding 200 million people and expanding digital service adoption. Smartphone manufacturers are focusing on affordable devices with improved audio capabilities, while local assembly operations and telecom investments are strengthening access to advanced mobile technologies.

Middle East & Africa is emerging as a high-potential market for smartphone audio codecs due to rapid digital transformation, smartphone upgrades, and telecom infrastructure modernization. The region represents approximately 7% of global demand, with adoption concentrated in countries such as Saudi Arabia, the United Arab Emirates, and South Africa. Expanding 5G networks and increasing demand for mobile entertainment are encouraging manufacturers to introduce advanced audio features. Strategic investments in smart cities and digital services are supporting technology adoption, while companies are developing affordable codec solutions for diverse consumer markets.

Saudi Arabia Market Outlook: Saudi Arabia is becoming a leading technology adoption hub through smart city initiatives, telecom modernization, and consumer electronics investment. The country’s expanding 5G infrastructure covers major urban areas, supporting demand for advanced smartphones with enhanced audio capabilities. Technology partnerships and digital transformation programs are strengthening opportunities for premium codec-enabled devices.

The Smartphone Audio Codecs Market features competition between global semiconductor leaders such as Qualcomm, MediaTek, and Cirrus Logic versus regional chip suppliers and OEM-focused solution providers. The top five players collectively control approximately 55% of the market, creating a moderately concentrated structure. Competition centers on codec performance, power efficiency, licensing flexibility, customization, and supply reliability. Leading suppliers improve positioning through AI audio integration, chipset partnerships, and vertical platform development, while cost-focused players compete through affordable solutions and faster regional deployment. Advanced codec adoption improves processing efficiency by 20%–30%, increasing differentiation pressure. The market is shifting toward integrated AI-enabled audio platforms, making semiconductor expertise and ecosystem partnerships critical barriers. Winning companies must combine innovation speed, scalable manufacturing, and strong smartphone manufacturer alliances.

MediaTek

Cirrus Logic

Realtek Semiconductor

Dolby Laboratories

Sony Semiconductor Solutions

Samsung Electronics

Apple

NXP Semiconductors

Broadcom

STMicroelectronics

Huawei

AI-powered audio processing is becoming a core technology shift, enabling real-time noise suppression, voice enhancement, and personalized sound profiles. Advanced AI codec architectures improve audio processing efficiency by approximately 20% while reducing manual tuning requirements. Adoption is expanding across more than 40% of premium smartphones, giving manufacturers stronger differentiation through intelligent audio experiences.

Bluetooth LE Audio, lossless wireless transmission, and spatial audio technologies are transforming mobile entertainment ecosystems. Compared with older Bluetooth solutions, newer architectures improve power efficiency by nearly 25% and support higher-quality streaming with lower latency. Companies including Qualcomm and MediaTek are integrating these capabilities directly into mobile chipsets to strengthen ecosystem control.

Between 2026 and 2028, neural audio codecs and edge AI processing will become disruptive forces, enabling smarter compression and adaptive sound optimization. New-generation solutions deliver improved bandwidth utilization and support up to 30% better processing efficiency than traditional approaches. Competitive advantage will shift toward suppliers that combine AI algorithms, low-power hardware, and smartphone ecosystem partnerships.

February 2025, Qualcomm introduced Snapdragon 6 Gen 4 with Snapdragon Sound support for mid-tier smartphones, improving AI and audio capabilities. The platform enables wireless lossless audio features and expands premium codec access. Source: www.qualcomm.com

March 2025, Qualcomm highlighted Snapdragon Sound XPAN technology at MWC, enabling Wi-Fi-based lossless audio up to 192kHz. The innovation reduces Bluetooth limitations and strengthens wireless ecosystem partnerships.

2025, MediaTek expanded Dimensity 9400 audio capabilities with AI Audio Focus and 24-bit/384kHz Bluetooth playback support. The chipset delivers 2x higher lossless sampling capability and improves premium smartphone audio positioning.

2025, Cirrus Logic continued advancing mobile audio semiconductor solutions through optimized mixed-signal technologies. Its codec portfolio supports smartphone audio improvements with focus on power efficiency and compact integration.

The Smartphone Audio Codecs Market Report covers comprehensive segmentation across codec types, including Lossless Audio Codecs, Lossy Audio Codecs, and Hybrid Audio Codecs, along with applications spanning smartphones, tablets, wearable devices, and consumer electronics. The analysis evaluates adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing hubs, technology trends, and competitive positioning.

The report examines AI audio processing, Bluetooth LE Audio, spatial sound technologies, semiconductor integration, and emerging neural codec innovations. It provides strategic insights into company participation, deployment trends, supply-chain dynamics, and investment priorities. With analysis of leading manufacturers and evolving end-user requirements, the report supports expansion planning, technology decisions, competitive strategy development, and future market positioning through 2026–2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 802.0 Million |

| Market Revenue (2033) | USD 1,247.7 Million |

| CAGR (2026–2033) | 5.68% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Qualcomm; MediaTek; Cirrus Logic; Realtek Semiconductor; Dolby Laboratories; Sony Semiconductor Solutions; Samsung Electronics; Apple; NXP Semiconductors; Broadcom; STMicroelectronics; Huawei |

| Customization & Pricing | Available on Request (10% Customization Free) |