Reports

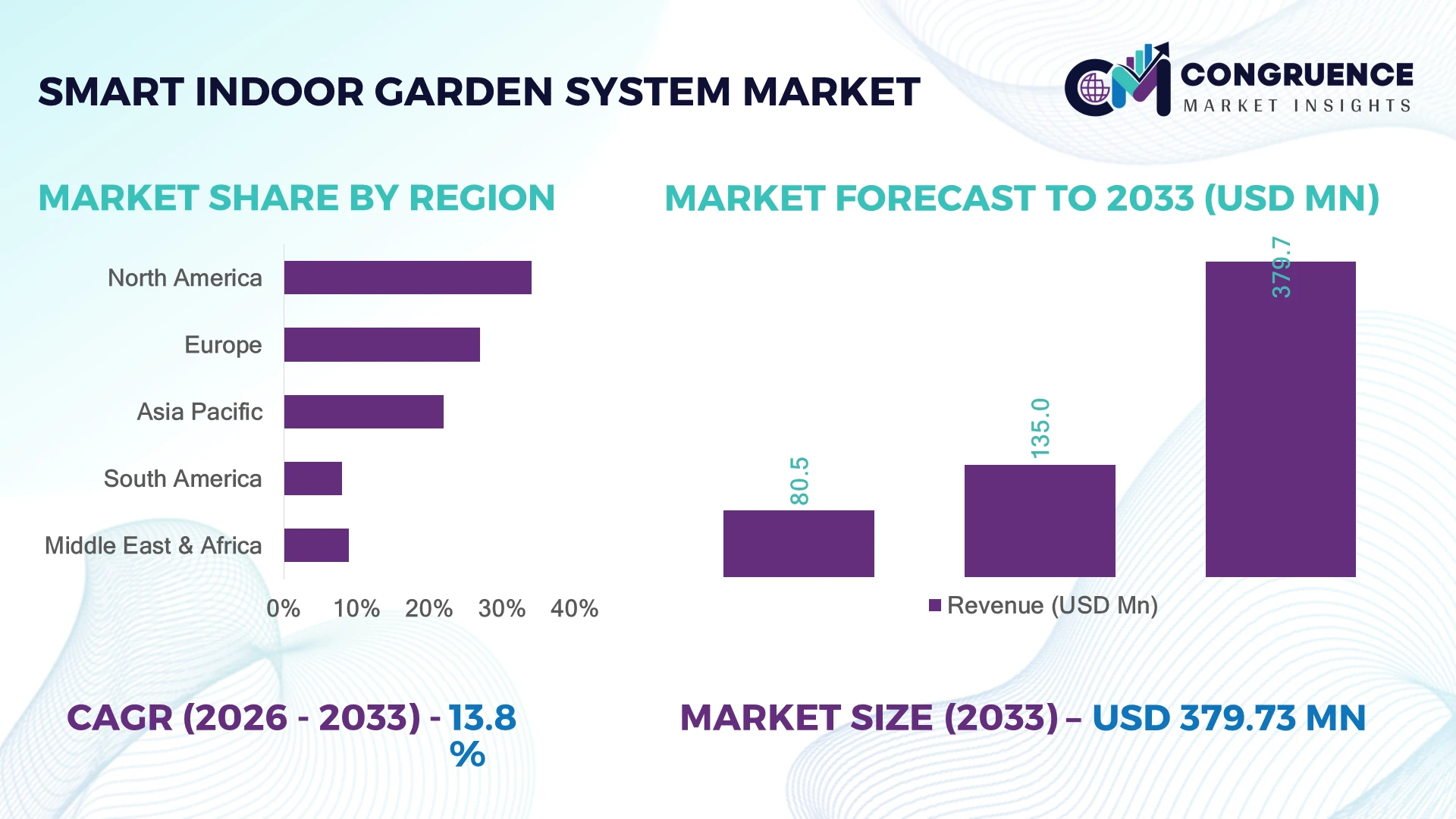

The Global Smart Indoor Garden System Market was valued at USD 135.0 Million in 2025 and is anticipated to reach a value of USD 379.7 Million by 2033 expanding at a CAGR of 13.8% between 2026 and 2033. Rapid adoption of AI-enabled hydroponic cultivation, rising urban food security initiatives, and expanding smart home ecosystems are accelerating commercial and residential deployment of connected indoor gardening systems.

