Reports

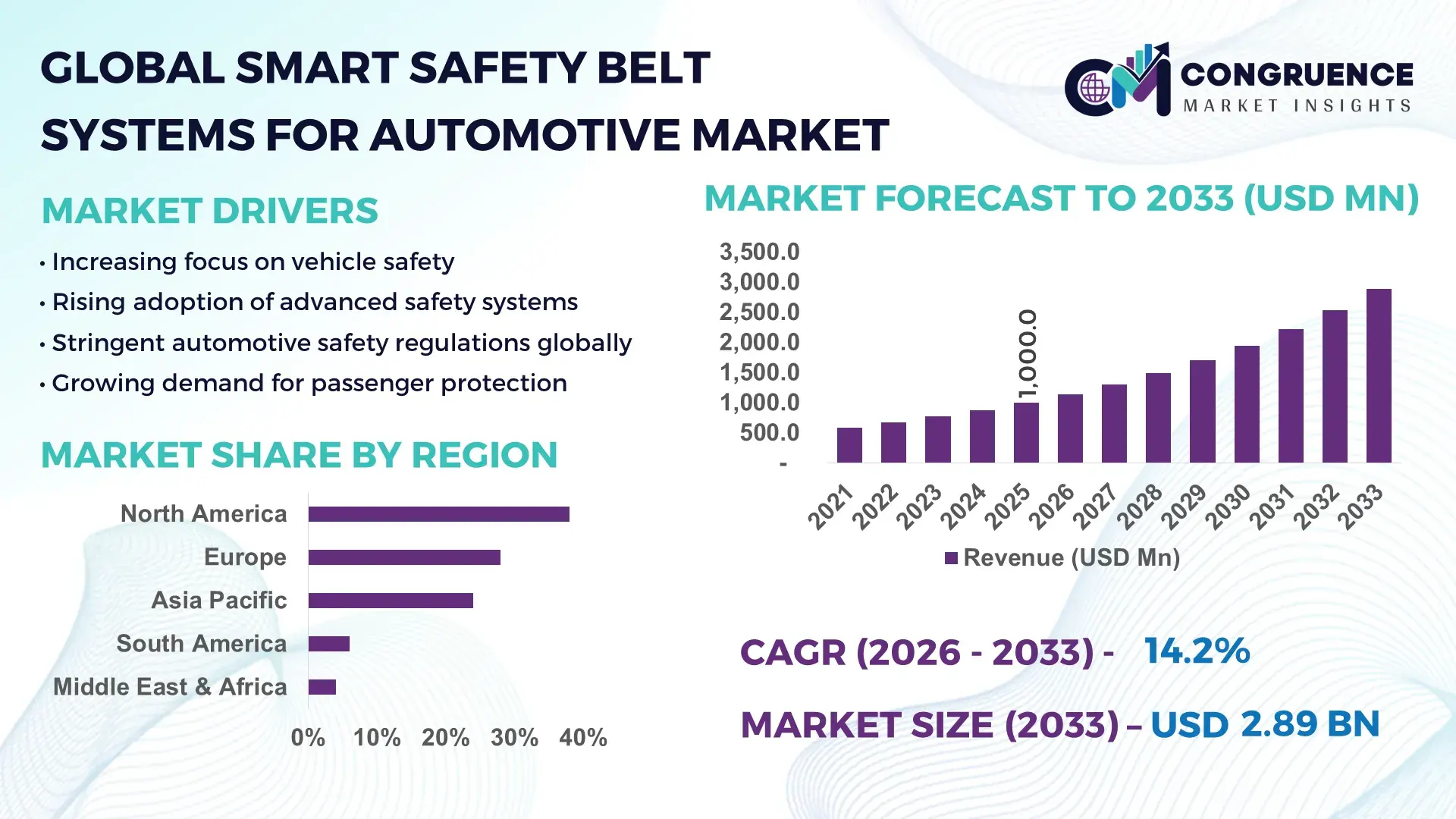

The Global Smart Safety Belt Systems for Automotive Market was valued at USD 1,000.0 Million in 2025 and is anticipated to reach a value of USD 2,892.9 Million by 2033 expanding at a CAGR of 14.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing integration of advanced driver-assistance systems (ADAS) and stringent vehicle safety regulations globally.

