Reports

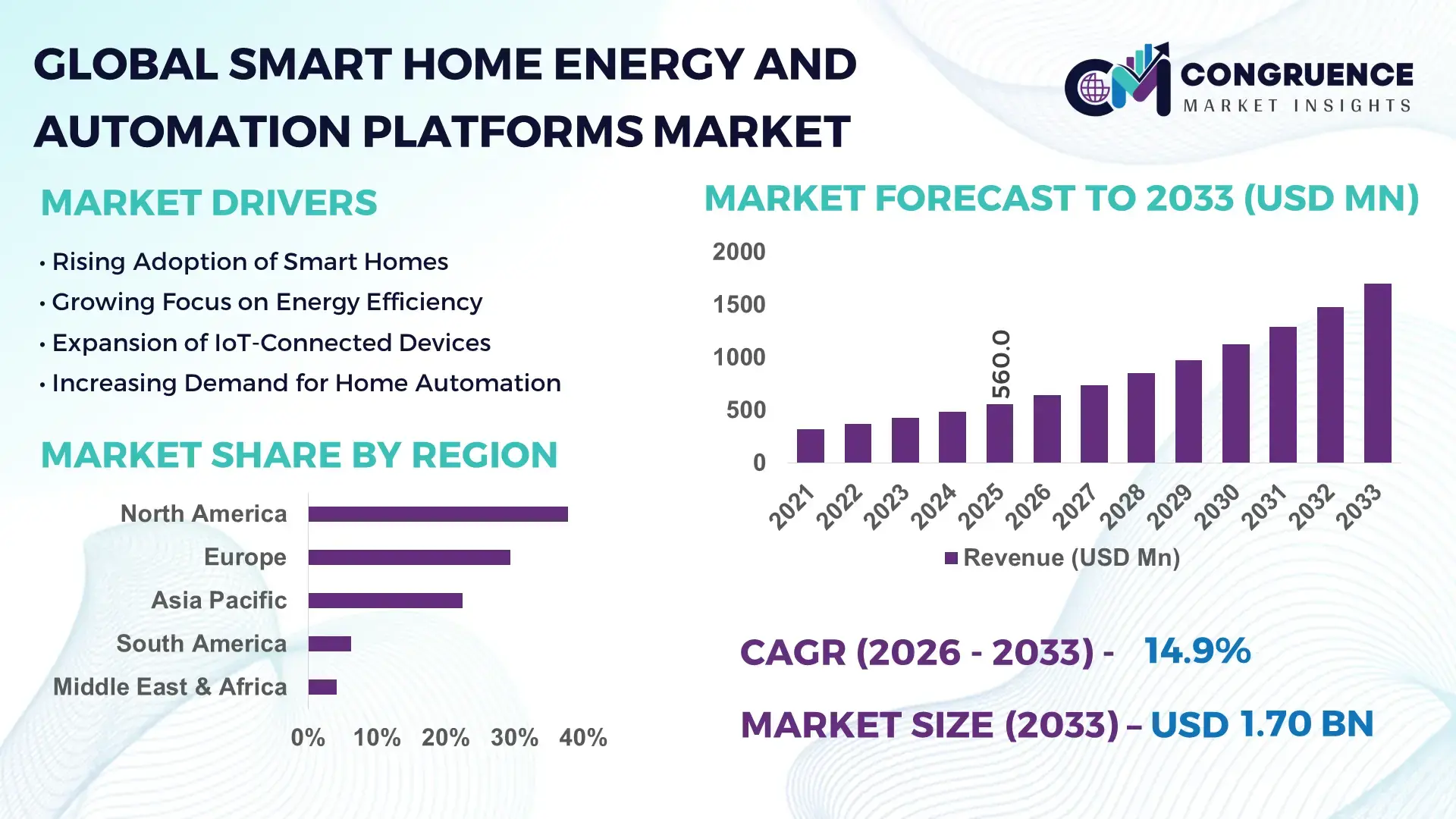

The Global Smart Home Energy and Automation Platforms Market was valued at USD 560.0 Million in 2025 and is anticipated to reach a value of USD 1,701.2 Million by 2033 expanding at a CAGR of 14.90% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth of this market is primarily driven by rising adoption of connected home technologies that enable real-time energy monitoring, automated appliance control, and optimized electricity consumption across residential environments.

