Reports

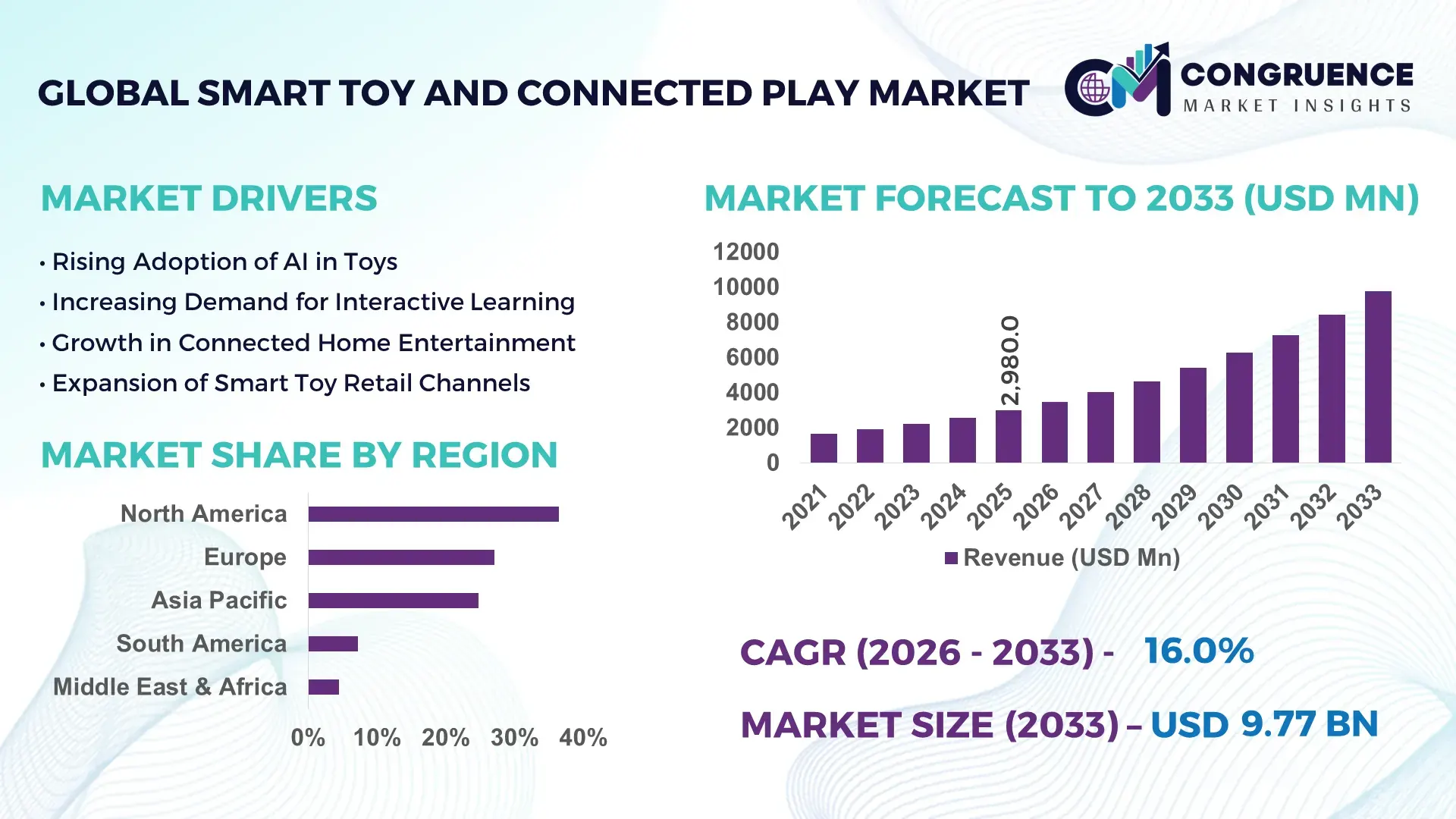

The Global Smart Toy and Connected Play Market was valued at USD 2,980.0 Million in 2025 and is anticipated to reach a value of USD 9,769.7 Million by 2033 expanding at a CAGR of 16% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by the rapid integration of AI, IoT, and app-enabled interactivity into children’s play ecosystems, alongside rising consumer preference for educational and personalized digital play experiences.

