Reports

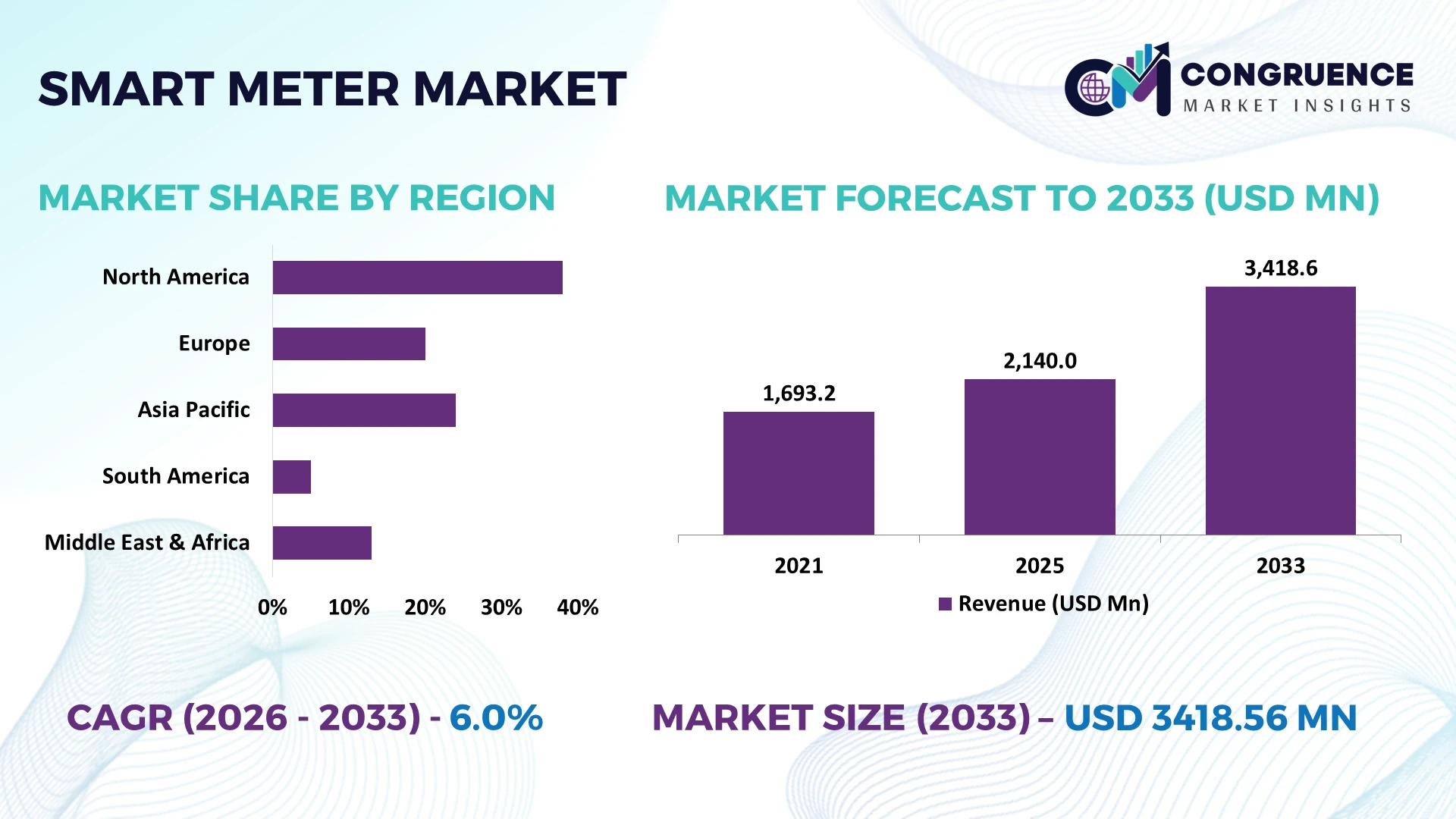

The Global Smart Meter Market was valued at USD 2140 Million in 2025 and is anticipated to reach a value of USD 3418.56 Million by 2033 expanding at a CAGR of 6.03% between 2026 and 2033. Grid digitalization, advanced metering infrastructure deployment, and large-scale utility modernization programs are accelerating smart meter installations while enabling real-time energy management and stronger grid resilience.

