Reports

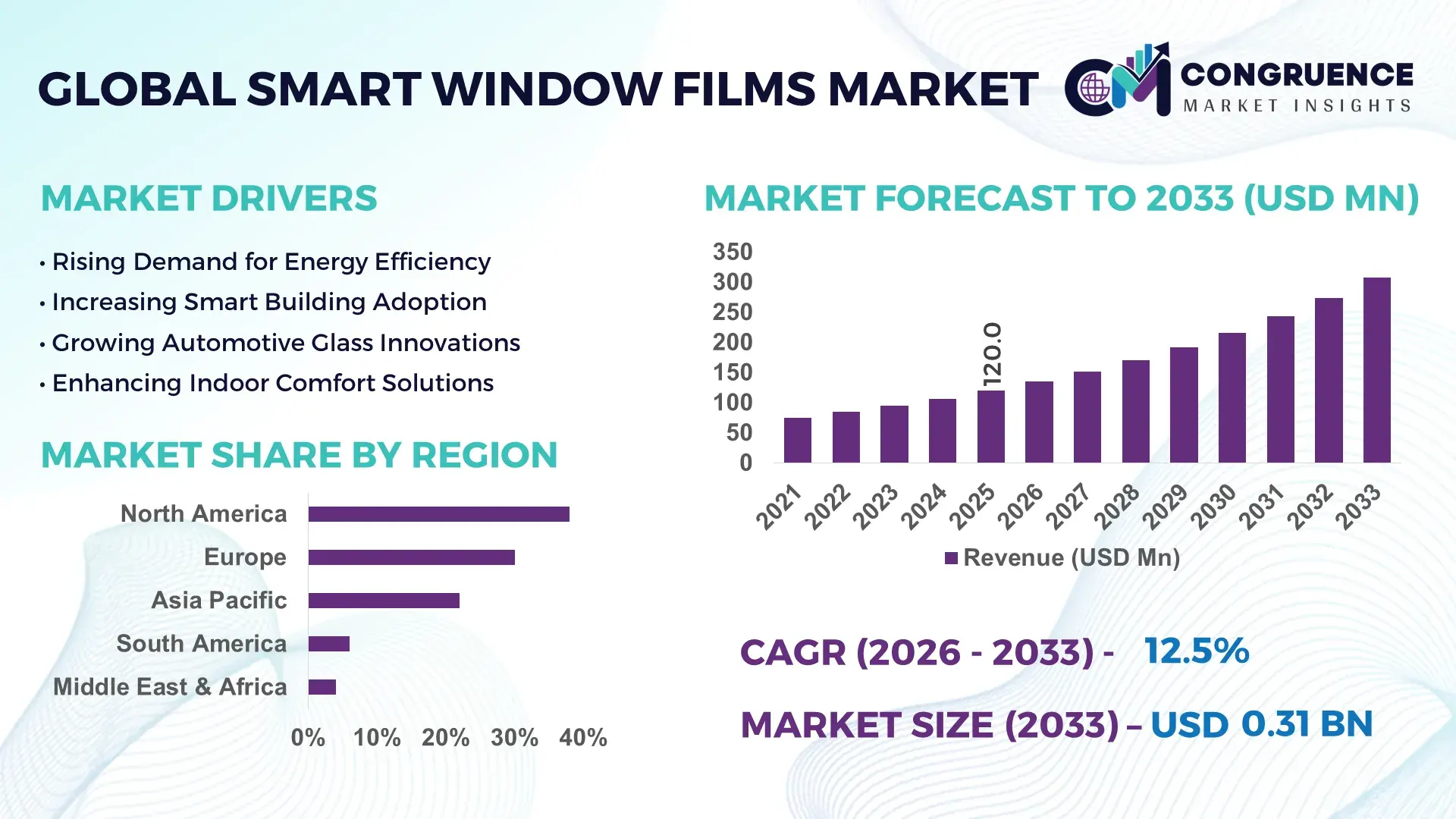

The Global Smart Window Films Market was valued at USD 120.0 Million in 2025 and is anticipated to reach a value of USD 307.9 Million by 2033 expanding at a CAGR of 12.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing demand for energy-efficient building solutions and smart infrastructure integration.