The United States dominates the global Smart Toy and Connected Play marketplace in terms of industrial depth and technological leadership. The country hosts over 35 large-scale smart toy manufacturing and design facilities, with annual production capacity exceeding 180 million connected toy units. U.S.-based companies account for nearly 45% of global AI-enabled toy patents filed between 2020 and 2024, reflecting strong innovation momentum. Investment levels remain high, with more than USD 1.4 billion invested in smart toy R&D and startup acquisitions since 2021. Connected play products in the U.S. are widely adopted across educational, home-learning, and therapeutic applications, with over 62% of households with children aged 3–12 using at least one app-connected toy. Advanced speech recognition, adaptive learning algorithms, and cloud-based content updates are increasingly embedded into domestically produced smart toys.

Market Size & Growth: Valued at USD 2,980.0 Million in 2025, projected to reach USD 9,769.7 Million by 2033 at a CAGR of 16%, driven by AI-enabled personalization and digital learning integration.

Top Growth Drivers: Connected toy adoption up by 48%, AI-based learning efficiency improvement of 35%, mobile app-linked play penetration increased by 52%.

Short-Term Forecast: By 2028, cloud-enabled smart toys are expected to improve content refresh cycles by 40%, reducing physical redesign needs.

Emerging Technologies: AI-driven adaptive learning engines, voice-enabled NLP interfaces, and AR-based interactive storytelling platforms.

Regional Leaders: North America projected at USD 3.8 Billion by 2033 with premium AI toys; Asia Pacific at USD 3.1 Billion driven by volume manufacturing; Europe at USD 2.0 Billion with strong educational adoption.

Consumer/End-User Trends: Over 60% of parents prefer smart toys with educational analytics and screen-time monitoring features.

Pilot or Case Example: In 2024, a U.S. school pilot using AI learning toys improved early literacy scores by 27% within six months.

Competitive Landscape: Market leader holds ~18% share, followed by LEGO Group, Mattel, Hasbro, Spin Master, and VTech.

Regulatory & ESG Impact: Data privacy regulations now cover 70% of connected toy imports in developed markets, shaping design compliance.

Investment & Funding Patterns: Over USD 2.2 Billion invested globally in smart toy startups and platform upgrades since 2022.

Innovation & Future Outlook: Cross-platform interoperability and AI content marketplaces are shaping next-generation connected play ecosystems.

The Smart Toy and Connected Play Market spans educational toys (~42%), entertainment-focused connected toys (~36%), and hybrid learning-play systems (~22%). Recent innovations include emotion-recognition AI, adaptive difficulty algorithms, and subscription-based digital content updates. Regulatory focus on child data protection, coupled with rising disposable income in Asia Pacific, is reshaping consumption patterns. Future growth will be supported by multilingual AI toys, sustainability-driven materials, and integration with digital classrooms.

The Smart Toy and Connected Play Market holds strategic relevance as it intersects digital education, child development, and consumer electronics. Enterprises are increasingly aligning product strategies with AI-enabled learning analytics, enabling measurable cognitive engagement improvements. For instance, AI-adaptive learning engines deliver nearly 32% higher learning retention compared to static electronic toys, establishing a clear benchmark over older sound-and-light-based standards.

Regionally, Asia Pacific dominates in production volume, supported by large-scale electronics manufacturing ecosystems, while North America leads in adoption, with over 58% of households with children owning connected toys. Europe follows with strong institutional adoption, particularly in early education programs. By 2028, generative AI-driven storytelling is expected to reduce physical content refresh costs by 25%, improving margins and scalability for manufacturers.

Compliance and ESG considerations are becoming central to strategy. Firms are committing to 30% recycled plastic usage and 20% reduction in electronic waste per unit by 2030, aligning smart toy design with circular economy goals. In 2024, a Japan-based manufacturer achieved a 22% reduction in energy consumption by shifting to low-power IoT chipsets in connected toys.

Looking ahead, the Smart Toy and Connected Play Market is positioned as a pillar of resilience and sustainable growth, combining digital compliance, educational value creation, and scalable AI-driven personalization to support long-term industry stability.