The United States dominates the global Smart Indoor Garden System Market with approximately 34% market share, supported by strong consumer adoption, smart home integration, and over 1,200 controlled-environment agriculture facilities. Federal support for urban agriculture and resilient food systems has strengthened deployment, while Germany leads European automation standards through energy-efficient indoor cultivation technologies, highlighting North America's stronger consumer ecosystem and Europe's sustainability-focused innovation.

This leadership reinforces the importance of investing in intelligent cultivation technologies, regional manufacturing capabilities, and integrated digital ecosystems to strengthen long-term competitive positioning.

Market Size & Growth: USD 135.0 Million in 2025, reaching USD 379.7 Million by 2033 at 13.8% CAGR, driven by AI-powered hydroponics and connected home automation.

Top Growth Drivers: Smart home adoption +28%, hydroponic farming expansion +24%, urban food cultivation initiatives +19%.

Short-Term Forecast: By 2028, automated nutrient management improves water efficiency by 35% while reducing maintenance time by 25%.

Emerging Technologies: AI crop monitoring, IoT environmental sensors, and adaptive LED lighting deliver over 20% higher cultivation precision.

Regional Leaders: North America USD 145 Million, Europe USD 104 Million, Asia-Pacific USD 88 Million, driven by premium consumer adoption, sustainability programs, and urban farming expansion.

Consumer/End-User Trends: Nearly 46% of premium smart-home buyers prefer connected indoor gardening solutions with mobile monitoring features.

Pilot/Case Example: In 2024, automated vertical garden installations improved leafy vegetable yields by 30% while lowering water consumption by 40%.

Competitive Landscape: AeroGarden holds roughly 18% market share alongside Click and Grow, Gardyn, Rise Gardens, and LG Electronics.

Regulatory & ESG Impact: Water-efficient cultivation reduces consumption by up to 90%, supporting urban sustainability and climate-resilience initiatives.

Investment & Funding: More than USD 400 Million has been directed toward controlled-environment agriculture partnerships, automation, and product expansion.

Innovation & Future Outlook: Advanced AI cultivation assistants, modular vertical systems, and predictive plant analytics are redefining premium indoor food production worldwide.

Smart Indoor Garden System Market demand continues expanding across residential smart homes, hospitality, educational facilities, and compact commercial farming applications. AI-driven plant monitoring, adaptive LED lighting, and automated nutrient dosing are improving cultivation precision, while nearly 40% of new premium systems now integrate mobile application control. Ongoing localization of component sourcing and controlled-environment agriculture initiatives are strengthening supply resilience, setting the stage for broader strategic adoption.

Smart indoor garden systems are becoming a strategic investment area as urban agriculture, connected living, and sustainable food production converge into a single technology ecosystem. Companies are strengthening product portfolios through AI-enabled automation, subscription-based plant care services, and ecosystem partnerships. Supply-chain diversification and localized electronics manufacturing are also reducing component dependency while improving product availability across major consumer markets.

Compared with conventional indoor planters, intelligent hydroponic systems reduce water consumption by nearly 90% and lower routine maintenance requirements by approximately 35% through automated irrigation, lighting, and nutrient optimization. North America maintains leadership through advanced consumer technology adoption and established smart-home ecosystems, while Asia-Pacific is expanding deployment through urban residential developments and high-density living environments. Over the next two to three years, connected platform integration is expected to become standard across more than 50% of newly launched premium systems.

Manufacturers are deploying modular cultivation platforms for apartments, offices, and hospitality spaces while expanding collaborations with smart appliance providers and controlled-environment agriculture specialists. These strategies improve operational scalability, strengthen product differentiation, and support sustainable resource utilization. Organizations that prioritize intelligent automation, software integration, and localized manufacturing capabilities will secure stronger competitive positioning as connected indoor cultivation becomes a mainstream lifestyle and food-production solution.