China remains the dominant market with approximately 38% of global smart meter manufacturing capacity, supported by sustained grid investments exceeding USD 70 billion and nationwide deployment across power utilities. In comparison, India is expanding faster through nationwide smart metering programs targeting over 250 million installations, while Europe strengthens adoption through energy security initiatives following the regional energy transition triggered by the Russia-Ukraine conflict, with advanced meter penetration exceeding 70% across several leading economies.

Utilities and technology providers should prioritize scalable manufacturing, secure communication platforms, and localized deployment strategies to strengthen long-term market positioning.

Market Size & Growth: USD 2140 million in 2025, reaching USD 3418.56 million by 2033 at 6.03% CAGR, driven by advanced grid modernization and intelligent metering infrastructure deployment.

Top Growth Drivers: Advanced metering infrastructure adoption (+31%), utility digitalization (+28%), and smart grid investments (+24%) continue expanding global implementation.

Short-Term Forecast: By 2028, remote meter reading reduces field service costs by nearly 30% while improving billing accuracy above 98%.

Emerging Technologies: AI-powered analytics, edge computing, and secure IoT communication enhance outage detection, demand forecasting, and grid optimization.

Regional Leaders: Asia-Pacific exceeds USD 1450 million through utility expansion, Europe approaches USD 870 million with energy-transition deployment, while North America surpasses USD 760 million through grid modernization.

Consumer & End-User Trends: More than 65% of connected households actively monitor electricity consumption through digital platforms, improving energy efficiency.

Pilot & Case Example: A 2026 utility deployment achieved approximately 22% faster outage restoration using advanced smart meter network analytics.

Competitive Landscape: Leading suppliers collectively account for roughly 42% market share, supported by Landis+Gyr, Itron, Siemens, Schneider Electric, and Honeywell.

Regulatory & ESG Impact: Digital metering programs improve billing transparency while supporting emissions management, reducing technical and commercial losses by nearly 18%.

Investment & Funding: More than USD 10 billion in utility modernization programs and strategic partnerships supports manufacturing expansion amid evolving regional supply chains.

Innovation & Future Outlook: Next-generation interoperable smart meters integrate AI, cybersecurity, and distributed energy management, strengthening utility resilience and grid flexibility.

Rising deployment across residential, commercial, and industrial electricity networks is increasing demand for interoperable smart meters capable of supporting distributed energy resources and real-time analytics. AI-enabled load forecasting and secure communication modules now improve operational visibility by nearly 25%, while localized manufacturing and evolving regulatory requirements are reshaping procurement strategies and strengthening regional supply-chain resilience, setting the stage for broader strategic market expansion.

Smart meters have become a strategic infrastructure asset as utilities shift from periodic billing to real-time grid intelligence and data-driven energy management. Competition increasingly centers on secure communication platforms, analytics capabilities, and interoperable metering ecosystems rather than hardware alone. Infrastructure modernization programs, stricter grid resilience requirements, and localized manufacturing strategies are reshaping procurement priorities, while digital utility transformation is accelerating investment decisions across electricity distribution networks.

Compared with conventional electromechanical meters, advanced smart meters reduce manual meter-reading costs by nearly 80% and improve outage identification by approximately 35% through continuous network monitoring and automated alerts. China leads large-scale deployment through integrated manufacturing and utility coordination, whereas Germany emphasizes secure communication standards and certified digital infrastructure, resulting in slower but highly standardized implementation. Over the next two to three years, utilities are expected to increase remote connection capabilities beyond 70% of new installations while expanding predictive maintenance across distribution assets.

A practical example is the integration of smart meters with distribution management systems, allowing utilities to isolate faults remotely and shorten restoration cycles while improving operational efficiency. Technology suppliers are expanding software partnerships, cybersecurity capabilities, and local manufacturing to strengthen delivery resilience. Organizations that combine interoperable platforms, secure data management, and scalable deployment models will secure stronger competitive positioning as digital electricity networks become an essential component of long-term energy infrastructure.