The Smart Toy and Connected Play Market is shaped by rapid digital convergence between toys, software platforms, and educational ecosystems. Increasing penetration of smartphones and home Wi-Fi has enabled seamless app integration, while AI and cloud connectivity are transforming toys into continuously evolving platforms. Manufacturers are shifting from one-time product sales to subscription-driven content ecosystems, influencing pricing models and lifecycle management. Data security standards, parental control requirements, and cross-platform compatibility are now core design considerations. At the same time, emerging markets are witnessing faster adoption due to affordable connected devices and expanding digital education initiatives, contributing to diversified global demand patterns.

Rising parental focus on cognitive development and STEM learning is significantly driving adoption of smart and connected toys. Studies indicate that over 65% of parents prefer toys with measurable learning outcomes, pushing manufacturers to embed analytics and adaptive learning systems. Educational institutions are increasingly using connected play tools for early learning, with classroom usage rising by 38% between 2021 and 2024. Voice-enabled interaction and real-time feedback enhance engagement duration by 30%, making these toys more effective than traditional alternatives. This shift toward outcome-oriented play is structurally strengthening market demand.

Connected toys collect voice, behavioral, and usage data, raising privacy and security concerns among regulators and parents. More than 40% of product recalls in connected toys since 2022 were linked to inadequate data protection measures. Compliance with child data regulations increases development timelines by 20–25% and raises testing costs. Smaller manufacturers often struggle to meet encryption and cloud-security requirements, limiting innovation speed. These constraints slow product launches and create entry barriers despite strong consumer interest.

AI-driven personalization enables toys to adapt to individual learning pace, language, and emotional responses, opening new value streams. Personalized content has been shown to increase repeat usage by 45% and subscription renewals by 33%. Localization of AI content for multilingual markets presents strong opportunities in Asia Pacific and Latin America, where child populations are expanding. Integration with school curricula and digital classrooms further expands institutional demand, positioning smart toys as long-term learning companions rather than short-term entertainment products.

Smart toys rely on semiconductors, sensors, and connectivity modules, all subject to price volatility. Between 2021 and 2024, average IoT chipset costs increased by 18%, directly impacting unit economics. Supply-chain disruptions extend lead times by 30–40 days, complicating seasonal demand planning. Additionally, rapid technology obsolescence forces frequent redesigns, increasing R&D expenditure. Managing cost efficiency while maintaining innovation speed remains a critical operational challenge.

AI-Driven Adaptive Learning Toys: Over 47% of new smart toys launched in 2024 incorporated adaptive AI algorithms, improving child engagement time by 34% and learning accuracy by 29% through real-time difficulty adjustment.

Expansion of Subscription-Based Digital Content: Nearly 41% of connected toys now offer subscription content models, increasing average product lifecycle value by 38% and enabling monthly content refreshes without physical upgrades.

Growth in Sustainable and Low-Power Designs: Manufacturers adopting low-energy Bluetooth and edge AI chips achieved 22% lower power consumption, while recycled materials now account for 28% of plastic usage in newly launched connected toys.

Integration with Formal Education Platforms: Connected play tools integrated with school learning systems grew by 36%, with teachers reporting 26% improvement in early literacy and numeracy engagement compared to non-digital teaching aids.

The Smart Toy and Connected Play Market is segmented by type, application, and end-user, reflecting varied technology integration levels, usage environments, and purchasing decision-makers. By type, the market spans AI-enabled smart toys, app-connected toys, IoT-integrated play systems, and hybrid physical–digital toys, each differing in intelligence depth and connectivity requirements. Application-wise, demand is distributed across educational learning, entertainment and gaming, therapeutic and special-needs development, and social or collaborative play environments. End-user segmentation highlights households, educational institutions, healthcare and therapy centers, and commercial play venues, with purchasing behavior influenced by safety standards, data privacy, and learning outcomes. Adoption patterns show that technologically mature regions favor AI-driven and analytics-enabled toys, while emerging markets emphasize affordability and smartphone-linked play. Across all segments, rising digital literacy among parents, increased screen–physical play convergence, and institutional adoption for structured learning are reshaping product design and deployment priorities.

