Reports

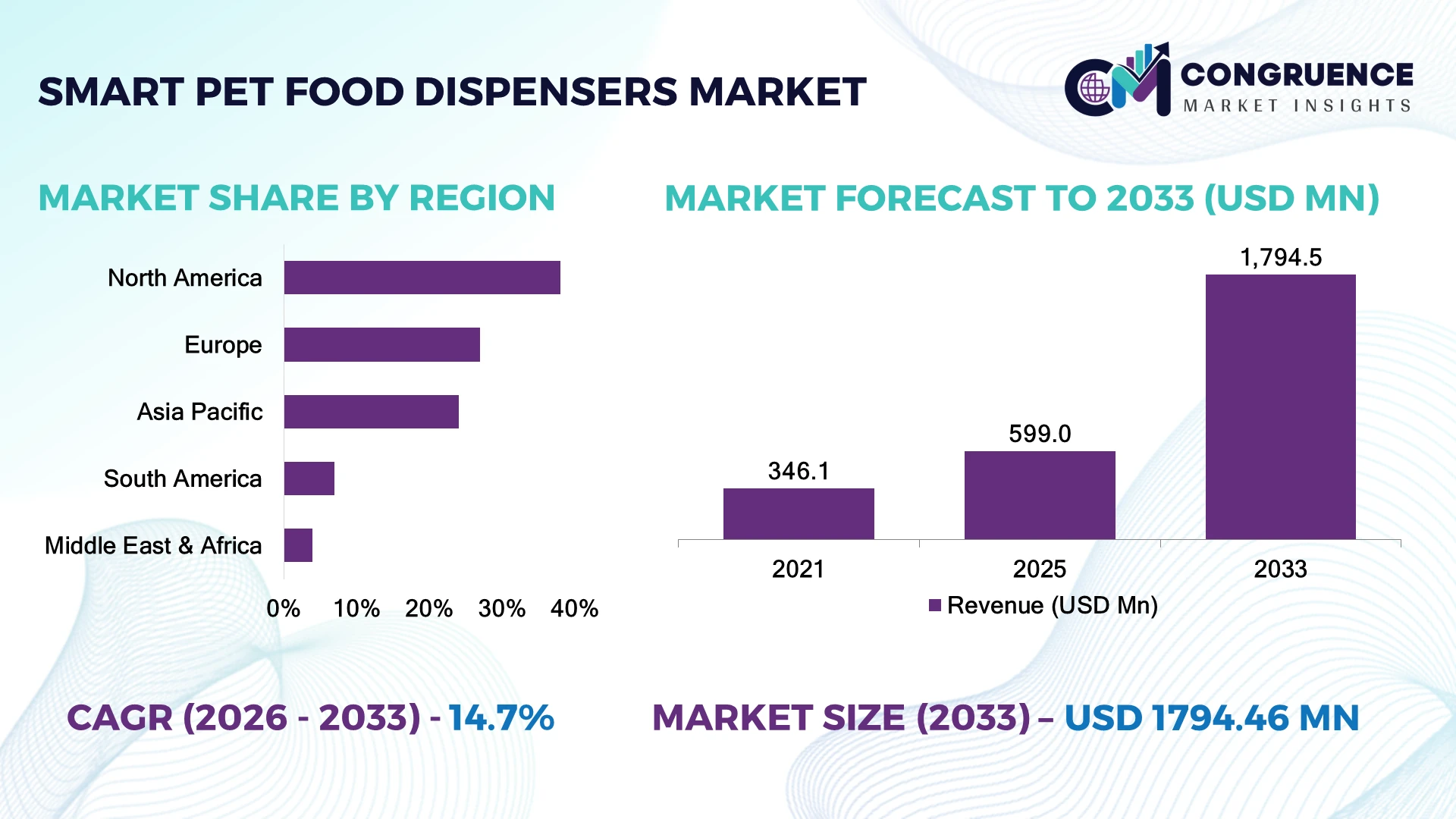

The Global Smart Pet Food Dispensers Market was valued at USD 599 Million in 2025 and is anticipated to reach a value of USD 1,794.5 Million by 2033 expanding at a CAGR of 14.7% between 2026 and 2033. Growth is driven by AI-enabled feeding schedules, IoT-based remote monitoring, portion-control automation, and rising adoption of connected pet-care ecosystems among urban pet owners.

The United States accounted for the largest market presence, supported by over 66 million dog-owning households and rapid smart home integration, while China is expanding through domestic IoT manufacturing and e-commerce pet technology platforms. North America represented nearly 40% of global adoption, compared with Asia-Pacific’s faster deployment growth supported by increasing premium pet-care spending and technology investments.