Large-scale utility modernization is accelerating smart meter deployment as electricity providers prioritize real-time monitoring, automated billing, and distribution network optimization. Utilities deploying advanced metering infrastructure report approximately 25% lower operational service costs and up to 30% faster outage response through remote diagnostics, while billing accuracy exceeds 98%. India's nationwide smart metering rollout continues to stimulate manufacturing and communication technology investments, encouraging suppliers to expand domestic production and software integration capabilities. Companies are strengthening partnerships with telecom providers, cloud platform developers, and grid automation specialists to deliver end-to-end digital metering ecosystems. The strategic outcome is stronger asset utilization, reduced field operations, and enhanced customer engagement through continuous energy visibility.

Fragmented communication protocols and aging distribution infrastructure continue limiting deployment efficiency across several utility networks. Integration costs can represent nearly 20% of total implementation expenditure, while interoperability issues delay deployment schedules by approximately 15% in multi-vendor environments. Several utilities operating legacy substations require additional investment before advanced metering infrastructure can function efficiently, increasing project complexity. To reduce operational risk, manufacturers are adopting open communication standards, expanding localized component sourcing, and signing long-term semiconductor supply agreements. Companies that prioritize standardized architectures and flexible system integration are better positioned to minimize deployment disruptions and improve implementation consistency across diverse electricity networks.

The convergence of artificial intelligence, distributed energy resources, and advanced analytics is creating high-value opportunities beyond conventional electricity metering. AI-assisted demand forecasting improves load prediction accuracy by nearly 20%, while intelligent voltage optimization reduces network losses by approximately 8%. Japan and India are accelerating investments in digital substations and distributed renewable integration, creating demand for interoperable smart metering platforms capable of supporting bidirectional energy flows. Technology providers are expanding R&D collaborations and software ecosystems to deliver predictive maintenance, dynamic pricing, and grid balancing solutions. Companies positioning around integrated digital energy platforms rather than standalone hardware are establishing stronger long-term competitive differentiation.

As millions of connected devices become part of critical electricity infrastructure, cybersecurity and system integration have emerged as long-term execution challenges. Smart utility networks generate over 90% more operational data than legacy systems, increasing security monitoring requirements and expanding the attack surface for connected assets. Utilities must also integrate metering platforms with billing, outage management, and distribution automation systems without compromising operational continuity. Companies are responding through zero-trust cybersecurity frameworks, encrypted communication protocols, and strategic partnerships with industrial cybersecurity specialists. Organizations that successfully secure interoperable, large-scale digital infrastructure will strengthen operational resilience, regulatory compliance, and long-term competitiveness in modern electricity networks.

AI-Powered Grid Intelligence Utilities are embedding AI-driven analytics into smart meter ecosystems to improve network visibility and operational efficiency. Fault detection accuracy has increased by nearly 30%, while remote diagnostics have reduced field inspections by approximately 25%. Digital grid modernization and stricter reliability requirements are accelerating software integration, prompting technology providers to expand cloud partnerships and intelligent asset management capabilities.

Localized Manufacturing Strategies Utilities and meter manufacturers are restructuring supply chains by expanding domestic production and regional component sourcing. Local procurement has increased by around 20%, while equipment lead times have fallen by nearly 18%. India and Southeast Asian manufacturing hubs are attracting new production investments, enabling companies to strengthen supply continuity, reduce logistics risks, and improve project execution speed.

Secure Interoperability Adoption Utilities are replacing proprietary communication architectures with standardized, interoperable smart metering platforms capable of supporting multi-vendor ecosystems. Device compatibility has improved by approximately 35%, while deployment complexity has declined by nearly 15%. Companies are investing in certified cybersecurity frameworks, firmware automation, and standardized communication protocols to simplify large-scale installations and reduce lifecycle integration costs.

Edge Computing Deployment Smart meters increasingly process operational data at the device level instead of relying solely on centralized systems. Edge-enabled deployments reduce communication latency by almost 40% and lower network bandwidth usage by roughly 22%. Utilities are integrating embedded analytics with automated demand-response programs, while technology suppliers continue expanding intelligent firmware capabilities and secure remote device management solutions.

Electricity Meters hold the largest market share at approximately 68% because they form the foundation of advanced metering infrastructure, enabling automated billing, outage detection, demand response, and renewable energy integration. Utilities continue prioritizing electricity meter replacement as digital grid modernization accelerates across developed and emerging economies. Water Meters maintain stable demand through municipal infrastructure upgrades and smart water management programs, where digital monitoring improves leak detection efficiency by nearly 20%. Manufacturers are expanding integrated product portfolios that support multiple communication standards and simplify deployment across utility networks.

