Reports

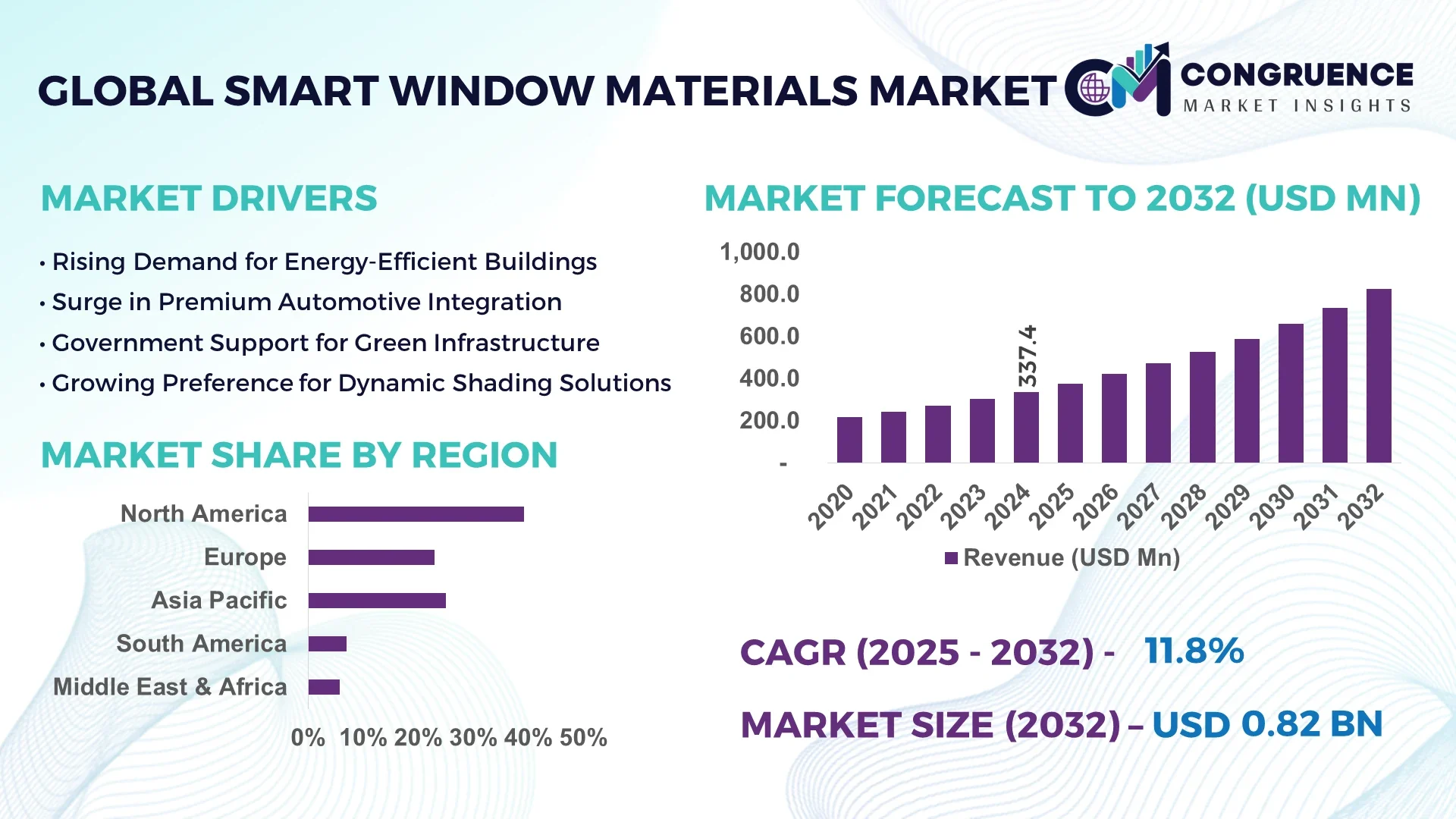

The Global Smart Window Materials Market was valued at USD 337.4 Million in 2024 and is anticipated to reach a value of USD 823.5 Million by 2032 expanding at a CAGR of 11.8% between 2025 and 2032.