Strategic focus on connected product innovation and regional expansion will define competitive positioning.

Market Size & Growth: USD 599 Million in 2025 to USD 1,794.5 Million by 2033 at 14.7% CAGR, driven by AI-based pet monitoring and automated feeding solutions.

Top Growth Drivers: Smart home integration 35%, pet health tracking 28%, and online pet product adoption 25% are key growth contributors.

Short-Term Forecast: By 2028, automated feeding adoption is expected to increase 30%, improving scheduling accuracy and reducing manual feeding efforts.

Emerging Technologies: AI feeding algorithms, IoT connectivity, voice assistants, and camera-enabled dispensers are transforming premium pet-care solutions.

Regional Leaders: North America projected at USD 720 Million, Europe at USD 480 Million, and Asia-Pacific at USD 430 Million, supported by connected lifestyle adoption.

Consumer/End-User Trends: Over 45% of smart pet product users prioritize remote feeding control and personalized nutrition management.

Pilot/Case Example: In 2024, smart feeding trials using connected monitoring reduced irregular feeding events by 35% among participating households.

Competitive Landscape: Leading brands hold nearly 30% combined share, with key players including Petlibro, WOPET, PetSafe, Xiaomi, and Sure Petcare.

Regulatory & ESG Impact: Sustainable packaging initiatives and energy-efficient devices are reducing material waste by nearly 20% across newer product lines.

Investment & Funding: Over USD 200 Million invested in connected pet-care startups and partnerships, emphasizing AI, IoT, and global retail expansion.

Innovation & Future Outlook: Next-generation dispensers will integrate predictive nutrition, health analytics, and ecosystem-based pet wellness platforms.

Smart Pet Food Dispensers are becoming essential components of connected pet-care systems, supported by innovations in AI scheduling, camera monitoring, and app-controlled nutrition management. Around 50% of premium pet owners prioritize technology-enabled convenience, while supply-chain improvements in electronics manufacturing are accelerating product availability across global markets. The shift toward personalized pet wellness solutions is creating new opportunities for manufacturers and technology providers.

The Smart Pet Food Dispensers Market is becoming strategically important as pet-care companies transition from traditional feeding products toward connected wellness platforms. Rising urban pet ownership, digital adoption, and demand for personalized nutrition management are reshaping competition, encouraging brands to invest in AI, sensors, and cloud-based monitoring capabilities.

Supply-chain restructuring in consumer electronics and expanded smart-home infrastructure are improving accessibility of connected pet devices. Compared with conventional feeders, AI-enabled dispensers provide automated portion control, remote scheduling, and usage analytics, improving feeding accuracy by nearly 30% while reducing manual intervention.

North America leads through mature smart-home adoption and premium pet spending, while Asia-Pacific is gaining momentum through manufacturing advantages, e-commerce expansion, and increasing technology adoption among younger consumers. Over the next 2–3 years, companies are prioritizing app integration, subscription-based nutrition services, and partnerships with veterinary technology providers.

Manufacturers are expanding production capabilities and forming ecosystem partnerships to strengthen customer retention. Connected feeding platforms that combine convenience, health monitoring, and operational efficiency will create stronger competitive advantages and establish long-term relevance in the evolving pet-care industry.

Rising adoption of connected pet-care devices is the primary driver, supported by smart home integration, AI-based feeding systems, and remote monitoring capabilities. More than 45% of premium pet owners prioritize app-controlled feeding solutions, while nearly 35% of smart pet product buyers seek automated nutrition management features. In the United States, increasing demand for personalized pet wellness is encouraging companies to expand AI-enabled product portfolios and strengthen technology partnerships. Manufacturers are investing in cloud connectivity, camera-based monitoring, and predictive feeding algorithms to differentiate offerings. The strategic shift from standalone feeders to connected pet ecosystems is improving customer retention and creating recurring service opportunities.

Smart Pet Food Dispensers face scalability limitations due to electronic component costs, software complexity, and supply-chain dependency on sensors and connectivity modules. Imported semiconductor components account for a significant portion of device costs, with hardware expenses often representing over 40% of total manufacturing inputs. Supply disruptions in China’s electronics manufacturing ecosystem continue to pressure production planning and inventory management. Additionally, nearly 30% of consumers remain price-sensitive toward premium connected pet devices, limiting mass adoption in developing markets. Companies are addressing these challenges through supplier diversification, localized assembly strategies, and modular designs that reduce manufacturing complexity while improving profitability.