Gas Meters represent the fastest-growing type, with deployments increasing by approximately 24% as gas utilities strengthen network monitoring, remote diagnostics, and safety compliance. Automated consumption monitoring reduces manual inspections by nearly 18%, lowering operational costs while improving service continuity. Companies are expanding localized production, investing in interoperable communication technologies, and forming strategic partnerships with utility operators. Investment priorities increasingly favor flexible platforms capable of supporting electricity, gas, and water metering through a unified digital infrastructure.

Utility Networks account for approximately 52% of total smart meter deployments, making them the largest application segment due to nationwide grid modernization initiatives, automated billing, and advanced distribution monitoring. Large utilities continue replacing legacy infrastructure with connected metering systems that improve outage management and operational transparency. Residential applications remain a major deployment area through smart home energy management, while Commercial applications expand steadily as enterprises prioritize energy monitoring, sustainability reporting, and operational efficiency.

Industrial applications are the fastest-growing segment, with deployments increasing by nearly 21% as manufacturers implement digital energy management and production optimization systems. Real-time consumption analytics improve operational efficiency by approximately 15% while supporting predictive maintenance initiatives. Technology providers are expanding industrial software integration, automation capabilities, and deployment partnerships to deliver sector-specific energy intelligence. Investment continues shifting toward intelligent analytics platforms that extend value beyond conventional meter functionality.

Utilities represent the largest end-user segment with an estimated 61% market share, driven by nationwide smart grid programs, distribution network modernization, and long-term infrastructure replacement strategies. Large deployment volumes and centralized procurement continue supporting sustained investment in secure communication platforms and advanced metering infrastructure. Residential Buildings maintain consistent demand through smart home integration, while Commercial Facilities increasingly adopt digital metering to improve building energy management and regulatory compliance.

Industrial Facilities are emerging as the fastest-growing end-user segment, with deployment increasing by approximately 22% as manufacturers prioritize energy optimization, predictive maintenance, and continuous operational monitoring. Advanced energy analytics improve facility efficiency by nearly 18% while reducing unnecessary consumption. Companies are responding by developing industry-specific software platforms, strengthening ecosystem partnerships, and offering customized digital energy management solutions. Competitive differentiation increasingly depends on integrated software services and long-term operational support rather than hardware supply alone.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, South America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Advanced Grid Modernization Drives Utility Transformation

North America remains a mature smart meter market, supported by extensive advanced metering infrastructure, utility digitalization, and strong cybersecurity investments. The region accounts for approximately 24% of global deployments, with utilities prioritizing real-time grid monitoring, outage automation, and demand-response capabilities. More than 80% of electricity customers in the United States already have access to advanced metering infrastructure, allowing utilities to optimize distribution efficiency and reduce manual operations. Utilities are increasingly integrating smart meters with distribution management platforms, while technology suppliers expand software capabilities and cloud-based grid intelligence solutions. Enterprise partnerships between utilities and communication technology providers continue strengthening interoperability and long-term operational resilience across electricity networks.

United States Market Outlook: The United States leads regional deployment through nationwide utility modernization, advanced communication infrastructure, and large-scale grid automation investments. More than 125 million advanced electricity meters are operational across utility networks, supporting automated billing, outage management, and renewable energy integration. Utilities continue replacing aging infrastructure while expanding AI-enabled grid analytics and cybersecurity capabilities, encouraging technology providers to strengthen domestic manufacturing, software development, and long-term utility partnerships.

Regulatory Digitalization Strengthens Grid Efficiency

Europe continues advancing smart meter deployment through energy transition policies, standardized communication frameworks, and digital electricity infrastructure modernization. The region represents approximately 22% of global market activity, with utilities emphasizing interoperability, secure data exchange, and renewable energy integration. Several countries have exceeded 70% smart electricity meter penetration, enabling improved demand management and enhanced distribution visibility. Utilities are accelerating replacement of legacy systems while technology suppliers expand secure communication platforms and firmware management capabilities. Regulatory alignment across electricity markets continues supporting standardized deployment and long-term operational consistency.