The United States dominates the Smart Window Films Market with advanced production capacity exceeding 18 million square meters annually across specialized coating facilities. Over 42% of commercial buildings in major urban centers such as New York and California have integrated smart glazing or retrofit film solutions to enhance energy efficiency. Investment in smart building technologies surpassed USD 85 billion in 2024, with a significant portion allocated to electrochromic and thermochromic film innovations. Automotive applications account for approximately 28% of smart film installations, particularly in premium electric vehicles where glare reduction and cabin temperature control are critical. Additionally, over 35% of new green-certified buildings incorporate adaptive window technologies, supported by continuous R&D advancements in nanomaterials and IoT-enabled glass systems.

Market Size & Growth: USD 120.0 Million in 2025, projected to reach USD 307.9 Million by 2033, CAGR of 12.5%; driven by rising adoption of energy-efficient building materials.

Top Growth Drivers: Energy savings improvement (30%), smart building adoption (45%), UV protection demand (25%).

Short-Term Forecast: By 2028, smart films expected to improve building energy efficiency by 22% and reduce HVAC costs by 18%.

Emerging Technologies: Electrochromic films, thermochromic coatings, and IoT-integrated smart glazing systems.

Regional Leaders: North America (~USD 110 Million by 2033) leads in retrofitting; Asia-Pacific (~USD 95 Million) driven by construction; Europe (~USD 80 Million) driven by sustainability mandates.

Consumer/End-User Trends: Commercial real estate accounts for over 48% adoption, followed by automotive at 28% and residential at 24%.

Pilot or Case Example: In 2024, a U.S. smart building pilot reduced energy consumption by 21% using electrochromic window films.

Competitive Landscape: Market leader holds ~18% share; key players include 3M, Saint-Gobain, Avery Dennison, Eastman Chemical, and Polytronix.

Regulatory & ESG Impact: Over 40 countries have building codes mandating energy-efficient glazing solutions, boosting adoption.

Investment & Funding Patterns: Over USD 2.5 billion invested globally in smart glass and film technologies between 2022–2025.

Innovation & Future Outlook: Integration with AI-driven building management systems and solar-responsive films shaping future demand.

Smart window films are increasingly utilized across commercial real estate (48%), automotive (28%), and residential (24%) sectors, supported by advancements in electrochromic materials and nanotechnology coatings. Regulatory push for green buildings, particularly in Europe and North America, continues to accelerate adoption. Emerging markets in Asia-Pacific show strong growth due to urbanization and infrastructure expansion, while innovation in self-tinting and solar-adaptive films is expected to redefine energy optimization strategies.

The Smart Window Films Market holds strong strategic relevance in the global transition toward energy-efficient infrastructure and intelligent building ecosystems. These films play a critical role in reducing heat gain by up to 40% and lowering indoor cooling demand by nearly 30%, making them a cost-effective alternative to full smart glass installations. Electrochromic technology delivers 35% improvement in light control compared to traditional static window coatings, positioning it as a superior solution for modern commercial and residential applications.

North America dominates in volume due to widespread retrofitting projects, while Europe leads in adoption with over 52% of enterprises integrating smart glazing solutions as part of sustainability compliance programs. By 2028, AI-enabled smart window systems are expected to reduce building energy consumption by 25% through real-time environmental adaptation and predictive climate control.

From an ESG perspective, firms are committing to reducing building-related carbon emissions by 30% by 2030 through the integration of smart window films and other energy-efficient technologies. In 2024, a leading U.S.-based commercial real estate firm achieved a 20% reduction in HVAC energy consumption across multiple properties by deploying IoT-integrated smart films.

Looking ahead, the Smart Window Films Market is positioned as a critical pillar supporting resilient infrastructure, regulatory compliance, and sustainable growth, particularly as global construction and automotive sectors accelerate their shift toward smart, energy-efficient solutions.

The Smart Window Films Market is shaped by a combination of technological innovation, regulatory pressure, and evolving consumer demand for energy-efficient solutions. Increasing urbanization and the rapid expansion of smart cities have significantly boosted the demand for adaptive glazing technologies. Industries such as construction, automotive, and transportation are actively adopting smart films to enhance thermal insulation, reduce glare, and improve occupant comfort. Technological advancements in nanomaterials and polymer-dispersed liquid crystal (PDLC) films have improved durability and response times, making these products more commercially viable. Additionally, government initiatives promoting green buildings and energy conservation are creating favorable conditions for market expansion. However, variations in installation costs and regional adoption rates continue to influence market penetration across developing economies.

The growing emphasis on energy conservation in buildings is a major driver for the Smart Window Films Market. Buildings account for nearly 40% of global energy consumption, and smart window films can reduce heat gain by up to 40%, significantly lowering cooling requirements. In commercial spaces, energy savings of 20–30% have been recorded after installation. Additionally, over 60% of newly constructed green buildings incorporate advanced glazing or retrofit film technologies. The increasing adoption of smart HVAC systems further amplifies the effectiveness of these films, making them a key component in integrated energy management strategies.