The United States remains a central hub for smart home energy and automation platforms due to its advanced digital infrastructure, large-scale consumer adoption, and strong technology ecosystem. More than 63 million U.S. households use at least one smart home device connected to an energy management or automation platform. Utility companies across 35+ states have implemented demand-response programs that integrate with smart thermostats and automation hubs to manage peak electricity demand. The country has also witnessed over USD 2.8 billion in investments in residential energy technology startups since 2021, supporting innovations in AI-driven home energy optimization, smart meters, and distributed energy integration. In addition, around 48% of new residential constructions in the U.S. incorporate pre-installed smart home automation systems, enabling energy usage monitoring, appliance scheduling, and integration with rooftop solar and battery storage systems.

Market Size & Growth: The market was valued at USD 560.0 Million in 2025 and is projected to reach USD 1,701.2 Million by 2033, expanding at 14.90% CAGR, driven by the increasing adoption of connected home ecosystems that enable automated energy optimization and cost savings.

Top Growth Drivers: Rapid smart device adoption (+52% households using connected devices), energy efficiency improvements through automation (up to 30% reduction in household energy consumption), and smart thermostat penetration (40% adoption in developed economies).

Short-Term Forecast: By 2028, AI-powered automation platforms are expected to improve home energy efficiency by 25% while reducing electricity bills by 18% through predictive appliance scheduling and dynamic load balancing.

Emerging Technologies: AI-driven home energy analytics, IoT-enabled smart meters, and edge-based automation controllers that process device-level energy consumption data in real time.

Regional Leaders: North America projected to exceed USD 720 Million by 2033 driven by strong smart thermostat adoption; Europe expected to reach USD 510 Million supported by green building regulations; Asia-Pacific projected to surpass USD 360 Million due to rapid urban smart-home deployments.

Consumer/End-User Trends: Residential homeowners represent the largest user base, with over 58% of smart home device owners integrating energy automation platforms to manage lighting, HVAC, and appliance scheduling via mobile apps and voice assistants.

Pilot or Case Example: In 2024, a residential energy automation pilot across 12,000 homes demonstrated 22% reduction in peak electricity demand using AI-based load management systems integrated with smart thermostats.

Competitive Landscape: The market leader holds approximately 21% share, followed by key competitors including major smart home ecosystem providers and home automation platform developers with strong IoT integration capabilities.

Regulatory & ESG Impact: Energy efficiency mandates and smart grid initiatives across 40+ countries are encouraging adoption of home automation systems that support carbon reduction and electricity demand management.

Investment & Funding Patterns: Over USD 4.5 billion has been invested globally in smart home energy technologies and connected residential infrastructure since 2020, with growing venture funding for AI-based home energy optimization startups.

Innovation & Future Outlook: Integration of home automation platforms with rooftop solar, battery storage, and electric vehicle charging systems is expected to create fully autonomous residential energy ecosystems over the next decade.

Smart home energy and automation platforms are increasingly integrated across residential energy management, HVAC control, smart lighting, and distributed energy resources. Residential energy management contributes nearly 46% of platform adoption, while smart appliance integration accounts for approximately 27%. Advances in AI-driven predictive energy analytics and IoT connectivity are enabling real-time optimization of household electricity consumption. Strong regulatory focus on energy efficiency and decarbonization is also accelerating adoption across developed and emerging economies.

The Smart Home Energy and Automation Platforms Market has become strategically significant as energy efficiency, digital connectivity, and sustainable residential infrastructure increasingly intersect. Governments and utility providers are emphasizing smart energy ecosystems that allow households to actively participate in energy optimization and demand-response programs. Advanced automation platforms now integrate lighting, HVAC systems, appliances, solar panels, and battery storage into a unified digital environment that allows homeowners to monitor and optimize electricity consumption in real time.

Technological innovation is a central component shaping the future trajectory of this market. AI-based predictive energy management delivers nearly 35% improvement in electricity optimization compared to traditional programmable thermostats, enabling automated appliance scheduling and real-time load balancing. In addition, edge computing controllers embedded in smart hubs can process energy usage data locally, reducing latency and improving responsiveness across connected devices.