Germany Market Outlook: Germany is strengthening its smart meter ecosystem through certified communication gateways, strict cybersecurity standards, and nationwide digital grid modernization. Utility operators continue expanding intelligent metering infrastructure across residential and industrial users, while regulatory reforms accelerate secure digital deployments. Advanced smart meter installations continue increasing as energy transition objectives encourage greater operational visibility, distributed energy integration, and standardized interoperability throughout electricity distribution networks.

Large-Scale Manufacturing Powers Deployment

Asia-Pacific dominates the global smart meter market through extensive manufacturing capacity, rapid utility modernization, and nationwide deployment programs. The region contributes approximately 46.8% of global demand, supported by integrated supply chains and strong domestic production capabilities. China and India continue expanding advanced metering programs, while regional manufacturers strengthen export competitiveness through localized component production. Utility modernization projects targeting millions of new installations annually continue driving communication technology innovation, production expansion, and digital infrastructure development. Companies are increasing automation across manufacturing facilities while expanding strategic partnerships with utility operators to improve deployment efficiency and supply reliability.

China Market Outlook: China remains the largest national market through unmatched manufacturing capacity, vertically integrated supply chains, and extensive utility deployment programs. The country accounts for nearly 38% of global smart meter production capacity while continuing large-scale grid modernization initiatives. Domestic manufacturers invest heavily in communication technologies, AI-enabled meter platforms, and export-oriented production, reinforcing China's leadership across both manufacturing and advanced utility infrastructure deployment.

Utility Modernization Accelerates Adoption

South America is expanding smart meter deployment through electricity distribution upgrades, loss reduction initiatives, and digital utility transformation. The region represents approximately 5% of global deployments, with utilities prioritizing automated billing, remote monitoring, and operational efficiency improvements. Smart metering projects have reduced non-technical electricity losses by nearly 15% in several utility programs while improving billing transparency. Infrastructure limitations remain across selected markets, encouraging phased deployment strategies and greater collaboration between utilities and technology suppliers. Companies continue strengthening local partnerships and deployment services to improve project execution and operational reliability.

Brazil Market Outlook: Brazil leads regional deployment through extensive electricity distribution networks, regulatory modernization, and large utility investment programs. Electricity distributors continue expanding advanced metering infrastructure to improve network visibility and reduce commercial losses. Digital utility transformation, combined with increasing renewable energy integration, is encouraging technology providers to establish stronger local partnerships, expand deployment capabilities, and customize smart metering solutions for large-scale electricity distribution systems.

Infrastructure Investment Supports Digital Utilities

The Middle East & Africa market is progressing through utility modernization, smart city development, and national electricity infrastructure investment programs. The region contributes approximately 2.8% of global market activity, with governments prioritizing digital electricity management and operational efficiency. Large utility projects increasingly integrate smart metering with automated grid monitoring, while deployment programs improve consumption transparency and reduce distribution inefficiencies. Technology suppliers continue expanding regional partnerships and localized technical support to strengthen implementation quality and long-term system performance across diverse operating environments.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through extensive smart city investments, electricity infrastructure modernization, and digital utility transformation initiatives. National utility operators continue deploying advanced metering infrastructure to improve energy management and support grid automation objectives. Large-scale infrastructure projects and expanding renewable energy integration are encouraging international technology providers to strengthen partnerships, local engineering capabilities, and long-term deployment support across the Kingdom.

The Smart Meter Market is led by Landis+Gyr, Itron, Siemens, Schneider Electric, and Honeywell, competing directly with regional manufacturers and specialized metering suppliers across utility modernization projects. The top five companies collectively control approximately 44% of the global market, while regional suppliers compete aggressively through localized production, faster delivery, and lower implementation costs. Global leaders differentiate through secure communication platforms, advanced analytics, and interoperable software, achieving deployment efficiencies nearly 25% higher than legacy solutions. Regional competitors frequently reduce implementation costs by 10–15% through localized sourcing and customized utility services. Competition increasingly centers on integrated platforms rather than standalone hardware, prompting strategic partnerships, software acquisitions, and vertical integration across communication modules and digital services. Growing demand for cybersecurity-certified products and standardized interoperability is accelerating consolidation while raising certification and infrastructure compliance requirements for new entrants. Companies capable of combining secure digital platforms, scalable manufacturing, localized support, and continuous software innovation will consistently outperform rivals in utility procurement and long-term infrastructure contracts.