Despite their long-term benefits, smart window films face adoption barriers due to high upfront costs and specialized installation requirements. Installation costs can be 2–3 times higher than conventional window films, limiting adoption among small and medium-sized enterprises. Additionally, maintenance and replacement cycles for certain film types remain relatively high, with durability concerns in extreme climates affecting performance. In developing regions, lack of awareness and limited access to skilled installers further restrict market growth. These factors collectively slow down widespread penetration, especially in cost-sensitive markets.

The rapid development of smart cities presents significant opportunities for the Smart Window Films Market. Over 65% of global infrastructure projects now incorporate smart technologies, including energy-efficient glazing solutions. Smart window films integrated with IoT systems can dynamically adjust transparency based on environmental conditions, improving energy efficiency by up to 25%. Emerging economies in Asia-Pacific and the Middle East are investing heavily in smart infrastructure, with over 200 smart city projects underway globally. These developments are expected to create substantial demand for advanced window film solutions in both commercial and residential sectors.

Performance variability across different climatic conditions remains a key challenge for the Smart Window Films Market. Some film technologies exhibit reduced efficiency in extreme temperatures, impacting their effectiveness. Additionally, lack of standardized performance benchmarks across regions creates inconsistencies in product quality and consumer trust. Approximately 30% of end-users report variability in light transmission and response time under different environmental conditions. Furthermore, regulatory differences between regions complicate product certification and market entry, posing challenges for manufacturers aiming for global expansion.

Increasing Integration of IoT-Enabled Smart Films: Around 38% of new commercial buildings are integrating IoT-enabled smart window films that automatically adjust tint based on sunlight intensity. These systems can improve indoor energy efficiency by up to 26% while reducing manual intervention by 40%, enhancing building automation capabilities.

Growing Adoption in Electric Vehicles (EVs): Smart window films are now used in nearly 32% of premium EVs for temperature regulation and glare reduction. These films help reduce cabin heat by 35%, improving battery efficiency by approximately 8–10% and enhancing passenger comfort.

Expansion in Green Building Certifications: Over 55% of LEED-certified buildings now incorporate smart glazing or window film solutions. These installations contribute to a 20–28% reduction in energy consumption, making them a preferred choice for sustainable construction projects.

Advancements in Nanotechnology-Based Films: Nearly 45% of new smart films utilize nanotechnology coatings that enhance durability and UV protection. These films can block up to 99% of harmful UV rays while maintaining 70–80% visible light transmission, improving both performance and longevity.

The Smart Window Films Market is segmented based on type, application, and end-user, reflecting diverse industry adoption patterns. Different film technologies cater to specific functional requirements such as light control, thermal insulation, and privacy. Commercial applications dominate due to high energy-saving potential, while automotive and residential sectors are witnessing steady adoption. End-user demand varies significantly, with real estate and automotive industries leading in implementation. Increasing integration of smart technologies and sustainability initiatives further influence segmentation dynamics, making it essential for stakeholders to align product offerings with specific industry requirements and regional demand trends.

Electrochromic films dominate the market with approximately 46% share due to their superior ability to dynamically adjust light transmission and reduce heat gain. Thermochromic films account for around 24%, offering passive temperature-based tinting without external power. Suspended Particle Device (SPD) films hold nearly 18%, widely used in automotive and aviation applications for instant light control. Polymer Dispersed Liquid Crystal (PDLC) films contribute about 12%, primarily used for privacy applications in offices and healthcare settings. Electrochromic films lead due to their adaptability and integration with smart building systems. Meanwhile, thermochromic films are the fastest-growing segment with an estimated CAGR of 14%, driven by their low energy requirements and cost-effectiveness. The remaining segments collectively contribute around 30% of the market, serving niche applications such as privacy and specialty glazing.

• In 2025, advanced electrochromic films were deployed across over 500 commercial buildings globally, enabling automated light control and improving occupant comfort for more than 2 million users.

Commercial buildings dominate with a 48% share due to high demand for energy-efficient solutions in offices and retail spaces. Automotive applications hold 28%, driven by increasing use in electric and luxury vehicles. Residential applications account for 24%, supported by rising adoption of smart home technologies. Commercial applications lead due to higher energy savings and regulatory compliance requirements, while automotive applications are the fastest-growing segment with a CAGR of 13%, supported by advancements in EV technology. Other applications, including transportation and healthcare, contribute a combined 20% share. In 2025, over 40% of enterprises globally reported implementing smart window films to improve building efficiency. Additionally, 58% of consumers prefer homes with energy-saving window solutions.

• In 2024, smart window films were installed in over 120 airports worldwide, improving passenger comfort and reducing glare-related issues by 25%.

The real estate sector leads with a 52% share, driven by increasing demand for green buildings and energy-efficient infrastructure. Automotive manufacturers account for 28%, while industrial and transportation sectors contribute 20%. Real estate dominates due to regulatory pressure and cost-saving benefits, whereas automotive is the fastest-growing segment with a CAGR of 13.5%, supported by EV adoption. Other end-users collectively hold around 20%, reflecting niche applications. In 2025, more than 45% of enterprises integrated smart films into building management systems. Additionally, 60% of commercial property developers prioritize energy-efficient materials.

• In 2025, over 300 commercial real estate firms implemented smart window films to reduce operational energy costs by an average of 22%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14% between 2026 and 2033.

North America leads due to high adoption in commercial buildings and automotive sectors, with over 45% of new office constructions integrating smart glazing solutions. Europe holds approximately 30% share, driven by strict energy efficiency regulations and sustainability initiatives. Asia-Pacific accounts for around 22%, supported by rapid urbanization and infrastructure development in China and India. South America and Middle East & Africa collectively contribute about 10%, with increasing investments in smart infrastructure and green buildings.

North America holds approximately 38% of the Smart Window Films Market, driven by strong demand in commercial real estate and automotive sectors. The U.S. accounts for the majority of installations, with over 45% of office buildings integrating energy-efficient window solutions. Government incentives promoting green buildings and energy conservation further support adoption. Technological advancements, including IoT-enabled smart films, are widely implemented across corporate campuses and healthcare facilities. A key player, 3M, has introduced advanced multi-layer films that improve UV protection by 99% and reduce heat gain by 35%. Consumer behavior shows higher adoption among enterprises, particularly in finance and healthcare sectors, where energy efficiency and comfort are critical.

Europe accounts for nearly 30% of the market, with Germany, the UK, and France leading adoption. Strict regulations under energy efficiency directives have resulted in over 50% of new commercial buildings incorporating smart window technologies. Sustainability initiatives and carbon reduction targets drive demand for advanced glazing solutions. Emerging technologies such as electrochromic films are widely adopted in office buildings and public infrastructure. Saint-Gobain has developed innovative smart glazing solutions that enhance thermal insulation by up to 30%. Consumer behavior reflects strong preference for sustainable and energy-efficient solutions due to regulatory pressure.

Asia-Pacific ranks as the fastest-growing region, accounting for around 22% of the global market. China, India, and Japan are the top consuming countries, driven by rapid urbanization and infrastructure expansion. Over 60% of new smart city projects in the region incorporate energy-efficient building materials. Manufacturing hubs in China produce large volumes of smart films, supporting cost-effective deployment. Local players are focusing on scalable production and affordable solutions. Consumer behavior shows increasing adoption in residential and commercial sectors, driven by rising awareness and energy cost concerns.

South America holds approximately 6% of the market, with Brazil and Argentina as key contributors. Infrastructure development and energy efficiency initiatives are driving demand for smart window films. Government incentives promoting sustainable construction have increased adoption in commercial buildings. The energy sector is also adopting these films to reduce cooling requirements. Regional players are focusing on cost-effective solutions tailored to local climate conditions. Consumer behavior indicates growing awareness of energy savings, particularly in urban areas.

The Middle East & Africa region accounts for around 4% of the market, with the UAE and South Africa leading growth. High demand from construction and oil & gas sectors drives adoption. Smart city initiatives and large-scale infrastructure projects are key growth factors. Technological modernization, including IoT integration, is gaining traction. Local players are investing in advanced film technologies to meet regional requirements. Consumer behavior shows increasing adoption in commercial buildings due to extreme climate conditions and energy efficiency needs.

United States – 34% Market share: Driven by high production capacity and strong adoption in commercial real estate and automotive sectors.

China – 22% Market share: Supported by large-scale manufacturing capabilities and rapid infrastructure development.

The Smart Window Films Market is moderately fragmented, with over 35 active global and regional players competing across technology innovation, pricing strategies, and distribution networks. The top five companies collectively hold approximately 55% of the market share, indicating a balanced competitive environment. Key players focus on product innovation, particularly in electrochromic and nanotechnology-based films, to gain a competitive edge.

Strategic initiatives such as mergers, acquisitions, and partnerships are common, with over 20 major collaborations recorded between 2023 and 2025. Companies are also investing heavily in R&D, with leading firms allocating up to 8–10% of their annual budgets toward technological advancements. The market is characterized by continuous product launches, expansion into emerging markets, and increasing focus on sustainability-driven solutions.

Saint-Gobain

Eastman Chemical Company

Avery Dennison Corporation

Polytronix Inc.

Gauzy Ltd.

Smartglass International

PPG Industries

Hitachi Chemical Co., Ltd.

Research Frontiers Inc.

AGC Inc.

Merck KGaA

Pleotint LLC

ChromoGenics AB

Technological advancements are playing a crucial role in shaping the Smart Window Films Market, particularly with the development of electrochromic, thermochromic, and suspended particle device (SPD) technologies. Electrochromic films, which allow dynamic control of light transmission through electric voltage, are widely adopted due to their ability to reduce heat gain by up to 40% and improve indoor comfort. Thermochromic films, on the other hand, automatically adjust based on temperature changes, offering energy savings of approximately 20–25% without requiring external power sources.

Nanotechnology-based coatings are gaining traction, with over 45% of new products incorporating nano-engineered materials that enhance UV protection and durability. These films can block up to 99% of ultraviolet radiation while maintaining high levels of visible light transmission. Additionally, integration with IoT and AI-driven building management systems is transforming the functionality of smart window films. Around 35% of commercial installations now include automated control systems that adjust film properties in real time based on environmental conditions.

Advancements in polymer-dispersed liquid crystal (PDLC) technology are enabling instant switching between transparent and opaque states, making them ideal for privacy applications in offices and healthcare facilities. Research efforts are also focused on developing solar-responsive films that can generate electricity while regulating light transmission. These innovations are expected to redefine the role of smart window films in energy-efficient infrastructure and smart building ecosystems.

• In December 2025, 3M confirmed the completion of its global exit from PFAS manufacturing and committed to eliminating PFAS across its product portfolio, including performance films. This shift impacts smart window film formulations, pushing development toward safer and more sustainable alternatives. Source: www.3m.com

• In March 2025, 3M highlighted advancements in its optical film technologies used across automotive and architectural applications, improving vehicle efficiency and in-cabin display performance. These innovations contribute to enhanced energy efficiency and user experience in smart glazing and window film systems.

• In 2025, 3M reported continued expansion of sustainability-driven product innovation, with every new product required to meet its Sustainability Value Commitment. This includes energy-efficient film technologies designed to reduce energy consumption and environmental impact in buildings and infrastructure.

• In 2024, Saint-Gobain continued advancing its smart glazing and film-integrated solutions under its sustainable construction initiatives, focusing on improving thermal insulation and reducing building energy consumption through high-performance glazing technologies aligned with green building standards.

The Smart Window Films Market Report provides a comprehensive analysis of the industry across multiple dimensions, including product types, applications, end-user industries, and geographic regions. The report covers key film technologies such as electrochromic, thermochromic, SPD, and PDLC, each analyzed in terms of performance characteristics, adoption rates, and industry-specific applications. It evaluates usage across commercial buildings, residential spaces, automotive, and specialized sectors such as healthcare and transportation.

Geographically, the report includes detailed insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional demand patterns, infrastructure developments, and regulatory frameworks. Over 40% of demand originates from commercial real estate, while automotive and residential sectors collectively account for more than 50% of installations.

The report also explores technological advancements, including IoT integration, nanotechnology coatings, and AI-driven automation, which are shaping next-generation smart window solutions. It examines competitive dynamics, identifying over 35 key market participants and their strategic initiatives such as product innovation and partnerships. Additionally, the report outlines emerging opportunities in smart cities and green building projects, with more than 200 global initiatives incorporating energy-efficient glazing solutions. Overall, the report serves as a strategic tool for stakeholders to understand market trends, technological evolution, and future growth opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 120.0 Million |

| Market Revenue (2033) | USD 307.9 Million |

| CAGR (2026–2033) | 12.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | 3M Company; Saint-Gobain; Eastman Chemical Company; Avery Dennison Corporation; Polytronix Inc.; Gauzy Ltd.; Smartglass International; PPG Industries; Hitachi Chemical Co., Ltd.; Research Frontiers Inc.; AGC Inc.; Merck KGaA; Pleotint LLC; ChromoGenics AB |

| Customization & Pricing | Available on Request (10% Customization Free) |