In 2024, the United States emerged as the dominant country in the Smart Window Materials Market. U.S.-based manufacturers ramped up production capacity by commissioning two major electrochromic coating plants, each capable of producing over 1 million m² of dynamic glazing annually. Public and private entities committed over USD 150 million in smart glazing innovation programs, focusing on next‑generation electro‑ and thermochromic materials. Key end‑use sectors include commercial high‑rise offices and transportation, leveraging automated tinting for occupant comfort. Technological advancements, such as app‑driven tint control and IoT integration, are now industry standard in the U.S. market.

Globally, the Smart Window Materials Market spans critical sectors including architecture, transportation, and automotive. In architecture, dynamic glazing now accounts for nearly 45 % of material volume usage in commercial high‑rise projects. In transportation, adoption in luxury vehicles and aircraft is increasing, with SPD and electrochromic modules installed in over 500,000 vehicle units in 2023. Recent innovations include hybrid photochromic–electrochromic laminates offering dual automatic and manual control, and lightweight flexible smart films tailored for existing window retrofits. Regulatory drivers include energy‑efficiency mandates such as LEED certification and strict building codes in Europe and North America. Economically, rising electricity costs foster demand for adaptive fenestration that reduces HVAC load and enhances occupant well‑being. Regionally, Europe’s smart window consumption is driven by retrofit incentives, while Asia‑Pacific’s growth is propelled by urbanization and smart-city initiatives. Emerging trends include integration of photovoltaic coatings for dual power generation and shading, and algorithmic tinting that adapts in real-time to light conditions—positioning smart window materials as a pivotal component in sustainable, intelligent built environments.

AI technologies are revolutionizing the Smart Window Materials Market by elevating performance, automation, and sustainability. Decision-makers in building development and transportation sectors are witnessing intelligent glazing systems that autonomously adjust tint levels in real‑time, based on sensor data and predictive algorithms. These AI‑enhanced systems continuously monitor metrics such as solar irradiance, interior heat accumulation, and occupancy to optimize light transmission and thermal comfort. In commercial buildings, AI‑controlled electrochromic windows have reduced peak cooling loads by up to 18 %, by forecasting solar patterns and pre‑tinting glass panels ahead of heat influx. Integration of cloud‑based machine learning platforms enables centralized management across building portfolios, generating actionable insights on energy usage, occupant behavior, and glass performance.

In automotive applications, AI‑driven smart glazing dynamically adapts transparency in response to changing driving conditions—dimming at high solar angles or bright overhead light. Some pilot fleets report a 12 % improvement in in‑cab temperature stability, reducing HVAC reliance. Similarly, AI-based material characterization accelerates development cycles: deep learning models analyze spectroscopic and durability data to identify optimal electrochromic compound blends, decreasing R&D time by 25 %. Manufacturers use reinforcement learning to refine drive voltages, extending glass lifespan and reducing power draw. The Smart Window Materials Market, once reliant on manual operation and static controls, is now evolving into an intelligent ecosystem, where AI-driven systems bolster energy efficiency, occupant well‑being, and operational insight. These smart materials integrate seamlessly with building management systems and automotive ECUs, making them essential to future‑ready infrastructure and mobility.

“In early 2025, a pilot installation of AI‑based control systems in a U.S. office tower showed that auto‑adaptive electrochromic windows, using predictive shading algorithms, reduced peak-hour interior temperatures by 3 °C and cut central HVAC runtime by 14 % during summer months.”

The Smart Window Materials Market is undergoing rapid transformation driven by widespread adoption of dynamic glazing across sectors. Demand is influenced by urbanization, sustainability mandates, and technological convergence with IoT and AI. Material innovation—such as hybrid composites and photovoltaic-coated films—enhances window functionality beyond mere light control. Regulatory frameworks push both new construction and retrofit projects to incorporate smart glazing for energy compliance and occupant wellness. At the same time, supply-side factors like scaling of manufacturing capacities and supply chain diversification affect deployment pace. Cost structures are evolving as automated production lowers material costs, yet initial pricing remains a consideration. Strategic partnerships between window manufacturers, tech integrators, and architects are reshaping market dynamics, enabling tailored solutions aligned with regional infrastructure goals and climate considerations.

