Reports

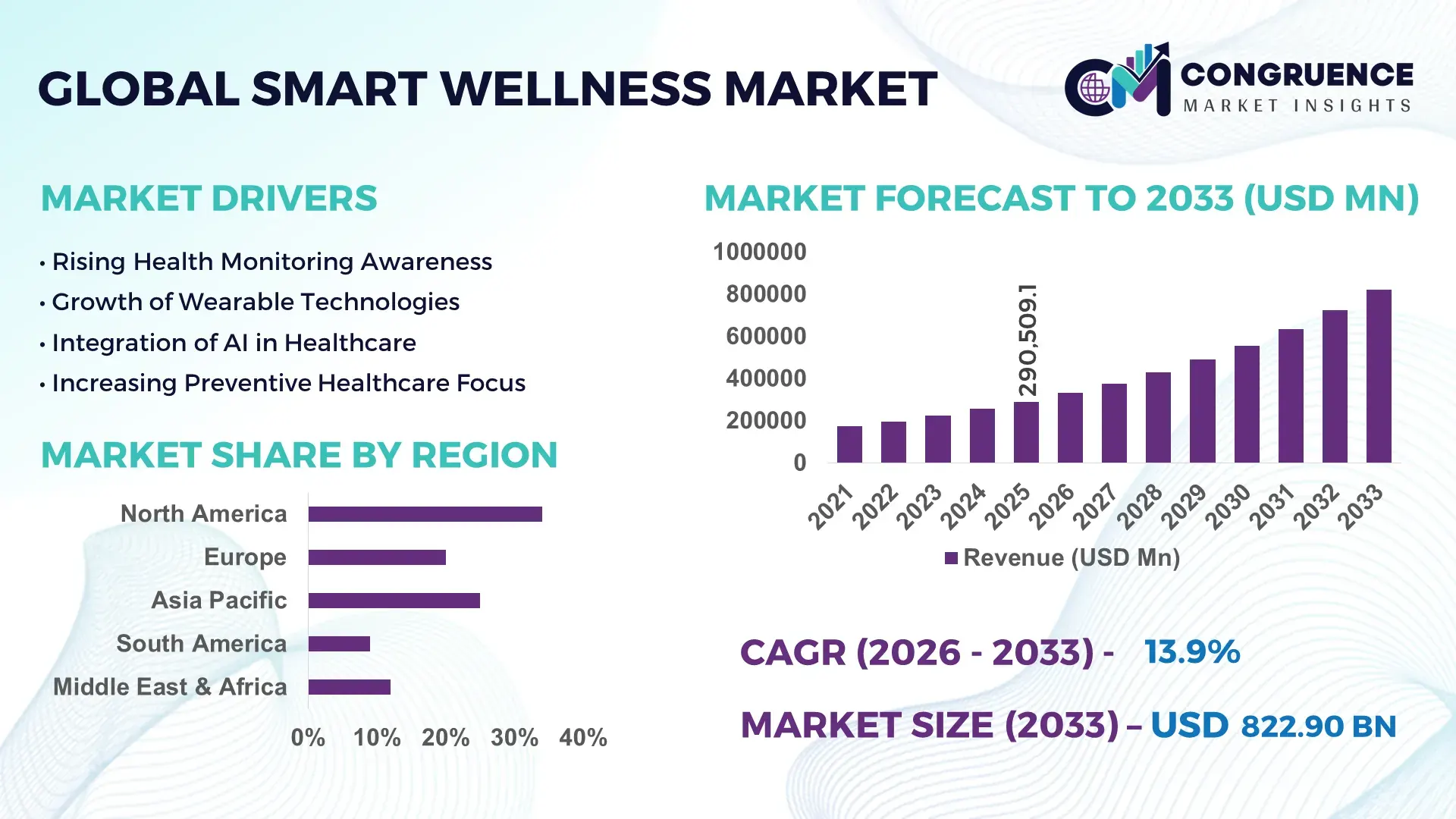

The Global Smart Wellness Market was valued at USD 290509.09 Million in 2025 and is anticipated to reach a value of USD 822904.65 Million by 2033 expanding at a CAGR of 13.9% between 2026 and 2033.