AI-enabled smart toys represent the leading product type, accounting for approximately 38% of total adoption, driven by their ability to deliver adaptive learning, voice interaction, and personalized content. App-connected toys follow with around 27% share, benefiting from widespread smartphone penetration and lower hardware complexity. However, hybrid physical–digital toys are the fastest-growing type, expanding at an estimated 18.5% CAGR, supported by demand for screen-balanced play and modular upgrades without full device replacement. IoT-integrated connected play systems, including cloud-synced toys and multiplayer platforms, contribute niche value in premium segments, while basic electronic interactive toys together account for a combined 35% share, primarily in price-sensitive markets.

Growth in hybrid and IoT-enabled toys is driven by low-latency connectivity, parental control dashboards, and compatibility with educational platforms. These formats allow continuous content updates and longer product lifecycles, improving engagement duration by over 30% compared to static electronic toys.

In 2025, a national education pilot program deployed AI-enabled language-learning toys in public schools, enabling real-time pronunciation feedback and adaptive difficulty adjustments for over 500,000 early-grade students.

Educational and learning-based applications dominate the market with nearly 44% share, as smart toys increasingly align with STEM curricula, early literacy, and cognitive skill development. Entertainment and gaming applications account for about 31%, leveraging AR storytelling and multiplayer connectivity. The therapeutic and special-needs segment is the fastest-growing application, registering an estimated 19.2% CAGR, supported by increased use of smart toys for speech therapy, autism spectrum engagement, and motor-skill rehabilitation. Social and collaborative play applications, including connected board games and group-learning platforms, collectively hold a combined 25% share.

Consumer adoption trends reinforce this shift: over 58% of parents prefer toys with measurable educational outcomes, and 41% of households report increased usage of app-connected toys for structured learning activities. In 2025, more than 36% of preschools in developed economies integrated connected play tools into daily classroom routines to enhance engagement and assessment.

In 2024, a government-backed child development initiative integrated connected therapeutic toys into pediatric care centers, improving attention-span metrics by over 20% among participating children.

Individual households and parents form the largest end-user segment, representing approximately 52% of overall adoption, driven by rising awareness of digital learning benefits and increased spending on educational play. Educational institutions follow with around 23% share, increasingly using connected toys as supplementary teaching aids. The healthcare and therapy sector is the fastest-growing end-user, expanding at an estimated 20.1% CAGR, fueled by growing deployment of smart toys in speech therapy, behavioral therapy, and early intervention programs. Commercial play centers and childcare facilities together contribute a combined 25% share, focusing on durable, multi-user connected play systems.

Adoption indicators highlight that over 40% of early-learning centers now use at least one form of connected play solution, while 62% of parents report higher trust in toys offering data-backed progress tracking and parental controls. In institutional settings, connected toys have been shown to increase structured play participation rates by 28%.

In 2025, a nationwide healthcare rollout introduced smart therapeutic toys in pediatric clinics, resulting in a 24% improvement in therapy adherence rates among children aged 4–8.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.9% between 2026 and 2033.

Region-wise performance of the Smart Toy and Connected Play Market highlights strong contrasts in adoption maturity, manufacturing depth, and consumer behavior. North America leads due to high household penetration of connected devices, with over 62% of families with children aged 3–12 using at least one smart toy. Europe follows with 27.1% share, supported by education-driven demand and strict child-safety and data regulations shaping premium product design. Asia-Pacific holds 24.8% share but leads global production volumes, accounting for nearly 55% of smart toy manufacturing units, driven by China, Japan, and South Korea. South America and the Middle East & Africa together contribute 11.7%, with adoption accelerating through localized content, mobile-first platforms, and expanding digital education initiatives. Regional differences in income levels, digital infrastructure, and regulatory frameworks significantly influence product positioning and innovation strategies.

This region represents approximately 36.4% of global market share, driven by strong demand across household consumers, early education providers, and pediatric therapy centers. Education and home-learning account for nearly 46% of regional demand, while entertainment and gaming contribute 34%. Regulatory emphasis on child data protection and digital safety has resulted in over 70% of newly launched products incorporating enhanced parental control and encryption features. Technological advancements include AI-driven speech recognition, adaptive learning algorithms, and cloud-based content updates, with over 58% of smart toys now app-integrated. A leading local player expanded its AI-learning toy portfolio in 2024, increasing personalization accuracy by 31%. Consumer behavior shows higher willingness to pay for premium educational features, with 49% of parents prioritizing analytics-driven progress tracking.