Regulatory pressure is a major driver of the Smart Window Materials Market. In 2024, nearly 60 % of newly certified LEED and BREEAM buildings in North America and Europe feature dynamic glazing as part of their envelope systems. Government subsidy programs in multiple states offered rebates of up to USD 5 per ft² of smart glass installed, motivating adoption in both commercial and residential segments. Moreover, cities implementing net‑zero targets are mandating adaptive façade elements; for instance, Chicago’s 2024 energy code incentivizes electrochromic window installations with up to a 30 % reduction in required insulation performance. These policy measures are pushing developers and architects to include smart window materials early in project planning to access financial incentives and comply with emissions limits, making such glazing a core element of green building strategies.

The Smart Window Materials Market is constrained by high initial investments. Advanced electrochromic and SPD glazing systems typically cost 3–5 times more per square meter than conventional double‑glazed units. In 2024, procurement of dynamic window panels and control systems represented upward of USD 200–250/m², excluding installation. This cost differential discourages adoption in cost-sensitive markets, particularly for retrofit projects where structural adjustments are needed. Smaller commercial developers and residential owners cite extended payback periods—often over 8–10 years—as a barrier to entry. Additionally, integration of AI control systems and IoT connectivity adds technical complexity and upfront engineering costs, slowing uptake among mainstream developers despite operational benefits.

Retrofitting offers significant untapped potential in the Smart Window Materials Market. Over 1.5 billion m² of existing commercial glazing stock in North America and Europe is eligible for smart window film overlays. These retrofit solutions require minimal structural modification and can reduce peak solar heat gain by up to 60 %, while costing roughly half the price of full‑panel replacements. Government incentives are now extending to retrofit projects; 2024 saw several utility programs offer USD 3–4/ft² rebates for smart film installations. This is encouraging facility managers to upgrade aging façades with electrochromic or SPD film solutions, accelerating market penetration beyond new builds and unlocking value in low‑cost capital investment cycles.

A key challenge in the Smart Window Materials Market is achieving seamless control integration. Smart window systems often use proprietary protocols, creating silos within Building Management Systems (BMS) and Vehicle ECUs. In 2024, a survey revealed that 45 % of facility managers encountered compatibility issues when integrating dynamic glazing into multi‑vendor automation platforms. Fragmented wiring standards, differing communication protocols, and lack of universal APIs increase system complexity and cost. These integration bottlenecks require additional engineering hours and coordination with in‑house IT and automation teams, sometimes adding 10–15 % to project timelines and budgets. Addressing interoperability will be essential for unlocking efficiency gains and ensuring a smooth user experience.

Advanced Hybrid Composite Films for Retrofit Applications: Hybrid photochromic–electrochromic films gained traction in 2024, with over 250 pilot projects reporting an average installation area of 5,000 m² each. These composites offer dual automatic response to UV and manual override via mobile apps, meeting performance and user control requirements without full window replacement. Adoption rates in retrofit portfolios doubled year-over-year in North America.

Integration of Photovoltaic Transparent Coatings: In 2024, transparent photovoltaic smart glass began deployment in three university campus buildings in California, supplying over 2 kW of on-site solar generation per building. This dual-function glazing enables façades to produce renewable energy while maintaining daylighting and privacy control, driving a new efficiency benchmark in sustainable design.

Automated Fleet-Wide Tint Control in Automotive: Luxury EV fleets incorporating AI-tinting smart windows achieved cabin temperature variance reductions of 8 °C compared to static glazing, during summer 2024 trials. Fleet operators reported a 9 % decrease in battery energy used for climate control during highway driving, showcasing operational benefits of dynamic glazing in mobility.

Certification of IoT-Ready Smart Window Standards: In late 2024, an industry consortium finalized ISO/IEC guidelines for IoT-enabled smart windows, ensuring secure API access, encryption, and adaptive control protocols. Compliance is expected to be mandatory for new commercial projects in multiple jurisdictions beginning 2025, fostering unified integration and cybersecurity in Smart Window Materials Market deployments.