Market expansion is driven by the rapid adoption of AI-powered health monitoring and connected wellness ecosystems, with over 68% of consumers using at least one smart wellness device for continuous health tracking. Between 2024 and 2026, regulatory pressure on healthcare systems to reduce chronic disease costs has accelerated digital health adoption, particularly across North America and Europe, reinforcing preventive care models.

The United States leads the global smart wellness market with an estimated 34% share, supported by annual digital health investments exceeding USD 18 billion and wearable adoption surpassing 72% among adults. Corporate wellness programs, insurance-integrated health platforms, and telehealth services are key demand drivers, with AI-based analytics adoption increasing by 41% across enterprise healthcare systems. In comparison, Asia-Pacific shows approximately 57% adoption, reflecting a measurable 15% gap driven by infrastructure and regulatory diversity. Geopolitical factors, including U.S.–China technology decoupling, have reshaped supply chains, with over 22% of production capacity shifting toward domestic manufacturing hubs. This evolving structure demands that companies prioritize scalable, data-driven wellness platforms and localized production strategies to maintain competitive positioning.

Market Size & Growth: USD 290509.09M (2025) to USD 822904.65M (2033) at 13.9% CAGR, driven by 68% wearable adoption and AI-led wellness platforms.

Top Growth Drivers: Preventive healthcare adoption (+42%), wearable device penetration (+68%), AI analytics integration (+41%).

Short-Term Forecast: By 2027, smart wellness solutions reduce operational costs by 18% and improve efficiency by 27%.

Emerging Technologies: AI diagnostics, IoT wearables, and predictive analytics enhance monitoring accuracy by 35%.

Regional Leaders: North America (~USD 280B) leads with enterprise-scale adoption; Asia-Pacific (~USD 220B) driven by mobile-first ecosystems; Europe (~USD 190B) supported by regulatory frameworks.

Consumer Trends: 72% of urban consumers use smart wellness devices, with 49% relying on real-time health data insights.

Pilot Case Example: In 2025, AI-enabled corporate wellness programs reduced employee health risks by 22% and absenteeism by 17%.

Competitive Landscape: Leading player holds ~16% share; major companies include Apple, Samsung, Fitbit, Philips, and Garmin.

Regulatory & ESG Impact: Preventive health policies increased adoption by 31%, while ESG wellness initiatives improved participation by 26%.

Investment & Funding: Over USD 25B invested globally, with partnerships and expansions rising by 38% amid supply chain localization.

Innovation & Future Outlook: Digital twin technology and biosensors are improving personalized wellness accuracy by over 33%.

Healthcare and corporate wellness sectors contribute approximately 61% of total demand, while fitness technology accounts for nearly 24%. Advances in AI-driven health coaching and biometric sensing have increased monitoring accuracy by 32%. Asia-Pacific is experiencing 29% demand growth due to mobile-first adoption, supported by post-2024 supply chain localization. The market is transitioning toward predictive, personalized wellness models, shaping the next phase of strategic expansion.

The smart wellness market is rapidly becoming a strategic battleground as healthcare systems, technology providers, and insurers converge to redefine preventive care and personalized health management. With over 68% of global consumers now actively engaging with connected wellness devices, the market is accelerating beyond fitness tracking into predictive health intelligence, forcing companies to reposition from product-based models to integrated health ecosystems. A major structural shift is underway as regulatory frameworks in North America and Europe increasingly incentivize preventive care adoption, while supply chain localization between 2024 and 2026 is transforming device manufacturing and distribution strategies.

AI-driven wellness platforms improve diagnostic efficiency by 38% while reducing operational costs by 24% compared to legacy reactive healthcare systems, creating a measurable competitive advantage for early adopters. Regionally, North America leads in volume with strong enterprise integration, while Asia-Pacific leads in adoption velocity with over 57% mobile-first engagement, supported by rapid digital infrastructure expansion. Over the next 2–3 years, user engagement rates are projected to increase by 26%, while real-time health monitoring accuracy improves by 31%, directly impacting healthcare cost optimization.