Growing adoption of AI-powered hydroponics, IoT sensors, and automated nutrient systems is accelerating Smart Indoor Garden System deployment across residential and commercial applications. In the United States, smart gardening platforms are gaining traction as over 45% of premium connected-home consumers prioritize automated food cultivation solutions, while advanced systems improve water efficiency by up to 90% compared with traditional gardening. The expansion of controlled-environment agriculture investments and supply-chain resilience programs is encouraging companies to enhance product intelligence, develop subscription-based plant care services, and establish partnerships with smart-home technology providers. Strategic differentiation is increasingly shifting from hardware availability toward software-driven cultivation performance and user experience.

High upfront equipment costs, dependency on specialized electronic components, and limited consumer awareness restrict broader Smart Indoor Garden System adoption. Premium systems incorporating automated lighting, sensors, and AI controls often cost 30–50% more than conventional indoor gardening solutions, affecting price-sensitive markets such as India and Southeast Asian countries. Semiconductor supply fluctuations and imported LED component dependencies create additional cost pressures, with some manufacturers experiencing 15–20% increases in input expenses during supply disruptions. Companies are addressing these limitations through localized manufacturing, supplier diversification, modular product designs, and long-term procurement agreements to improve cost stability and increase accessibility across emerging markets.

The integration of AI analytics, robotics, and cloud-based cultivation platforms creates significant opportunities for next-generation Smart Indoor Garden System solutions. Japan and Singapore are expanding urban agriculture initiatives, with controlled-environment projects targeting 40%+ reductions in water usage and improved food production efficiency within dense urban settings. Growth opportunities are emerging through hospitality, educational institutions, and corporate wellness programs seeking sustainable food solutions. Companies are investing in ecosystem partnerships, predictive plant monitoring technologies, and connected appliance integration to capture new demand segments. A key strategic opportunity lies in transforming indoor gardens from standalone devices into intelligent food-production platforms connected with broader smart-home and sustainability networks.

Long-term market expansion faces execution challenges related to system interoperability, cybersecurity protection, and consistent crop performance across different environments. Approximately 35% of smart agriculture operators identify software integration and data management as major deployment concerns, while nearly 25% of users require improved technical support for automated cultivation systems. Differences in climate conditions, indoor infrastructure, and consumer operating skills create variability in system effectiveness. Companies must strengthen cloud security frameworks, improve AI training models, and develop standardized hardware ecosystems to ensure reliable performance. Competitive advantage will depend on solving operational complexity while maintaining affordable, scalable, and user-friendly indoor cultivation solutions.

AI Precision Cultivation Shift AI-powered monitoring platforms are transforming indoor gardening workflows, with automated systems improving plant-care accuracy by 30–40% through real-time climate, nutrient, and lighting adjustments. Adoption of IoT-enabled cultivation units has increased as urban households and commercial growers prioritize lower maintenance operations. Companies are responding by integrating machine learning algorithms, mobile applications, and predictive analytics to improve user retention and differentiate premium smart garden products.

Modular Garden Expansion Models Compact modular indoor gardens are gaining traction as apartment-based cultivation expands, with space-efficient systems supporting 25–35% higher utilization of small urban areas. In Japan and Singapore, high-density housing trends and urban food initiatives are accelerating demand for scalable cultivation units. Manufacturers are shifting toward customizable designs, subscription-based seed systems, and interchangeable components to reduce installation barriers and improve recurring customer engagement.

Energy-Efficient Hardware Integration Advanced LED lighting, low-power sensors, and automated irrigation technologies are reshaping operating efficiency, reducing electricity consumption by approximately 20–35% compared with older indoor cultivation setups. Rising energy costs and sustainability requirements are encouraging companies to redesign hardware architectures and optimize resource usage. Non-obvious market movement is the growing focus on energy intelligence, where systems adjust cultivation cycles based on environmental conditions and power availability.

Connected Food Ecosystem Development Smart indoor gardens are increasingly becoming part of broader connected-home and sustainable living ecosystems, with nearly 40% of new premium devices incorporating app-based controls, cloud monitoring, or smart assistant compatibility. Supply-chain localization and stronger demand for home-based food resilience after global disruptions are influencing product strategies. Companies are expanding partnerships with appliance manufacturers, technology providers, and urban agriculture networks to create integrated cultivation ecosystems.

Automated hydroponic systems represent the leading type segment due to their scalability, precise nutrient management, and integration with smart sensors and AI-based monitoring platforms. These systems account for approximately 45% of market adoption, supported by higher productivity, reduced water consumption, and suitability for residential as well as commercial applications. Soil-based smart gardens remain relevant for beginner users because of simpler operation, while aeroponic and aquaponic systems are gaining attention due to resource efficiency and advanced cultivation capabilities. The fastest-growing segment is aeroponic smart garden systems, expanding as users seek higher efficiency and reduced resource dependency. Adoption is being supported by improved misting technology, automated root-zone management, and increasing interest from urban farming operators. Companies are investing in modular designs, sensor-based optimization, and hybrid cultivation platforms to capture premium customers. The competitive focus is shifting toward systems that combine automation, sustainability, and data-driven plant performance rather than basic gardening functionality.

Residential applications dominate the Smart Indoor Garden System Market as consumers increasingly adopt compact cultivation solutions for herbs, vegetables, and ornamental plants within apartments and connected homes. This segment represents nearly 60% of deployments, supported by rising smart-home integration and demand for convenient food-growing solutions. Commercial indoor farming applications are expanding rapidly as restaurants, retailers, and small-scale growers use smart systems to improve freshness, reduce supply dependency, and maintain consistent crop quality. The fastest-growing application is commercial and institutional cultivation, driven by restaurants, hospitality operators, educational facilities, and corporate wellness programs. These users are adopting automated systems to reduce operational labor requirements by approximately 25% and improve resource monitoring. Companies are responding through enterprise-grade platforms, remote management capabilities, and customized installation models. The application landscape is shifting from individual consumer gardening toward integrated food-production solutions with measurable operational benefits.

Household consumers remain the dominant end-user group due to growing interest in self-sufficient food production, smart-home technology, and compact gardening solutions. Residential buyers contribute approximately 65% of adoption, particularly in countries such as the United States, Japan, and Germany where connected lifestyle products have strong penetration. Commercial growers, restaurants, and hospitality operators are emerging as important users as they seek consistent supply, reduced waste, and localized production capabilities. The fastest-growing end-user segment is commercial establishments, including restaurants, hotels, and workplace facilities, where demand is increasing through sustainability initiatives and customer preference for locally grown produce. Adoption among commercial users is rising by around 20–30% as automated systems improve workflow efficiency and reduce manual intervention. Companies are targeting these segments through customized solutions, leasing models, service partnerships, and scalable cultivation platforms. Future competition will depend on balancing consumer simplicity with enterprise-level performance requirements.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of15.2% between 2026 and 2033.

North America maintains market leadership due to strong smart-home adoption, advanced consumer technology infrastructure, and increasing interest in localized food production. The region contributes approximately 34% of global adoption, supported by high penetration of connected devices and controlled-environment agriculture investments. The United States represents the largest deployment hub, with residential smart gardening systems increasingly integrated into IoT ecosystems. More than 45% of premium indoor gardening users prioritize automated monitoring features, encouraging companies to expand AI-powered platforms, subscription services, and connected cultivation solutions. Strategic partnerships between technology providers and agriculture startups are accelerating product innovation and commercial adoption.

United States Market Outlook: The United States leads North America's Smart Indoor Garden System Market through strong consumer spending, technology adoption, and controlled-environment agriculture development. Over 1,200 indoor farming and cultivation facilities operate across the country, supporting demand for automation, energy-efficient lighting, and digital crop management platforms. Companies are focusing on premium residential systems, commercial deployments, and software-enabled gardening ecosystems to strengthen market positioning.

Europe is expanding its position through sustainability-focused agriculture policies, energy-efficient cultivation practices, and increasing urban food initiatives. The region represents nearly 27% of market adoption, driven by demand for water-saving technologies and environmentally responsible food production. Countries including Germany, the Netherlands, and the United Kingdom are integrating smart cultivation systems into urban farming projects and commercial facilities. More than 40% of European indoor cultivation projects emphasize resource optimization through automated irrigation and lighting controls. Companies are responding by developing low-energy systems, recyclable components, and partnerships with urban agriculture networks to align with sustainability objectives and changing consumer preferences.

Germany Market Outlook: Germany remains a key European market due to advanced automation capabilities, sustainability regulations, and strong engineering expertise. The country’s indoor agriculture sector benefits from industrial automation infrastructure and growing investment in climate-controlled farming solutions. More than 30% of commercial cultivation technology deployments in Germany incorporate digital monitoring capabilities, creating opportunities for smart garden manufacturers focused on precision agriculture and energy efficiency.

Asia-Pacific is emerging as the fastest-growing market due to dense urban populations, rising technology adoption, and strong electronics manufacturing capabilities. The region contributes approximately 22% of current deployments but demonstrates significant expansion potential through smart-city programs and compact agriculture solutions. Japan, China, South Korea, and Singapore are accelerating adoption through urban farming initiatives and advanced automation ecosystems. Nearly 50% of new indoor cultivation projects in major Asian cities prioritize automated environmental control systems. Companies are leveraging regional manufacturing advantages, expanding local production networks, and developing affordable modular systems to address residential and commercial demand.

Japan Market Outlook: Japan represents a strategic growth center due to limited agricultural land availability, aging farming workforce challenges, and strong robotics expertise. The country has adopted advanced indoor cultivation technologies across urban facilities, with more than 35% of smart farming projects incorporating automation and sensor-based management. Japanese companies are investing in compact, energy-efficient systems designed for apartments, restaurants, and commercial food production environments.

South America is gradually adopting Smart Indoor Garden Systems as urban consumers and businesses seek reliable food cultivation alternatives. The region accounts for approximately 8% of global adoption, with Brazil and Argentina representing key demand centers. Limited urban farming infrastructure and higher equipment costs remain challenges, but increasing interest in sustainable agriculture is supporting deployment. More than 25% of emerging indoor cultivation projects focus on reducing water dependency and improving local food availability. Companies are addressing market barriers through affordable modular designs, local partnerships, and simplified automation technologies tailored to regional operating conditions.

Brazil Market Outlook: Brazil is the leading South American market due to its large urban population, agricultural expertise, and growing interest in technology-enabled farming. Urban agriculture initiatives are expanding in major cities, with approximately 20% of new cultivation projects incorporating digital monitoring solutions. Companies are targeting restaurants, residential users, and educational institutions through compact systems designed for tropical climate conditions and efficient resource management.

The Middle East & Africa market is developing through investments in water-efficient agriculture, food security programs, and advanced cultivation infrastructure. The region represents nearly 9% of global adoption, with demand concentrated in countries facing water scarcity and limited arable land availability. The United Arab Emirates and Saudi Arabia are increasing investment in controlled-environment agriculture projects, with some facilities achieving 80–90% water savings compared with traditional farming. Companies are expanding through government partnerships, technology collaborations, and climate-adaptive cultivation solutions to support local food production strategies.

United Arab Emirates Market Outlook: The United Arab Emirates is a leading market due to strong food security initiatives, advanced infrastructure development, and investment in vertical farming technologies. Government-supported agriculture innovation programs are encouraging deployment of automated cultivation systems, with commercial facilities increasingly adopting AI-based monitoring and efficient irrigation solutions. Companies are positioning the UAE as a regional hub for desert agriculture technology and smart cultivation experimentation.

The Smart Indoor Garden System Market features competition between global smart-home leaders, specialized hydroponics brands, and emerging agriculture technology providers. Companies such as LG Electronics, Click & Grow, Gardyn, and Rise Gardens compete through automation, ecosystem integration, and premium consumer experiences, while regional manufacturers compete on affordability and customization. The top five players collectively account for approximately 45% of the market, reflecting moderate consolidation. Competition is driven by AI capabilities (35% of premium product differentiation), energy efficiency (25% of purchasing decisions), and supply-chain reliability. Leading companies are expanding through smart-home partnerships, modular product launches, and vertically integrated seed-to-software ecosystems. The competitive landscape is shifting toward software-enabled cultivation platforms rather than standalone hardware. Entry barriers include proprietary technology, customer ecosystems, and supply relationships. Winning players will combine affordable automation, reliable performance, and scalable digital cultivation services.

Click & Grow

Gardyn

Rise Gardens

AeroGarden

iDOO

LetPot

VegeBox

Back to the Roots

Smart Garden Products

Plantui

Veritable

Artificial intelligence, IoT sensors, and automated cultivation platforms are becoming core technologies in smart indoor gardening. AI-based plant monitoring improves disease detection and growth optimization by approximately 25–40%, while IoT-enabled systems provide real-time control of humidity, lighting, and nutrients. Adoption is increasing among premium residential users and commercial growers seeking predictable crop performance and reduced manual intervention.

Advanced LED lighting, automated irrigation, and cloud-based analytics are replacing traditional indoor growing methods. Compared with conventional timer-based systems, intelligent lighting platforms improve energy efficiency by nearly 30% through adaptive cycles. Companies benefiting most are those combining hardware, software, and consumable ecosystems, creating recurring engagement beyond initial device sales.

Between 2026 and 2028, disruptive technologies such as computer vision, predictive crop algorithms, and connected smart-home integration will reshape competitive positioning. Modular robotic cultivation and AI assistants are expected to improve operational efficiency by 20–35%, enabling broader commercial adoption. Companies investing in data-driven cultivation platforms, cybersecurity, and ecosystem partnerships will gain stronger advantages as indoor gardening evolves into a connected agricultural technology segment.

January 2025 LG Electronics introduced new indoor gardening concepts at CES 2025, expanding its smart cultivation portfolio with design-focused systems integrated into connected living environments. The products support automated plant care functions and reinforce LG’s expansion into lifestyle agriculture solutions. Source: www.lg.com

December 2025 Click & Grow strengthened consumer adoption of automated indoor gardening through continued expansion of its Smart Garden product ecosystem, featuring automated lighting, watering, and nutrient delivery. The platform supports simplified cultivation for urban households and improves accessibility for beginner growers. Source: www.clickandgrow.com

December 2024 LG Electronics showcased an indoor garden lamp concept designed to grow up to 20 plants with automated watering, nutrient control, and ThinQ connectivity. The innovation demonstrated a shift toward multifunctional smart-home agriculture products. Source: www.theverge.com

October 2024 AeroGarden announced operational changes affecting its product ecosystem as the company prepared to wind down operations, highlighting consolidation pressure among smart gardening brands and creating opportunities for alternative providers to strengthen market positions. Source: gardening community reports and market discussions.

The Smart Indoor Garden System Market Report provides comprehensive coverage across product types including hydroponic, aeroponic, aquaponic, and soil-based smart gardening systems. The report analyzes applications spanning residential cultivation, commercial farming, hospitality, education, and institutional environments, along with end-user adoption patterns across households, businesses, and controlled-environment agriculture operators.

The study evaluates key technologies such as AI monitoring, IoT sensors, automated irrigation, LED lighting, and cloud-based cultivation platforms across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. With analysis of leading companies, competitive positioning, deployment trends, and emerging innovation areas, the report supports investment planning, market expansion strategies, technology prioritization, and competitive decision-making through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 135.0 Million |

| Market Revenue (2033) | USD 379.7 Million |

| CAGR (2026–2033) | 13.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | LG Electronics; Click & Grow; Gardyn; Rise Gardens; AeroGarden; iDOO; LetPot; VegeBox; Back to the Roots; Smart Garden Products; Plantui; Veritable |

| Customization & Pricing | Available on Request (10% Customization Free) |