The integration of artificial intelligence, predictive analytics, and health monitoring features is creating new opportunities beyond basic automated feeding. More than 50% of technology-focused pet owners show interest in personalized feeding recommendations, while camera-enabled monitoring adoption is increasing across premium households. Companies in Japan and South Korea are developing advanced pet-care ecosystems combining nutrition tracking, behavioral insights, and smart-home connectivity. Partnerships between pet technology firms and veterinary platforms are opening new service models based on data-driven wellness management. The emerging opportunity lies in transforming dispensers into intelligent health-support platforms, enabling manufacturers to capture higher-value customers through subscription services and ecosystem-based offerings.

Long-term market expansion is challenged by cybersecurity risks, fragmented software ecosystems, and inconsistent connectivity standards across smart pet devices. Connected dispensers transmitting feeding schedules and usage data require stronger data protection frameworks, with over 60% of IoT users globally expressing concerns about device security. Compatibility issues between pet devices and smart-home platforms also affect user experience and product scalability. Companies must invest in secure cloud infrastructure, firmware upgrades, and cross-platform integration to maintain consumer trust. The key operational challenge is balancing advanced functionality with reliability, as device failures or connectivity interruptions directly impact customer satisfaction and brand competitiveness.

AI-Powered Feeding Personalization AI-based feeding systems are becoming a core product shift, with nearly 50% of premium pet owners showing interest in personalized nutrition recommendations and automated feeding adjustments. Companies are integrating machine learning, weight sensors, and behavioral tracking to improve feeding accuracy by approximately 30%. The transition toward data-driven pet wellness is encouraging manufacturers to expand connected platforms rather than focus only on hardware sales.

Smart Home Integration Expansion Connected pet devices are increasingly linking with smart home ecosystems, with around 40% of new premium dispensers featuring app controls, voice assistant compatibility, and remote monitoring functions. Companies are restructuring product development around IoT interoperability to improve user convenience. Rising cybersecurity requirements and evolving connected-device standards are pushing manufacturers to adopt stronger software frameworks and cloud-based management systems.

Premium Product Automation Shift High-income households are accelerating demand for automated pet-care solutions, with over 35% of buyers prioritizing cameras, portion control, and real-time alerts. Companies are responding through advanced materials, compact designs, and subscription-based service models. A non-obvious shift is the move toward preventive pet health monitoring, where feeding data supports broader wellness management.

Supply Chain Localization Strategies Electronics supply-chain pressure is driving manufacturers to diversify sourcing beyond traditional production hubs, with approximately 25% of companies increasing regional assembly capabilities. Businesses are adopting modular components and local partnerships to reduce inventory risks and improve delivery speed. The restructuring of global electronics supply networks is strengthening operational resilience for connected pet-care brands.

Automated smart feeders dominate the Smart Pet Food Dispensers Market, accounting for approximately 62% share due to their broad household adoption, affordable scalability, and compatibility with mobile applications. These devices provide scheduled feeding, portion control, and remote management, making them the preferred choice among urban pet owners in countries such as the United States, Japan, and Germany. Companies are prioritizing automated feeder innovation through improved battery efficiency, cloud connectivity, and AI-based scheduling features. Wi-Fi-enabled smart dispensers represent the fastest-growing type, supported by increasing demand for remote monitoring and integration with smart home ecosystems. Adoption of connected models is rising by nearly 20–25% annually among premium consumers, while traditional programmable feeders continue serving cost-sensitive users. Manufacturers are shifting investments toward camera-enabled, sensor-driven, and app-connected products to capture higher-value segments and strengthen ecosystem-based customer engagement.

Household pet care applications represent the leading segment, contributing nearly 75% market share as pet owners increasingly adopt automated feeding solutions for convenience, routine management, and personalized nutrition. Rising pet ownership in the United States and China is strengthening demand for compact, connected dispensers designed for apartments and urban lifestyles. Companies are expanding consumer-focused product lines with mobile applications, voice control, and health-monitoring features. Commercial pet facilities and veterinary applications are emerging as the fastest-growing use cases, supported by professional demand for accurate feeding schedules and operational efficiency. Adoption in commercial environments is increasing by around 25% as shelters, boarding facilities, and pet-care centers seek automation to reduce manual workload. Manufacturers are developing higher-capacity dispensers and multi-user management systems to address institutional requirements while maintaining reliability.