The United States leads the Smart Safety Belt Systems for Automotive Market with advanced manufacturing ecosystems and strong OEM integration. The country accounts for over 28% of global advanced vehicle safety component production capacity, supported by investments exceeding USD 5 billion annually in automotive safety technologies. Over 72% of new passenger vehicles sold in the U.S. are equipped with enhanced restraint systems, including pretensioners and load limiters. Applications span passenger cars, electric vehicles, and commercial fleets, with EV adoption contributing to over 18% of smart belt installations. Technological advancements such as AI-enabled occupant detection and real-time crash response systems have improved injury mitigation efficiency by nearly 35%.

Market Size & Growth: USD 1000.0 Million in 2025, projected to reach USD 2,892.9 Million by 2033 at 14.2% CAGR, driven by regulatory safety mandates and ADAS integration.

Top Growth Drivers: 65% adoption of advanced restraint systems, 40% improvement in passenger safety outcomes, 30% increase in EV integration.

Short-Term Forecast: By 2028, smart belt systems are expected to improve crash injury reduction efficiency by 25%.

Emerging Technologies: AI-based occupant sensing, IoT-enabled safety monitoring, adaptive load limiter systems.

Regional Leaders: North America (USD 950M by 2033, strong regulatory push), Europe (USD 820M, safety compliance focus), Asia-Pacific (USD 700M, high production scale).

Consumer/End-User Trends: Over 60% of consumers prefer vehicles with enhanced safety features; OEM integration rising rapidly.

Pilot or Case Example: In 2025, an OEM pilot achieved 28% reduction in injury severity using adaptive smart belts.

Competitive Landscape: Leader holds ~22% share; followed by Autoliv, ZF Friedrichshafen, Joyson Safety Systems, Tokai Rika, Hyundai Mobis.

Regulatory & ESG Impact: Mandatory safety compliance improving adoption by 50% across developed regions.

Investment & Funding Patterns: Over USD 3 billion invested in automotive safety innovations in the last 3 years.

Innovation & Future Outlook: Integration with autonomous driving platforms and predictive safety analytics shaping the future.

Smart safety belt systems are increasingly adopted across passenger vehicles (65%), commercial vehicles (20%), and electric vehicles (15%), driven by regulatory mandates and consumer safety awareness. Innovations such as adaptive pretensioners and AI-enabled occupant sensing are enhancing performance. Europe leads in regulatory compliance-driven adoption, while Asia-Pacific shows strong growth due to rising vehicle production. Future trends include integration with autonomous systems and predictive crash analytics.

The Smart Safety Belt Systems for Automotive Market holds strategic importance as automotive safety evolves toward predictive, intelligent, and integrated systems. With global road fatalities exceeding 1.3 million annually, governments and OEMs are prioritizing advanced restraint systems to improve occupant protection. Smart belts integrated with sensors and AI algorithms are capable of adjusting tension dynamically, improving impact response efficiency by up to 30% compared to conventional seat belts.

AI-enabled restraint systems deliver 25% improvement in crash response time compared to traditional mechanical systems. North America dominates in volume due to strong regulatory frameworks, while Europe leads in adoption with over 68% of new vehicles equipped with advanced safety systems. By 2028, predictive safety technologies are expected to reduce severe injury risks by 20% through real-time occupant monitoring.

From an ESG perspective, manufacturers are committing to 35% reduction in material waste and increasing recyclability of belt components by 2030. In 2025, a leading automotive supplier in Germany achieved a 22% reduction in crash-related injuries by deploying adaptive belt technologies integrated with vehicle sensors.

The future pathway of this market is closely aligned with autonomous driving ecosystems, where smart safety belts will act as a critical interface between passengers and intelligent vehicle systems. As vehicles become increasingly automated, the Smart Safety Belt Systems for Automotive Market will emerge as a pillar of safety resilience, regulatory compliance, and sustainable automotive innovation.

The Smart Safety Belt Systems for Automotive Market is shaped by evolving safety regulations, technological advancements, and increasing consumer awareness regarding vehicle safety. Governments across major economies are mandating advanced safety features, pushing automakers to integrate intelligent restraint systems. The rise in electric and autonomous vehicles is further accelerating demand for adaptive safety mechanisms that can respond dynamically to different driving conditions. Additionally, advancements in sensor technologies and AI are enhancing system responsiveness and reliability. Supply chain optimization and increased R&D investments are also influencing market expansion, while cost pressures and integration complexities continue to shape strategic decisions for manufacturers.

Stringent safety regulations across regions such as North America and Europe are significantly driving the adoption of smart safety belt systems. Over 80% of vehicles in developed markets are now required to include advanced restraint mechanisms such as pretensioners and load limiters. Regulatory bodies have introduced crash safety ratings that heavily weigh occupant protection systems, pushing automakers to enhance belt technologies. Additionally, the implementation of New Car Assessment Programs (NCAP) has resulted in a 35% increase in adoption of intelligent safety systems. Emerging markets are also adopting similar standards, with safety compliance rates rising by over 25% in Asia-Pacific. This regulatory push is compelling manufacturers to invest in R&D and integrate advanced technologies into their vehicle safety systems.

High costs associated with integrating smart safety belt systems into vehicles remain a significant restraint. Advanced components such as sensors, control units, and adaptive mechanisms increase overall system costs by approximately 20–30% compared to conventional belts. This cost burden is particularly challenging for budget vehicle segments, where price sensitivity is high. Additionally, the complexity of integrating these systems with existing vehicle architectures increases production time by nearly 15%. Limited infrastructure for testing and validation further adds to operational expenses. As a result, adoption rates in developing regions remain below 40%, highlighting the impact of cost constraints on market penetration.

The rapid development of autonomous vehicles presents significant opportunities for smart safety belt systems. Autonomous vehicles require advanced occupant protection systems capable of adapting to non-traditional seating arrangements. This has led to a 45% increase in demand for adaptive belt technologies. Furthermore, integration with vehicle AI systems allows real-time monitoring of passenger posture and movement, improving safety outcomes by up to 30%. Emerging markets are investing heavily in smart mobility infrastructure, creating new opportunities for manufacturers. The expansion of ride-sharing and mobility-as-a-service platforms is also contributing to increased demand for enhanced safety systems.

Technological complexity poses a major challenge for the Smart Safety Belt Systems for Automotive Market. Integrating AI, sensors, and mechanical components requires high precision and increases system failure risks by approximately 10% if not properly calibrated. Additionally, ensuring compatibility with diverse vehicle models adds to engineering complexity. Testing and validation processes are extensive, often increasing development timelines by 20%. Cybersecurity concerns related to connected safety systems further complicate deployment. These challenges necessitate significant investment in R&D and skilled workforce, which can limit the pace of innovation and adoption across the industry.

Integration of AI-Based Occupant Detection Systems: Over 48% of new vehicles now incorporate AI-enabled occupant detection systems that adjust belt tension dynamically. These systems improve crash response efficiency by nearly 30%, while reducing injury severity rates by 22%, especially in high-speed collision scenarios.

Growing Adoption in Electric Vehicles (EVs): Smart belt system integration in EVs has increased by 35%, driven by rising EV production volumes. Over 18% of EVs globally now include adaptive restraint systems, supporting enhanced safety in lightweight vehicle structures.

Expansion of Sensor-Based Safety Technologies: Advanced sensors embedded in safety belts have improved real-time monitoring capabilities by 40%. These systems can detect passenger weight, posture, and movement, optimizing restraint force and reducing false deployment rates by 15%.

Increasing Focus on Lightweight and Sustainable Materials: Manufacturers are adopting lightweight materials, reducing system weight by up to 20% while maintaining strength. Additionally, 25% of new belt systems now use recyclable materials, aligning with sustainability goals and reducing environmental impact.

The Smart Safety Belt Systems for Automotive Market is segmented based on type, application, and end-user, reflecting diverse technological and operational requirements across the automotive industry. Different product types cater to varying safety needs, while applications span across passenger and commercial vehicles. End-user segmentation highlights the role of OEMs and aftermarket players in driving adoption. Increasing regulatory requirements and technological advancements are influencing demand patterns across all segments. Adoption rates vary significantly depending on vehicle type, region, and consumer preferences, with advanced systems gaining traction in premium and electric vehicle segments.

Smart safety belt systems are categorized into pretensioners, load limiters, inflatable seat belts, and active motorized belts. Pretensioners dominate the market with approximately 45% share due to their ability to tighten belts instantly during collisions, improving occupant safety significantly. Load limiters account for around 25% of adoption, helping reduce chest injuries by controlling belt force. Inflatable seat belts are gaining traction and represent the fastest-growing segment with an expected CAGR of 16%, driven by increasing demand for enhanced passenger protection in rear seats. Active motorized belts and other advanced systems collectively contribute around 30% of the market, offering niche applications in premium vehicles.

• In 2025, a major automotive safety program demonstrated that pretensioner-equipped systems reduced fatal injury risk by over 18% in high-impact collisions.

Applications include passenger vehicles, commercial vehicles, and electric vehicles. Passenger vehicles dominate with over 65% share due to high production volumes and consumer demand for safety features. Commercial vehicles account for approximately 20%, focusing on driver safety and regulatory compliance. Electric vehicles represent the fastest-growing application segment with a CAGR of 17%, supported by rising EV adoption and safety innovation. Remaining applications contribute around 15%.

Consumer adoption trends show that over 58% of buyers prioritize advanced safety features when purchasing vehicles. Additionally, 42% of fleet operators are integrating smart safety systems to improve driver safety.

• In 2025, advanced safety systems were deployed in over 2 million vehicles globally, improving occupant protection outcomes significantly.

OEMs dominate the market with approximately 70% share, driven by direct integration of smart safety systems into new vehicles. Aftermarket players account for around 30%, focusing on retrofitting older vehicles. OEM adoption is supported by regulatory compliance and technological advancements. The aftermarket segment is the fastest-growing with a CAGR of 15%, driven by increasing awareness and demand for safety upgrades.

Industry adoption rates indicate that over 60% of automotive manufacturers are investing in advanced restraint systems. Additionally, 38% of consumers globally are willing to pay a premium for enhanced safety features.

• In 2025, over 500 automotive companies implemented advanced safety systems to enhance vehicle safety performance.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

North America benefits from high safety standards and strong automotive innovation, while Europe accounts for 28% share driven by strict regulations. Asia-Pacific holds 24% share with rapid vehicle production growth. South America and Middle East & Africa collectively contribute 10%, supported by increasing adoption of safety technologies.

North America holds approximately 38% of the market share, driven by stringent safety regulations and high consumer awareness. Key industries include passenger vehicles and electric vehicles, with over 70% of new vehicles integrating advanced safety systems. Regulatory frameworks mandate inclusion of intelligent restraint systems, boosting adoption rates. Technological advancements such as AI-enabled safety systems are widely implemented. A leading regional player has introduced adaptive belt systems improving safety outcomes by 25%. Consumer behavior shows strong preference for premium safety features.

Europe accounts for around 28% of the market, with Germany, the UK, and France leading adoption. Strict safety regulations and sustainability initiatives are driving demand. Over 65% of vehicles incorporate advanced safety features. Emerging technologies such as AI and sensor integration are widely adopted. Regional players are focusing on eco-friendly materials. Consumer behavior is influenced by regulatory compliance, increasing adoption rates.

Asia-Pacific ranks as the fastest-growing region, with strong demand from China, India, and Japan. High vehicle production and increasing safety awareness drive adoption. Over 50% of new vehicles in the region include advanced safety systems. Manufacturing hubs are expanding rapidly. A key regional player is investing heavily in smart safety technologies. Consumer behavior reflects growing preference for safety-enhanced vehicles.

South America holds around 6% market share, led by Brazil and Argentina. Infrastructure development and regulatory improvements are supporting adoption. Automotive production growth is increasing demand. Government incentives are encouraging safety compliance. Consumer awareness is gradually increasing, boosting adoption of smart safety systems.

Middle East & Africa accounts for approximately 4% share, driven by UAE and South Africa. Growth is supported by modernization in automotive infrastructure. Demand is rising in commercial and passenger vehicles. Technological adoption is improving, with increasing integration of safety systems. Consumer behavior shows gradual shift toward safety-conscious purchasing.

United States – 28% Market share: Strong automotive production capacity and high adoption of advanced safety technologies

Germany – 18% Market share: Robust automotive industry and strict regulatory safety standards

The Smart Safety Belt Systems for Automotive Market is moderately consolidated, with the top five companies accounting for approximately 55% of the total market share. The market includes over 25 active global and regional players competing on technology innovation, product quality, and strategic partnerships. Leading companies are focusing on R&D investments, with annual spending exceeding USD 500 million collectively to enhance safety system capabilities. Strategic initiatives such as mergers, acquisitions, and collaborations are common, enabling companies to expand their technological capabilities and geographic reach.

Product innovation is a key competitive factor, with companies introducing AI-enabled and sensor-integrated safety systems. The competitive landscape is also influenced by regulatory compliance requirements, pushing companies to continuously upgrade their offerings. Emerging players are entering the market with niche technologies, intensifying competition.

ZF Friedrichshafen AG

Joyson Safety Systems

Hyundai Mobis

Tokai Rika Co., Ltd.

Continental AG

Denso Corporation

AISIN Corporation

Bosch Mobility Solutions

Faurecia SE

Toyoda Gosei Co., Ltd.

Delphi Technologies

Hyundai Transys

Aptiv PLC

Technological advancements are transforming the Smart Safety Belt Systems for Automotive Market, with a strong focus on automation, connectivity, and predictive safety. AI-based occupant sensing systems are increasingly integrated, enabling real-time adjustments in belt tension based on passenger size, posture, and movement. These systems improve safety outcomes by up to 30%. Advanced sensor technologies embedded in belts can detect crash severity within milliseconds, ensuring rapid deployment of pretensioners.

Integration with ADAS and autonomous driving systems is a key trend, allowing seamless coordination between vehicle safety components. IoT-enabled monitoring systems are being adopted, enabling predictive maintenance and improving system reliability by approximately 25%. Lightweight materials such as high-strength polymers are reducing system weight by up to 20%, enhancing fuel efficiency and vehicle performance.

Another significant innovation is the development of inflatable seat belts, which distribute impact forces more evenly across the body, reducing injury risks. Digital twin technology is also being used to simulate crash scenarios, improving design accuracy and reducing development time by 15%. Cybersecurity measures are being enhanced to protect connected safety systems, addressing emerging risks associated with vehicle connectivity. These technological advancements are positioning smart safety belt systems as a critical component of next-generation automotive safety solutions.

• In March 2026, Autoliv Inc.announced a partnership with RS Taichi to advance motorcycle rider protection through airbag-integrated wearable systems, expanding its smart restraint portfolio beyond vehicles and reinforcing its strategy to enhance multi-modal safety ecosystems.

• In June 2025, Autoliv Inc.showcased its next-generation “belt-in-seat” and adaptive restraint concepts during its Capital Markets Day, focusing on integrated smart seatbelt architectures designed to improve crash protection and occupant comfort in next-generation vehicles. Source: www.autoliv.com

• In February 2026, Autoliv Inc.reported large-scale deployment of advanced seatbelt technologies including pretensioners and active belts, which can reduce serious injury risk in frontal crashes by up to 60%, highlighting continuous innovation in intelligent restraint systems.

• In 2025, Autoliv Inc.expanded the global deployment of AI-driven seatbelt quality systems such as “The Sound of Safety,” enabling automated defect detection in seatbelt retractors and improving manufacturing efficiency and product reliability across multiple facilities worldwide.

The Smart Safety Belt Systems for Automotive Market Report provides a comprehensive analysis of the global market, covering key segments such as product types, applications, and end-user industries. The report evaluates various system types including pretensioners, load limiters, inflatable belts, and active motorized systems, highlighting their adoption across passenger vehicles, commercial vehicles, and electric vehicles. It offers detailed regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, analyzing production capacity, consumption patterns, and technological advancements.

The report also examines key industry trends such as integration with ADAS, adoption of AI-enabled safety systems, and development of lightweight materials. It provides insights into regulatory frameworks influencing market growth, including safety mandates and environmental standards. Additionally, the report covers competitive landscape analysis, profiling major players and their strategic initiatives such as partnerships, product launches, and innovation efforts.

Emerging segments such as autonomous vehicle safety systems and predictive analytics are also explored, highlighting future growth opportunities. The scope includes analysis of consumer adoption trends, industry investments, and technological innovations shaping the market. This comprehensive coverage enables stakeholders to make informed decisions and develop effective strategies in the evolving automotive safety landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,000.0 Million |

| Market Revenue (2033) | USD 2,892.9 Million |

| CAGR (2026–2033) | 14.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Autoliv Inc.; ZF Friedrichshafen AG; Joyson Safety Systems; Hyundai Mobis; Tokai Rika Co., Ltd.; Continental AG; Denso Corporation; AISIN Corporation; Bosch Mobility Solutions; Faurecia SE; Toyoda Gosei Co., Ltd.; Delphi Technologies; Hyundai Transys; Aptiv PLC |

| Customization & Pricing | Available on Request (10% Customization Free) |