Landis+Gyr

Itron

Siemens

Schneider Electric

Honeywell

Kamstrup

Sensus

Aclara Technologies

Iskraemeco

EDMI Limited

Wasion Holdings

Holley Technology

CyanConnode

Apator SA

Advanced metering infrastructure remains the technological foundation of the Smart Meter Market, but value creation is shifting toward AI-driven analytics, edge computing, and secure IoT connectivity. AI-based load forecasting improves demand prediction accuracy by nearly 20%, while edge processing reduces communication latency by approximately 40% by analyzing operational data directly within the device. More than 70% of newly deployed smart meters now support two-way communication, enabling utilities to automate billing, outage detection, and remote service management. Utilities adopting integrated digital platforms gain stronger operational visibility and lower field service requirements, creating a clear competitive advantage over organizations relying on isolated metering systems.

Compared with conventional electromechanical meters, modern smart meters reduce manual operating costs by almost 80% while improving outage identification by roughly 35%. Interoperable communication standards, digital twins, and cloud-native meter management platforms are replacing proprietary architectures, allowing utilities to integrate renewable energy resources and distributed assets more efficiently. Global technology leaders benefit from faster deployment and stronger software differentiation, while regional manufacturers increasingly compete through localized firmware development and customized communication modules.

Between 2026 and 2028, cybersecurity-enhanced metering, embedded edge AI, and digital grid orchestration will define competitive leadership. Zero-trust device security, predictive asset diagnostics, and interoperable firmware management are expected to become standard procurement requirements. Companies investing now in software ecosystems, secure communication technologies, and intelligent grid automation will strengthen long-term utility partnerships, reduce operational complexity, and establish sustainable differentiation in increasingly digital electricity infrastructure.

April 2025 Landis+Gyr secured a five-year agreement to supply smart meters for Enea Operator in Poland, supporting one of the country's largest rollout programs. The deployment targets more than 2 million smart meters, strengthening long-term utility modernization and reinforcing Landis+Gyr's European market position.

May 2025 Honeywell introduced an AI-enabled Battery Energy Storage System platform that integrates with advanced utility infrastructure, improving energy optimization by up to 20%. The innovation strengthens grid flexibility and expands digital energy management capabilities for smart utility ecosystems.

January 2026 Mitsubishi Electric joined Landis+Gyr's Application Ecosystem to accelerate grid-edge innovation, combining advanced automation with intelligent metering platforms. The collaboration enhances interoperability across utility networks and supports faster deployment of next-generation digital grid applications. Source: (https://www.landisgyr.com)

April 2026 Landis+Gyr joined the Electric Power Research Institute's Open Power AI Consortium to accelerate AI adoption across electricity networks. The initiative promotes collaborative development of AI applications to improve grid reliability, resilience, and operational efficiency for modern utility infrastructure. Source: (https://www.epri.com)

This report delivers a comprehensive assessment of the Smart Meter Market by examining technology evolution, deployment strategies, competitive positioning, and operational developments influencing industry performance between 2026 and 2033. The analysis covers Electricity Meters, Gas Meters, and Water Meters across Residential, Commercial, Industrial, and Utility Network applications while evaluating demand from Utilities, Residential Buildings, Commercial Facilities, and Industrial Facilities. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, infrastructure modernization, and enterprise adoption patterns.

The study evaluates AI-enabled analytics, advanced metering infrastructure, edge computing, secure communication technologies, and interoperability trends shaping digital utility transformation. It benchmarks leading manufacturers and technology providers, assesses deployment strategies across major economies, and identifies emerging opportunities in smart grid modernization, distributed energy integration, and intelligent utility management. The report supports investment prioritization, expansion planning, competitive benchmarking, product development, and long-term strategic decision-making through detailed operational, technological, and market intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2140 Million |

Market Revenue in 2033 | USD 3418.56 Million |

CAGR (2026 - 2033) | 6.03% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Landis+Gyr, Itron, Siemens, Schneider Electric, Honeywell, Kamstrup, Sensus, Aclara Technologies, Iskraemeco, EDMI Limited, Wasion Holdings, Holley Technology, CyanConnode, Apator SA |

Customization & Pricing | Available on Request (10% Customization is Free) |