Regional dynamics also highlight the evolving landscape of this market. North America dominates in deployment volume due to high smart device penetration, while Europe leads in adoption rates with nearly 44% of new homes integrating smart energy systems as part of sustainable housing initiatives. Asia-Pacific is emerging rapidly as urban smart housing projects accelerate across countries such as China, Japan, and South Korea.

In the short term, digital transformation will further expand the market. By 2028, AI-driven home energy optimization platforms are expected to reduce household electricity consumption by nearly 20%, driven by predictive energy analytics and integration with smart grid infrastructure. Environmental commitments are also influencing corporate and government policies. Firms and technology providers are committing to 30–40% energy efficiency improvements in residential buildings by 2030 through automation, demand-response integration, and renewable energy management.

Practical results from pilot programs illustrate the effectiveness of such technologies. In 2024, a large-scale residential automation initiative in the United States achieved a 21% reduction in peak electricity demand through AI-powered energy scheduling integrated with smart thermostats and appliance controllers. Such results demonstrate how intelligent automation platforms can significantly reduce grid strain and household electricity costs.

As connected home technologies continue to evolve, the Smart Home Energy and Automation Platforms Market is positioned as a key pillar supporting energy resilience, regulatory compliance, and sustainable digital infrastructure across modern residential environments.

The Smart Home Energy and Automation Platforms Market is evolving rapidly as residential infrastructure becomes increasingly digital and energy-efficient. The market is influenced by a combination of technological innovation, sustainability goals, and growing consumer demand for connected living environments. Smart platforms integrate IoT devices, sensors, energy meters, and automation software to provide centralized control of home systems such as lighting, HVAC, security, and appliances. This integration enables homeowners to monitor and optimize electricity consumption while enhancing comfort and operational efficiency.

Energy efficiency regulations and smart grid deployments are also reshaping market dynamics. Governments across multiple regions are implementing policies that encourage adoption of smart energy technologies within residential buildings. The expansion of renewable energy installations such as rooftop solar systems is further accelerating demand for platforms capable of managing distributed energy resources. Additionally, the rising number of connected households worldwide—expected to surpass 500 million smart homes by the end of the decade—is creating strong demand for unified automation platforms capable of integrating diverse devices and energy systems.

The rapid proliferation of connected devices within residential environments is a primary driver of the Smart Home Energy and Automation Platforms Market. Smart thermostats, lighting systems, intelligent appliances, and energy monitoring devices are increasingly integrated into centralized automation platforms that provide unified control and energy optimization. Studies indicate that households equipped with smart thermostats and automated lighting systems can reduce energy consumption by 20–30%, encouraging wider adoption among homeowners seeking cost savings and sustainability benefits. Additionally, the global installed base of IoT-enabled residential devices exceeded 14 billion units, creating a substantial ecosystem that requires integrated automation platforms for effective management. Smart energy platforms enable real-time data analytics, remote device management, and predictive energy scheduling, allowing households to automate electricity usage during off-peak hours and reduce energy waste. These capabilities have significantly improved residential energy efficiency while enhancing convenience and user engagement.

Despite strong growth potential, the Smart Home Energy and Automation Platforms Market faces challenges related to installation complexity and compatibility between devices from different manufacturers. Many smart homes operate devices using diverse communication protocols such as Wi-Fi, Zigbee, Z-Wave, and Bluetooth, which can create integration difficulties for consumers attempting to unify devices under a single platform. Surveys show that nearly 38% of homeowners encounter connectivity or compatibility issues when integrating multiple smart devices within the same ecosystem. Additionally, installation and configuration often require specialized technical expertise, increasing deployment costs and limiting adoption among non-technical users. Security concerns also remain a critical barrier, as connected devices may expose households to cybersecurity risks if platforms are not properly secured. These challenges can discourage consumers from fully adopting automation platforms despite the potential benefits associated with energy management and operational efficiency.