Residential pet owners account for approximately 80% of market demand, driven by increasing pet humanization, busy lifestyles, and preference for technology-enabled convenience. Consumers in the United States, Canada, and South Korea are adopting smart dispensers to manage feeding schedules remotely and maintain consistent pet routines. Companies are targeting this segment through affordable product variants, subscription services, and integrated mobile applications. Commercial pet-care providers represent the fastest-growing end-user group, expanding as boarding centers, shelters, and grooming businesses adopt automation to improve efficiency. Commercial adoption is increasing by nearly 30% as operators seek solutions that reduce labor dependency and improve feeding consistency. Manufacturers are developing enterprise-grade dispensers with larger storage capacity, centralized controls, and maintenance support programs to address institutional demand.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.2% between 2026 and 2033.

North America held the dominant position with a 38% market share in 2025, supported by strong smart-home penetration, high pet ownership rates, and widespread adoption of IoT-enabled consumer devices. The United States represents the largest deployment hub, with demand concentrated among urban households seeking automated feeding, remote monitoring, and personalized pet-care solutions. Over 40% of premium pet technology buyers prioritize app-connected devices, encouraging manufacturers to expand AI-based features and cloud-enabled platforms. Companies are increasing investments in software integration, retail partnerships, and direct-to-consumer channels to strengthen market reach and customer engagement.

United States Market Outlook: The United States remains the leading country market due to advanced consumer electronics infrastructure and strong pet-care spending. More than 65 million households own dogs, creating a large customer base for automated feeding technologies. Companies are focusing on AI-powered nutrition tracking, voice assistant compatibility, and connected wellness platforms to capture premium consumer demand.

Europe accounted for approximately 27% market share in 2025, supported by increasing adoption of connected home technologies, premium pet products, and sustainable consumer solutions. Countries including Germany, the United Kingdom, and France are leading deployments due to strong digital infrastructure and high pet ownership levels. European consumers are increasingly prioritizing energy-efficient devices and durable product designs, influencing manufacturers to improve material efficiency and lifecycle performance. Around 35% of smart pet product buyers in developed European markets prefer devices with remote monitoring features. Companies are responding through localized product development, retail collaborations, and improved data security capabilities aligned with evolving digital regulations.

Germany Market Outlook: Germany represents the strongest European market due to its advanced consumer technology sector and strong manufacturing ecosystem. The country’s focus on connected household solutions is supporting adoption of smart pet devices, with manufacturers expanding distribution networks and developing energy-efficient dispensers suited for environmentally conscious consumers.

Asia-Pacific represented nearly 24% market share in 2025 and is positioned as the fastest-expanding market due to manufacturing capabilities, rising disposable incomes, and rapid e-commerce adoption. China, Japan, and South Korea are major contributors, combining electronics expertise with growing demand for premium pet-care products. China serves as a major production center for smart pet devices, supporting global supply through established component and assembly networks. More than 30% of new pet technology launches in the region incorporate app connectivity and automation features. Companies are leveraging local manufacturing advantages, digital retail platforms, and technology partnerships to scale production and improve market accessibility.

China Market Outlook: China is the key Asia-Pacific market due to its electronics manufacturing strength and expanding domestic pet-care industry. The country supports large-scale production of smart devices through established supply chains, while companies are investing in AI integration, online distribution, and affordable connected products for urban consumers.

South America accounted for around 7% market share in 2025, with Brazil and Argentina representing the largest demand centers. Growth is supported by increasing urban pet ownership, expanding online retail channels, and rising awareness of automated pet-care solutions. Brazil has become the primary regional market due to its large pet population and growing premium pet product segment. However, pricing sensitivity and uneven technology infrastructure continue to influence adoption rates. Approximately 20% of consumers in major urban markets are adopting smart pet products, encouraging companies to introduce affordable models and flexible product offerings. Manufacturers are strengthening local distribution partnerships to improve accessibility and reduce supply-chain challenges.

Brazil Market Outlook: Brazil leads South America through its extensive pet ownership base and expanding digital commerce ecosystem. The country’s growing urban consumer segment is encouraging companies to introduce cost-effective smart dispensers with mobile connectivity and automated feeding features while building stronger retail partnerships.

Middle East & Africa accounted for approximately 4% market share in 2025, supported by premium household technology adoption, rising pet ownership among urban consumers, and expanding smart-home infrastructure in Gulf countries. The United Arab Emirates and Saudi Arabia are emerging as important markets due to higher technology spending and demand for luxury pet-care solutions. Smart dispenser adoption is concentrated in metropolitan areas where connected household devices are becoming more common. Around 15% of premium pet owners in major Gulf cities are shifting toward automated care solutions. Companies are targeting the region through distributor partnerships, localized product availability, and advanced connected features designed for high-income consumers.