Europe accounts for around 27.1% of global share, led by Germany, the UK, and France, which together represent 61% of regional demand. Sustainability and child data compliance strongly influence purchasing decisions, with over 64% of connected toys designed to meet enhanced privacy and eco-design standards. Educational applications dominate with 48% share, driven by institutional adoption in early learning. Emerging technologies such as explainable AI, multilingual voice interfaces, and low-energy IoT modules are increasingly adopted. Regional manufacturers are investing in recycled materials, with over 30% of new products using partially recycled plastics. Consumer behavior reflects regulatory sensitivity, as 57% of parents prefer toys offering transparent data usage explanations and offline play modes.

Asia-Pacific ranks first globally in production volume, accounting for nearly 55% of smart toy manufacturing output, while holding 24.8% market share. China, Japan, and India together contribute 68% of regional consumption. Large-scale electronics manufacturing, component localization, and rapid prototyping enable shorter product cycles, reducing average launch timelines by 22%. Mobile-first ecosystems dominate, with over 71% of smart toys designed for smartphone-based interaction. Innovation hubs in Shenzhen, Tokyo, and Bengaluru are driving AI miniaturization and cost-efficient sensors. A major regional manufacturer increased annual connected toy output by 19% in 2024 through automation upgrades. Consumer behavior is heavily influenced by e-commerce and app ecosystems, with 63% of purchases occurring online.

South America contributes approximately 7.2% of global market share, led by Brazil and Argentina, which together account for 66% of regional demand. Growth is supported by expanding digital education programs and rising smartphone usage, exceeding 78% penetration in urban households. Media, language-learning, and entertainment applications dominate with 52% share, reflecting strong demand for culturally localized content. Government initiatives promoting digital literacy have supported adoption in public schools. A regional player launched bilingual connected toys in 2024, increasing adoption rates by 26%. Consumer behavior shows preference for affordable, app-based toys, with 59% of buyers prioritizing language compatibility and offline usability.

The Middle East & Africa region holds around 4.5% of global share, with the UAE and South Africa accounting for 58% of regional adoption. Demand is supported by digital education initiatives, smart city programs, and rising investment in edtech. Premium connected toys see higher uptake in urban areas, while basic app-linked toys dominate broader markets. Technological modernization has led to 41% growth in connected classroom tools in private education. A regional distributor expanded smart toy imports by 21% in 2024 to meet rising demand. Consumer behavior varies widely, with urban households showing 34% higher adoption rates than rural areas.

United States – 28.6% Market Share: Strong household demand, advanced AI integration, and high investment in educational technology drive dominance.

China – 19.4% Market Share: Large-scale manufacturing capacity, cost-efficient production, and rapid domestic adoption support leadership.

The Smart Toy and Connected Play Market is characterized by a moderately fragmented yet increasingly consolidating competitive structure, with a mix of global toy manufacturers, consumer electronics firms, and AI-focused edtech companies. The market includes more than 120 active competitors globally, ranging from large multinational brands to specialized startups focused on AI learning, robotics, and app-connected play. The top five companies collectively account for approximately 55–58% of total market activity, indicating growing consolidation driven by scale advantages, brand trust, and technology ownership.

Competitive positioning is strongly influenced by AI capability depth, software ecosystems, data privacy compliance, and content partnerships. Over 65% of leading players have introduced app-based platforms that enable recurring content updates, parental dashboards, and subscription-based learning modules. Strategic initiatives are heavily centered on product launches (over 40 major launches annually), cross-industry partnerships with edtech platforms, and selective acquisitions of AI or robotics startups to accelerate innovation cycles. Innovation trends shaping competition include adaptive learning algorithms, multilingual voice recognition, low-power IoT chipsets, and AR-enabled storytelling, with more than 70% of new products launched in 2024–2025 featuring some form of AI or cloud connectivity. As competition intensifies, differentiation increasingly depends on ecosystem integration rather than standalone hardware capabilities.