The rapid expansion of distributed renewable energy systems such as rooftop solar panels and residential battery storage presents significant opportunities for the Smart Home Energy and Automation Platforms Market. Modern automation platforms are increasingly designed to integrate with solar inverters, energy storage systems, and electric vehicle charging stations, allowing households to manage electricity production and consumption dynamically. Residential solar installations worldwide have surpassed 40 million systems, creating strong demand for platforms capable of optimizing energy flows between solar generation, storage batteries, and household appliances. Automation platforms can schedule energy-intensive tasks such as washing or EV charging during periods of high solar generation, improving energy utilization and reducing reliance on grid electricity. In addition, utilities are launching virtual power plant programs that aggregate thousands of connected homes to balance electricity demand, offering financial incentives for households participating through automation platforms.

Data privacy and cybersecurity concerns represent a major challenge for the Smart Home Energy and Automation Platforms Market. Automation platforms collect significant amounts of data related to household energy consumption, device usage patterns, and occupancy behaviors, which could potentially be exploited if not properly protected. Reports indicate that over 25% of connected home devices have experienced some form of attempted cyber intrusion, highlighting vulnerabilities within IoT ecosystems. As smart homes integrate more connected devices and automation capabilities, the number of potential entry points for cyberattacks increases. Unauthorized access to automation platforms could allow malicious actors to manipulate home systems, disrupt energy management operations, or access sensitive personal data. Addressing these concerns requires stronger encryption standards, secure authentication mechanisms, and continuous software updates to ensure that platforms maintain robust protection against evolving cybersecurity threats.

Rapid Expansion of AI-Driven Energy Optimization Systems: Artificial intelligence is transforming residential energy management by enabling predictive automation across connected devices. AI-based platforms can analyze historical consumption patterns from over 200 household data points including appliance usage, temperature preferences, and occupancy behavior. Smart homes equipped with AI-enabled energy management systems have demonstrated energy savings of up to 28% through automated load shifting and device scheduling. In addition, nearly 42% of newly installed smart home hubs in developed markets now include embedded AI energy analytics, allowing systems to automatically adjust HVAC settings, lighting levels, and appliance operations to minimize electricity consumption.

Integration of Home Energy Platforms with Solar and Battery Systems: The increasing deployment of residential solar panels and battery storage solutions is driving integration with smart home automation platforms. Globally, more than 35 million homes are equipped with rooftop solar systems, and around 22% of these installations are connected to smart automation platforms that manage electricity flows between generation, storage, and consumption. Integrated platforms allow households to prioritize solar power usage during daytime hours and store excess energy for later consumption. This capability has helped some smart homes reduce reliance on grid electricity by up to 40%, particularly in regions with high renewable energy adoption.

Growth in Voice-Controlled and Mobile-Based Energy Automation: Consumer interaction with home automation platforms is evolving through voice assistants and mobile applications. Approximately 65% of smart home device users control their automation systems through smartphone apps, while over 45% rely on voice assistants for device commands and energy monitoring. Voice-controlled automation enables quick adjustments to lighting, temperature, and appliance operations without manual configuration. The integration of conversational AI into home energy systems has also improved accessibility for elderly and disabled users, enabling seamless interaction with connected household technologies.

Increasing Deployment in Smart Residential Communities: Large-scale residential developments are increasingly incorporating automation platforms as part of smart community infrastructure. Around 48% of new residential construction projects in North America and Europe include integrated smart home automation systems, allowing centralized management of energy usage, lighting, and security. Developers report that smart energy platforms can reduce building energy consumption by 18–22% through automated HVAC management and intelligent lighting systems. Smart residential communities are also integrating shared energy resources such as community solar installations, enabling collective energy optimization across hundreds of connected homes.

The Smart Home Energy and Automation Platforms Market is segmented based on platform type, application areas, and end-user adoption patterns. These segments reflect how different technologies and consumer needs shape the deployment of smart home energy systems. Platform types typically vary based on the scope of automation capabilities, ranging from energy monitoring tools to fully integrated home automation ecosystems. Applications span across multiple household functions including lighting management, heating and cooling optimization, appliance automation, and energy monitoring. End-user segmentation highlights the role of residential homeowners, property developers, and utility providers in driving market adoption. Increasing integration of connected devices, renewable energy systems, and AI-driven analytics is also influencing how these segments evolve. As smart home adoption continues to expand globally, segmentation trends reveal growing demand for platforms capable of integrating multiple energy technologies and providing centralized management of residential energy systems.