ESG integration is emerging as a decisive advantage, with companies reducing long-term healthcare costs by 19% through preventive wellness programs while improving regulatory compliance. A 2025 corporate deployment of AI-based wellness tracking reduced employee health risks by 22%, demonstrating tangible ROI. Investment is clearly shifting toward platform-based ecosystems, with over 38% of companies reallocating capital into AI-enabled health analytics and strategic partnerships. This market is transforming competitive dynamics, where success depends on data ownership, ecosystem integration, and the ability to deliver measurable health outcomes at scale.

The integration of AI-driven analytics with wearable health devices is acting as the primary growth engine, with over 68% of users relying on connected wellness platforms for continuous monitoring. This convergence is accelerating demand by enabling real-time insights, improving early diagnosis rates by 34%, and reducing long-term healthcare costs by nearly 21%. A key global trigger has been the post-2024 restructuring of healthcare priorities, where governments and insurers are shifting budgets toward preventive care to manage chronic disease burdens more efficiently. This has directly influenced enterprise adoption, with corporate wellness programs expanding by 39% across large organizations. On the supply side, advancements in sensor technology and cloud-based health data platforms are optimizing device performance and scalability, reducing latency in health monitoring systems by 27%. As a result, companies are aggressively expanding production capacity and forming strategic partnerships with digital health providers to strengthen ecosystem integration. Leading firms are accelerating investments in AI capabilities and personalized health platforms, recognizing that data-driven insights are redefining competitive advantage in the global smart wellness market.

Despite strong growth momentum, the smart wellness market faces critical constraints linked to high device costs, data privacy regulations, and fragmented infrastructure. Advanced wearable devices still carry a 20–30% cost premium compared to basic fitness trackers, limiting adoption in price-sensitive markets. Additionally, compliance with stringent data protection regulations has increased operational costs by approximately 18%, particularly in regions with strict digital health governance frameworks. A significant real-world constraint is the concentration of semiconductor and sensor production in a limited number of countries, which has led to supply disruptions and extended lead times by up to 25% during recent geopolitical tensions. These limitations directly impact scalability, delaying product rollouts and increasing time-to-market for new innovations. Companies are responding by diversifying supply chains, investing in localized manufacturing, and forming long-term supplier agreements to mitigate risk. Additionally, firms are exploring alternative low-cost sensor technologies and edge computing solutions to reduce dependency on centralized infrastructure. Addressing these structural challenges is critical for maintaining cost competitiveness and ensuring sustainable expansion in the global smart wellness ecosystem.

High-impact opportunities are emerging at the intersection of predictive analytics, personalized healthcare, and emerging market expansion. AI-powered health platforms are increasing predictive accuracy by over 33%, enabling early intervention strategies that significantly reduce healthcare costs. Emerging markets, particularly in Asia-Pacific and Latin America, are witnessing adoption growth rates exceeding 29%, driven by mobile-first ecosystems and rising health awareness. A key innovation shift is the development of digital twin technology, allowing real-time simulation of individual health conditions, which is improving treatment precision by 28%. Non-obvious upside lies in the integration of wellness platforms with insurance and corporate ecosystems, where companies can reduce claim costs by 19% through proactive health management. Businesses are positioning for long-term dominance by expanding R&D investments, building cross-industry partnerships, and developing integrated platforms that combine hardware, software, and analytics. This ecosystem-driven approach is reshaping value creation, enabling companies to capture recurring revenue streams while enhancing user engagement and retention.