The Smart Window Materials Market is segmented based on type, application, and end-user, offering a multi-dimensional view of industry dynamics. Each segment serves a distinct set of performance criteria and adoption drivers, influencing product development and deployment strategies. Material types such as electrochromic, thermochromic, and suspended particle devices (SPD) lead the innovation front, with market demand closely tied to functionality, responsiveness, and integration ease. Application-wise, the market sees broad adoption across architectural glazing, transportation, and solar energy systems. End-users include commercial real estate developers, automotive OEMs, and public infrastructure authorities—each pushing the boundaries of adaptive fenestration use. Segment-wise insights reveal that technological adaptability, retrofit capability, and regulatory alignment are key factors defining market performance and growth potential across all categories.

The Smart Window Materials Market comprises several material technologies, each tailored to specific performance and application needs. Electrochromic materials represent the leading type, widely adopted in architectural and transportation sectors due to their controllable light modulation, durability, and ability to integrate with building automation systems. Electrochromic windows are now standard in high-performance commercial buildings and premium automotive models, where occupant comfort and energy savings are prioritized.

Suspended Particle Devices (SPD) are the fastest-growing material type, particularly in luxury vehicles and aviation applications. Their ability to offer near-instant tinting response and variable transparency levels has accelerated their adoption in sunroofs, cockpits, and high-glare environments. SPD technology’s responsiveness to voltage adjustments and flexibility in form factor make it ideal for curved or non-standard window geometries.

Thermochromic materials maintain a niche presence, especially in passive buildings, offering tint changes based on temperature without the need for wiring or electricity. Although less flexible in control, their low maintenance profile makes them attractive for remote or off-grid structures. Photochromic and liquid crystal-based materials also contribute to the product mix, serving specialty segments where light sensitivity or switchable privacy is required.

In the Smart Window Materials Market, architectural glazing remains the dominant application, driven by rising demand for energy-efficient and occupant-responsive building envelopes. Commercial office spaces, hospitals, and educational campuses are primary adopters, particularly in climates where solar gain and daylight control are critical factors. Dynamic glazing contributes to thermal load reduction, daylight optimization, and enhanced user comfort in these environments.

Automotive applications are witnessing the fastest growth, fueled by the rising integration of smart glazing in electric vehicles and premium car models. Features such as self-dimming windshields, smart sunroofs, and rear passenger windows are now considered differentiators in luxury segments. These applications benefit from AI-enhanced systems that adapt to external lighting and temperature conditions in real-time, improving passenger comfort and reducing HVAC usage.

Other applications include aviation, where smart windows are replacing mechanical shades, and marine vessels, particularly luxury yachts, that require adaptive light control for onboard comfort. Emerging use in greenhouses and solar power systems indicates further diversification, especially in climate-sensitive agricultural operations and energy-producing building components.

Among end-users, commercial building developers and real estate companies lead the Smart Window Materials Market, driven by regulatory compliance, green certification goals, and the need for energy cost reductions. These stakeholders prioritize smart glazing in new construction and retrofit projects alike, particularly in urban commercial centers where occupant wellness and building performance are under scrutiny.

The automotive sector is the fastest-growing end-user segment, with OEMs integrating smart glazing into next-generation vehicle models. The adoption is driven by consumer preference for enhanced aesthetics, interior comfort, and energy efficiency. Automotive brands are leveraging smart window materials to differentiate their electric and autonomous vehicle offerings, as these materials contribute to intelligent system integration and futuristic cabin experiences.

Public infrastructure authorities are also significant contributors, especially in transport terminals, government buildings, and educational institutions where occupant comfort, sustainability, and security are important. Other end-users include hospitality, healthcare, and retail chains, which are gradually embracing smart glazing to improve visitor experience and reduce operational energy use, rounding out the market with diverse, function-driven demand.

North America accounted for the largest market share at 39.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.1% between 2025 and 2032.

North America's strong market presence is driven by mature adoption across commercial real estate, transportation, and institutional buildings, backed by energy efficiency regulations. Meanwhile, Asia-Pacific’s rapid urbanization, rising construction investments, and smart city initiatives are accelerating demand for adaptive glazing technologies. The shift toward sustainable architecture, especially in countries like China and India, is catalyzing growth, supported by expanding manufacturing capacity and government-led innovation programs across the region.