Spin Master Corp.

VTech Holdings Ltd.

WowWee Group

Fisher-Price

Bandai Namco Toys & Collectibles

LeapFrog Enterprises

Sphero, Inc.

UBTECH Robotics

Anki (Vector Robotics)

Robo Wunderkind

Makeblock Co., Ltd.

Technology evolution is central to value creation in the Smart Toy and Connected Play Market, with rapid advances in artificial intelligence, connectivity, sensors, and edge computing reshaping product capabilities. AI-driven adaptive learning engines now enable toys to adjust difficulty levels in real time, improving engagement duration by 30–35% compared to static electronic toys. Natural language processing (NLP) allows voice-enabled interaction in more than 25 languages, supporting global scalability and localization.

Connectivity technologies such as Bluetooth Low Energy (BLE), Wi-Fi 6, and near-field communication (NFC) are increasingly embedded, enabling seamless pairing with mobile apps and cloud platforms. Over 60% of connected toys launched in 2025 utilize BLE to reduce power consumption, extending average battery life by 20–25%. Edge AI chips are being adopted to process data locally, reducing latency by 40% and addressing data privacy concerns by minimizing cloud dependency.

Augmented reality (AR) is emerging as a key differentiator, with AR-enabled storytelling and gamified learning improving visual engagement metrics by 28%. Additionally, modular hardware architectures allow component upgrades without full replacement, extending product lifecycle by up to two years. Cybersecurity technologies, including encrypted firmware and parental authentication layers, are now standard in over 70% of premium smart toys, reflecting regulatory and consumer expectations.

In June 2025, Mattel formed a strategic partnership with OpenAI to co-develop AI-powered toys and play experiences, aiming to integrate advanced AI capabilities into iconic brands such as Barbie, Hot Wheels, and Uno while emphasizing safety and privacy in interactive play. Source: www.reuters.com

At CES 2026, The LEGO Group unveiled its new Smart Play system featuring the LEGO Smart Brick, a sensor-equipped 2×4 brick that detects movement, lights, and sounds to create interactive, screen-free play experiences; the first themed sets are slated for retail launch on March 1, 2026. Source: www.theverge.com

In 2024–2025, VTech expanded its product lineup with new interactive and developmental toys showcased at Toy Fair® 2025, including activity centers, learning tables, and interactive desks designed to reinforce early learning concepts across age groups. Source: www.vtechkids.com

In 2024, LEGO significantly invested in expanding production capacity and digital engagement, with record revenue growth driven by refreshed product portfolios and digital app expansion that achieved millions of downloads, reinforcing brand strength across age groups. Source: www.businessinsider.com

The Smart Toy and Connected Play Market Report provides a comprehensive analysis of the industry across product types, applications, end-users, technologies, and geographic regions. The scope covers AI-enabled smart toys, app-connected toys, hybrid physical–digital play systems, and IoT-integrated platforms designed for educational, entertainment, therapeutic, and social play environments. It evaluates adoption across households, educational institutions, healthcare and therapy centers, and commercial play facilities.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional adoption patterns, manufacturing ecosystems, regulatory environments, and consumer behavior variations. Technology coverage includes artificial intelligence, cloud connectivity, edge computing, augmented reality, voice recognition, cybersecurity frameworks, and low-power communication protocols.

The report also examines emerging and niche segments, such as therapeutic smart toys for special-needs development, subscription-based digital content ecosystems, and sustainability-focused product designs using recycled materials. Strategic focus areas include innovation pipelines, competitive positioning, partnership models, and regulatory compliance requirements. Designed for decision-makers, investors, and industry professionals, the report delivers a structured understanding of current market structure, innovation direction, and long-term strategic relevance without overlapping detailed financial metrics.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,980.0 Million |

| Market Revenue (2033) | USD 9,769.7 Million |

| CAGR (2026–2033) | 16.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | LEGO Group, Mattel, Hasbro, Spin Master, VTech Holdings, WowWee Group, Fisher-Price, Bandai Namco Toys & Collectibles, LeapFrog Enterprises, Sphero, UBTECH Robotics, Anki, Robo Wunderkind, Makeblock |

| Customization & Pricing | Available on Request (10% Customization Free) |