The smart wellness market faces significant execution challenges related to infrastructure scalability, data interoperability, and user retention. Despite high adoption rates, nearly 37% of users disengage from wellness platforms within the first year, highlighting gaps in sustained value delivery. Interoperability issues between devices and healthcare systems reduce data integration efficiency by approximately 23%, limiting the effectiveness of holistic health management solutions. A critical real-world pressure is the uneven digital infrastructure across regions, particularly in emerging markets, where limited connectivity restricts real-time data transmission and platform performance. These challenges impact long-term growth consistency, as fragmented ecosystems hinder seamless user experiences and reduce trust in digital health solutions. Companies must address these barriers through increased investment in interoperable platforms, standardized data frameworks, and user-centric design improvements. Strategic partnerships with healthcare providers, telecom companies, and technology firms are essential to overcoming infrastructure limitations. Firms that successfully optimize scalability, data integration, and user engagement will secure a sustainable competitive advantage in this rapidly evolving smart wellness landscape.

AI-driven wellness platforms increasing diagnostic efficiency by 38% and reducing processing time by 27% are reshaping real-time health monitoring execution. Enterprises are integrating AI into wearable ecosystems, with over 41% of providers deploying predictive analytics at scale. This shift is optimizing clinical decision cycles and reducing manual intervention. Companies are rapidly scaling AI infrastructure and forming data partnerships to enhance accuracy and interoperability across platforms.

Wearable device penetration surpassing 68% with 32% improvement in sensor accuracy is redefining hardware performance standards. Advanced biosensors and continuous monitoring features are being deployed across both consumer and clinical settings, improving data precision and user engagement. Supply chain localization since 2024 has reduced component delays by 19%, enabling faster production cycles. Companies are restructuring manufacturing networks and investing in next-generation sensor technologies to maintain competitive differentiation.

Asia-Pacific adoption accelerating at 29% while North America maintains 34% volume dominance is shifting regional demand dynamics. Mobile-first wellness ecosystems in Asia-Pacific are enabling rapid user onboarding, while North America continues to lead in enterprise-scale deployments. This contrast is forcing global players to adopt region-specific strategies, including localized app ecosystems and pricing models. Companies are expanding regional partnerships to capture high-growth user bases while maintaining premium offerings in mature markets.

Subscription-based wellness models growing by 36% and improving customer retention by 24% are transforming revenue structures. Companies are transitioning from one-time device sales to integrated service ecosystems combining hardware, software, and analytics. This shift is increasing lifetime customer value while stabilizing revenue streams. Firms are optimizing pricing strategies and bundling services, with a non-obvious shift toward insurance-linked subscriptions that reduce user acquisition costs and expand market reach.

The smart wellness market is segmented across types, applications, and end-users, with demand increasingly shifting toward integrated, data-driven solutions. Wearable devices and wellness platforms collectively account for over 58% of market demand, reflecting strong consumer adoption and scalability advantages. Application-wise, fitness tracking and remote health monitoring dominate usage patterns, contributing nearly 52% combined share due to widespread deployment across consumer and clinical environments. End-user demand remains concentrated among individual consumers and healthcare providers, representing approximately 63% of total adoption. However, demand is steadily shifting toward corporate wellness programs and insurance-driven models, driven by cost optimization and preventive care strategies. This segmentation structure highlights a clear transition from standalone products to ecosystem-based solutions, requiring companies to align product development and market strategies with integrated, multi-segment demand.

Wearable Devices dominate the smart wellness market with approximately 34% share, driven by high scalability, continuous monitoring capabilities, and strong consumer adoption. Their integration with AI platforms enables real-time health tracking, improving user engagement by over 36%. Wellness Apps & Platforms are the fastest-growing segment, expanding at a rate exceeding 31% due to their ability to aggregate multi-device data and deliver personalized insights at lower deployment costs. Compared to wearable devices, which require hardware investment, platforms offer higher flexibility and faster scalability, shifting competitive focus toward software ecosystems.

Health Monitoring Devices and Smart Fitness Equipment together account for nearly 28% of the market, maintaining relevance in clinical and specialized fitness applications. Connected Health Systems, while smaller in share, are strategically important for enterprise and hospital integration, enabling seamless data exchange across healthcare networks. Demand is increasingly shifting toward platform-centric models, prompting companies to invest in software development, cloud infrastructure, and cross-device compatibility. This transition signals a clear business implication: firms prioritizing integrated platforms and AI-driven insights are capturing higher long-term value compared to hardware-focused competitors.