United Arab Emirates Market Outlook: The United Arab Emirates represents the leading Middle East market due to strong smart-home adoption and technology-focused consumer behavior. Growing investment in connected residential infrastructure is supporting demand for automated pet-care products, while companies are expanding through premium retail channels and regional partnerships.

The Smart Pet Food Dispensers Market features global technology leaders such as Petlibro, PetSafe, Sure Petcare, and Petkit competing against regional OEMs and cost-focused manufacturers from China. Top five players collectively account for approximately 35% share, with competition centered on AI features, pricing, connectivity, and supply-chain efficiency. Premium brands differentiate through camera monitoring, health analytics, and ecosystem integration, while OEMs compete through lower manufacturing costs and customization. Around 40% of new product launches emphasize smart connectivity, and nearly 30% focus on personalized feeding solutions. Companies are expanding through retail partnerships, software upgrades, and vertical integration of hardware and applications. The competitive shift is moving toward intelligent pet wellness platforms rather than standalone feeders. High technology investment, brand trust, and software capability remain major entry barriers. Winning requires superior user experience, reliable hardware, and continuous innovation.

PetSafe

Sure Petcare

Petkit

Xiaomi

WOPET

Furbo

Cat Mate

DOGNESS

Arf Pets

HoneyGuaridan

Feed and Go

Faroro

iPettie

Smart Pet Food Dispensers are evolving through AI-based feeding algorithms, IoT connectivity, camera monitoring, and predictive pet wellness analytics. AI-enabled models improve feeding personalization by approximately 30% compared with traditional timers, while connected platforms enable remote scheduling and behavioral tracking. Companies are integrating sensors, cloud applications, and voice assistant compatibility to create broader pet-care ecosystems.

Advanced RFID identification and weight-monitoring technologies are improving multi-pet feeding accuracy, reducing food management errors by nearly 25%. Compared with conventional mechanical feeders, modern smart dispensers provide real-time usage visibility and automated adjustments, creating operational advantages for premium pet-care brands. Technology leaders benefit by combining hardware sales with digital service capabilities.

Between 2026 and 2028, disruptive innovations will focus on predictive nutrition, AI health insights, and ecosystem integration. Adoption of camera-enabled dispensers is increasing among technology-focused pet owners, encouraging companies to invest in software development, partnerships, and connected product portfolios. Competitive advantage will depend on reliable automation, secure data management, and personalized user experiences.

June 2026 Petlibro launched the Granary 2 smart feeder series featuring four new models with behavioral insights, personalized schedules, and health-focused tracking features. The company expanded its connected feeding portfolio to strengthen AI-based pet wellness positioning and improve premium customer engagement. Source: www.prnewswire.com

March 2026 Petlibro expanded smart pet technology distribution through PetSmart availability, increasing retail accessibility across nearly 400 stores. The move strengthened omnichannel expansion and supported broader adoption of AI-enabled pet-care products through physical retail and online channels. Source: www.prnewswire.com

2025 Petlibro advanced its smart pet-care ecosystem by introducing AI-driven monitoring technologies across its product portfolio. The company focused on integrating intelligent analysis features to improve customer interaction and reinforce its position in connected pet technology markets. Source: www.prnewswire.com

2024 PetSafe continued expanding automated feeding solutions through connected Smart Feed technology, supporting remote scheduling and portion management capabilities. The platform enables up to 12 scheduled meals daily and strengthens automated pet-care adoption among digitally connected households.

The Smart Pet Food Dispensers Market Report covers comprehensive analysis across product types, including automated feeders, Wi-Fi-enabled dispensers, camera-based models, and connected feeding systems. The study evaluates applications across household pet care, commercial facilities, shelters, and veterinary environments, along with end-user analysis covering residential and professional buyers.

The report examines regional markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting adoption patterns, manufacturing hubs, technology integration, and competitive strategies. It evaluates AI, IoT, automation, RFID, and cloud-based innovations shaping product development. The analysis supports investment planning, expansion strategies, partnership decisions, and competitive positioning by identifying emerging opportunities, operational challenges, and future technology pathways through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 599 Million |

| Market Revenue (2033) | USD 1,794.5 Million |

| CAGR (2026–2033) | 14.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Petlibro; PetSafe; Sure Petcare; Petkit; Xiaomi; WOPET; Furbo; Cat Mate; DOGNESS; Arf Pets; HoneyGuaridan; Feed and Go; Faroro; iPettie |

| Customization & Pricing | Available on Request (10% Customization Free) |