The Smart Home Energy and Automation Platforms Market includes several platform categories designed to manage and optimize residential energy usage and automation functions. Comprehensive Home Automation Platforms represent the leading segment, accounting for approximately 41% of platform adoption, as these systems integrate lighting, HVAC, appliance control, security systems, and energy monitoring into a unified interface. Their dominance is driven by consumer demand for centralized control over multiple connected devices through a single application or hub. Energy Management Platforms are the fastest-growing type, expanding at an estimated 17.8% growth rate, driven by increasing consumer awareness of electricity consumption and the rising adoption of smart meters and demand-response technologies. These platforms primarily focus on monitoring energy usage patterns and optimizing appliance schedules to reduce electricity consumption and utility costs. Other platform types include Device-Specific Automation Platforms and Cloud-Based Energy Analytics Platforms, which together account for roughly 34% of adoption. These platforms are typically used for targeted functions such as smart thermostat control or appliance-level monitoring, often integrated with larger automation ecosystems.

• In 2025, a major university research initiative deployed AI-driven home energy management platforms across a smart residential testbed of 1,000 connected homes, enabling automated energy scheduling that reduced peak electricity consumption by 23%.

Applications of smart home energy and automation platforms extend across several household energy management functions. HVAC and Climate Control Automation currently accounts for approximately 38% of platform applications, as heating and cooling systems represent one of the largest sources of residential energy consumption. Automated climate control systems can adjust temperature settings dynamically based on occupancy patterns, improving comfort while minimizing energy waste. Smart Appliance Automation is emerging as the fastest-growing application segment with an estimated 18.6% growth rate, supported by the increasing availability of IoT-enabled household appliances such as washing machines, refrigerators, and dishwashers that can be programmed to operate during off-peak electricity periods. Other applications include Smart Lighting Management, Energy Consumption Monitoring, and Security System Integration, which together contribute around 44% of platform usage across residential environments. These applications allow homeowners to automate lighting schedules, monitor real-time energy usage, and coordinate home security systems within a single platform. Consumer adoption is rising rapidly. In 2025, nearly 46% of smart home users reported using automation platforms primarily for energy monitoring and appliance scheduling, while over 52% preferred mobile-app-based control of home automation systems.

• In 2024, a large-scale residential pilot program implemented smart automation platforms in more than 10,000 homes, enabling real-time HVAC optimization and reducing household electricity consumption by 19%.

End-user adoption in the Smart Home Energy and Automation Platforms Market is dominated by residential homeowners, property developers, and utility providers. Residential Homeowners represent the largest end-user segment with approximately 62% of platform adoption, driven by increasing demand for convenience, energy efficiency, and connected living experiences. Homeowners are integrating automation platforms with smart thermostats, lighting systems, and appliance controls to reduce electricity consumption and manage household devices remotely. Real Estate Developers and Smart Housing Projects represent the fastest-growing end-user segment, expanding at an estimated 16.5% growth rate, as new residential developments increasingly incorporate built-in automation platforms and connected energy management systems. Developers are deploying integrated automation hubs to enhance property value and attract technology-oriented homebuyers. Other end-users include Utility Companies and Energy Service Providers, which collectively account for approximately 23% of adoption. These organizations use smart home automation platforms to implement demand-response programs and optimize electricity distribution across residential networks. Consumer behavior also highlights strong adoption trends. In 2025, more than 40% of smart home device owners globally reported integrating their devices into centralized automation platforms, while over 58% expressed interest in platforms that can automatically optimize household energy consumption.

• In 2025, a national smart-grid initiative connected more than 50,000 households to an automated energy management platform, enabling utilities to balance electricity demand while helping households reduce peak energy consumption by 20%.

North America accounted for the largest market share at 37.8% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a 16.2% CAGR between 2026 and 2033.