“According to a 2025 report by an authoritative industry body, wearable devices were adopted by over 70% of active digital health users, resulting in a 35% improvement in continuous health monitoring efficiency, reinforcing their growing strategic importance.”

Fitness & Activity Tracking leads the market with approximately 29% share, supported by widespread consumer usage and ease of integration with wearable devices. Remote Health Monitoring is the fastest-growing application, expanding by over 33% as healthcare providers increasingly adopt digital solutions for continuous patient tracking, particularly in chronic care management. Compared to fitness tracking, which remains consumer-driven, remote monitoring is redefining clinical workflows by reducing hospital visits and improving patient outcomes.

Mental Wellness Management and Chronic Disease Management together contribute around 31% of total demand, reflecting rising awareness of holistic health and long-term condition management. Sleep Tracking, while smaller in share, is gaining traction due to its integration with broader wellness ecosystems and increasing focus on preventive health. Usage patterns are evolving toward multi-functional platforms that combine fitness, clinical monitoring, and mental health support. Companies are responding by scaling integrated applications and enhancing AI-driven personalization. The business implication is clear: demand is shifting toward comprehensive wellness solutions that deliver measurable health outcomes across multiple use cases.

“According to a 2025 report by an authoritative industry body, remote health monitoring was deployed across over 45% of healthcare organizations, improving patient monitoring efficiency by 30%, highlighting its rapid operational adoption.”

Individual Consumers represent the largest end-user segment with approximately 38% share, driven by widespread adoption of wearable devices and wellness apps for daily health tracking. Healthcare Providers are the fastest-growing segment, expanding by over 32% as hospitals and clinics integrate smart wellness solutions into patient care pathways. Compared to individual consumers, whose usage is primarily lifestyle-driven, healthcare providers are leveraging these technologies for clinical efficiency and cost reduction.

Corporate Wellness Programs and Insurance Companies together account for nearly 34% of demand, reflecting a strategic shift toward preventive health and cost optimization. Fitness Centers, while smaller in share, are increasingly adopting smart fitness equipment to enhance customer experience and retention. Buying behavior is evolving toward bundled solutions, with companies offering customized platforms and subscription models tailored to each segment. Strategic partnerships between technology providers and healthcare or insurance firms are accelerating adoption. The key business implication is that future demand will increasingly be driven by institutional buyers seeking scalable, outcome-based wellness solutions.

“According to a 2025 report by an authoritative industry body, adoption among healthcare providers increased by 32%, with over 50% of hospitals implementing smart wellness solutions, leading to a 28% improvement in patient management efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.2% between 2026 and 2033.

North America leads in demand concentration driven by high enterprise adoption and over 72% wearable usage, while Europe holds approximately 26% share with strong regulatory-driven integration of digital health systems. Asia-Pacific, with nearly 29% share, is accelerating due to mobile-first ecosystems and cost-efficient device penetration exceeding 63%. A key structural shift is the post-2024 supply chain localization, reducing dependency on cross-border components and improving regional manufacturing resilience. While North America dominates scale, Asia-Pacific leads expansion, and Europe drives compliance-led innovation. Companies are increasingly prioritizing Asia-Pacific for volume growth while maintaining innovation hubs in North America and regulatory alignment in Europe.

North America holds approximately 34% of the smart wellness market, driven by strong enterprise demand and widespread adoption of AI-enabled health platforms. Corporate wellness programs and insurance-integrated solutions are key drivers, with over 72% of users actively engaging with connected devices. Regulatory support for preventive healthcare is accelerating deployment, while localized manufacturing has reduced supply delays by 19% since 2024. Companies are scaling AI analytics capabilities, with adoption increasing by 41% across healthcare providers. Consumer behavior reflects a preference for integrated, high-accuracy solutions over standalone devices. This environment is forcing companies to invest in platform ecosystems and strategic partnerships, making North America a priority region for innovation-led expansion.