North America held 39.2% of the global Smart Window Materials Market share in 2024, with the U.S. as the primary contributor. The region’s growth is fueled by strong demand from the commercial construction sector, particularly high-performance office buildings, educational institutions, and healthcare facilities. Regulatory updates, such as California Title 24 and New York’s Local Law 97, are pushing for higher energy efficiency standards, driving the adoption of smart glazing. Technological innovation in electrochromic and SPD systems is widespread, with North American manufacturers pioneering IoT-enabled control systems and app-driven user interfaces. Government incentives and utility rebate programs further support market adoption.

Europe accounted for approximately 28.7% of the global Smart Window Materials Market in 2024, with leading markets including Germany, the UK, and France. The market benefits from stringent EU sustainability mandates, such as the European Green Deal and the Energy Performance of Buildings Directive (EPBD). These frameworks encourage the integration of dynamic glazing to reduce emissions and improve indoor comfort. Countries like Germany have embraced smart materials in retrofit strategies for public infrastructure. Technological adoption is also strong, with advancements in thermochromic and hybrid coatings gaining popularity. European companies are investing in AI-integrated solutions for real-time light and thermal optimization.

Asia-Pacific ranked as the fastest-growing regional market in 2024, with major consumption in China, India, and Japan. The region is undergoing a construction and infrastructure boom, supported by national smart city missions and green building policies. China’s public and private sectors are heavily investing in dynamic façades and AI-driven glazing systems, especially for metro stations, airports, and tech campuses. India is witnessing increased demand for retrofittable smart window films in commercial spaces and government projects. Japan’s R&D centers remain innovation hubs for advanced nanomaterials and low-voltage electrochromic films. Regional tech convergence and urban infrastructure growth are rapidly expanding the market’s reach.

In 2024, Brazil and Argentina led the South American Smart Window Materials Market, with Brazil accounting for the majority of regional adoption. The market is emerging as governments invest in sustainable infrastructure, modern public buildings, and eco-certified commercial properties. Construction trends linked to urban expansion and green architecture, especially in São Paulo and Buenos Aires, are supporting the uptake of smart glazing. The energy sector, particularly solar-integrated façades, is gaining traction. Trade incentives under regional agreements are easing material imports, while government-backed efficiency initiatives encourage developers to integrate smart technologies into both public and private projects.

The Middle East & Africa region is witnessing a growing demand for smart window materials, particularly in UAE and South Africa. Regional adoption is driven by extreme climate conditions and energy efficiency initiatives in mega infrastructure projects. The UAE, in particular, is incorporating dynamic glazing in high-rise buildings and transit hubs to reduce air-conditioning loads. South Africa is exploring retrofitting solutions in public institutions to manage electricity consumption. Technological modernization, including AI-based tint control and integration with building management systems, is gaining momentum. Regulatory initiatives promoting sustainable construction and partnerships with European tech firms are further supporting market expansion.

United States – 34.5% Market Share

Dominance driven by large-scale production capacity and high adoption across commercial and automotive sectors.

China – 21.7% Market Share

Strong end-user demand in construction and government-funded smart city developments fuels growth in the Smart Window Materials Market.

The Smart Window Materials Market is characterized by a competitive landscape comprising more than 40 active global and regional players, ranging from technology innovators to vertically integrated manufacturers. Leading firms are strategically positioned through proprietary technologies in electrochromic, thermochromic, and SPD-based materials. Competitive intensity is driven by innovation cycles, patent activity, and product differentiation in terms of responsiveness, durability, and energy efficiency.

Strategic initiatives include multi-million-dollar joint ventures between glazing manufacturers and building automation companies, aimed at integrating AI-driven controls. Several players launched second-generation electrochromic window systems in 2023–2024, with faster switching times and enhanced visual clarity. Mergers and acquisitions have also shaped the competitive arena, with at least four major deals completed since early 2023 to consolidate IP portfolios and expand manufacturing footprints.

Companies are increasingly competing on digital compatibility—offering smart windows pre-configured for BMS and IoT platforms. Innovation is also targeting sustainability, with biodegradable substrates and recyclable conductive coatings entering development pipelines. The competition extends into regional expansion strategies, with Asia-Pacific markets emerging as key battlegrounds due to rising construction activity and government mandates on energy-efficient buildings.

Saint-Gobain S.A.

View Inc.

AGC Inc.

Gentex Corporation

Smartglass International Ltd.

Research Frontiers Inc.

ChromoGenics AB

Polytronix, Inc.

Gauzy Ltd.

Pleotint LLC

The Smart Window Materials Market is being reshaped by a wave of emerging technologies that enhance both functionality and integration. One of the most transformative technologies is electrochromic coating, which enables glass to modulate transparency when voltage is applied. Recent advances have reduced switching times to under 90 seconds while improving color neutrality, making electrochromic windows more suitable for both commercial and residential installations.

Suspended Particle Devices (SPD) have seen significant improvements in scalability and voltage efficiency. New SPD films launched in 2024 demonstrate over 99% UV blockage and over 60% modulation in visible light transmission, catering especially to automotive and aerospace segments.

Thermochromic and photochromic materials continue to evolve for passive smart window systems. Their temperature- and light-responsive features are gaining traction in off-grid and climate-sensitive installations. Manufacturers are working on hybrid composites that combine electrochromic and photochromic properties, enabling multi-functional control over light and heat.

Integration with Internet of Things (IoT) infrastructure is another major shift. Smart windows now come with built-in sensors and connectivity modules for real-time environmental monitoring. These windows can adjust in response to data from building energy systems or weather inputs, helping optimize lighting and HVAC operations.

Additionally, AI-enabled smart glass is on the rise. These systems use predictive analytics and machine learning to anticipate solar gain patterns and adjust window tinting automatically, maximizing occupant comfort and energy efficiency. In 2024, flexible OLED-powered smart films entered pilot trials, offering ultra-thin form factors for curved surfaces and retrofit applications.

• In January 2023, Gentex Corporation introduced a new SPD-based dimmable sunroof technology for premium electric vehicles, achieving over 70% reduction in light transmission and enhancing in-cabin climate control without mechanical shading components.

• In April 2023, ChromoGenics AB completed installation of over 4,000 square meters of electrochromic glass at a Scandinavian medical facility, marking one of the largest smart glazing installations in the region focused on patient comfort and energy savings.

• In August 2024, Gauzy Ltd. launched a transparent rear-projection smart film integrated with SPD technology, enabling dual-function smart windows for both shading and dynamic display applications in retail and automotive segments.

• In February 2024, AGC Inc. unveiled its next-gen thermochromic glass capable of tint transition at 3°C lower threshold than previous models, enhancing energy performance in colder climates and extending usability across building types.

The Smart Window Materials Market Report provides an in-depth analysis of current trends, market structure, and technological evolution shaping the global landscape. The report encompasses a comprehensive segmentation based on product type—including electrochromic, thermochromic, SPD, photochromic, and liquid crystal-based materials. It also evaluates key application areas such as architectural glazing, automotive, aviation, marine, and niche sectors like greenhouses and solar control systems.

The geographic scope covers five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with further granularity on major markets such as the U.S., China, Germany, Japan, Brazil, and the UAE. It details end-user categories including commercial real estate developers, automotive OEMs, public infrastructure agencies, and specialty building operators like hospitals and schools.

The report also addresses emerging segments such as retrofit smart films and AI-integrated dynamic glazing systems. Special attention is given to technological trends, including sensor-enabled systems, IoT interoperability, and AI-based adaptive control. Regulatory drivers, environmental mandates, energy efficiency goals, and building automation compatibility are explored to provide strategic context for stakeholders. The report is structured to support investment decisions, product strategy development, and market entry planning across all key verticals.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 337.4 Million |

| Market Revenue (2032) | USD 823.5 Million |

| CAGR (2025–2032) | 11.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Saint-Gobain S.A., View Inc., AGC Inc., Gentex Corporation, Smartglass International Ltd., Research Frontiers Inc., ChromoGenics AB, Polytronix, Inc., Gauzy Ltd., Pleotint LLC |

| Customization & Pricing | Available on Request (10% Customization is Free) |