North America’s strong position is supported by the presence of over 65 million smart homes, high penetration of IoT devices, and large-scale integration of smart thermostats and energy management hubs. Europe follows with approximately 29.4% market share, driven by stringent building efficiency directives and rising demand for sustainable residential infrastructure. The Asia-Pacific region is rapidly expanding due to urban housing development and smart city initiatives, with over 120 million connected households expected to adopt automation platforms within the next decade. Meanwhile, South America holds nearly 6.3% share, while the Middle East & Africa collectively contribute about 4.1% of global demand. Across regions, more than 58% of new residential developments are incorporating at least one smart automation feature, while around 43% of consumers use mobile applications to monitor and control household energy consumption. Government incentives for smart grid participation and residential solar integration are also expanding the addressable market for energy automation platforms.

North America represents the most mature ecosystem for smart home energy and automation platforms, accounting for nearly 37.8% of global market adoption. The region’s demand is driven primarily by residential smart energy management, home security integration, and automated HVAC control. More than 63 million households use at least one connected home automation device, while nearly 41% of homeowners integrate multiple IoT devices through centralized automation platforms. Government initiatives promoting energy efficiency, including tax incentives for energy-efficient home upgrades and smart thermostat adoption, have significantly supported technology deployment. Advanced digital infrastructure and strong broadband penetration exceeding 92% household coverage enable seamless connectivity of smart devices. Local technology innovators are also actively expanding the ecosystem. For example, Resideo Technologies has expanded its intelligent thermostat ecosystem to integrate with over 30 different smart home device categories, allowing unified energy optimization and device management. Consumer behavior in the region shows high willingness to adopt integrated home ecosystems, with more than 52% of homeowners prioritizing energy monitoring and automated climate control systems as part of their smart home upgrades.

Europe accounts for approximately 29.4% of global adoption in the Smart Home Energy and Automation Platforms Market, supported by strong regulatory frameworks and sustainability goals. Countries such as Germany, the United Kingdom, and France represent the largest deployment centers, collectively contributing over 60% of the region’s installed smart home automation platforms. The European Union’s building efficiency initiatives require residential buildings to implement energy monitoring and management solutions to reduce carbon emissions. As a result, nearly 47% of new residential developments in Western Europe incorporate smart energy monitoring systems. Technological innovation is also accelerating, with IoT-based energy sensors and AI-enabled home automation hubs gaining traction across urban housing developments. Several regional technology firms are actively developing interoperable automation ecosystems. For example, Schneider Electric has expanded its smart home energy solutions across multiple European countries, enabling integrated control of lighting, heating, and renewable energy systems. Consumer behavior patterns in the region highlight strong sustainability awareness, with over 56% of European homeowners prioritizing energy-efficient technologies when upgrading residential infrastructure.

Asia-Pacific ranks as the fastest-expanding region in the Smart Home Energy and Automation Platforms Market and accounts for nearly 22.4% of global adoption. Major consumption centers include China, Japan, and India, which collectively represent more than 70% of regional installations. Rapid urbanization and large-scale residential construction are driving the deployment of smart home infrastructure across metropolitan regions. In China alone, more than 40 million households are estimated to use connected home devices integrated with automation platforms. Japan has also introduced smart energy management programs across residential communities, enabling automated energy scheduling and grid participation. The region has become a global manufacturing hub for smart home components such as IoT sensors, automation hubs, and connected appliances, producing nearly 45% of the world’s smart home hardware. Companies such as Samsung SmartThings continue to expand platform ecosystems to integrate appliances, lighting, and home energy devices. Consumer behavior across Asia-Pacific shows strong mobile-centric adoption, with more than 60% of users controlling smart home devices through smartphone apps and cloud platforms, reflecting the region’s digital lifestyle trends.

South America accounts for around 6.3% of global demand in the Smart Home Energy and Automation Platforms Market. The region’s growth is primarily concentrated in Brazil and Argentina, where increasing urban housing projects and rising electricity costs are encouraging households to adopt energy monitoring technologies. Brazil alone represents nearly 58% of regional installations, supported by government energy-efficiency programs promoting smart meters and connected home devices. Residential electricity consumption monitoring has become a key driver of adoption, with more than 18% of urban households using at least one connected home energy device. Infrastructure improvements in broadband connectivity and mobile internet penetration—now exceeding 74% across urban areas—are enabling broader deployment of IoT-based home automation systems. Local technology integrators are also expanding partnerships with international platform providers to deploy smart residential ecosystems. Consumer behavior in the region shows increasing interest in energy cost optimization, with over 46% of homeowners adopting automation primarily for electricity monitoring and lighting control.

The Middle East & Africa region accounts for approximately 4.1% of global market demand but is steadily expanding as smart city and sustainable housing initiatives gain momentum. Key markets include the United Arab Emirates, Saudi Arabia, and South Africa, where smart residential infrastructure is being integrated into urban development projects. In the Gulf region alone, more than 30 large-scale smart city developments are incorporating connected home technologies and energy automation platforms into residential buildings. Government initiatives promoting energy efficiency in buildings have encouraged the deployment of intelligent HVAC and lighting control systems. The construction sector remains a major driver of adoption, particularly in newly developed smart communities that integrate digital infrastructure from the planning stage. Regional technology adoption is also supported by high smartphone penetration exceeding 80% in several Gulf countries, enabling mobile-based automation control. Consumer behavior patterns indicate growing interest in convenience and security, with over 44% of smart home adopters using automation platforms primarily for climate control and energy monitoring.

United States – 32.6% Market Share: High penetration of smart home devices, advanced IoT infrastructure, and strong adoption of residential energy management technologies support leadership.

China – 19.8% Market Share: Large-scale urban housing development and rapid growth in connected home ecosystems are accelerating the adoption across residential communities.

The Smart Home Energy and Automation Platforms Market is characterized by a moderately fragmented competitive structure, with more than 70 active technology providers and platform developers operating globally. The market features a mix of large multinational technology companies, smart home ecosystem providers, and specialized energy management platform developers. The top five companies collectively account for approximately 42–46% of global market presence, reflecting strong competition but also increasing consolidation around large digital ecosystems.

Major players are focusing on expanding interoperability across connected devices, allowing consumers to integrate multiple IoT products within unified automation platforms. Strategic partnerships between device manufacturers, software providers, and energy utilities have become increasingly common. For instance, technology companies are collaborating with energy providers to enable demand-response programs that connect thousands of households through smart automation platforms.

Product innovation remains a central competitive strategy. Companies are integrating AI-based predictive analytics, edge computing controllers, and voice-enabled automation into their platforms to enhance user experience and energy optimization capabilities. The introduction of open connectivity standards has also intensified competition, allowing third-party device manufacturers to integrate with existing platforms. Additionally, mergers and acquisitions have accelerated as technology firms seek to strengthen their smart home ecosystems and expand into residential energy management solutions.

Investments in research and development continue to grow, with several companies allocating over 8–12% of technology budgets toward IoT and smart home automation innovation. As smart home adoption expands globally, companies that provide highly interoperable, secure, and AI-enabled energy automation platforms are expected to gain a competitive advantage in the evolving market landscape.

Schneider Electric

Samsung Electronics

Google LLC

Amazon.com Inc.

Apple Inc.

Siemens AG

Johnson Controls International

ABB Ltd.

Resideo Technologies Inc.

Legrand SA

Lutron Electronics Co., Inc.

Crestron Electronics, Inc.

Control4 Corporation

Bosch Smart Home GmbH

Technological innovation plays a central role in shaping the Smart Home Energy and Automation Platforms Market as residential environments become increasingly digital and interconnected. Modern automation platforms rely on Internet of Things (IoT) infrastructure, enabling communication between sensors, appliances, thermostats, lighting systems, and centralized control hubs. The average connected home now contains 10–15 IoT devices, generating large volumes of operational data that automation platforms analyze to optimize household energy usage.

Artificial intelligence and machine learning technologies are transforming how home automation platforms manage electricity consumption. AI algorithms analyze patterns such as occupancy behavior, weather conditions, and appliance usage to predict energy demand and automatically adjust device settings. Smart thermostats equipped with AI-driven learning capabilities can reduce heating and cooling energy consumption by 15–25% through predictive climate control.

Edge computing is another critical advancement enabling faster decision-making within smart home ecosystems. Instead of relying entirely on cloud infrastructure, edge-enabled automation hubs process energy data locally, reducing latency and improving device responsiveness. This capability is particularly valuable in homes with 20+ connected devices, where real-time coordination between appliances is necessary for effective automation.

Interoperability standards are also evolving rapidly. Connectivity protocols such as Matter, Zigbee, Z-Wave, and Thread are improving compatibility between devices from different manufacturers. The adoption of universal standards allows homeowners to integrate smart lighting, energy meters, security systems, and appliances within a single platform interface. By 2025, more than 200 technology companies had adopted cross-platform interoperability frameworks to enable seamless device integration.

Emerging technologies are also expanding the scope of smart home energy platforms. Integration with residential solar systems, battery storage units, and electric vehicle charging infrastructure allows automation platforms to manage distributed energy resources within households. In homes equipped with rooftop solar panels and battery storage, automation platforms can optimize electricity usage and store excess power, reducing grid reliance by up to 35% during peak demand periods. These technological developments are positioning automation platforms as the digital backbone of next-generation smart residential ecosystems.

• In July 2025, Samsung introduced an AI-powered Routine Creation Assistant for its SmartThings platform, enabling users to create smart home automations through natural language commands such as scheduling lights or appliances based on daily routines. The update simplifies automation setup and enhances user adoption of energy-efficient device scheduling. Source: www.samsung.com

• In April 2025, Samsung expanded SmartThings compatibility with the Matter 1.4 standard, enabling integration with energy-related devices including water heaters, heat pumps, solar energy systems, and battery storage units. The update improves cross-platform device interoperability and supports broader home energy management capabilities.

• In June 2025, Apple introduced the EnergyKit framework for its Apple Home ecosystem, allowing developers to access residential energy data and create applications that optimize electricity usage across smart thermostats, appliances, and electric vehicle charging systems within smart homes.

• In March 2025, Samsung expanded its SmartThings Flex Connect demand-response program to additional U.S. regions, enabling connected households to automatically reduce electricity consumption during peak grid demand events while earning incentives through the SmartThings Energy platform.

The Smart Home Energy and Automation Platforms Market Report provides a comprehensive analysis of the global ecosystem supporting connected residential energy management and digital home automation technologies. The report examines market developments across multiple dimensions including technology platforms, applications, end-user segments, and geographic regions. It evaluates more than 20 key technology categories, including IoT sensors, automation hubs, AI-driven energy management software, smart thermostats, connected appliances, and integrated home control platforms.

The scope includes segmentation across platform types such as comprehensive home automation systems, energy management platforms, and cloud-based analytics tools. Applications covered in the report span across residential climate control, lighting automation, appliance management, energy monitoring, and home security integration. The report also analyzes adoption trends among various end-user groups including homeowners, property developers, utilities, and smart housing infrastructure providers.

Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting variations in technology adoption, infrastructure readiness, and consumer behavior patterns. The report evaluates market penetration across more than 25 major countries, including the United States, China, Germany, Japan, India, and Brazil. In addition to regional insights, the report assesses the impact of emerging technologies such as AI-enabled predictive energy analytics, edge computing-based automation hubs, and interoperability frameworks designed to connect multiple smart home devices.

Furthermore, the report examines the evolving role of smart home automation platforms in supporting sustainable energy ecosystems. Integration with renewable energy systems, battery storage, and electric vehicle charging infrastructure is analyzed to highlight how connected homes are becoming active participants in modern energy networks. With increasing digitalization of residential infrastructure and rising consumer demand for energy efficiency, the report outlines the expanding technological and operational scope shaping the Smart Home Energy and Automation Platforms Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 560.0 Million |

| Market Revenue (2033) | USD 1,701.2 Million |

| CAGR (2026–2033) | 14.90% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Honeywell International Inc.; Schneider Electric; Samsung Electronics; Google LLC; Amazon.com Inc.; Apple Inc.; Siemens AG; Johnson Controls International; ABB Ltd.; Resideo Technologies Inc.; Legrand SA; Lutron Electronics Co., Inc.; Crestron Electronics, Inc.; Bosch Smart Home GmbH |

| Customization & Pricing | Available on Request (10% Customization Free) |