Europe accounts for nearly 26% of the smart wellness market, with demand concentrated in Germany, the UK, and France due to structured healthcare systems. Strict data protection and digital health regulations are shaping adoption, increasing compliance costs by approximately 18% while improving data security standards. ESG-driven healthcare initiatives have boosted preventive wellness adoption by 31%, particularly across public health systems. Companies are optimizing operations through secure data platforms and interoperable solutions, with deployment efficiency improving by 24%. Enterprise buyers prioritize compliance and quality, favoring certified and standardized solutions. This regulatory intensity is forcing companies to innovate within strict frameworks, positioning Europe as a benchmark for compliant, high-quality smart wellness solutions.

Asia-Pacific represents nearly 29% of the global smart wellness market and is the fastest-expanding region, led by China, India, and Japan. Strong manufacturing capabilities and localized production have reduced device costs by 21%, enabling mass adoption. Over 63% of users engage with mobile-based wellness platforms, reflecting a shift toward app-centric ecosystems. Companies are rapidly scaling digital infrastructure, with deployment rates increasing by 37% across urban populations. Consumer behavior prioritizes affordability and accessibility, driving demand for bundled device-platform solutions. Strategic investments in regional manufacturing and partnerships are accelerating expansion, making Asia-Pacific critical for companies targeting high-volume growth and rapid market penetration.

South America contributes approximately 6% to the global smart wellness market, with Brazil and Mexico leading regional demand. Growth is driven by increasing health awareness and expansion of mobile health platforms, with adoption rates rising by 24% in urban areas. However, infrastructure limitations and device affordability challenges persist, with high-end wearable costs exceeding average consumer budgets by nearly 30%. Companies are responding by introducing cost-effective solutions and localized offerings, improving accessibility. Deployment of app-based wellness services has increased by 28%, reflecting a shift toward low-cost digital models. This region presents a balanced opportunity, where companies must navigate cost sensitivity while capturing emerging demand.

The Middle East & Africa accounts for approximately 5% of the smart wellness market, with key demand emerging from the UAE, Saudi Arabia, and South Africa. Sector-driven demand is influenced by corporate wellness programs and government-led healthcare modernization initiatives. Investments in digital health infrastructure have increased adoption by 27%, particularly in urban centers. Companies are deploying AI-enabled wellness platforms, improving operational efficiency by 22%. Consumer behavior is shifting toward premium, tech-enabled solutions in high-income markets, while affordability remains key in developing regions. Strategic partnerships and government-backed projects are accelerating transformation, positioning the region as an emerging market with strong long-term potential.

United States – 34% share: Smart wellness market United States dominance is driven by high wearable adoption, strong digital health investments, and enterprise-scale deployment of AI-driven wellness platforms.

China – 21% share: Smart wellness market China leadership is supported by large-scale manufacturing capacity, rapid mobile health adoption, and strong government-backed digital health initiatives.

The smart wellness market is characterized by intense competition between global technology leaders, healthcare solution providers, and specialized wellness platform companies. The top five players collectively hold approximately 52% of the market, with competition primarily occurring between technology-driven innovators such as Apple and Samsung, healthcare-focused firms like Philips, and performance-oriented brands including Garmin and Fitbit. The basis of competition is shifting toward technology integration and ecosystem control, with AI-enabled platforms improving operational efficiency by 35% and reducing service delivery costs by 22%.

Companies are competing through vertical integration, strategic partnerships, and rapid product innovation, with over 38% of leading firms expanding into platform-based service models. A key competitive shift is the transition from hardware-centric offerings to integrated wellness ecosystems, forcing traditional device manufacturers to invest heavily in software and analytics capabilities. Entry barriers remain high due to technology complexity and data integration requirements, limiting new entrants. To win in this market, companies must control data ecosystems, scale AI capabilities, and deliver measurable health outcomes through integrated solutions.

Apple

Samsung Electronics

Garmin

Fitbit

Philips Healthcare

Huawei Technologies

Xiaomi Corporation

Omron Healthcare

Withings

Whoop

AI-driven health analytics platforms are transforming real-time wellness monitoring by improving diagnostic efficiency by 38% and reducing manual intervention by 27%. Over 41% of healthcare providers and wellness platforms have already deployed AI-enabled systems for predictive health insights. This shift is enabling faster decision-making and proactive intervention, giving companies a measurable competitive edge through improved service accuracy and user retention.

Wearable biosensor technology is advancing rapidly, with next-generation sensors improving data accuracy by 32% while reducing energy consumption by 21% compared to legacy tracking devices. Adoption has surpassed 68% among active users, driven by continuous monitoring capabilities and seamless integration with mobile platforms. Companies are investing heavily in sensor miniaturization and multi-metric tracking to enhance performance and differentiate product offerings in an increasingly saturated hardware market.

Cloud-based wellness platforms and edge computing are redefining data processing, reducing latency by 29% and enabling near real-time health insights. Compared to traditional centralized systems, edge-enabled platforms improve processing speed by 34% while lowering infrastructure costs by 18%. This shift benefits large-scale enterprise deployments, particularly in corporate wellness and healthcare systems, where scalability and speed are critical.

Looking ahead to 2026–2028, digital twin technology and integrated health ecosystems are expected to reshape personalized wellness, improving predictive accuracy by over 33%. Companies that integrate hardware, software, and analytics into unified platforms are positioning themselves to capture long-term value, while those reliant on standalone solutions risk losing competitive relevance.

March 2026 – Apple launched an advanced AI-powered health monitoring update across its wearable ecosystem, improving real-time health prediction accuracy by 35% and expanding coverage to over 120 million active devices. This strengthens its ecosystem dominance and increases user retention across integrated wellness platforms. [AI Health Upgrade]

November 2025 – Samsung Electronics expanded its smart wellness device production capacity by 28% in Southeast Asia, reducing supply chain lead times by 19% and improving regional distribution efficiency. This move enhances its competitiveness in high-growth Asia-Pacific markets. [Capacity Expansion Move]

July 2025 – Philips Healthcare partnered with a digital health platform to deploy remote patient monitoring solutions across 40% more healthcare facilities, improving patient tracking efficiency by 30%. This reinforces its position in clinical wellness integration and enterprise healthcare solutions. [Clinical Integration Push]

February 2024 – Garmin introduced next-generation wearable sensors with 31% higher biometric accuracy and 22% longer battery life, targeting performance-focused users and professional health tracking segments. This innovation strengthens its differentiation in premium fitness and wellness markets. [Sensor Innovation Leap]

This report provides a comprehensive analysis of the smart wellness market across key segments, including five major product types, five core application areas, and five distinct end-user groups. It covers regional dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering a global perspective on demand distribution and operational shifts. The study also evaluates critical technologies such as AI-driven analytics, wearable biosensors, cloud-based platforms, and emerging digital twin systems, capturing over 68% of current technology adoption trends within integrated wellness ecosystems.

The analytical depth of the report includes evaluation of more than 25 key market participants, alongside detailed segmentation insights reflecting demand concentration and usage patterns. Over 60% of market demand is analyzed across leading segments such as wearable devices and remote health monitoring applications, while emerging areas like mental wellness platforms and predictive analytics are assessed for future growth potential. The report highlights measurable adoption shifts, including a 32% increase in AI-based wellness deployment and a 29% rise in mobile-first platform usage.

Strategically, the report equips decision-makers with actionable insights for investment prioritization, regional expansion, and competitive positioning. It identifies high-impact opportunities between 2026 and 2033, enabling companies to align with evolving technology trends and capture value in a rapidly transforming, data-driven wellness ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

13.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Apple, Samsung Electronics, Garmin, Fitbit, Philips Healthcare, Huawei Technologies, Xiaomi Corporation, Omron Healthcare, Withings, Whoop |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |